- HVAC

- HVAC Packaged Units Market

HVAC Packaged Units Market Size, Share, and Growth Forecast, 2026 - 2033

HVAC Packaged Units Market by Product Type (Rooftop Units (RTU), Air-Cooled Packaged Units, Water-Cooled Packaged Units, Heat Pump Packaged Units), Cooling Capacity (Below 10 Tons, 10-30 Tons, Above 30 Tons), End-user (Residential, Commercial, Industrial) and Regional Analysis for 2026 - 2033

HVAC Packaged Units Market Size and Trends Analysis

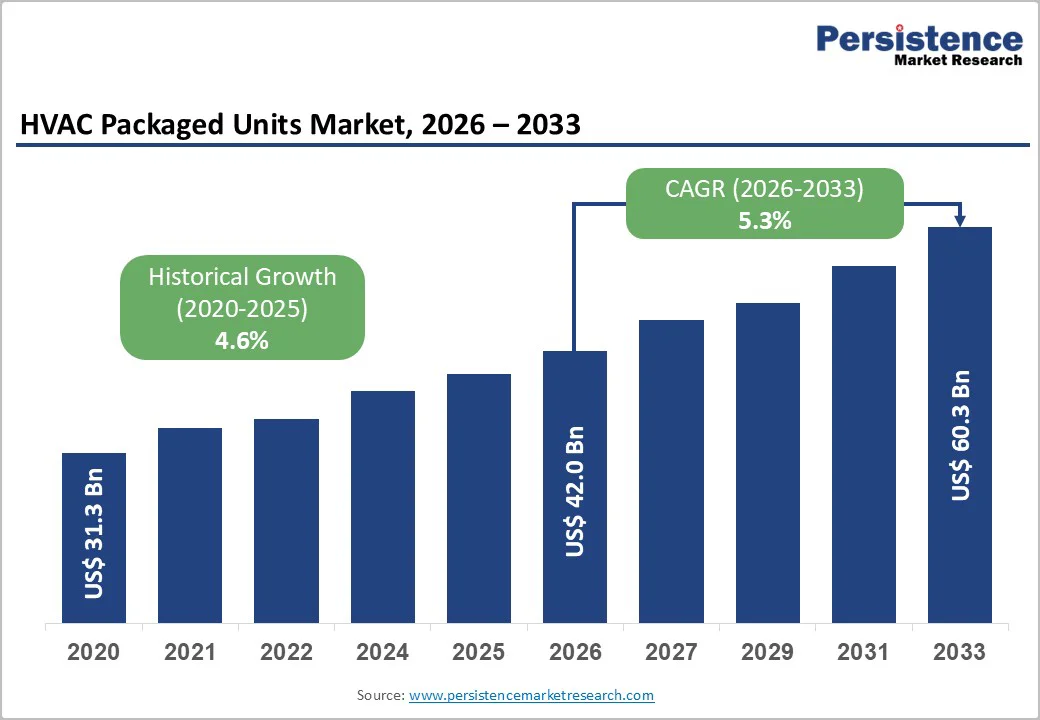

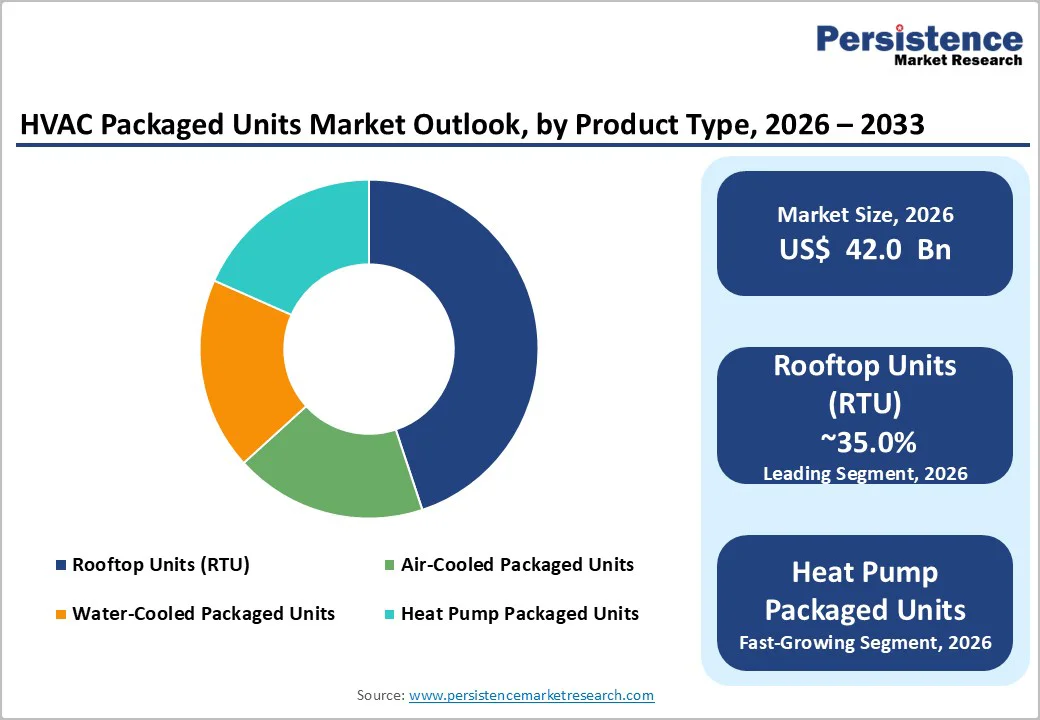

The global HVAC packaged units market size is valued at US$ 42.0 billion in 2026 and is projected to reach US$ 60.3 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

The market expansion is primarily driven by increasing demand for energy-efficient heating, ventilation, and air conditioning systems, supported by innovations such as heat pump technologies and low-GWP refrigerants.

Regulatory initiatives aimed at reducing carbon emissions and enhancing energy efficiency, alongside rapid urbanisation and infrastructural developments, are further propelling market growth. Additionally, rising emphasis on sustainability and decarbonization in commercial and residential sectors significantly influences market dynamics.

Key Industry Highlights:

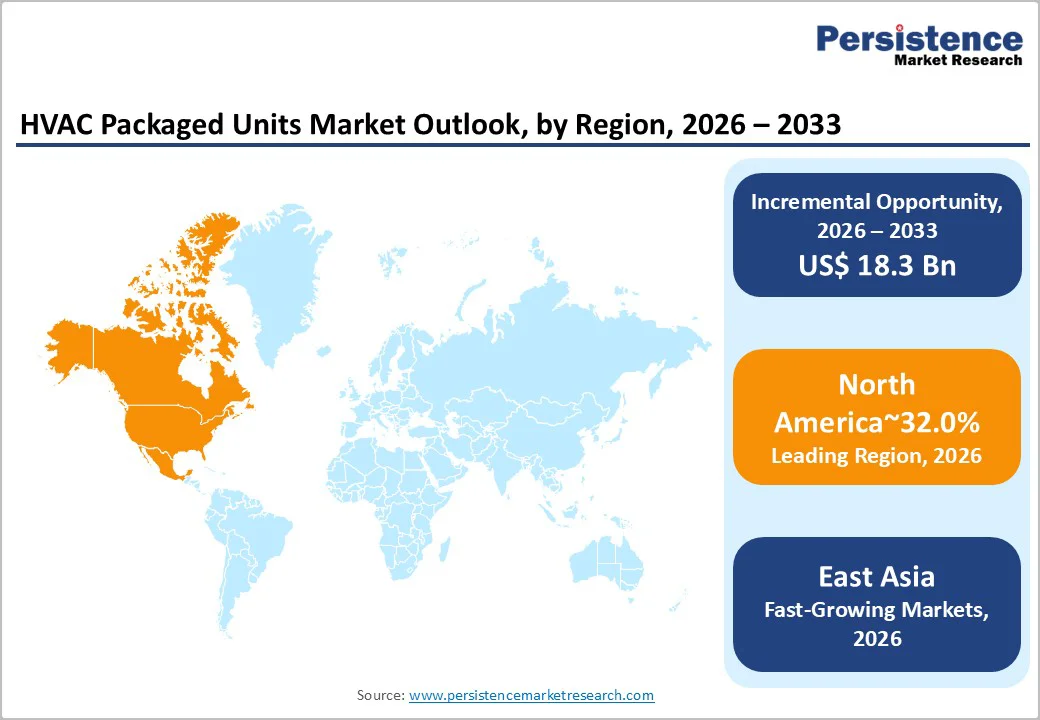

- Regional Leadership: North America is the dominant region in the HVAC Packaged Units Market, accounting for 32% of the global market share in 2026, driven by stringent energy efficiency regulations and significant investments in electrification and decarbonization initiatives.

- Fastest-Growing Region: East Asia represents 19% of the market share in 2026, emerging as the fastest-growing region due to rapid urbanization, government incentives for energy-efficient technologies, and a strong push for electrification in both residential and commercial buildings.

- Leading Product Segment: Rooftop Units (RTU) holds 35% of the global market share in 2026, driven by their versatility, cost-effectiveness, and ease of installation, particularly in commercial and light industrial applications.

- Fastest-Growing Product Segment: Heat Pump Packaged Units is the fastest-growing category, benefiting from innovations such as inverter compressors and eco-friendly refrigerants like R-32, aligning with global decarbonization trends.

- Technological Innovation: Smart HVAC Integration presents a major opportunity, as convergence with IoT and predictive maintenance platforms enhances system reliability, energy efficiency, and customer satisfaction, driving competitiveness in the market.

- Key End-user Leadership: Commercial Sector leads the market with 45% share in 2026, reflecting the significant demand from office buildings, hotels, and hospitals that require scalable and energy-efficient HVAC solutions.

| Key Insights | Details |

|---|---|

| HVAC Packaged Units Market Size (2026E) | US$ 42.0 Bn |

| Market Value Forecast (2033F) | US$ 60.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Drivers - Environmental Regulations and Energy Efficiency Policies

Government policies targeting energy conservation and greenhouse gas emission reductions are a fundamental driver in the HVAC Packaged Units Market. Regulatory bodies such as the U.S. Environmental Protection Agency have introduced mandates for refrigerants with lower global warming potential (GWP), prompting manufacturers to develop advanced HVAC systems compliant with these standards.

For example, the adoption of refrigerants like R-32 and R-454B in packaged rooftop units aligns with efforts to lower environmental impact.

These regulations incentivise the shift from conventional equipment to energy-efficient, environmentally friendly solutions, encouraging investments in HVAC technologies that reduce operational carbon footprints in residential, commercial, and industrial settings. Consequently, the market benefits from enhanced product innovation, making energy-efficient HVAC units increasingly integral to sustainable building practices.

Technological Advancements in HVAC Systems

Technological innovation plays a crucial role in the evolution of the HVAC Packaged Units Market. The integration of inverter compressors, advanced heat pumps, and digital control systems substantially improves system performance and energy management.

Recent product introductions by leading manufacturers emphasise heat pump packaged units that leverage low-ambient operation capabilities and inverter-driven compressors, optimising efficiency even in colder climates.

Such advancements enable HVAC packaged units to balance energy consumption and operational efficacy while supporting electrification in heating and cooling applications. Moreover, ongoing research and development initiatives focus on improving lifecycle sustainability by enhancing components such as refrigerants, fan systems, and system configurations, thereby reinforcing the market’s transition toward smarter, greener HVAC solutions.

Infrastructure Development and Urbanization Trends

Urbanization and expanding commercial infrastructure continue to influence market demand for HVAC packaged units. The construction of new commercial buildings, including offices, schools, hotels, and healthcare facilities, necessitates reliable, efficient HVAC solutions to manage indoor air quality and thermal comfort. Industrial growth and facility modernisation further drive demand for scalable HVAC packaged products adaptable to diverse environments.

The commercial sector accounts for a substantial portion of installations due to these infrastructure trends, emphasizing the need for HVAC units that can deliver performance in varied climates and settings. Urbanization also propels residential HVAC needs as housing developments incorporate energy-efficient systems compliant with evolving regulatory landscapes, underpinning the steady market progression.

Restraint - High Initial Investment Costs

The relatively high upfront capital expenditure associated with advanced HVAC packaged units poses a barrier to adoption, especially in cost-sensitive markets or projects with tight budget constraints. Installation complexities and the need for specialised maintenance for cutting-edge components can elevate total lifecycle costs.

These financial challenges limit the pace at which new, energy-efficient technologies penetrate certain market segments, particularly in developing regions. Cost-related concerns necessitate careful consideration of long-term energy savings versus short-term investment, influencing procurement decisions across commercial, industrial, and residential users.

Opportunity - Emerging Markets with Expanding Construction Sectors

Emerging economies exhibit significant potential for HVAC packaged unit adoption due to rapid urbanization, industrialization, and infrastructure development. Market players can capitalise on the expanding construction of commercial and residential buildings in regions like the Middle East, Southeast Asia, and Latin America.

Government initiatives focused on sustainable cities and smart infrastructure further support HVAC system integration. These opportunities encourage tailored product offerings that meet region-specific climatic conditions and regulatory frameworks, facilitating market penetration and long-term growth in under-tapped geographies.

Technological Convergence and Smart HVAC Systems

The convergence of HVAC technologies with IoT, digital monitoring, and predictive maintenance solutions presents a substantial opportunity for enhancing system reliability and operational efficiency. Advanced digital platforms enable real-time monitoring of packaged units, facilitating proactive servicing and reducing downtime.

Manufacturers integrating cloud-based services and AI-driven analytics can differentiate their offerings, improving energy management and cost savings for end-users. This technological synergy unlocks new business models focused on performance-based contracting and service continuity, promoting customer retention and market competitiveness in the HVAC packaged units market.

Policy Support for Decarbonization and Electrification

Global and regional policy frameworks aimed at decarbonising heating and cooling systems provide a supportive environment for the HVAC Packaged Units Market. Incentives for adopting electric heat pumps and low-carbon HVAC solutions align with broader climate action plans such as the European Green Deal and the U.S. Clean Energy initiatives.

These policies mitigate operational costs through subsidies and tax credits, encouraging end-users to transition from fossil-fuel-based systems. The HVAC market stands to benefit from such regulatory encouragement, enabling the introduction of innovative products tailored to meet strict emissions and efficiency criteria.

Category-wise Analysis

Product Type Insights

Rooftop Units (RTU) dominate the product segment with a commanding market share of approximately 35.0% in 2026. This leadership is attributed to their adaptability across commercial and light industrial facilities, ease of installation on building rooftops, and suitability for larger-scale air conditioning needs. Their modular design allows flexibility and relatively lower installation costs, making them favourable in diverse applications.

Heat pump packaged units represent the fastest-growing segment, driven by technological advancements such as inverter compressors and the usage of eco-friendly refrigerants like R-32. Heat pump units are increasingly preferred for their dual functionality in heating and cooling, offering energy-efficient alternatives to conventional units, particularly in regions with moderate to cold climates, aligning with global decarbonization trends.

End-user Insights

The commercial sector holds a dominant share near 45.0% in 2026, underscoring the importance of packaged HVAC systems in office buildings, retail, hospitality, and institutional infrastructures. Commercial users prioritise HVAC reliability, energy efficiency, and compliance with ventilation standards, driving robust demand for advanced packaged units.

Residential end-users present the fastest-growing segment, influenced by rising awareness of indoor air quality and energy cost savings among homeowners. Adoption of HVAC packaged units in residential new builds and retrofit applications is stimulated by advances in heat pump technology and stricter energy codes promoting sustainable housing solutions.

Regional Insights and Trends

North America HVAC Packaged Units Market Trends

In 2026, North America accounts for about 32% of the global HVAC packaged units Market. The region's growth is supported by stringent energy efficiency regulations, such as the U.S. Department of Energy’s (DOE) 2025 standards, driving manufacturers to innovate products with lower GWP refrigerants and enhanced energy performance.

Leading companies like Carrier have validated rooftop heat pump solutions exceeding DOE efficiency targets, boosting market confidence. The commercial sector remains the primary consumer due to extensive infrastructure upgrades and sustainability commitments across industries.

Regionally specific initiatives encouraging electrification and decarbonization further underpin market dynamics, attracting investments in local manufacturing capacities and technology partnerships.

East Asia HVAC Packaged Units Market Trends

East Asia represents approximately 19% share in 2026. The region benefits from substantial government incentives promoting energy-efficient HVAC technologies to combat urban air pollution and reduce carbon emissions. Countries such as China, Japan, and South Korea are investing in advanced heat pump technologies and smart HVAC integration aligned with environmental targets.

Notable developments include Daikin’s expansion of heat pump manufacturing and its focus on low-GWP refrigerants like R-32 in new product lines unveiled in 2024 and 2025. The regional market is shaped by rapid urbanization, infrastructure growth, and policy directives encouraging electrification in residential and commercial buildings, making East Asia a significant contributor to global market progression.

Europe HVAC Packaged Units Market Trends

Europe accounts for roughly 25% of the global market, driven by aggressive climate policies such as the European Union’s Fit for 55 targets. These policies mandate improved energy efficiency and CO2 emissions reduction, encouraging the adoption of advanced HVAC packaged units equipped with eco-friendly refrigerants and energy-saving features. Key markets like Germany and France exhibit strong demand for retrofit and new installations to meet tightening energy codes.

The region’s competitive landscape is characterised by collaboration between manufacturers and governmental bodies promoting research in sustainable HVAC solutions. Regulatory compliance, combined with a high concentration of environmentally conscious commercial properties, supports steady market demand and technological innovation investments.

Competitive Landscape

The global HVAC packaged units market is characterized by a fragmented competitive landscape with numerous players offering a wide range of solutions across residential, commercial, and industrial sectors.

Leading players such as Daikin, Carrier, Trane, Johnson Controls, and Mitsubishi Electric dominate the market with extensive product portfolios and global reach. However, other companies like LG, Samsung, Lennox, and Rheem also contribute to the competitive dynamics, offering innovative and energy-efficient packaged units.

Additionally, brands like Bosch, Hitachi, York, Gree, and Midea continue to expand their footprint, particularly in emerging markets. Despite a few dominant players, the market remains open to new entrants and regional manufacturers, contributing to its fragmented nature.

Key Industry Developments:

- In Nov 2025 Daikin began construction on a new manufacturing facility in Jeddah, Saudi Arabia, aimed at localising the production of chillers and hydronic heat pumps for advanced cooling needs. This strategic initiative supports Daikin’s commitment to meeting regional demands and enhancing manufacturing capabilities in the Middle East. Moreover, the facility adheres to Daikin's global standards, ensuring high-quality, energy-efficient products tailored to the region's climate. Additionally, it will support the Kingdom’s Vision 2030 by promoting sustainability, job creation, and innovation, while strengthening Daikin’s regional growth strategy.

- In Feb 2025 At the 2025 AHR Expo, Applied Americas showcased its commitment to decarbonization with a new suite of HVAC solutions designed to improve energy efficiency and reduce carbon emissions. Highlighting the use of low-GWP R-32 refrigerants, the company unveiled its advanced HVAC systems, including the Trailblazer AGZ-F and Smart Source Water Source Heat Pumps, optimised for sustainability. These technologies reflect Daikin’s broader goal to accelerate the electrification of heating and support the global transition to energy-efficient, decarbonized HVAC systems.

Companies Covered in HVAC Packaged Units Market

- Daikin Industries, Ltd.

- Carrier Global Corporation

- Trane Technologies

- Johnson Controls International plc

- Mitsubishi Electric Corporation

- LG Electronics Inc.

- Samsung Electronics Co., Ltd.

- Lennox International Inc.

- Robert Bosch GmbH

- Rheem Manufacturing Company

- Hitachi, Ltd.

- York International Corporation

- Gree Electric Appliances, Inc. of Zhuhai

- Midea Group Co., Ltd.

- Fujitsu Limited.

Frequently Asked Questions

The global HVAC Packaged Units Market is projected to be valued at US$ 42.0 Bn in 2026.

Rooftop Units (RTU) are expected to account for approximately 35% of the global HVAC Packaged Units Market by Product type in 2026.

The market is expected to witness a CAGR of 11.3% from 2026 to 2033.

The growth of the HVAC Packaged Units Market is driven by environmental regulations, energy efficiency policies, technological advancements, and infrastructure development spurred by urbanization, with government policies pushing for sustainable and energy-efficient solutions.

Key market opportunities in the HVAC Packaged Units Market include emerging markets with expanding construction sectors, technological convergence with smart HVAC systems, and policy support for decarbonization and electrification.

The key players in the HVAC Packaged Units Market include IBM, Cisco Systems, Vodafone Group, Accenture, Ericsson, and Amazon Web Services (AWS).