- Technology

- Industrial Demand Side Management Market

Industrial Demand Side Management Market Size, Share, and Growth Forecast 2026 - 2033

Industrial Demand Side Management Market by Service (Demand Response, Energy Efficiency, Load Management), Technology Solutions (Smart Thermostats, AMI Meters, EMS), and Regional Analysis for 2026 - 2033

Industrial Demand Side Management Market Size and Trend Analysis

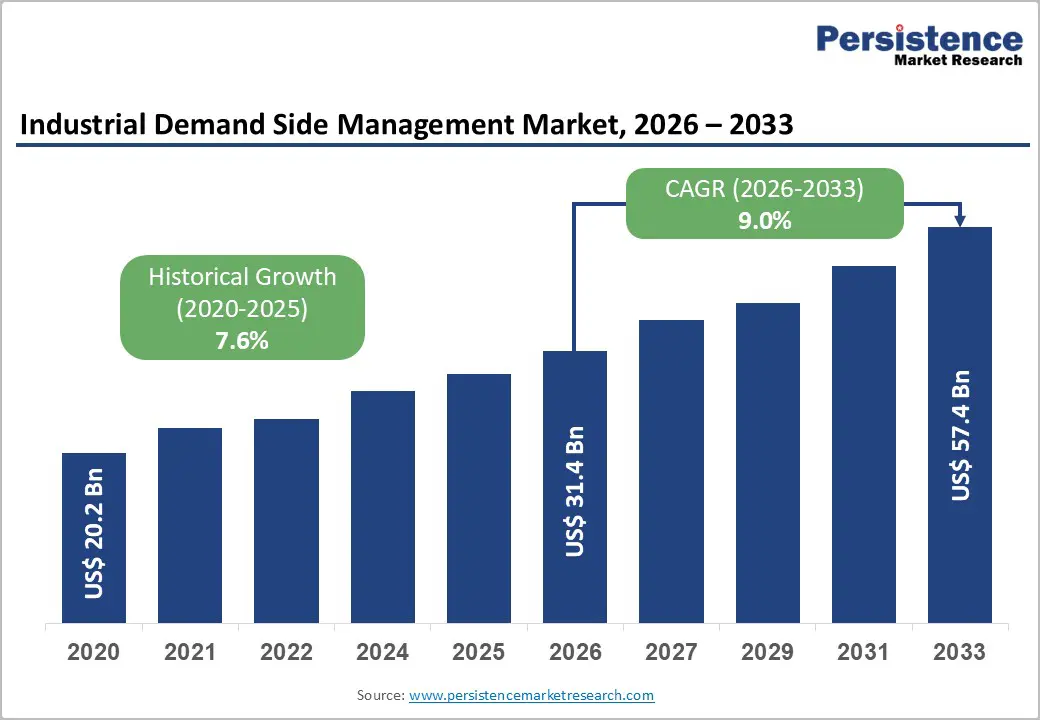

The global industrial demand-side management market size is expected to reach US$ 31.3 billion in 2026 and is projected to reach US$ 57.4 billion by 2033, growing at a CAGR of 9.0% between 2026 and 2033. This robust acceleration is driven by the convergence of decarbonization mandates, rising electricity tariffs, and the integration of AI-powered energy management systems that enable industrial facilities to optimize consumption in real time.

The market is propelled by expanding utility demand response programs, government energy efficiency regulations across the EU, U.S., and Asia Pacific, and the rapid proliferation of Advanced Metering Infrastructure (AMI) and industrial IoT sensor networks that provide the granular consumption data necessary for effective demand-side management across energy-intensive manufacturing, chemicals, and process industries globally.

Key Market Highlights

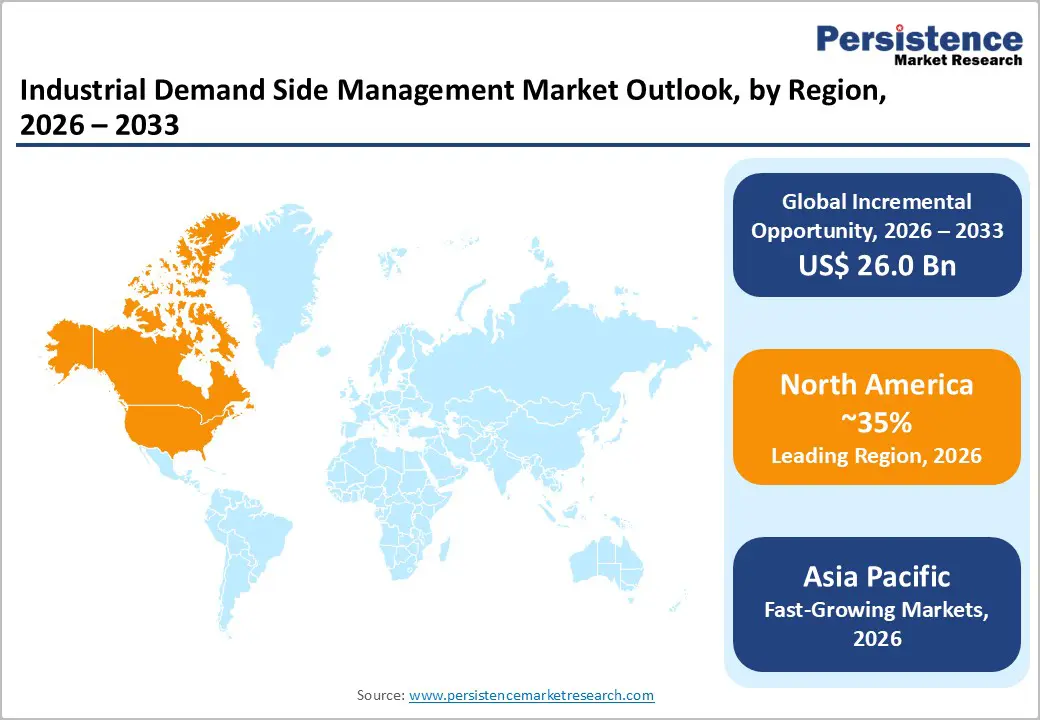

- Leading Region - North America leads the global industrial DSM market, driven by mature FERC-regulated demand response markets, U.S. DOE Better Plants Program with 250+ industrial partners representing 14% of U.S. manufacturing energy use, and the Inflation Reduction Act's industrial efficiency tax credits.

- Fastest Growing Region - Asia Pacific is the fastest growing industrial DSM region, with China at 10.2% CAGR under its 14th Five-Year Plan energy intensity mandates, India's BEE PAT scheme driving EMS adoption, and Japan's METI Green Innovation Fund expanding industrial demand response capabilities.

- Dominant Segment - EMS holds 48% technology solutions market share in 2025, driven by ISO 50001 certification requirements, U.S. DOE Superior Energy Performance mandates, and comprehensive platforms from Schneider Electric, Siemens, Honeywell, and Johnson Controls integrating with industrial SCADA and automation systems.

- Fastest-Growing Segment - AI-powered EMS is the fastest-growing technology segment, delivering 18% additional energy savings beyond conventional systems per U.S. DOE case studies, with C3.ai, Schneider Electric EcoStruxure, and Siemens MindSphere driving enterprise adoption under outcome-based Energy as a Service contracts

- Key Market Opportunity - India's 250 million SMNP smart meter target, U.S. 115 million+ installed AMI meters, and the EU Smart Metering Directive's 80% penetration mandate are creating massive foundational AMI data infrastructure for industrial EMS and demand response platform deployment through 2033.

DRO Analysis

Market Growth Drivers

Expanding Utility Demand Response Programs and Grid Flexibility Mandates

Government and utility-driven demand response programs are the primary structural catalyst for industrial DSM adoption globally. In the United States, the Federal Energy Regulatory Commission (FERC) Order 2222 enables aggregated distributed energy resources, including industrial demand response assets, to participate directly in wholesale electricity markets, unlocking significant economic value for industrial participants and driving rapid adoption of DSM platforms.

The International Energy Agency (IEA) estimates that demand response can provide 500-600 GW of global flexibility by 2030 under its Net Zero scenario. In Europe, the EU Energy Efficiency Directive (EED) and Electricity Regulation (EU) 2019/943 mandate member states to facilitate demand response participation, creating regulatory tailwinds across 27 markets. These frameworks collectively incentivize industrial operators to invest in real-time load monitoring, automated load curtailment systems, and EMS platforms that maximize demand response revenue while maintaining production continuity.

Industrial Decarbonization Targets and Energy Cost Pressure Driving EMS Adoption

Rising electricity prices and binding corporate and national decarbonization commitments are compelling energy-intensive industries to deploy comprehensive energy management systems (EMS) that provide real-time consumption visibility, automated optimization, and carbon accounting. The IEA reports that industrial energy use accounts for approximately 37% of global final energy consumption, making efficiency improvements in this sector critical to meeting Paris Agreement targets.

The EU's Fit for 55 package mandates emissions reductions of 55% by 2030, compelling European industrial operators to measurably reduce consumption. Corporate net-zero pledges with over 9,000 companies committing to the Science Based Targets initiative (SBTi) by 2025require granular Scope 2 energy measurement and reduction capabilities that only industrial EMS and DSM platforms can provide at the required metering and reporting precision.

Market Restraints

High Upfront Investment and Long Payback Periods for Industrial DSM Systems

Comprehensive industrial DSM deployments encompassing AMI meter networks, EMS software platforms, SCADA integration, and building automation system upgrades require substantial upfront capital investment ranging from US$ 500,000 to US$ 5+ million for large industrial facilities. The payback period for such investments, while ultimately positive, can range from 3 to 7 years depending on energy rates, utilization patterns, and the availability of incentives.

For smaller industrial operators with constrained capital budgets and short-horizon investment criteria, this upfront cost burden represents a significant adoption barrier that slows market penetration below its technical potential.

Cybersecurity Risks and OT/IT Integration Complexity in Industrial Environments

Industrial DSM platforms require deep integration between operational technology (OT) systems, SCADA, PLCs, DCS and information technology (IT) networks to enable real-time energy visibility and automated load control. This OT/IT convergence introduces significant cybersecurity risks: the U.S. Cybersecurity and Infrastructure Security Agency (CISA) consistently identifies industrial control system (ICS) cybersecurity as a critical national infrastructure risk.

High-profile industrial cyber incidents and regulatory frameworks, including NERC CIP standards, impose stringent security requirements that increase implementation complexity and slow deployment timelines for industrial DSM systems requiring network connectivity to production systems.

Market Opportunities

AI-Powered Energy Management Systems: Fastest Growing Technology Segment

The integration of artificial intelligence and machine learning into industrial Energy Management Systems (EMS) is creating a new premium technology category that commands significantly higher solution values and is growing at above-market rates. AI-powered EMS platforms deployed by companies including C3.ai, Schneider Electric (EcoStruxure), and Siemens (Mind Sphere) can identify consumption anomalies, optimize multivariable energy procurement strategies, and predict demand flexibility in real time, delivering 10-25% additional energy savings beyond conventional rule-based EMS systems per U.S.

Department of Energy (DOE) case studies. The DOE's Industrial Assessment Centers have documented AI-driven EMS achieving sub-two-year payback periods in process industries, strengthening the investment case and accelerating enterprise adoption of next-generation AI-EMS platforms through 2033.

Advanced Metering Infrastructure (AMI) Rollouts Creating National DSM Platform Deployment Opportunities

Government-mandated smart meter rollouts across major economies are creating the foundational data infrastructure needed for industrial DSM at scale, generating substantial platform-deployment opportunities for solution providers. The U.S. Department of Energy reports that over 115 million smart meters have been installed in the U.S. as of 2023, with ongoing rollouts expanding AMI coverage to industrial facilities.

The European Union's Smart Metering Directive mandates 80% smart meter penetration across member states, with industrial metering receiving priority in energy-intensive sectors under the EU Energy Efficiency Directive. India's Smart Meter National Program (SMNP), targeting 250 million smart meter installations by 2025, is similarly creating an enormous AMI foundation for industrial DSM deployment. Each AMI rollout wave creates a corresponding demand opportunity for EMS software, demand response aggregation platforms, and load management systems that leverage granular AMI data streams.

Category-wise Analysis

Service Insights

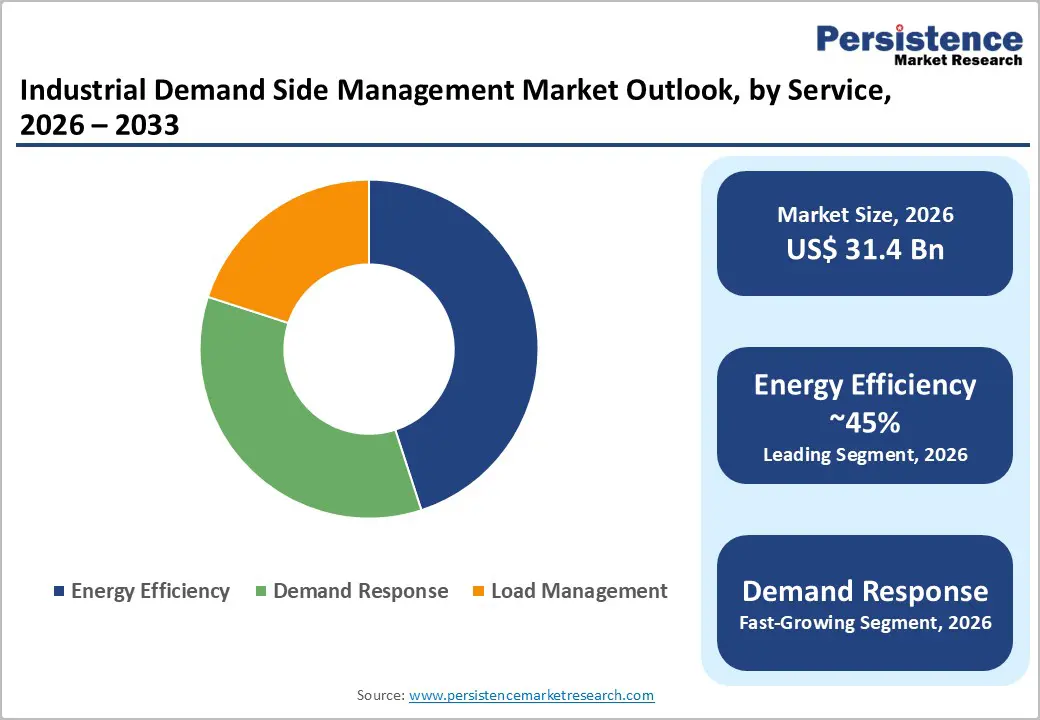

Energy Efficiency services represent the dominant segment in the Service category, accounting for approximately 42% market share in 2026. Energy efficiency encompasses the full spectrum of industrial consumption reduction services including facility energy audits, compressed air system optimization, motor drive efficiency upgrades, industrial lighting retrofit programs, and building envelope improvements that reduce baseline energy demand.

The U.S. Department of Energy's Industrial Assessment Centre (IAC) program which has conducted over 20,000 assessments across U.S. manufacturing plants consistently identifies energy efficiency upgrades delivering average savings of 12-20% of total facility energy consumption.

The ISO 50001 Energy Management System standard adopted by over 20,000 certified organizations globally per ISO data provides a structured framework for continuous energy efficiency improvement that drives systematic service engagement and creates recurring advisory revenue for DSM solution providers.

Technology Solutions Insights

Energy Management Systems (EMS) constitute the leading Technology Solutions segment, accounting for approximately 48% market share in 2026. Industrial EMS platforms provide centralized real-time monitoring, analysis, and control of energy consumption across all facility systems, HVAC, compressed air, process heating, lighting, and production equipment, enabling operators to visualize consumption patterns, identify inefficiencies, and implement automated optimization responses.

The ISO 50001 standard and the U.S. DOE's Superior Energy Performance (SEP) program both mandate EMS implementation as a prerequisite for certification, creating institutional demand for compliant EMS platforms. Major providers, including Schneider Electric, Siemens, Honeywell, and Johnson Controls, offer comprehensive industrial EMS suites that integrate with existing SCADA, building automation, and enterprise resource planning systems, reinforcing the segment's dominant position.

Regional Analysis

North America Industrial Demand Side Management Market Trends & Analysis

North America leads the global Industrial DSM market, driven by the world's most developed utility demand response infrastructure, aggressive federal and state energy efficiency mandates, and high industrial electricity prices that create compelling economic incentives for DSM adoption. The FERC reports consistent growth in demand response resource registrations across organized wholesale electricity markets including PJM, MISO, and CAISO, with industrial customers representing the highest-capacity demand response resource class.

The region's leading position is further reinforced by the U.S. DOE's Industrial Assessment Centre network, extensive utility rebate programs for industrial energy efficiency upgrades, and active smart meter rollout programs that provide the AMI data foundation for advanced DSM platform deployment. Key industrial DSM technology providers including Schneider Electric, Honeywell, Eaton, and Johnson Controls are all headquartered or have primary operations in North America, sustaining strong regional product development and sales infrastructure.

U.S. Industrial DSM Market Size

The United States accounts for approximately 80% of North American industrial DSM market revenue in 2025, representing the world's single largest national market. The U.S. industrial DSM ecosystem is anchored by mature wholesale demand response markets administered by FERC-regulated RTOs/ISOs, ENERGY STAR Industrial certification programs, and the Better Plants Program of the U.S. DOE which has enrolled over 250 industrial partners representing 14% of U.S. manufacturing energy use.

Europe Industrial Demand Side Management Market Trends, Drivers & Insights

Europe represents the second-largest industrial DSM market, shaped by the world's most stringent energy efficiency regulatory framework under the EU Energy Efficiency Directive (EED), Fit for 55 package, and national carbon pricing mechanisms. The energy crisis of 2021-2023, which drove industrial electricity prices across the EU to 2-4 times pre-crisis levels, dramatically accelerated industrial energy management platform investment as organizations sought to mitigate exposure to volatile energy markets.

European industrial DSM is additionally driven by the EU Emissions Trading System (EU ETS) imposing carbon costs on major industrial installations, the ISO 50001 adoption requirement under the EU EED for large energy consumers, and the bloc's REPower EU plan targeting reduced fossil fuel dependence through accelerated industrial energy efficiency improvements.

Germany Industrial DSM Market Size

Germany holds approximately 24% of the European industrial DSM market in 2025. As Europe's largest industrial economy, Germany's energy-intensive sectors chemicals (BASF, Bayer), automotive (BMW, Volkswagen), and heavy manufacturing are among the continent's highest industrial energy consumers and largest DSM solution buyers. The German Energy Efficiency Act (EnEfG) mandates energy audits and management systems for large enterprises. Germany is projected to grow at approximately 8.8% CAGR through 2033.

U.K. Industrial DSM Market Size

The United Kingdom represents approximately 15% of the European industrial DSM market in 2025. The UK's Climate Change Agreements (CCA) scheme providing energy-intensive industries with reduced Climate Change Levy rates in exchange for meeting energy efficiency targets has driven systematic DSM adoption across manufacturing. The UK National Grid ESO's active demand flexibility services create direct financial incentives for industrial load management participation. UK market CAGR is projected at approximately 9.2% through 2033.

France Industrial DSM Market Size

France accounts for approximately 12% of European industrial DSM market revenue in 2025. France's ARENH regulated electricity access program and RTE's industrial demand response market including interpretability contracts worth significant capacity premiums incentivize large industrial facilities to invest in load management infrastructure. France's nuclear-heavy grid faces periodic capacity constraint events that elevate industrial DSM's strategic importance. France is projected to grow at approximately 8.5% CAGR through 2033.

Asia Pacific Industrial Demand Side Management Market Drivers & Analysis

Asia Pacific is the fastest growing industrial DSM market globally, driven by rapid industrial capacity expansion, government energy efficiency mandates, and massive smart meter rollout programs that are creating the AMI data infrastructure for advanced DSM deployment. China dominates the regional market, accounting for approximately 46% of Asia Pacific industrial DSM revenue in 2025, with its 14th Five-Year Plan mandating energy intensity reductions of 13.5% per unit of GDP and primary energy consumption growth caps across industrial sectors.

China Industrial DSM Market Size

China holds approximately 46% of Asia Pacific industrial DSM market revenue in 2025 and is the world's largest single industrial energy consumer. China's National Energy Administration (NEA) has actively promoted demand response participation across provinces, with programs in Guangdong, Jiangsu, and Shanghai enrolling gigawatts of industrial load. State Grid Corporation of China's smart meter program already covering most urban industrial users provides the AMI foundation for advanced DSM deployment. China is projected to grow at approximately 10.2% CAGR through 2033, driven by industrial decarbonization mandates.

India Industrial DSM Market Size

India represents approximately 14% of the Asia Pacific industrial DSM market revenue in 2025. India's Bureau of Energy Efficiency (BEE) administers the Perform, Achieve and Trade (PAT) schemea market-based mechanism incentivizing energy-intensive industries to exceed efficiency targets, which has directly driven EMS and load management technology adoption across steel, cement, textile, and chemical industries.

Japan Industrial DSM Market Size

Japan contributes approximately 11% of the Asia Pacific industrial DSM market revenue in 2025. Japan's Act on the Rational Use of Energy (Energy Conservation Act) mandates annual energy management plans and efficiency improvement targets for designated energy-intensive industrial facilities. Japan's METI is driving expansion of the demand response program under the Green Innovation Fund, targeting industrial load flexibility to address post-Fukushima grid constraints. Japan is projected to grow at approximately 8.4% CAGR through 2033.

Competitive Landscape

The global Industrial DSM market exhibits a moderately consolidated competitive structure, with large industrial technology and automation conglomerates, including Schneider Electric, Siemens, Honeywell, Johnson Controls, and Eaton, competing alongside specialized energy management software providers, including C3.ai, eSight Energy, and Optimum Energy.

Emerging business model trends include outcome-based EaaS (Energy as a Service) contracts where providers share energy savings under performance guarantees, reducing customer risk and accelerating adoption. Strategic acquisitions of specialized AI energy analytics firms by large industrial technology players are reshaping the competitive landscape.

Key Market Developments

- In February 2025, GE Vernova, the energy branch of GE, renewed its commitment to the creation of sustainable energy products and technologies for industrial energy management and demand response, with the intention to help industries lower their energy consumption and expenditures.

- In February 2025, Schneider Electric emphasized its focus on demand-side management in India, aiming to reduce peak demand and improve grid efficiency. The company's AI-powered energy management systems are designed to support the integration of 500 GW of renewable energy into the national grid.

Industrial Demand Side Management Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 20.2 Bn |

| Current Market Value (2026) | US$ 31.4 Bn |

| Projected Market Value (2033) | US$ 57.4 Bn |

| CAGR (2026 - 2033) | 9.0% |

| Leading Region | North America, 35% share |

| Dominant Application | Energy Management Systems, 48% share |

| Top-ranking Product | Energy Efficiency services, 43% |

| Incremental Opportunity | US$ 26.0 Bn |

Companies Covered in Industrial Demand Side Management Market

- C3.ai

- Dexma Sensors

- Eaton Corporation

- Emerson Electric

- eSight Energy

- General Electric

- Honeywell International

- IBM Corporation

- Johnson Controls

- Optimum Energy

- Rockwell Automation

- Schneider Electric

- Siemens AG

- ABB Ltd.

- Itron Inc.

- Landis+Gyr

Frequently Asked Questions

The global Industrial Demand Side Management market is projected to reach US$ 57.4 billion by 2033, growing from an estimated US$ 31.3 billion in 2026 at a CAGR of 9.0%.

Primary demand drivers include FERC Order 2222 enabling industrial demand response in U.S. wholesale electricity markets, the EU EED mandating ISO 50001 for large energy users, and the IEA identifying 500-600 GW of global demand response potential by 2030. Corporate SBTi net-zero commitments covering over 9,000 companies by 2025require granular industrial energy measurement and reduction capabilities.

Energy Management Systems (EMS) lead the Technology Solutions segment with approximately 48% market share in 2025. EMS platforms are mandated under ISO 50001 and U.S. DOE's Superior Energy Performance programs and are deployed by over 20,000 ISO 50001-certified organizations globally.

North America leads with the U.S. accounting for approximately 80% of regional revenue, driven by mature FERC-regulated demand response markets across PJM, MISO, and CAISO, the U.S. DOE Better Plants Program with 250+ industrial partners representing 14% of U.S. manufacturing energy use, and the Inflation Reduction Act's industrial efficiency incentives.

Key companies include Schneider Electric (EcoStruxure, world's leading industrial EMS platform), Siemens AG (MindSphere, SIMATIC Energy Suite), Honeywell (Forge Energy Management), Johnson Controls, Eaton, Emerson Electric, Rockwell Automation, C3.ai, IBM, General Electric, ABB Ltd., Itron, and Landis+Gyr.