- Inks, Coatings, Adhesives & Sealants (ICAS)

- Direct Thermal Inks & Coating Market

Direct Thermal Inks & Coating Market Size, Share, and Growth Forecast 2026 - 2033

Direct Thermal Inks & Coating Market by Product Type (Direct Thermal Inks, Direct Thermal Coatings), by Ink Chemistry (Water-Based Inks, Solvent-Based Inks, UV-Curable Inks, Hot-Melt Inks), Coating Layer (Top-Coated Thermal, Non-Top-Coated Thermal, Dual-Coated / Hybrid), Application, Industry, and Regional Analysis, 2026 - 2033

Direct Thermal Inks & Coating Market Size and Trend Analysis

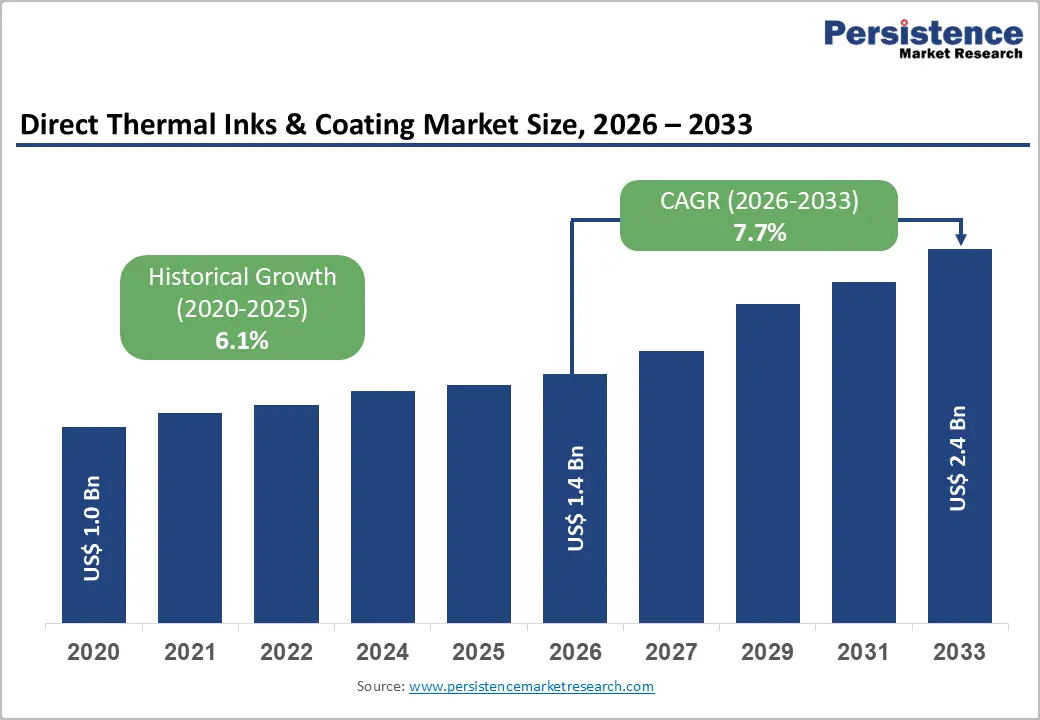

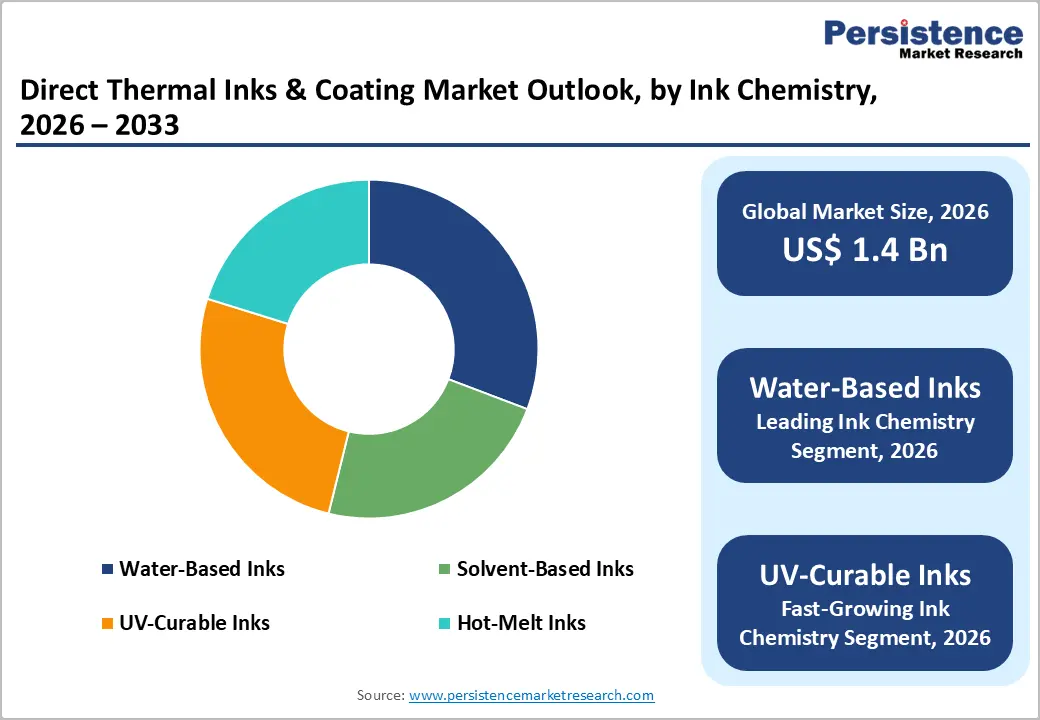

The global direct thermal inks & coating market size is expected to reach US$ 1.4 billion in 2026 and is projected to reach US$ 2.4 billion by 2033, growing at a CAGR of 7.7% between 2026 and 2033.

Growth is driven by rising adoption of contactless, cost-efficient printing across logistics, retail, and healthcare sectors. Rapid e-commerce expansion increases demand for labels, barcodes, and shipping tags. Sustainability trends are accelerating the shift toward BPA-free and eco-friendly formulations. Meanwhile, advancements in coating technologies improve image stability, heat resistance, and durability, enabling reliable high-speed printing in demanding, high-volume operational environments globally.

Key Industry Highlights:

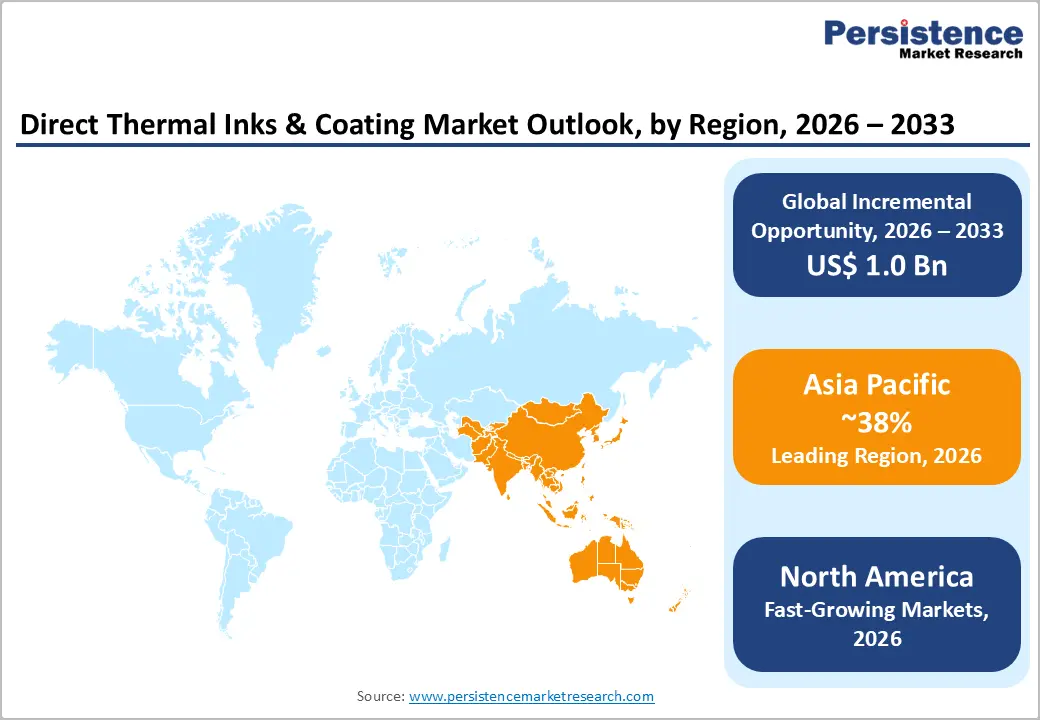

- Leading Region: Asia Pacific dominates, with a 38% share in 2025, driven by strong manufacturing capabilities and rapid e-commerce expansion.

- Fastest-Growing Region: North America emerges as the fastest-growing region, supported by advanced logistics infrastructure, digital supply chain adoption, and rising demand for sustainable labeling solutions.

- Leading Category: Direct Thermal Inks lead the market with 55% share, owing to their cost-efficiency and suitability for high-volume, cartridge-free printing applications.

- Fastest-Growing Category: UV-Curable Inks are the fastest-growing segment, driven by the increasing need for durable, high-resolution, and environmentally compliant printing solutions.

- Key Opportunity: Smart packaging integration presents a major opportunity, unlocking IoT-enabled demand for hybrid coatings and real-time tracking solutions across global supply chains.

Market Dynamics

Driver - Surging E-commerce Expansion Driving Thermal Labeling Demand Globally

The surge in online shopping and supply chain digitization propels demand for direct thermal inks and coatings. According to the United Nations Conference on Trade and Development, global e-commerce sales reached US$ 26.7 trillion in 2023, with logistics and transportation sectors relying heavily on thermal labels for real-time tracking and inventory visibility across increasingly complex distribution networks.

This driver enhances efficiency, as thermal printing eliminates the need for ink cartridges, reducing costs by up to 30% per the International Air Transport Association. Businesses widely adopt these solutions for barcode and shipping labels, ensuring scannable, fade-resistant prints that withstand harsh handling and environmental exposure, strengthening operational reliability and reinforcing long-term market demand.

Stringent Environmental Regulations Accelerating Eco-Friendly Ink Adoption

Stringent environmental policies worldwide favor water-based and UV-curable thermal inks over solvent-based alternatives. The European Chemicals Agency highlights that compliance with the REACH Regulation is driving significant innovation in low-VOC and sustainable coating technologies, encouraging manufacturers to transition toward greener production processes and safer chemical compositions.

These formulations minimize waste and emissions, align with sustainability certifications such as FSC, and comply with corporate environmental goals. Their low-energy curing process reduces operational costs and energy consumption, making them highly attractive for large-scale retail and e-commerce operations, thereby fostering broader adoption and supporting long-term market expansion.

Restraints - Stringent Regulatory Compliance Limiting Formulation Flexibility and Innovation

Harsh chemical restrictions limit formulation flexibility for thermal inks and coatings. The U.S. Environmental Protection Agency enforces limits on bisphenol A (BPA) in thermal papers, affecting nearly 40% of legacy products per U.S. Food and Drug Administration guidelines. This creates significant pressure on manufacturers to redesign formulations while maintaining performance standards across critical applications.

These requirements raise reformulation costs by 15–20%, slowing innovation, particularly in healthcare and pharmaceutical applications where durability and compliance are essential. Manufacturers also face prolonged approval timelines and certification hurdles, which delay product launches, restrict scalability, and limit market penetration in highly regulated regions.

Volatile Raw Material Supply Chains Impacting Production Stability

Fluctuations in the prices of specialty resins and dyes disrupt the economics of thermal ink and coating production. According to the World Bank, petroleum-based inputs experienced around 25% price volatility in 2024, significantly affecting solvent-based ink formulations and increasing cost unpredictability across manufacturing operations.

Geopolitical tensions further exacerbate raw material shortages and logistics constraints, particularly for Asia Pacific suppliers. Lead times have increased by nearly 30%, impacting production planning and delivery schedules. These disruptions constrain growth in packaging and labeling segments, where consistent supply and cost efficiency are critical for maintaining competitive advantage.

Market Opportunities

Integration of Smart Packaging Technologies: Unlocking Advanced Tracking Solutions

Integration with IoT-enabled smart labels presents massive potential for direct thermal inks and coatings. The GS1 promotes RFID-embedded thermal coatings, with logistics and transportation expected to achieve nearly 50% adoption by 2030, according to forecasts from the International Telecommunication Union. This shift is transforming traditional labeling into intelligent, data-driven systems.

Companies investing in hybrid dual-coated papers gain a competitive edge in real-time tracking, especially in food and beverage supply chains where visibility is critical. These technologies can reduce spoilage by up to 20%. Policy incentives, such as the U.S. Farm Bill, support traceable supply chains, amplifying demand for advanced thermal coating solutions.

Increasing Demand for Secure and High-Precision Healthcare Labeling

Rising pharmaceutical serialization is significantly boosting demand for high-resolution thermal coatings. The World Health Organization reports that approximately 10.5 billion falsified medical products are produced annually, driving stringent track-and-trace requirements under the Drug Supply Chain Security Act. These mandates require reliable, tamper-proof labeling technologies across global healthcare systems.

UV-curable inks provide superior print clarity and tamper-evident features, making them ideal for healthcare and pharmaceutical applications. Their ability to deliver durable, high-resolution output supports compliance and patient safety. With the rapid expansion of digital health ecosystems, this segment is expected to witness strong growth, with a potential CAGR reaching around 15% through 2032.

Category-wise Insights

Product Type Insights

Direct thermal inks lead with 55% market share in 2025, driven by superior print speed and cost-efficiency in high-volume printing environments. Innovations from Nippon Paper Industries in thermal paper compatibility further strengthen this dominance across retail and e-commerce labeling applications. Their cartridge-free operation reduces downtime by nearly 40%, as highlighted by the National Retail Federation, improving point-of-sale efficiency and operational throughput.

Direct thermal coatings are emerging as the fastest-growing segment due to increasing demand for enhanced durability and resistance properties. Industries such as logistics and healthcare are prioritizing coatings that improve image longevity and environmental resistance. The growing focus on advanced layering technologies and specialty coatings is accelerating adoption, particularly in applications that require long-term readability and protection under harsh conditions.

Ink Chemistry Insights

Water-Based inks command 45% share in 2025, favored for eco-compliance, safety, and regulatory acceptance across industries. Data from the U.S. Environmental Protection Agency shows that these inks emit nearly 70% fewer VOCs than solvent-based alternatives, making them ideal for food and beverage packaging. Compliance with U.S. Food and Drug Administration standards further supports their use in healthcare and sensitive applications.

UV-Curable inks are witnessing the fastest growth due to their superior print durability, rapid curing, and resistance to environmental factors. These inks are increasingly adopted for high-performance applications that require precision and long-lasting output. Their ability to deliver high-resolution, tamper-resistant prints is driving demand across healthcare, electronics, and industrial labeling segments.

Coating Layer Insights

Top-Coated thermal holds 50% share in 2025, offering superior image stability, chemical resistance, and smudge protection. Standards from ASTM International confirm that top-coated papers retain legibility up to three times longer in humid conditions, making them highly suitable for shipping and logistics labels. Their widespread use in e-commerce minimizes errors caused by unreadable barcodes.

Dual-Coated / Hybrid coatings are emerging as the fastest-growing category due to their ability to combine durability with enhanced print quality. These advanced coatings are gaining traction in industries requiring multifunctional performance, including resistance to heat, moisture, and abrasion. Their versatility supports broader adoption in demanding applications such as industrial labeling and global supply chain operations.

Application Insights

Labels & Tags dominate with 40% share in 2025, driven by their essential role in inventory management and product identification. Adoption rates from GS1 indicate that nearly 80% of global retailers rely on thermal labels to ensure accuracy and traceability. Their durability across diverse environments supports efficient logistics and streamlined operations.

Barcodes & shipping labels are the fastest-growing application segment, driven by the rapid expansion of global logistics and fulfillment networks. Increasing reliance on real-time tracking and automated scanning systems is driving demand for high-performance labeling solutions. These applications require consistent print quality and durability, making them critical for modern supply chains and delivery ecosystems.

Industry Insights

Retail & E-commerce leads with 35% share in 2025, propelled by strong demand for point-of-sale receipts, product labeling, and shipping tags. According to the United Nations Conference on Trade and Development, e-commerce continues to expand rapidly, underscoring the need for fast, reliable thermal printing solutions that enhance the customer experience and operational efficiency.

Healthcare & Pharmaceuticals is the fastest-growing segment, driven by increased emphasis on product traceability, regulatory compliance, and patient safety. Rising adoption of serialization and track-and-trace systems is boosting demand for high-quality thermal printing. The need for precise, tamper-evident labeling solutions is further accelerating growth across pharmaceutical and medical device applications.

Regional Insights

North America Direct Thermal Inks & Coating Market Trends and Insights

North America holds a significant 30% share in direct thermal inks & coating market in 2025, driven by advanced retail ecosystems and strong logistics infrastructure. The U.S. leads the region, supported by regulatory frameworks from the Federal Trade Commission that emphasize accurate labeling and consumer transparency. High adoption of top-coated thermal solutions further strengthens performance in demanding applications.

The region is witnessing steady growth due to continuous innovation and digital transformation across supply chains. Technology hubs such as Silicon Valley play a vital role in advancing smart labeling and automation. Increasing investments in sustainable packaging and eco-friendly ink formulations are also shaping market expansion, particularly across retail, healthcare, and food distribution sectors.

Europe Direct Thermal Inks & Coating Market Trends and Insights

Europe demonstrates stable growth with a projected CAGR of 8.5%, supported by stringent environmental regulations and strong industrial capabilities. Countries such as Germany lead in precision manufacturing, while regulatory alignment under the REACH Regulation ensures compliance and sustainability. The European Chemicals Agency reports increasing adoption of green formulations across the region.

The market is steadily expanding due to rising demand for sustainable and high-performance labeling solutions. The UK emphasizes eco-friendly inks post-Brexit, while France and Spain are witnessing growth through food and beverage packaging applications. Increasing focus on low-VOC coatings and recyclable materials is further driving innovation and long-term adoption across industries.

Asia Pacific Direct Thermal Inks & Coating Market Trends and Insights

Asia Pacific leads the global industry with a dominant 38% share in 2025, supported by strong manufacturing capabilities and export-driven production. China remains the key contributor, accounting for nearly 60% of global thermal paper exports as per China Customs. Countries such as India and Japan further strengthen regional growth through industrial expansion and technological advancements.

The region is expected to achieve a fast growth, driven by rapid e-commerce expansion, logistics infrastructure development, and government initiatives such as “Make in India.” Increasing adoption of advanced labeling solutions across retail, electronics, and supply chains is accelerating demand. Cost advantages and rising industrialization across ASEAN economies continue to position the Asia Pacific as a high-growth hub for thermal inks and coatings.

Competitive Landscape

The global direct thermal inks & coating industry’s competitive landscape is moderately consolidated, driven by continuous investment in research and development focused on eco-friendly ink and coating technologies. Leading players emphasize innovation through advanced formulations, patented chemistries, and performance enhancements that improve durability, print quality, and environmental compliance. Strategic collaborations and capacity expansions are also shaping competition, enabling firms to strengthen global supply chains and meet evolving regulatory standards.

At the same time, the market retains a fragmented structure at the regional level, with numerous local suppliers catering to cost-sensitive segments. Emerging business models centered on circular economy practices, including recycling and sustainable material use, are gaining traction, fostering innovation and differentiation across both established and emerging participants.

Key Developments

- In June 2025, Oji Holdings Corporation launched BPA-free direct thermal inks tailored for retail packaging, strengthening sustainability compliance and addressing global regulatory pressure on chemical safety while supporting eco-friendly labeling solutions across expanding e-commerce and logistics sectors.

- In March 2024, Nippon Paper Industries expanded its U.S. production capacity for top-coated thermal papers to meet rising logistics and e-commerce demand, enhancing supply reliability and supporting high-performance labeling applications requiring durability, clarity, and resistance in distribution environments.

- In October 2023, Ricoh Company developed advanced UV-curable thermal coatings designed for high-speed barcode printing, enabling faster curing, improved print durability, and enhanced resistance to environmental factors, supporting industrial and logistics sectors requiring precise, long-lasting labeling solutions.

Direct Thermal Inks & Coating Market- Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.0 Bn |

| Current Market Value (2026) | US$ 1.4 Bn |

| Projected Market Value (2033) | US$ 2.4 Bn |

| CAGR (2026 - 2033) | 7.7% |

| Leading Region | Asia Pacific, 38% share |

| Dominant Application | Labels & Tags, 40% share |

| Top-ranking Product | Direct Thermal Inks, 55% |

| Incremental Opportunity | US$ 1.0 Bn |

Companies Covered in Direct Thermal Inks & Coating Market

- Ricoh Company, Ltd.

- Oji Holdings Corporation

- Appvion Operations, Inc.

- Koehler Paper Group

- Nakagawa Manufacturing (USA), Inc.

- Mitsubishi Paper Mills Limited

- Hansol Paper Co., Ltd.

- Jujo Thermal Ltd.

- Kanzaki Specialty Papers Inc.

- Iconex LLC

- Nippon Paper Industries Co., Ltd.

- Avery Dennison Corporation

- Sihl GmbH

- Henan JiangHe Paper Co., Ltd.

- Rotolificio Bergamasco S.r.l.

Frequently Asked Questions

The global Direct Thermal Inks & Coating market is expected to reach US$ 1.4 Billion in 2026.

E-commerce expansion and logistics automation drive demand, with thermal labels enabling efficient, cost-saving printing.

Asia Pacific leads with 38% share in 2025, powered by manufacturing and rapid urbanization.

Smart packaging with IoT integration offers growth, enhancing traceability in food & beverages and logistics.

Leading players include Oji Holdings Corporation, Nippon Paper Industries, and Ricoh Company, focusing on sustainable innovations.