- Technology

- Anechoic Chamber Market

Anechoic Chamber Market Size, Share, and Growth Forecast 2026 - 2033

Anechoic Chamber Market by Chamber Type (Full Anechoic Chambers, Semi-Anechoic Chambers, Compact Anechoic Chambers, Portable Anechoic Chambers), Technology Type (RF Anechoic Chambers, Acoustic Anechoic Chambers, Hybrid Anechoic Chambers), Chamber Size (Small, Medium, Large, Custom), Application (Automotive, Aerospace & Defense, Telecommunications, Consumer Electronics, Medical Devices, Industrial), End-user, and Regional Analysis, 2026 - 2033

Anechoic Chamber Market Size and Trend Analysis

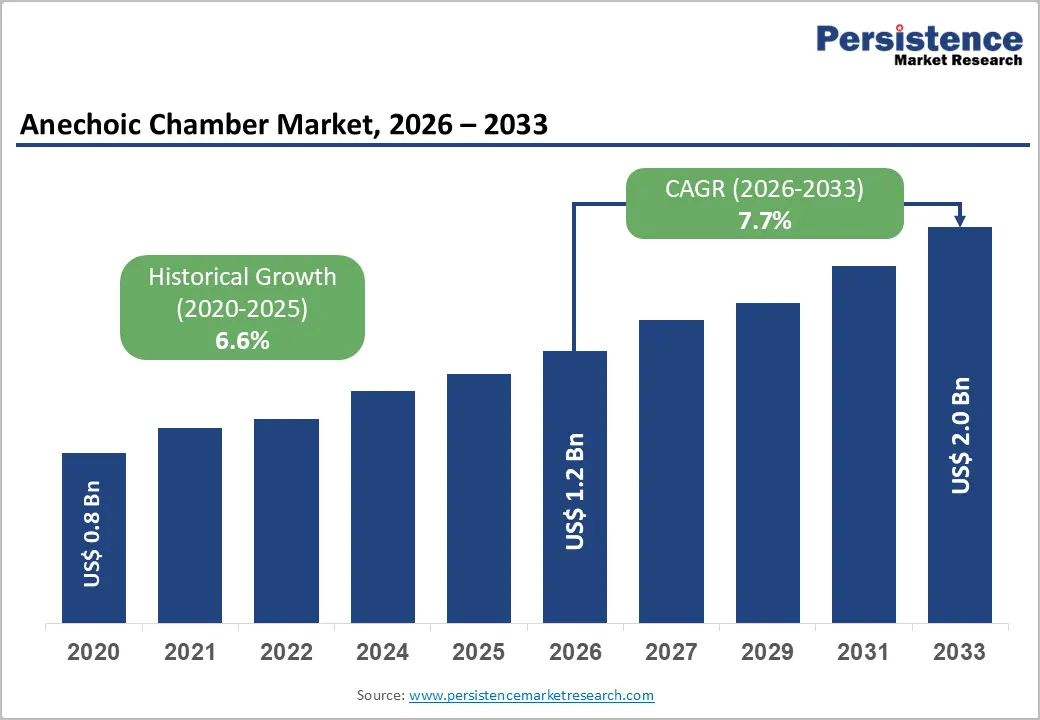

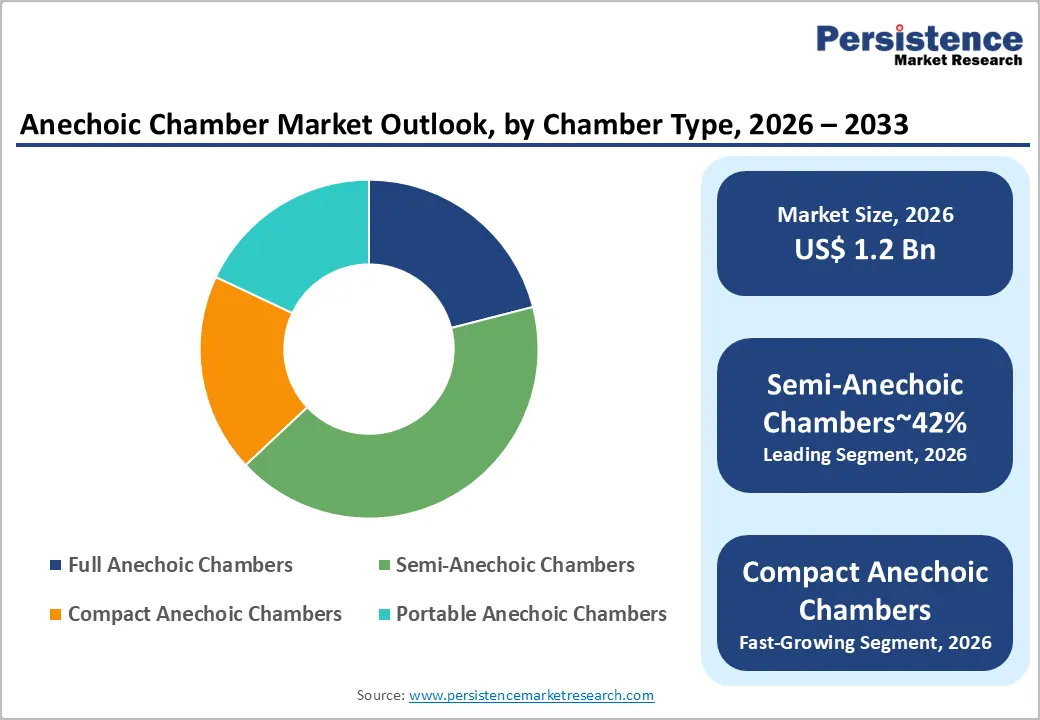

The global anechoic chamber market size is likely to be valued at US$ 1.2 billion in 2026 and is expected to reach US$ 2.0 billion by 2033, growing at a CAGR of 7.7% during the forecast period from 2026 to 2033.

The market is advancing on robust structural foundations driven by rapidly expanding electromagnetic compatibility (EMC) testing mandates across automotive, telecommunications, and consumer electronics sectors, the global proliferation of wireless-connected devices operating across crowded 5G and Wi-Fi 6/6E frequency spectrums, and escalating defense and aerospace procurement of RF-shielded testing environments for radar, satellite, and advanced antenna validation.

Key Industry Highlights:

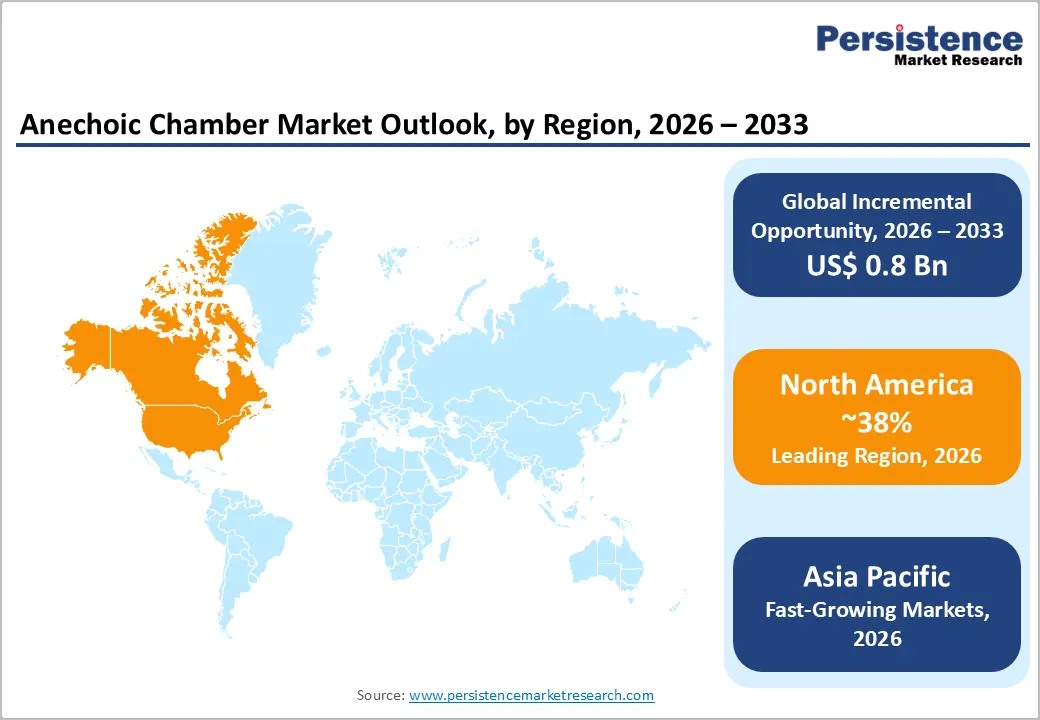

- Leading Region: North America, led by the United States, dominates the global Anechoic Chamber Market holding 38% share, supported by the FCC's thousands of annual wireless device certifications, DoD defense testing programs, the U.S. CHIPS Act's US$ 52.7 Billion semiconductor investment, and home to global chamber leaders ETS-Lindgren LLC and NSI-MI Technologies.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market with rising CAGR of 9.1%, driven by China's mandatory CCC/SRRC certification for electronics, over 3 Million deployed 5G base stations per MIIT, Japan's VCCI compliance ecosystem, and India's BIS CRO expansion under the PLI electronics manufacturing program.

- Dominant Segment: RF Anechoic Chambers lead the Technology Type category with approximately 58% market share, mandated by the FCC for all U.S. wireless device certifications, the CTIA Certification Program for cellular OTA testing, and 3GPP TS 38.521-2 for 5G NR device conformance testing across global markets.

- Fastest Growing Segment: Compact Anechoic Chambers are the fastest-growing chamber type, driven by 3GPP-mandated continuous 5G mmWave OTA testing in device development cycles and the GSMA's projection of over 2.8 Billion active 5G connections by 2025 creating demand for accessible in-lab test environments.

- Key Market Opportunity: Autonomous vehicle and V2X system OTA testing mandates, with SAE Level 3-5 programs active at GM, Ford, Waymo, and BMW, and the U.S. DOT and EU ITS Directive developing C-V2X regulatory frameworks, represent the highest-growth demand catalyst for large-format custom RF anechoic chambers through 2033.

Market Dynamics

Drivers - Global 5G Rollout and Proliferation of Wireless Devices Driving RF Testing Demand

The global deployment of 5G networks and the exponential growth of wireless-enabled connected devices are generating unprecedented demand for RF anechoic chamber testing infrastructure capable of validating antenna performance, over-the-air (OTA) characteristics, and electromagnetic compatibility (EMC) across expanded frequency bands extending from sub-6 GHz to millimeter wave (mmWave) frequencies above 24 GHz.

According to the International Telecommunication Union (ITU), global mobile subscriptions exceeded 8.4 Billion in 2023, with 5G connections growing rapidly across Asia Pacific, Europe, and North America. The 3rd Generation Partnership Project (3GPP), which governs 5G technical specifications, mandates OTA testing procedures for 5G New Radio (NR) devices that require dedicated RF anechoic test environments. With IoT device connections projected to exceed 25 Billion by 2030 per the ITU, the addressable test volume for RF anechoic chambers is expanding at a structural pace that directly translates into new chamber procurement and capacity investment.

Rise in Automotive EMC Compliance Requirements and Vehicle Electrification

The automotive industry's transition toward electric vehicles (EVs), advanced driver assistance systems (ADAS), and connected vehicle platforms is creating substantial and rapidly growing demand for anechoic chamber testing solutions across both RF and acoustic domains. Every new vehicle model requires comprehensive EMC testing under UNECE Regulation No. 10 in Europe and FCC Part 15 in the United States to ensure that onboard electronic systems do not generate or succumb to electromagnetic interference.

According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production reached approximately 93 Million units in 2023. EV powertrains, which generate high-frequency switching noise from inverters and electric motors, introduce new EMC challenges that require extended anechoic chamber testing protocols. The European Automobile Manufacturers' Association (ACEA) reports that modern premium vehicles incorporate over 100 electronic control units (ECUs), each requiring individual and system-level EMC validation, creating a multiplying demand effect for automotive anechoic chamber test hours.

Restraints - Prohibitive Capital Investment and Long Construction Lead Times for Large Anechoic Chambers

Full and semi-anechoic chambers, particularly large-scale facilities capable of testing full vehicles, aircraft components, or high-power industrial equipment, represent multi-million-dollar capital investments with construction lead times of 12-24 months.

According to technical literature published by the IEEE Electromagnetic Compatibility Society, a large automotive semi-anechoic chamber with a 10-meter measurement distance can cost between US$ 5 Million and US$ 20 Million to design, construct, and validate. These high capital costs limit procurement to well-funded OEMs, government defense laboratories, and accredited commercial testing organizations, constraining the addressable customer base and compressing market growth in cost-sensitive geographic regions and industry segments.

Technical Complexity of Absorber Materials for Emerging mmWave and Sub-THz Frequencies

The proliferation of 5G mmWave (24-100 GHz) and emerging sub-terahertz frequency applications is exposing a significant technical limitation in conventional RF anechoic chamber absorber materials. Traditional carbon-loaded foam and ferrite tile absorbers are optimized for frequencies below 18 GHz, and their reflectivity performance degrades substantially at mmWave frequencies, compromising test accuracy and requiring costly chamber upgrades or specialty absorber replacement.

The IEEE Antennas and Propagation Society has published research documenting measurement uncertainty challenges at mmWave frequencies in existing anechoic facilities. This technical gap creates upgrade cost obligations for existing chamber operators and raises the capital requirements for new 5G-capable chamber construction, restraining adoption velocity particularly among smaller commercial testing laboratories.

Opportunities - Growing Demand for Compact and Portable Anechoic Chambers in 5G Device Development

The rapidly increasing throughput requirements of 5G device development cycles, where design teams require continuous OTA antenna performance validation throughout product development rather than only at final compliance testing, are creating strong demand for compact and portable anechoic chambers that can be deployed in engineering laboratories, production floor environments, and field test locations.

According to 3GPP TS 38.521-2 (the 5G NR device conformance testing specification), OTA testing is mandatory for all 5G mmWave user equipment, requiring test environments that adequately suppress reflected signal paths across mmWave frequency bands. Technology companies including Apple, Samsung, and Qualcomm maintain in-house compact anechoic test facilities to accelerate product development timelines. The global 5G device ecosystem, projected by the GSMA to encompass over 2.8 Billion active connections by 2025, is creating a sustained and growing demand pipeline for compact chamber solutions priced accessibly for device manufacturers without large-scale test infrastructure budgets.

Expansion of Over-the-Air (OTA) Testing Requirements for Autonomous Vehicles and V2X Systems

The development and certification of autonomous vehicle (AV) systems and Vehicle-to-Everything (V2X) communication technologies is generating a new and specialized demand category for large-format RF anechoic chambers capable of simultaneously evaluating antenna arrays, radar systems, LiDAR sensors, and C-V2X communication modules in a controlled electromagnetic environment. The U.S. Department of Transportation (DOT) and the European Commission's ITS Directive are developing regulatory frameworks for connected and automated vehicle communication standards that will mandate rigorous OTA performance testing.

According to the SAE International standard J3061 for cybersecurity in automotive systems and the 5GAA (5G Automotive Association), C-V2X systems require specialized OTA validation protocols that necessitate dedicated large-format RF anechoic test environments. With SAE Level 3-5 autonomous vehicle programs active at General Motors, Ford, Waymo, BMW, and Volkswagen, the demand for automotive-grade anechoic chamber testing capacity is expected to surge through 2033.

Category-wise Analysis

Chamber Type Insights

Semi-Anechoic chambers represent the dominant chamber type, accounting for approximately 42% of total anechoic chamber market revenue. Semi-anechoic chambers, which feature RF or acoustic absorber treatment on walls and ceiling but a reflective ground plane floor, are the mandated test environment for automotive EMC testing under CISPR 25 (vehicle components) and CISPR 12 (vehicle radiators) international standards, as well as for radiated emissions and immunity testing per IEC 61000-4-3 and ANSI C63.4.

According to the International Electrotechnical Commission (IEC), semi-anechoic chamber testing is the global standard for product EMC certification across automotive, industrial, and consumer electronics categories. Their dominance reflects the broadest regulatory applicability, established absorber technology maturity, and the largest installed base of any chamber type across global test laboratories and OEM facilities.

Technology Type Insights

RF Anechoic Chambers dominate the Technology Type segment, accounting for approximately 58% of total market revenue. RF anechoic chambers, lined with electromagnetic wave-absorbing materials including ferrite tiles and carbon-loaded polyurethane foam pyramids, provide the electromagnetically quiet environment required for radiated emissions measurement, antenna gain characterization, OTA performance testing, and EMC immunity evaluation across radio frequency bands from MHz to GHz.

According to the Federal Communications Commission (FCC), all wireless-enabled devices sold in the U.S. market must obtain FCC certification through testing in accredited RF anechoic test facilities, creating a legally enforced and continuously growing demand base that scales directly with global device production. The CTIA Certification Program similarly mandates RF anechoic chamber-based OTA testing for cellular devices, reinforcing the segment's market leadership.

Chamber Size Insights

Medium-sized anechoic chambers represent the dominant size segment, accounting for approximately 39% of total market revenue. Medium chambers, typically defined by measurement distances of 3-5 meters and capable of accommodating automotive components, telecommunications base station equipment, consumer electronics subassemblies, and small industrial systems, offer the optimal balance of test versatility, construction cost, and physical installation footprint for commercial testing laboratories, OEM in-house facilities, and university research centers.

According to the IEEE EMC Society, the medium chamber configuration is the most widely deployed globally, serving the broadest range of regulatory compliance testing requirements under FCC, CE, VCCI (Japan), and CCC (China) certification frameworks. Custom chambers are the fastest-growing size segment, driven by specialized aerospace, defense, and autonomous vehicle test requirements.

Application Insights

Automotive represents the dominant application segment, accounting for approximately 30% of total anechoic chamber market revenue. The automotive industry's extensive and legally mandated EMC testing requirements, governed by UNECE Regulation No. 10 in Europe, FCC regulations in the U.S., and equivalent national frameworks across Japan, China, and South Korea, require comprehensive testing of every vehicle model's full electronic system suite across radiated emissions, conducted emissions, and immunity test methodologies.

According to the OICA, global vehicle production of approximately 93 Million units in 2023 generates a continuous and high-volume demand for anechoic chamber testing services. The proliferation of ADAS, V2X, and EV powertrain technologies is multiplying the number of electronic subsystems per vehicle requiring individual EMC qualification, amplifying testing demand beyond simple unit volume growth.

End-user Insights

Testing laboratories represent the leading end-user segment, accounting for approximately 34% of total anechoic chamber market share. Independent accredited testing laboratories, including global networks operated by TÜV Rheinland, SGS S.A., Intertek Group, Bureau Veritas, and UL LLC, serve as the primary outsourced EMC and acoustic compliance testing service providers for manufacturers unable to justify the capital cost of in-house anechoic chamber ownership.

According to the International Laboratory Accreditation Cooperation (ILAC), there are over 100,000 accredited testing laboratories globally, with EMC testing representing one of the most in-demand laboratory service categories. The growing complexity of 5G, automotive, and medical device compliance testing is compelling testing laboratories to invest in upgraded anechoic chamber infrastructure capable of supporting next-generation test methods, sustaining the segment's leadership and driving capacity expansion investment.

Regional Insights

North America Anechoic Chamber Market Trends & Analysis

North America remains a technologically advanced and regulation-driven market, led by strong RF compliance requirements, defense testing infrastructure, and aerospace innovation. The presence of leading testing solution providers, coupled with continuous investments in 5G, satellite communications, and semiconductor R&D, sustains stable demand growth across commercial and government sectors.

- U.S. Anechoic Chamber Market Size

The U.S. dominates the regional market, estimated at USD 580 million in 2026, driven by FCC certification mandates and extensive defense testing programs. Growth is supported by semiconductor facility expansion under the CHIPS Act and increasing OTA testing demand for 5G, IoT, and next-generation wireless devices.

- Europe Anechoic Chamber Market Trends, Drivers & Insights

Europe represents the second-largest market, shaped by strict EMC compliance under CE regulations and strong automotive and aerospace industries. Increasing electrification of vehicles, 5G rollout, and satellite programs are driving demand for advanced semi-anechoic and full anechoic chambers across industrial and research applications.

- Germany Anechoic Chamber Market Size

Germany leads Europe with an estimated market size of USD 200 million in 2026, supported by its dominant automotive OEM base and strong industrial testing ecosystem. Increasing EV development and autonomous driving validation are accelerating demand for vehicle-level EMC and antenna testing facilities.

- U.K. Anechoic Chamber Market Size

The U.K. anechoic chamber market is projected at USD 100 million in 2026, driven by aerospace, defense, and telecommunications testing needs. Government-backed R&D programs and satellite communications initiatives continue to support demand for high-frequency RF and microwave testing environments.

- France Anechoic Chamber Market Size

France is estimated at USD 90 million in 2026, supported by strong aerospace and defense sectors. Investments in satellite systems, avionics testing, and military-grade EMC infrastructure are key contributors, alongside growing telecom equipment testing requirements.

Asia Pacific Anechoic Chamber Market Drivers & Analysis

Asia Pacific is the fastest-growing region, fueled by large-scale electronics manufacturing, aggressive 5G deployment, and automotive expansion. Government mandates for product certification and strong domestic production ecosystems are driving widespread adoption of RF and EMC testing infrastructure.

- China Anechoic Chamber Market Size

China leads globally with an estimated USD 750 million in 2026, driven by its massive electronics manufacturing base and regulatory certification requirements. Rapid 5G infrastructure expansion and government-backed semiconductor initiatives are significantly increasing demand for RF testing facilities.

- India Anechoic Chamber Market Size

India’s market is projected at USD 130 million in 2026, growing rapidly due to BIS certification mandates and expanding domestic electronics manufacturing under PLI schemes. Increasing telecom infrastructure deployment and defense modernization programs are further supporting market expansion.

- Japan Anechoic Chamber Market Size

Japan is estimated at USD 220 million in 2026, supported by a mature electronics and automotive industry. Continuous innovation in advanced mobility, robotics, and high-frequency communication systems sustains steady demand for precision anechoic testing environments.

Competitive Landscape

The global anechoic chamber market is moderately consolidated, with a limited number of specialist engineering firms commanding a significant share of global chamber design, construction, and integration revenue. ETS-Lindgren LLC (part of ESCO Technologies Inc.), Microwave Vision Group, NSI-MI Technologies, Eckel Industries, and IAC Acoustics are the leading full-service chamber providers. Key competitive differentiators include measurement frequency range, absorber performance validation data, turnkey project management capability, post-installation accreditation support, and proprietary absorber material technology. Brüel & Kjær (part of HBK) leads in acoustic anechoic applications.

Emerging business model trends include anechoic-chamber-as-a-service platforms, remote testing portals, and modular portable chamber systems. R&D investment is focused on mmWave absorber technology, OTA measurement system integration, and hybrid RF-acoustic chamber architectures for automotive and IoT applications.

Key Developments:

- February 2025: ETS-Lindgren LLC unveiled its next-generation SMART Chamber platform with integrated 5G mmWave OTA measurement automation, targeting automotive, consumer electronics, and telecommunications device manufacturers requiring broadband anechoic test environments spanning sub-6 GHz to 100 GHz.

- October 2024: Microwave Vision Group announced the expansion of its CATR (Compact Antenna Test Range) anechoic chamber portfolio with a new large-format configuration designed for automotive V2X and ADAS radar system OTA testing, targeting the rapidly growing connected and autonomous vehicle certification market globally.

- April 2024: NSI-MI Technologies commissioned a state-of-the-art multi-purpose anechoic test facility in Suwanee, Georgia, combining RF and acoustic anechoic capabilities in a single installation to support simultaneous EMC, antenna, and noise, vibration, and harshness (NVH) testing for automotive and defense customers.

Anechoic Chamber Market- Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 0.8 Bn |

| Current Market Value (2026) | US$ 1.2 Bn |

| Projected Market Value (2033) | US$ 2.0 Bn |

| CAGR (2026 - 2033) | 7.7% |

| Leading Region | North America, 38% share |

| Dominant Technology Type | RF Anechoic Chambers, 58% share |

| Top-ranking Chamber Type | Semi-Anechoic Chambers, 42% |

| Incremental Opportunity | US$ 0.8 Bn |

Companies Covered in Anechoic Chamber Market

- ETS-Lindgren LLC

- Brül & Kjær

- Eckel Industries

- Microwave Vision Group

- E&C Anechoic Chambers

- Cuming Microwave Corporation

- Panashield

- TDK Corporation

- ESCO Technologies Inc.

- NSI-MI Technologies

- Albatross Projects GmbH

- Frankonia Group

- IAC Acoustics

- Raymond EMC

- Siepel

- MVG (Microwave Vision Group)

- Antenna Research Associates (ARA)

- Comtest Engineering