- Automation & Robotics

- Advanced Process Control Market

Advanced Process Control Market Size, Share, and Growth Forecast, 2026 - 2033

Advanced Process Control Market by Technology (Advanced Regulatory Control, Multivariable Model Predictive Control, Others), Component (Software, Services, Others), End-user Industry, Enterprise Size, and Regional Analysis for 2026 - 2033

Advanced Process Control Market Size and Trends Analysis

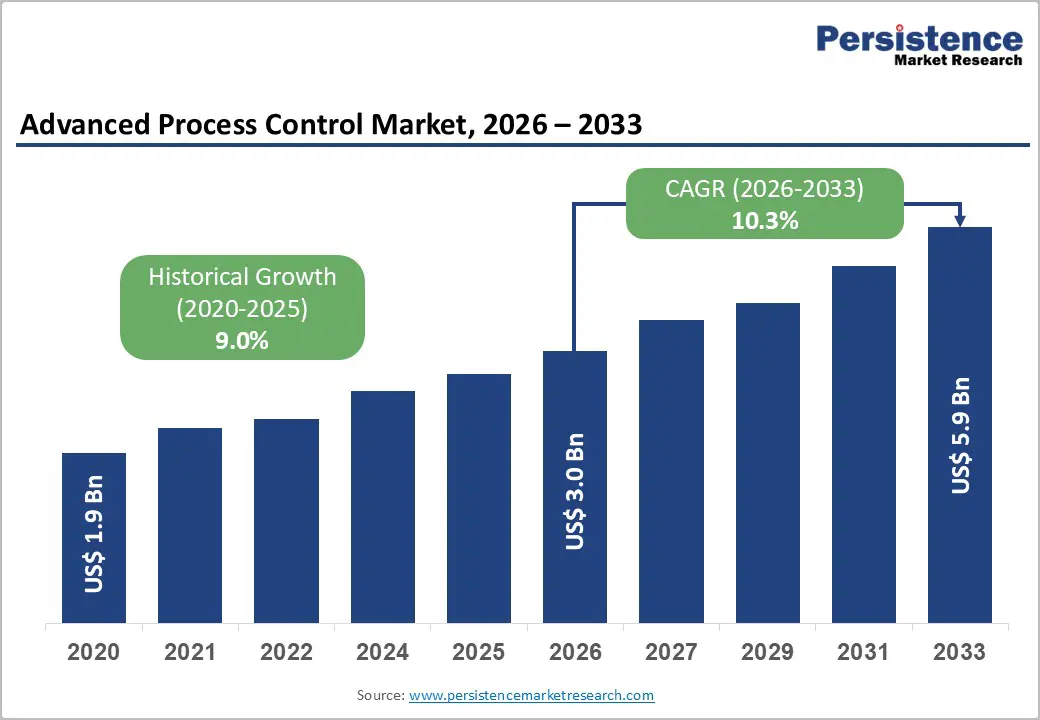

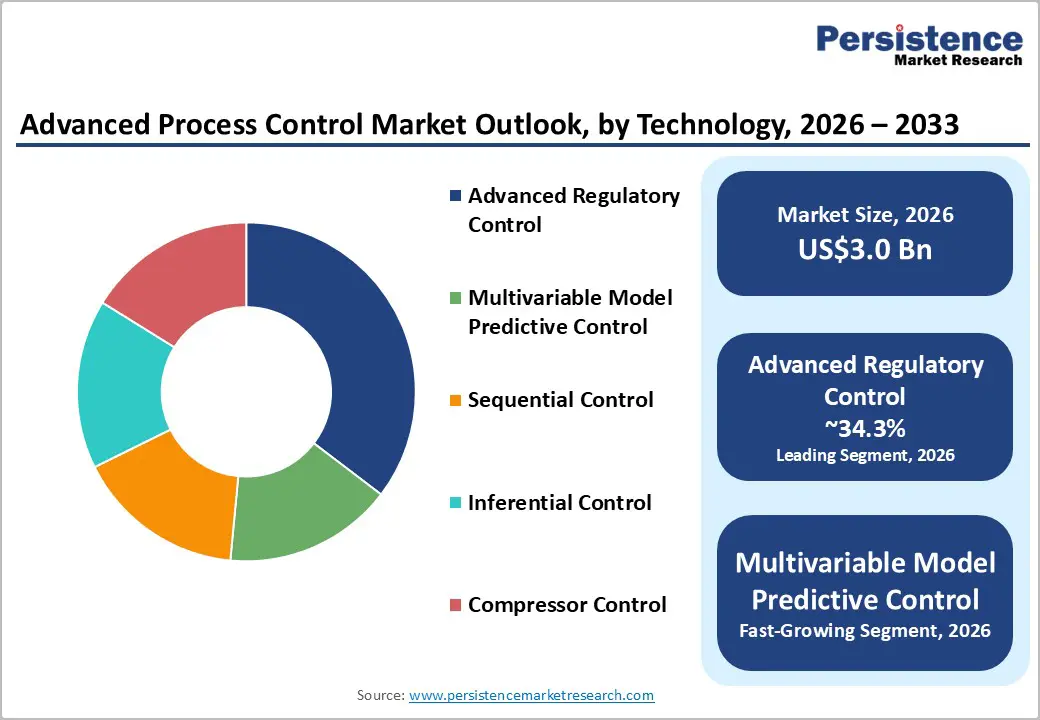

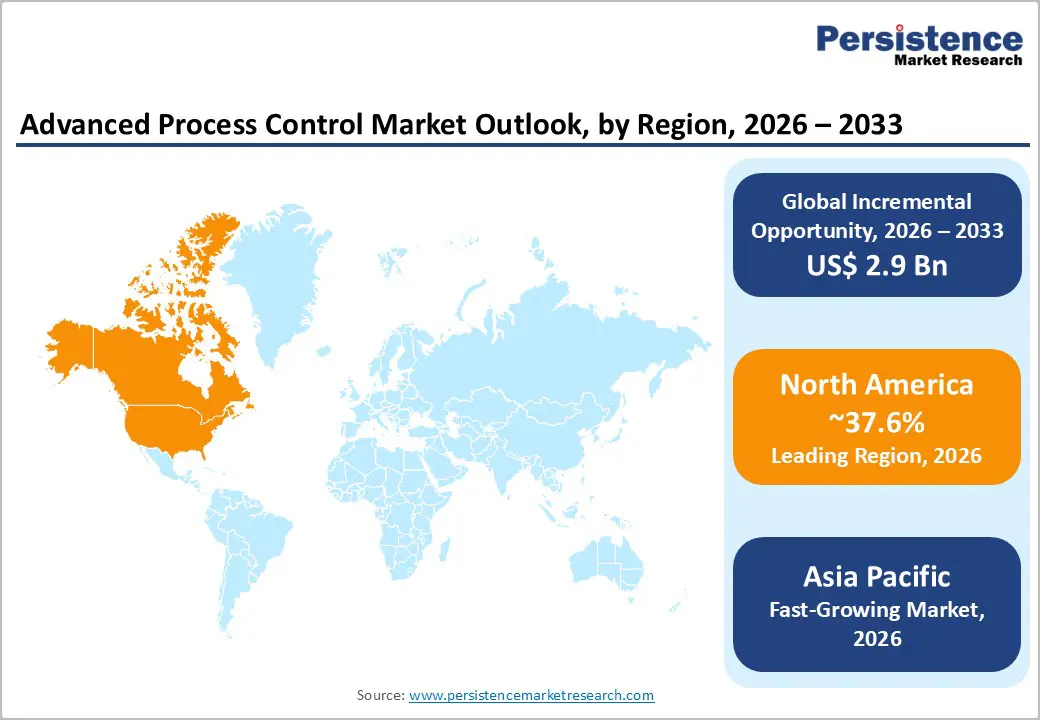

The global advanced process control market size is likely to be valued at US$3.0 billion in 2026 and is expected to reach US$5.9 billion by 2033, growing at a CAGR of 10.3% between 2026 and 2033, driven by increasing adoption of software-led optimization tools, stricter regulatory compliance requirements for emissions and quality, and the integration of AI-enabled industrial workflows.

Advanced process control (APC) is evolving into a critical operational layer that enhances throughput, improves yield, and reduces energy consumption across process industries. The shift toward data-driven manufacturing and autonomous control systems is reinforcing APC’s role as a strategic investment rather than a discretionary upgrade.

Key Industry Highlights:

- Leading Region: North America is projected to account for approximately 37.6% of the market share, supported by strong industrial automation adoption and advanced digital infrastructure.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rapid industrialization, smart manufacturing investments, and increasing adoption of automation technologies.

- Investment Plans: Companies are prioritizing investments in AI-integrated APC platforms, cloud-based analytics, and digital twin technologies, with a growing shift toward software-defined control systems and lifecycle optimization services to enhance operational efficiency.

- Dominant Technology: Advanced regulatory control is expected to lead the technology segment with an anticipated share of 34.3%, due to its compatibility with existing systems and lower implementation complexity.

- Leading Component: The software segment is expected to dominate, holding an anticipated share of 45.6%, driven by increasing demand for real-time optimization, predictive analytics, and data-driven process control solutions.

DRO Analysis

Driver - Energy Efficiency and Emissions Optimization are Becoming Board-Level Priorities

Industrial sectors are under sustained pressure to reduce energy consumption, minimize waste, and enhance operational efficiency. Energy-intensive industries such as oil & gas, chemicals, and power generation face increasing scrutiny from regulatory bodies and stakeholders to improve sustainability performance. Digital technologies, including APC, enable real-time monitoring and predictive control of industrial processes, leading to measurable reductions in energy usage and emissions. Studies across industrial facilities show that digital optimization systems can deliver double-digit improvements in energy efficiency during early implementation phases.

APC systems directly support these objectives by optimizing process variables, reducing variability, and ensuring operations remain within optimal limits. As a result, APC is increasingly positioned as both a cost-saving and sustainability-enabling technology, making it a priority investment across large-scale industrial operations.

AI, IIoT, and Software-Defined Automation Are Expanding the Use Case for APC

The convergence of artificial intelligence, Industrial Internet of Things (IIoT), and cloud-edge computing is significantly broadening the application scope of APC systems. Modern manufacturing environments generate large volumes of real-time data from connected sensors and control systems. APC solutions leverage this data to predict process behavior, optimize control strategies, and automate decision-making.

The integration of AI-driven analytics enables predictive adjustments, reducing downtime and improving product quality. Vendors are embedding advanced algorithms and digital assistants into APC platforms, enabling operators to manage complex processes with greater precision and speed. This technological convergence is driving adoption across diverse industries, including refining, chemicals, pharmaceuticals, and energy systems, where operational efficiency and reliability are critical.

Restraint - High Implementation Complexity and Integration Costs Limit Adoption among Smaller Enterprises

Despite its benefits, APC deployment involves significant technical and financial challenges. Implementation requires integrating with distributed control systems (DCS), programmable logic controllers (PLC), and industrial data historians, as well as developing and validating process models. These requirements result in high upfront costs and extended deployment timelines. Smaller enterprises often lack the technical expertise and capital required to implement and maintain APC systems effectively.

In addition, legacy infrastructure in many facilities complicates integration, requiring extensive customization and system upgrades. Cybersecurity concerns and regulatory validation requirements further increase complexity, particularly in highly regulated industries. As a result, APC adoption remains concentrated among large enterprises with the resources to support long-term digital transformation initiatives.

Opportunity - Expansion into Pharmaceuticals and Specialty Manufacturing Creates High-Value Opportunities

The pharmaceutical and life sciences industries are increasingly adopting advanced digital manufacturing practices to improve product quality and compliance. APC aligns closely with regulatory frameworks that emphasize real-time process monitoring and control. In pharmaceutical manufacturing, maintaining consistent quality and minimizing batch failures are critical, making APC highly valuable.

The adoption of real-time analytics, digital quality management systems, and automated workflows is accelerating demand for APC solutions in biologics, sterile manufacturing, and specialty chemicals. This shift presents a significant growth opportunity for vendors to expand beyond traditional industries such as oil & gas and chemicals into high-margin, regulated sectors.

Emerging Markets Offer Strong Growth Potential through Industrial Modernization

Rapid industrialization and infrastructure development in emerging economies are creating favorable conditions for the adoption of APCs. Countries across Asia Pacific are investing heavily in advanced manufacturing technologies to enhance productivity and global competitiveness. New industrial facilities are being designed with digital capabilities, making them more compatible with APC systems.

In addition, governments are promoting smart manufacturing initiatives and the adoption of automation, further supporting market growth. The combination of greenfield projects and modernization of existing plants creates a substantial opportunity for APC vendors to expand their footprint in these regions. This trend is expected to drive sustained demand over the forecast period.

Category-wise Analysis

Technology Insights

Advanced Regulatory Control (ARC) is expected to lead, holding 34.3% market share in 2026, due to its compatibility with existing industrial control systems and its ability to deliver incremental performance improvements. ARC solutions enhance traditional PID control loops by improving stability, reducing process variability, and ensuring consistent output quality. Industries such as oil & gas, chemicals, and utilities rely heavily on ARC to maintain operational efficiency without requiring extensive system overhauls.

For example, ARC is widely deployed in refinery distillation columns to stabilize temperature and pressure fluctuations, ensuring optimal separation efficiency. In power plants, ARC helps maintain boiler and turbine stability under varying load conditions. Its relatively lower implementation complexity compared to advanced control techniques makes it a preferred choice for facilities operating with legacy infrastructure, particularly where quick return on investment and minimal disruption are critical.

Multivariable Model Predictive Control (MPC) is experiencing the fastest growth due to its ability to manage complex, multivariable processes with high precision. MPC uses dynamic process models to predict future behavior and optimize multiple control variables simultaneously in real time. This capability is especially valuable in industries with tightly coupled processes, such as petrochemicals, refining, and specialty chemicals.

For instance, MPC is commonly applied in catalytic cracking units and hydroprocessing systems to maximize yield while maintaining safety constraints. In the chemical industry, MPC helps optimize reactor conditions and minimize energy consumption. The integration of AI and advanced analytics further enhances MPC performance by enabling adaptive learning and predictive maintenance. As industries move toward higher levels of automation, digital twins, and autonomous operations, MPC adoption is expected to accelerate significantly due to its superior optimization capabilities.

Component Insights

The software segment is projected to dominate, accounting for 45.6% of the market share in 2026, as it forms the core of process optimization, control logic, and decision-making capabilities. APC software includes model development platforms, real-time optimization engines, simulation tools, and advanced analytics applications that enable continuous process improvement. The growing emphasis on digital transformation and data-driven operations is driving demand for advanced software solutions across industries.

For example, in chemical manufacturing, APC software is used to optimize reaction conditions and improve product consistency. In oil refineries, it enables real-time optimization of crude distillation and blending operations. Vendors are increasingly integrating AI, machine learning, and cloud-based deployment models into their software offerings, enhancing scalability and performance. This shift toward software-centric architectures reflects the evolution of industrial automation from hardware-driven systems to intelligent, data-driven platforms.

Services are projected to be the fastest-growing component segment due to the complexity of APC implementation, integration, and lifecycle management. These services include consulting, system design, model development, commissioning, operator training, and ongoing performance optimization. As organizations deploy APC solutions, they require continuous monitoring and periodic recalibration of models to maintain optimal performance. For instance, in pharmaceutical manufacturing, services are critical for validating process models and ensuring compliance with regulatory standards.

In oil & gas operations, service providers support real-time optimization and troubleshooting of complex control systems. The increasing adoption of remote monitoring, cloud-based support, and managed services is further accelerating demand. This trend is shifting the market toward recurring revenue models, where vendors provide long-term value through continuous optimization and performance enhancement rather than one-time system deployment.

Regional Insights

North America Advanced Process Control Market Trends - AI-Driven APC Expansion and Industrial Software Consolidation

North America is expected to lead the market with an estimated 37.6% share in 2026, driven by a mature industrial base and high adoption of advanced automation technologies. The U.S. is projected to account for approximately 55% of the regional market, supported by strong investments in industrial digitalization and process optimization. A notable development shaping the region is the acquisition of Aspen Technology, Inc. by Emerson Electric Co. in 2025, which significantly strengthened Emerson’s software-defined control capabilities. This move enables deeper integration of APC with advanced analytics and lifecycle optimization tools, accelerating adoption across refining and chemical operations.

Another important example is Honeywell International Inc. introducing AI-enabled assistants within its industrial software platforms. These tools allow operators to troubleshoot and optimize processes using natural language inputs, improving efficiency and reducing downtime. In parallel, Rockwell Automation, Inc. continues expanding its digital twin and analytics capabilities, enabling manufacturers to simulate and optimize processes before deployment. These developments are reinforcing North America’s leadership by accelerating the transition from traditional automation to intelligent, AI-driven APC systems. Investments remain focused on upgrading legacy infrastructure, deploying cloud-based analytics, and strengthening cybersecurity frameworks, ensuring sustained regional dominance.

Europe Advanced Process Control Market Trends - Sustainability-Led APC Adoption and Regulatory-Driven Optimization

Europe represents a significant APC market, supported by strong regulatory frameworks and advanced industrial infrastructure. Countries such as Germany, the United Kingdom, France, and Spain play a key role in driving regional growth. The emphasis on sustainability and emissions reduction is evident in initiatives led by Siemens AG, which has been actively integrating industrial AI and digital twin technologies into process industries. These solutions enable real-time optimization and energy efficiency improvements, aligning with Europe’s stringent environmental standards.

Similarly, Schneider Electric SE has expanded its EcoStruxure platform to include advanced process optimization and energy management capabilities, helping industrial facilities reduce carbon emissions while improving operational efficiency. ABB Ltd. has also been investing in digital control systems and APC solutions tailored for the chemical and energy industries, supporting predictive maintenance and real-time optimization.

In the U.K., AVEVA Group plc continues to enhance its industrial software portfolio, focusing on data integration and advanced analytics for process industries. These developments collectively strengthen Europe’s position as a compliance-driven market where APC adoption is closely tied to sustainability goals and regulatory requirements. The integration of APC with broader digital transformation initiatives is enabling companies to achieve both operational efficiency and environmental compliance.

Asia Pacific Advanced Process Control Market Trends - Rapid Industrialization and Smart Manufacturing-Driven APC Growth

Asia Pacific is likely to be the fastest-growing market, with a CAGR exceeding 11.6%. The region accounts for a significant share of global industrial production, with China, Japan, India, and ASEAN countries leading demand. Rapid industrialization and smart manufacturing initiatives are key drivers of growth. In China, large-scale refinery and petrochemical expansions are increasingly incorporating APC systems to optimize production and reduce energy consumption. Companies such as Yokogawa Electric Corporation are actively deploying advanced control solutions across Asian process industries, particularly in the energy and chemicals sectors.

Japan’s strong focus on precision manufacturing is supported by firms like Mitsubishi Electric Corporation, which is advancing factory automation and control technologies that integrate APC with robotics and AI. In India, industrial digitalization initiatives and investments in sectors such as pharmaceuticals and specialty chemicals are driving demand for APC solutions, with multinational vendors expanding their presence through partnerships and localized offerings.

ASEAN countries are also emerging as important markets due to supply chain diversification and increasing foreign direct investment in manufacturing. Regional expansions by companies like Honeywell International Inc. and Siemens AG are enabling broader adoption of cloud-based APC and smart factory solutions. These developments are transforming the Asia Pacific into a high-growth region where APC adoption is driven by both greenfield projects and the modernization of existing facilities, positioning it as a critical contributor to global market expansion.

Competitive Landscape

The global advanced process control market is moderately fragmented, with a mix of global automation providers and specialized software vendors. A core group of leading companies dominates large-scale deployments, leveraging strong technological capabilities and extensive industry experience. These companies compete on innovation, system integration, and service offerings. While competition is intense, high entry barriers and technical complexity limit the number of new entrants, maintaining a relatively stable competitive environment.

Key players are focusing on AI integration, platform-based solutions, and recurring revenue models. Strategic priorities include expanding software capabilities, strengthening service offerings, and targeting high-growth industries such as pharmaceuticals and specialty manufacturing. Companies are also leveraging partnerships and acquisitions to enhance technological capabilities and market reach.

Key Industry Developments:

- In March 2025, Emerson Electric Co. announced the successful completion of its acquisition of Aspen Technology, Inc., making AspenTech a wholly owned subsidiary and significantly strengthening Emerson’s advanced process control and industrial optimization software portfolio.

- In July 2025, Honeywell International Inc. completed the acquisition of Sundyne and announced the acquisition of Johnson Matthey’s Catalyst Technologies business, aiming to expand its capabilities in petrochemical processing and enhance its APC-driven optimization solutions.

Companies Covered in Advanced Process Control Market

- ABB Ltd.

- Emerson Electric Co.

- Honeywell International Inc.

- Siemens AG

- Schneider Electric SE

- Aspen Technology, Inc.

- Yokogawa Electric Corporation

- Rockwell Automation, Inc.

- AVEVA Group plc

- General Electric Company

- Mitsubishi Electric Corporation

- Azbil Corporation

- Valmet Oyj

- FLSmidth & Co. A/S

- SUPCON Technology Co., Ltd.

Frequently Asked Questions

The global advanced process control market is estimated to be valued at US$3.0 billion in 2026.

The advanced process control market is projected to reach approximately US$5.9 billion by 2033.

Key trends include the integration of AI and machine learning into APC systems, increasing adoption of cloud-based and software-driven control platforms, and growing emphasis on energy efficiency, sustainability, and real-time process optimization.

Advanced Regulatory Control (ARC) is the leading segment, holding a significant share due to its compatibility with existing infrastructure and ease of implementation across industries such as oil & gas and chemicals.

The advanced process control market is expected to grow at a CAGR of 10.3% between 2026 and 2033.

Major players include Emerson Electric Co., Honeywell International Inc., ABB Ltd., Siemens AG, and Schneider Electric SE.