- Advanced Materials

- High Performance Fibers Market

High Performance Fibers Market Size, Share, and Growth Forecast 2026 - 2033

High Performance Fibers Market by Product Type (Carbon Fiber, Polybenzimidazole, Aramid Fiber, M5/PIPD, Polybenzoxazole (PBO), Glass Fiber, High-strength Polyethylene, Others), Application (Electronics & Telecommunication, Textile, Aerospace & Defense, Construction & Building, Automotive, Sporting Goods, Others), and Regional Analysis for 2026 - 2033

High Performance Fibers Market Size and Trend Analysis

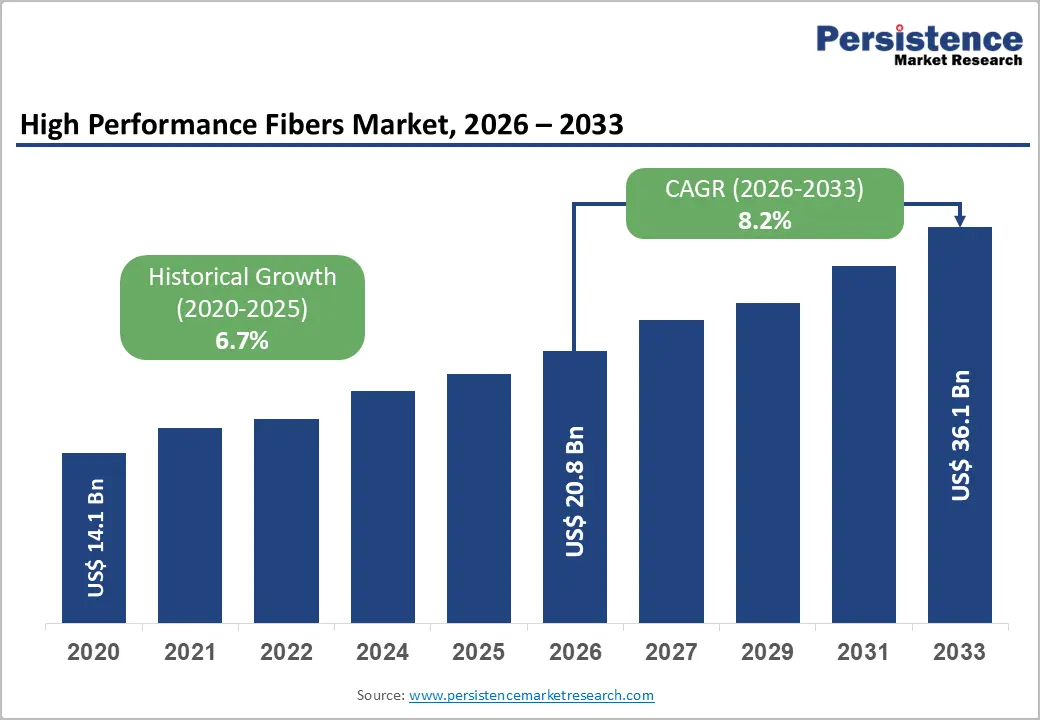

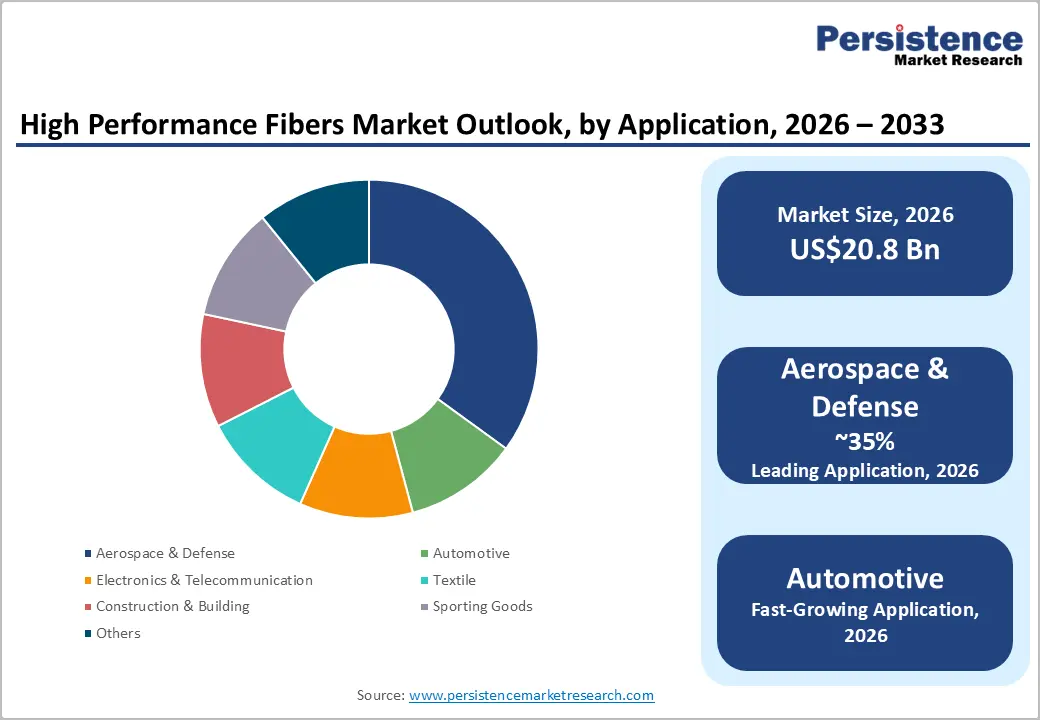

The global high-performance fibers market size is expected to be valued at US$ 20.8 billion in 2026 and is projected to reach US$ 36.1 billion by 2033, growing at a CAGR of 8.2% between 2026 and 2033.

High-performance fibers such as carbon fibers, aramid fibers, ultra-high molecular weight polyethylene (UHMWPE), PBI, PBO, and high-modulus glass fibers are increasingly replacing metals and conventional polymers due to their superior strength-to-weight ratios, thermal stability, and chemical resistance. The U.S. Department of Energy (DOE) estimates that a 10% reduction in vehicle weight can improve fuel economy by 6-8%, while advanced composites and high-performance fibers can reduce body and chassis weight by 30-50%, thereby boosting fuel efficiency by 20-25%. In modern commercial aircraft, composite materials already account for roughly 50% of structural weight, with carbon fiber-reinforced polymers dominating, directly linking high-performance fiber demand to global aircraft production cycles.

Key Industry Highlights:

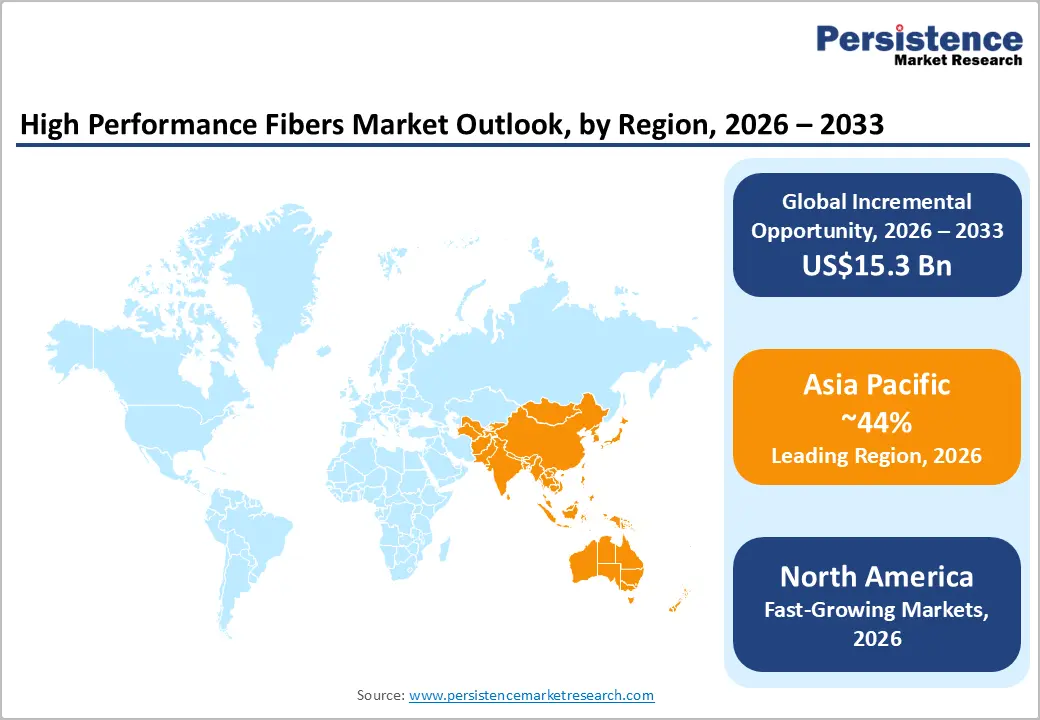

- Leading Region: Asia Pacific currently leads the high-performance fibers market, accounting for around 44% of global revenues in 2026, supported by China’s dominance in wind energy, EV production, and strategic investments in carbon fiber and UHMWPE capacity.

- Fastest-Growing Region: North America emerges as the fastest-growing region in the high-performance fibers market, due to U.S. aerospace innovation and defense spending exceeding USD 886 billion.

- Dominant Segment: Carbon fiber is the leading product type, holding about 38% of high-performance fiber revenues in 2026, thanks to its critical role in aircraft structures, EV lightweighting, wind blades, and high-end sporting goods.

- Fastest-Growing Segment: Automotive applications are the fastest-growing segment, driven

- by rising EV adoption and demand for lightweight battery enclosures, structural reinforcements, safety components, and thermally conductive materials.

- Key Opportunity: Protective textiles and ballistic armor, including body armor, helmets, and vehicle protection based on aramid and UHMWPE fibers, represent a major future opportunity, driven by rising security threats, stricter safety regulations, and innovation in lighter, smarter protective systems.

| Key Insights | Details |

|---|---|

| High Performance Fibers Market Size (2026E) | US$ 20.8 Bn |

| Market Value Forecast (2033F) | US$ 36.1 Bn |

| Projected Growth CAGR (2026 - 2033) | 8.2% |

| Historical Market Growth (2020 - 2025) | 6.7% CAGR |

Market Dynamics

Drivers - Surge in Lightweight Demand in Aerospace & Defense

The increasing adoption of high-performance fibers in aerospace and defense applications is a significant driver of market growth. These materials enable substantial weight reduction while preserving or enhancing structural durability and protective performance. According to the Aerospace Industries Association, the U.S. aerospace and defense sector generated more than US$ 955 billion in sales in 2023, reflecting a large and expanding installed base that relies heavily on carbon fiber, aramid fiber, and PBI/PBO composites for critical components such as aircraft structures, rotor blades, radomes, engine nacelles, and thermal protection systems.

The 30-50% weight savings achieved through carbon and aramid fibers improve fuel efficiency and performance. As investments rise in advanced fighters, unmanned platforms, and missile defense systems, many of which require materials capable of withstanding temperatures above 2,000°C, demand for ultra-high-modulus carbon fibers, ceramic fibers, and advanced aramids is expected to remain strong.

Electrification, EV Growth, and Renewable Energy Expansion

The accelerating electrification of transportation and the rapid expansion of wind energy are generating substantial demand for high-performance fibers. According to the International Energy Agency, global electric vehicle sales are projected to reach approximately 17 million units in 2024, up from 14 million in 2023, indicating that nearly one in five new cars sold worldwide is electric. Lightweight carbon and glass fiber composites play a vital role in EV battery enclosures, structural assemblies, and high-voltage insulation, thereby reducing battery mass and extending driving range. Regulatory frameworks such as the EU’s Euro-7 standards and China’s expanding electrification capacity further reinforce this trend.

Concurrently, the Global Wind Energy Council reports a record 117 GW of new wind installations in 2023, with China contributing about 75 GW. The use of high-modulus glass fibers, carbon fibers, and hybrid fabrics enables longer, lighter, and more durable turbine blades, firmly linking high-performance fiber demand with global decarbonization initiatives.

Restraint - High Material and Processing Costs vs. Conventional Alternatives

Despite their strong performance advantages, high-performance fibers remain considerably more expensive than commodity fibers, metals, and high-performance thermoplastics. Production costs for carbon fiber, aramid, PBI, and PBO fibers are elevated due to complex precursor chemistries, energy-intensive processes such as carbonization and graphitization, and rigorous quality-control requirements. Competing materials, such as advanced aluminum and magnesium alloys and engineering plastics, often provide adequate strength and thermal resistance at lower cost, thereby limiting broader adoption in price-sensitive automotive and construction applications.

High carbon-fiber production costs, driven by intricate manufacturing processes, low yields, and costly raw materials, further constrain adoption in general industrial applications. Although recycled carbon fiber offers meaningful cost and energy savings, its market penetration remains limited owing to standardization and quality concerns. Companies adopting automated fiber placement, thermoplastic prepregs, or integrated recycling processes may achieve cost advantages, while reliance on traditional prepreg technology continues to hinder growth in cost-sensitive sectors.

Supply Chain Concentration and Geopolitical Risks

Production of high-performance fibers, particularly carbon fiber, para-aramid, UHMWPE, and specialty glass fibers, is dominated by a small number of integrated manufacturers across Japan, North America, Europe, and China. Increasing trade protectionism, export controls, and regulatory measures, such as the EU’s Carbon Border Adjustment Mechanism (CBAM), are compelling producers to reassess their sourcing strategies and invest in regional manufacturing capacity.

Disruptions in precursor availability, energy price fluctuations, and logistics challenges can lead to extended lead times and heightened price volatility for downstream industries, including aerospace, automotive, and wind energy. Consequently, some OEMs are adopting multi-material strategies or delaying wider deployment of high-performance fibers in non-critical applications.

Opportunities - Next-Generation Aerospace, Space, and Defense Platforms

The shift toward more electric, autonomous, and sustainable aerospace and defense platforms is creating significant growth opportunities for high-performance fibers. As of 2024, the aerospace and defense sector accounts for approximately 35% of total demand, driven by extensive use in fuselages, wings, control surfaces, interior components, and ballistic protection systems. The Federal Aviation Administration reports that modern commercial aircraft incorporate nearly 50% by weight of composite materials, primarily carbon fiber-reinforced polymers, to achieve substantial fuel-efficiency gains.

Future applications, including lightweight cryogenic tanks for hydrogen-powered aircraft, reusable launch vehicles, hypersonic systems, and advanced thermal-protection solutions, will increasingly depend on PBI, PBO, ceramic fibers, and 3D woven carbon structures. Suppliers integrating material innovation with automated layup, out-of-autoclave processing, and digital certification workflows are poised to gain a competitive advantage as OEMs emphasize both performance and cost efficiency.

Protective Textiles, Ballistic Armor, and Smart High-Performance Fabrics

Protective clothing and ballistic armor present a substantial growth opportunity, particularly for aramid and UHMWPE fibers. Aramid fibers are expected to maintain strong demand across protective apparel, automotive components, and aerospace materials, with additional momentum from EV-related applications such as battery insulation. UHMWPE fibers, marketed under brands such as Dyneema and Spectra, offer exceptional performance, being up to 15 times stronger than steel and roughly 40% stronger than aramid on a weight basis, while remaining extremely lightweight. These characteristics make them well-suited for body armor, helmets, vehicle spall liners, high-strength ropes, and marine mooring systems.

Concurrently, research in smart textiles is expanding opportunities where high-performance fibers integrate sensors, conductors, or energy-storage elements. Rising security concerns and stricter safety regulations are expected to drive sustained demand for lighter, more comfortable, and multifunctional protective systems.

Category-wise Analysis

Product Type Insights

Carbon fiber continues to dominate the high-performance fibers market, accounting for approximately 38% of total demand. Its superior strength-to-weight ratio, stiffness, fatigue resistance, and thermal stability enable substantial weight reductions compared with metals, reinforcing its widespread adoption. According to the DOE, replacing steel with lightweight composites can reduce vehicle body and chassis weight by up to 50%, thereby enabling greater utilization of carbon fiber in EV platforms. In aerospace, where composites represent nearly half of structural weight in advanced programs, carbon fiber remains essential for primary structures and high-load components.

Premium high-modulus variants are priced between US$25 and US$35 per kilogram, while standard grades serve cost-sensitive sectors. Leading suppliers such as Toray, Mitsubishi Chemical, and Teijin benefit from integrated precursor supply chains. Aramid fibers retain a significant market share driven by defense and automotive lightweighting, while ultra-high-temperature fibers, glass fibers, and high-strength polyethylene address niche and cost-sensitive industrial applications.

Application Analysis

Aerospace and defense represent the largest application segment for high-performance fibers, accounting for roughly 35% of total demand. This leadership is driven by the need to reduce airframe and rotorcraft weight, improve fuel efficiency, and meet stringent performance and safety standards across commercial and military platforms. Carbon fiber, aramid, PBI, and ceramic fibers are extensively utilized in fuselage skins, wing structures, fairings, radomes, interior components, and protective systems. The Aerospace Industries Association reports that U.S. aerospace and defense sales exceeded US$955 billion in 2023, underscoring the sector’s scale and influence on global fiber consumption.

As fleets modernize and defense programs prioritize lighter, more resilient systems, the segment is expected to maintain its leading position. North America and Europe dominate current demand, while Asia-Pacific, particularly China, is rapidly expanding its presence in advanced composite platforms. Automotive applications form the fastest-growing segment, supported by rising EV adoption and demand for lightweight battery enclosures, structural reinforcements, safety components, and thermally conductive materials, with shorter development cycles favoring agile manufacturers in Asia-Pacific.

Regional Insights

North America High-Performance Fibers Market Trends

North America remains one of the most technologically advanced and high-value markets for high-performance fibers, with the United States serving as the primary driver of growth. The U.S. aerospace and defense sector generated over US$955 billion in sales in 2023 and supported 2.21 million jobs, driving substantial demand for carbon, aramid, UHMWPE, and specialty glass fibers used in aircraft, spacecraft, missiles, and military vehicles. High-performance fibers are integral to commercial airliners, business jets, rotorcraft, and multiple defense programs, where lightweight armor, structural composites, and high-temperature components are essential.

The region is also a significant market for electric vehicles and renewable energy. The United States accounted for nearly 10% of global EV sales in 2023, with supportive policies expected to sustain growth. In wind energy, the U.S. added approximately 6.4 GW of new capacity in 2023, reinforcing demand for high-modulus glass and carbon fibers in turbine blades and towers. A strong innovation ecosystem, robust intellectual-property protection, and stringent safety standards enable North American OEMs and Tier 1 suppliers to set global benchmarks for advanced fiber-reinforced systems, even as some production shifts to offshore facilities.

Europe High-Performance Fibers Market Trends

Advanced manufacturing, ambitious climate policies, and strict worker-safety regulations support Europe’s high-performance fibers market. The Global Wind Energy Council notes that Europe continues to expand its wind fleet, adding several gigawatts of new capacity annually and contributing to a global installed base exceeding 900 GW by the end of 2022, with strong momentum into 2023 and beyond. Germany, Spain, and the U.K. rely heavily on high-modulus glass and carbon fibers for onshore and offshore wind blades and structural components. The automotive sector, guided by EU CO2 fleet targets, increasingly uses carbon and aramid-reinforced composites to meet lightweighting and emissions goals.

Europe also leads in regulatory harmonization through the EU PPE Regulation and REACH, encouraging adoption of durable, high-performance fibers across firefighter gear, industrial PPE, and police armor. The upcoming Carbon Border Adjustment Mechanism (CBAM) will impose penalties on carbon-intensive imports, encouraging regional production of low-carbon carbon fiber and advanced composites.

Asia Pacific High-Performance Fibers Market Trends

Asia Pacific has emerged as the largest regional market for high-performance fibers, accounting for about 44% of global demand. This growth is supported by rapid industrialization, substantial infrastructure investment, and robust regional manufacturing capabilities. China alone added approximately 75 GW of new wind capacity in 2023, nearly 65% of global installations, highlighting the region’s central role in wind-energy expansion and its associated need for glass and carbon fibers.

China has also designated UHMWPE fiber as a strategic material under the “Made in China 2025” initiative, thereby accelerating production scale and innovation due to its exceptional strength. Additionally, China accounted for approximately 60% of global EV sales in 2023, with volumes projected to reach approximately 10 million units in 2024. Combined with expanding aerospace programs in China, Japan, and India, these factors solidify Asia Pacific’s position as both the largest consumption base and a rapidly advancing production hub for high-performance fibers.

Competitive Landscape

The high performance fibers market is moderately concentrated, with a mix of global leaders and regional specialists competing across carbon fiber, aramid, UHMWPE, glass fiber, and specialty polymer fibers. Major players such as Toray Industries, Inc., Teijin Ltd., DuPont de Nemours, Inc., Honeywell International Inc., DSM/Avient Corporation, Hexcel Corporation, Solvay, Owens Corning, SGL Carbon, Toyobo Co., Ltd., and Kolon Industries, Inc. leverage deep R&D capabilities, proprietary chemistries, and long-term aerospace and defense qualifications to defend share. Key strategies include capacity expansions in Asia, investments in recycling and low-carbon production, development of higher-modulus and higher-temperature fibers, and closer integration with composite part manufacturers. Emerging business models, such as “fiber-as-a-service” for armor integrators and co-development partnerships for 3D-printed composite parts, are gaining traction as end-users seek performance guarantees and lifecycle support rather than just material supply.

Key Developments:

- October 2025: Toray Industries has developed a low-temperature recycling technology that breaks down diverse CFRP waste while retaining over 95% of the original carbon-fiber strength and reducing CO2 emissions by more than half. The company has also created a high-quality recycled carbon-fiber nonwoven fabric suitable for automotive, construction, electronics, and consumer applications.

- September 2025: Teijin Carbon released its first sustainability report, highlighting major progress in circularity, climate action, and responsible operations across its global carbon-fiber business. The company introduced Tenax Next™, a new carbon-fiber line with up to 35% lower CO2 emissions, and launched a digital product passport for full lifecycle transparency.

- November 2025: DuPont Personal Protection introduced Tyvek® APX™, its most advanced disposable chemical-protective garment fabric, delivering unprecedented breathability without compromising protection or durability. Launched at A+A 2025 in Germany, the innovation addresses a major safety challenge by combining high comfort with high performance for workers in demanding environments.

Top Companies in High-Performance Fibers Market

- Toray Industries, Inc. (Tokyo, Japan) is a global leader in carbon fiber and advanced composite materials, supplying aerospace OEMs, automotive manufacturers, wind energy firms, and sporting goods brands. Its portfolio spans TORAYCA carbon fiber, prepregs, woven fabrics, and thermoplastic composites, backed by significant R&D and global manufacturing in Japan, Europe, North America, and Asia.

- Teijin Ltd. (Tokyo, Japan) is a key producer of high-performance fibers, including aramid (e.g., Twaron, Technora), carbon fiber, and high-performance polyester. The company holds strong positions in protective clothing, aerospace composites, and industrial applications, and is investing in recycled fibers and advanced fabrics to meet sustainability and performance requirements across Europe, North America, and Asia.

- DuPont de Nemours, Inc. (Wilmington, Delaware, U.S.) pioneered aramid fibers such as Kevlar and Nomex, which remain benchmarks in ballistic protection, firefighter gear, and high-temperature insulation. The company’s high-performance materials portfolio spans aramids, advanced engineering polymers, and barrier materials, giving it a broad footprint in aerospace, automotive, oil and gas, and electrical markets. Long-standing relationships with defense agencies and PPE manufacturers make DuPont one of the most influential players in the high-performance fibers ecosystem.

Companies Covered in High Performance Fibers Market

- Toray Industries, Inc.

- Teijin Ltd.

- DuPont de Nemours, Inc.

- DSM / Avient Corporation

- Honeywell International Inc.

- Hexcel Corporation

- Solvay

- Owens Corning

- SGL Carbon

- Toyobo Co., Ltd.

- Kolon Industries, Inc.

- Huvis Corp.

- Mitsubishi Chemical Corporation

- Yantai Tayho Advanced Materials Co., Ltd.

- PBI Performance Products, Inc.

Frequently Asked Questions

The global high-performance fibers market is expected to reach around US$ 20.8 Bn in 2026 and approximately US$ 36.1 Bn by 2033, implying a robust CAGR of about 8.2% over 2026-2033, building on the historical growth of around 6.7% between 2020 and 2025.

Key demand drivers include lightweighting and fuel‑efficiency targets in aerospace and automotive, rapid EV adoption, and expansion of wind power and other renewables. A 10% weight reduction can improve vehicle fuel economy by 6-8%, while modern aircraft structures incorporate roughly 50% composite materials by weight, cementing the role of carbon, aramid, and other high performance fibers.

Aerospace and defense is the leading application segment, accounting for roughly 35% of global high performance fiber demand, driven by the need for lighter airframes, rotorcraft blades, missile structures, space systems, and high‑performance ballistic and thermal protection.

Asia Pacific currently leads the global market, representing about 44% of revenues in 2026, supported by China’s dominance in wind installations (around 75 GW of new capacity in 2023) and its large share of global EV production and sales, alongside strong contributions from Japan, South Korea, and India.

Protective textiles and ballistic armor, spanning military and law‑enforcement body armor, helmets, vehicle armor, and industrial PPE, offer major growth potential as security threats rise and regulations tighten. Advanced aramid and UHMWPE fibers, which can be up to 15 times stronger than steel, enable lighter, more comfortable, and smarter protective systems.

Leading players include Toray Industries, Inc., Teijin Ltd., DuPont de Nemours, Inc., Honeywell International Inc., Hexcel Corporation, Solvay, Owens Corning, SGL Carbon, Toyobo Co., Ltd., Kolon Industries, Inc., and PBI Performance Products, Inc., among others.