- Advanced Materials

- Anti-reflective Coatings Market

Anti-reflective Coatings Market Size, Share, and Growth Forecast 2026–2033

Anti-reflective Coatings Market by Product Type (Single-layer Coatings, Multi-layer Coatings), Technology (Electron Beam Evaporation, Sputtering, Vacuum Deposition, Others), Substrate (Glass, Plastic, Others), Application (Eyewear, Electronics, Solar Panels, Automotive, Others), and Regional Analysis, 2026–2033

Anti-reflective Coatings Market Size and Trend Analysis

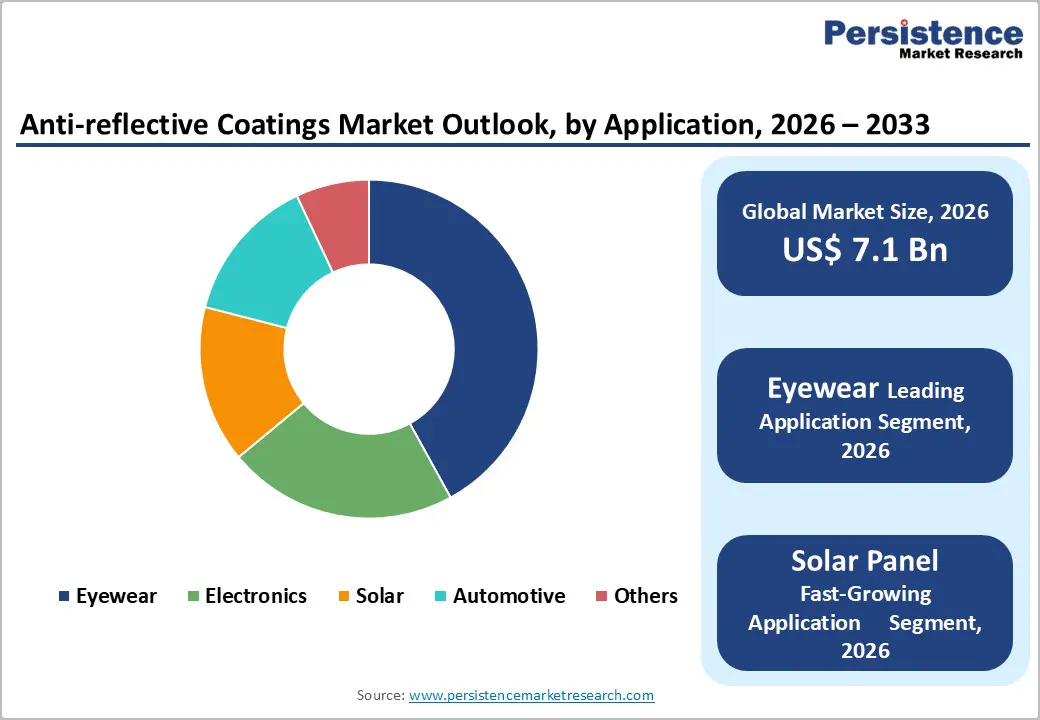

The global anti-reflective coatings market size is expected to be valued at US$ 7.1 billion in 2026 and projected to reach US$ 12.3 billion by 2033, growing at a CAGR of 8.2% between 2026 and 2033. This robust growth trajectory is driven by the accelerating global deployment of solar photovoltaic systems, rising consumer demand for high-performance optical eyewear, and the electronics industry's relentless drive toward brighter, glare-free display surfaces.

The demand is further reinforced by automotive ADAS camera integration, where anti-reflective coatings on optical sensors and head-up display substrates are essential for system reliability, and by expanding government-mandated renewable energy targets that are requiring record solar panel installations worldwide, collectively creating a diversified, technology-driven demand base with strong multi-decade visibility.

Key Industry Highlights:

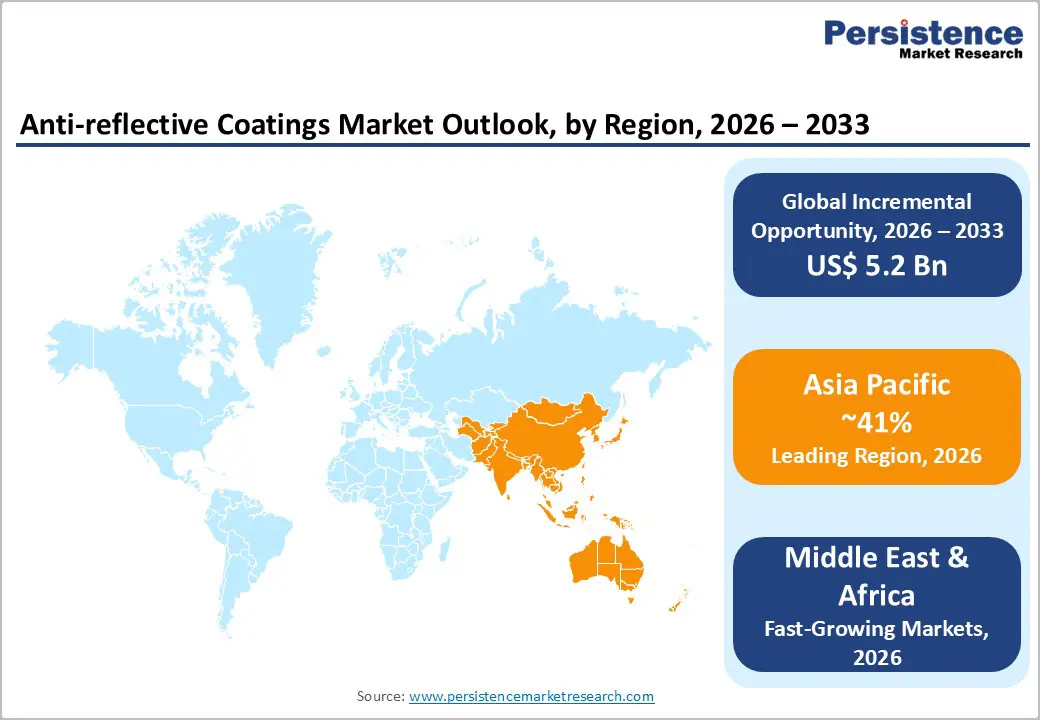

- Leading Region: Asia Pacific is likely to register 41% share in 2026, led by China's dominance in solar PV glass coating and Japan's world-class precision ophthalmic and electronics AR coating technology ecosystem.

- Fastest Growing Market: The Middle East & Africa region is projected to record the highest CAGR through 2033, driven by GCC solar megaproject pipelines, Saudi Arabia's Vision 2030 renewable energy investments, and Africa's expanding solar energy access programs.

- Dominant Application Type: Eyewear leads the application segment with approximately 37% market share in 2026, anchored by over one billion prescription lenses produced annually globally, near-universal AR coating adoption in premium lens categories, and recurring replacement demand cycles.

- Fastest Growing Type: Solar panel AR coatings are forecast to grow at approximately 10% CAGR (2026–2033), propelled by IEA record solar capacity additions, EU REPowerEU's 600 GW target, and India's MNRE 500 GW renewable energy mandate.

- Key Opportunity: The automotive ADAS revolution, with EU General Safety Regulation 2019/2144 mandating advanced sensor systems in all new vehicles, is creating a premium, durability-certified AR coating demand stream for camera, LiDAR, and HUD optical components across all major vehicle platforms.

DRO Analysis

Drivers - Rapid Global Solar Energy Expansion is Accelerating Demand for High-Efficiency Anti-reflective Coatings

The global transition to renewable energy represents the most powerful structural demand driver for the anti-reflective coatings market, as solar photovoltaic (PV) module manufacturers are among the largest and fastest-growing consumers of precision optical coatings that maximize light transmission and minimize reflection losses. Anti-reflective coatings applied to solar glass can improve module energy output by 2–4 percentage points according to research published by the Fraunhofer Institute for Solar Energy Systems (ISE), a performance gain that is commercially decisive in a highly competitive industry where every efficiency increment commands a price premium.

The International Energy Agency (IEA) reported that solar PV added a record 295 GW of new capacity globally in 2022, and its Net Zero by 2050 scenario requires solar capacity to exceed 14,000 GW by mid-century, implying decades of compounding demand for high-performance AR-coated solar glass. China, the EU, and the U.S. are all operating under statutory renewable energy targets that translate directly into capital expenditure on solar installations with AR-coated module fronts.

Global Eyewear Industry Growth and Premium Lens Upgrade Cycles Are Sustaining High-Volume AR Coating Consumption

The global eyewear market is a structurally growing application base for anti-reflective coatings, driven by rising global myopia prevalence, which the Brien Holden Vision Institute projects will affect approximately 50% of the world's population by 2050, and the accelerating consumer shift toward premium, digitally optimized lenses that reduce screen glare and blue light reflection. Anti-reflective coatings have transitioned from an optional eyewear accessory to an expected standard feature on prescription lenses in developed markets, with Euromonitor International data indicating that premium lens adoption rates in Western Europe and North America consistently exceed 65% of prescription lens volumes.

EssilorLuxottica, the world's largest eyewear group, has publicly stated that over 90% of its premium Varilux and Crizal branded lenses incorporate multi-layer AR coating systems, illustrating the depth of coating penetration in the premium segment. Digital device proliferation and aging demographics in Asia and Europe are structural tailwinds that will sustain eyewear AR coating volume growth through the forecast period.

Restraints

High Capital Cost of Physical Vapor Deposition Equipment Creates Significant Barriers to Entry and Capacity Expansion

The most precise and durable anti-reflective coating systems, produced via electron beam evaporation, magnetron sputtering, and ion-assisted deposition, require sophisticated high-vacuum physical vapor deposition (PVD) equipment that carries substantial capital investment requirements, typically ranging from USD 500,000 to over USD 5 million per coating chamber, depending on capacity and specification.

This high capex threshold creates meaningful barriers for smaller manufacturers seeking to enter the market or expand capacity and imposes long payback periods that reduce agility in responding to demand shifts across application segments. For developing market manufacturers, access to qualified PVD equipment, trained process engineers, and the precision metrology required for optical performance validation compounds the entry challenge significantly.

Durability and Scratch-Resistance Limitations of AR Coatings Constrain Adoption in Harsh-Environment Applications

Despite significant advances in hard-coat overcoating technologies, anti-reflective coatings remain susceptible to abrasion, chemical attack, and delamination in demanding field environments, a limitation that restricts their adoption in certain automotive exterior, industrial, and military-grade optical applications. Standard eyewear AR coatings show measurable degradation under repeated cleaning with inappropriate materials, and solar module AR coatings exposed to sand abrasion in desert environments can lose significant transmission performance over time.

The European Commission's JRC has documented AR coating degradation as a contributor to long-term solar module output decline in arid-climate installations, creating procurement hesitancy among solar developers operating in high-soiling environments.

Opportunities - Solar Panel AR Coating Segment Offers the Highest-Growth Revenue Opportunity Driven by Global Renewable Energy Mandates

The solar panels application segment is the fastest-growing end-use for anti-reflective coatings, forecast to expand at approximately 10% CAGR as record solar installation pipelines worldwide require progressively larger volumes of AR-coated module glass. The European Union's REPowerEU plan targets 600 GW of solar capacity by 2030, nearly tripling 2022 installed capacity, while India's Ministry of New and Renewable Energy (MNRE) targets 500 GW of renewable capacity by 2030, with solar comprising the majority. These statutory targets are translating into unprecedented solar glass production expansion, with China's solar glass industry operating at record output levels per the China Building Material Federation.

Advanced nanostructured and sol-gel AR coating technologies, which can achieve reflectance values below 0.5% on solar glass versus the standard 3–4% untreated glass reflectance, represent a premium technology differentiation opportunity for coating manufacturers who invest in next-generation deposition process development and long-term supply agreements with Tier-1 solar module manufacturers.

Automotive ADAS and Heads-Up Display Integration Is Opening a Premium Technology-Intensive Growth Segment for AR Coating Suppliers

The automotive sector's rapid integration of Advanced Driver Assistance Systems (ADAS), including LiDAR, camera arrays, and head-up displays (HUD), is creating a high-value, technically demanding growth segment for anti-reflective coating manufacturers with precision optical deposition capabilities. Every camera lens cover, HUD combiner glass, and LiDAR dome window in a modern ADAS-equipped vehicle requires AR coatings engineered to specific bandwidths and environmental durability standards, and the proliferation of sensors per vehicle is compounding coating volume requirements rapidly.

The European Automobile Manufacturers' Association (ACEA) projects that virtually all new passenger vehicles sold in the EU will incorporate advanced ADAS features by 2030 under the General Safety Regulation (EU) 2019/2144, mandating Intelligent Speed Assistance, Emergency Lane Keeping, and Advanced Emergency Braking as standard. Manufacturers who qualify their AR coating materials and processes to automotive AEC-Q grade standards and establish long-term supply agreements with Tier-1 optics suppliers to automotive OEMs are well-positioned to capture this premium, durability-sensitive demand stream.

Category-wise Analysis

Product Type Insights

Multi-layer coatings lead the product type segment with approximately 68% market share in 2026, a dominance rooted in their superior optical performance compared with single-layer designs, particularly their ability to achieve broadband anti-reflection across the full visible spectrum (380–780 nm) rather than at a single design wavelength. In precision optical applications, including premium eyewear, semiconductor lithography optics, and high-efficiency solar modules, multi-layer quarter-wave stack designs can achieve residual reflectance below 0.2% across the entire visible range, a performance that single-layer coatings based on quarter-wave magnesium fluoride (MgF2) simply cannot replicate across broad spectral bands.

The premium eyewear segment, led by EssilorLuxottica's Crizal and Hoya Corporation's HiVision product families, specifies multi-layer AR stacks as a non-negotiable performance standard, reinforcing high-value volume demand for multi-layer deposition processes.

Technology Insights

Electron Beam (E-beam) Evaporation leads the deposition technology segment with approximately 44% market share in 2026, reflecting its entrenched position as the industry-standard process for high-precision optical coating production across eyewear, semiconductors, and photonics applications. E-beam evaporation enables precise control of film thickness at the sub-nanometer level, critical for meeting the demanding optical performance tolerances of premium ophthalmic and precision instrument coatings, and supports the broad range of oxide, fluoride, and nitride coating materials required across application segments.

The technology's decades-long operational track record in large-format optical coating houses, combined with the extensive infrastructure investment already made by leading producers, including Carl Zeiss AG and Hoya Corporation, creates high switching costs that entrench E-beam's market leadership. Sputtering technology is the fastest-growing deposition method, driven by its advantages for large-area solar glass and flat-panel display substrates.

Substrate Insights

Glass substrates lead the substrate segment with approximately 57% market share in 2026, underpinned by its dominant role across the three largest AR coating application segments: solar module front glass, precision ophthalmic lenses manufactured in mineral glass, and high-performance optical instruments. Glass substrates offer thermal stability during high-temperature deposition processes, enabling the use of a wider range of coating materials including dense oxide films that provide superior environmental durability, and their chemical inertness ensures long-term adhesion integrity critical for outdoor applications such as solar panels.

Corning Incorporated's Gorilla Glass and Schott AG's optical glass product lines serve as high-value substrates for electronics and precision optics applications, respectively, with AR coating integrated as a value-adding process step. Plastic substrates are the fastest-growing segment, driven by the rapid growth of lightweight plastic ophthalmic lenses.

Application Insights

Eyewear leads the application segment with approximately 37% market share in 2026, reflecting the scale and consistency of prescription lens production globally, estimated at over 1 billion pairs of corrective lenses produced annually per the Vision Council of America, and the near-universal adoption of AR coatings as a standard feature on premium and mid-range lens products. The eyewear application benefits from a recurring replacement cycle driven by prescription changes and lens wear, generating predictable high-volume consumable demand for AR coating materials and services.

The convergence of progressive lens design, blue light filtering functionality, and anti-reflective performance into integrated multi-functional coating stacks, exemplified by EssilorLuxottica's Crizal Prevencia and Zeiss DuraVision BlueGuard products, is elevating the value per lens coated and driving revenue growth beyond volume. Solar panels represent the fastest-growing application, expanding at approximately 10% CAGR through 2033.

Regional Analysis

North America Anti-Reflective Coatings Market Trends and Insights

North America is a mature, innovation-led market for anti-reflective coatings, shaped by strong premium eyewear penetration, world-class semiconductor and photonics industries, and rapidly expanding solar energy deployment under the Inflation Reduction Act (IRA), which allocated USD 369 billion to clean energy investments. The U.S. solar installation market is experiencing record growth under IRA incentives, directly driving demand for AR-coated solar module glass, while the premium ophthalmic lens market sustains consistent high-value AR coating consumption.

U.S. Anti-reflective Coatings Market Size

The United States holds approximately 80% of the North American anti-reflective coatings market, anchored by its large prescription eyewear market, with 210 million Americans requiring corrective lenses per Vision Council of America data, and the world's most active solar energy deployment pipeline, increasingly supported by domestically manufactured solar glass following IRA domestic content requirements. The U.S. is also home to precision optics leaders, including Corning and II-VI Incorporated, reinforcing demand for high-performance AR coating materials.

Europe Anti-reflective Coatings Market Trends and Insights

Europe is the global center of gravity for premium optical coating technology, anchored by world-leading eyewear, photonics, and precision instrument industries concentrated in Germany, France, and the Netherlands. The EU's REPowerEU solar expansion target of 600 GW by 2030 is a major catalyst for solar glass and AR coating demand, while the ADAS mandate under EU General Safety Regulation 2019/2144 is opening new high-value coating application segments. European coating manufacturers lead in precision deposition technology, IP, and process innovation.

Germany Anti-reflective Coatings Market Size

Germany commands approximately 25% of the European anti-reflective coatings market, home to global leaders Carl Zeiss AG, Rodenstock GmbH, and Schott AG, collectively representing the densest concentration of precision optical coating expertise globally. Germany's automotive industry, undergoing rapid ADAS integration, is an expanding adjacent demand source for AR-coated camera and sensor optics. Germany's Energiewende solar expansion further amplifies domestic AR coating demand for solar glass applications.

U.K. Anti-reflective Coatings Market Size

The United Kingdom accounts for approximately 12% of the European market. The U.K.'s strong healthcare and National Health Service (NHS) prescription eyewear distribution network sustains consistent demand for AR-coated ophthalmic lenses, and the country's ambitious solar deployment targets, 70 GW by 2035 under the British Energy Security Strategy, are increasingly driving solar glass AR coating procurement. UK-based photonics and defense optics sectors add a premium, low-volume, high-value demand layer.

France Anti-reflective Coatings Market Size

France represents approximately 14% of the European anti-reflective coatings market, anchored by the global headquarters of EssilorLuxottica, the world's dominant ophthalmic lens and coating company, in Paris and Saint-Honoré. France's significant solar PV expansion programme under the Programmation Pluriannuelle de l'Énergie (PPE) and its growing automotive AR optics demand from Stellantis and Renault Group ADAS programs further diversify France's strong market position.

Asia Pacific Anti-reflective Coatings Market Trends and Insights

Asia Pacific leads the global anti-reflective coatings market with approximately 41% market share in 2026, driven by China's dominance as the world's largest solar PV manufacturer and installer, Japan's world-class precision optics industry, and South Korea's and Taiwan's leading electronics display manufacturing ecosystems. China accounts for approximately 55% of regional demand, with its solar glass producers, including Xinyi Solar and Flat Glass Group, operating the world's largest AR coating capacity for solar module glass. India and Southeast Asia are emerging as high-growth secondary markets driven by solar expansion and electronics manufacturing investment.

India Anti-reflective Coatings Market Size

India holds approximately 12% of the Asia Pacific anti-reflective coatings market, with demand primarily concentrated in solar energy and eyewear applications. India's National Solar Mission under the PM Surya Ghar Muft Bijli Yojana and MNRE's 500 GW renewable target are driving large-scale solar glass procurement, while India's growing domestic ophthalmic lens manufacturing industry, exporting globally, is expanding its use of AR coating services. India is emerging as a competitive AR coating services hub for the South Asian market.

Japan Anti-reflective Coatings Market Size

Japan accounts for approximately 18% of Asia Pacific's anti-reflective coatings market, underpinned by its world-leading precision optics industry. Hoya Corporation and Nikon are global leaders in ophthalmic and industrial AR coating technology, and Japan's advanced display manufacturing sector, producing OLED and microLED panels, is an intensive user of precision AR deposition technology. Dexerials Group (Sony) produces specialized optical functional films, including AR-integrated products for electronics display applications.

Southeast Asia Anti-reflective Coatings Market Size

Southeast Asia represents approximately 10% of the Asia Pacific anti-reflective coatings market and is among the region's fastest-growing sub-markets. Vietnam, Malaysia, and Thailand are expanding electronics and display manufacturing capacity, attracting foreign direct investment from Korean and Taiwanese display OEMs, while solar energy deployment across ASEAN nations is escalating under national renewable energy targets. These dual growth vectors are creating compounding demand for AR coating materials and services across the sub-region.

Competitive Landscape

The global anti-reflective coatings market is moderately consolidated at the premium technology tier, with EssilorLuxottica, Carl Zeiss AG, Hoya Corporation, AGC Group, and Saint-Gobain collectively commanding an estimated 45–50% of total market revenue through deep OEM integration, proprietary multi-layer coating formulations, and global optical coating service infrastructure. Strategic differentiation among leader’s centers on nano-structured coating architectures, sol-gel wet-process technology for solar glass, and ion-assisted deposition systems for precision optical applications.

Emerging competitive themes include sustainability-driven sol-gel process adoption, which reduces vacuum energy consumption versus PVD, and vertical integration of coating services into ophthalmic lens supply chains. Chinese domestic producers are intensifying cost competition in solar glass and standard ophthalmic segments, compelling Western incumbents to accelerate premium innovation cycles.

Key Developments

- In March 2025, EssilorLuxottica launched its Crizal Rock UV ultra-hardened anti-reflective coating range, incorporating a new nanocomposite overcoat layer that extends lens scratch resistance by a claimed 40% versus the previous generation, targeting premium prescription lens markets in North America and Europe.

- In November 2024, AGC Group announced the commercial launch of its SOLITE-AR solar glass product, incorporating a next-generation sol-gel anti-reflective coating achieving transmittance above 96%, targeting utility-scale solar module manufacturers in China, Europe, and the U.S. market.

- In June 2024, Carl Zeiss AG unveiled its ZEISS DuraVision Platinum UV multi-layer AR coating system with integrated UV-blocking and blue light management for premium progressive lenses, receiving UV400 protection certification from the International Commission on Non-Ionizing Radiation Protection (ICNIRP).

Global Anti-reflective Coatings Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 4.6 Billion |

|

Current Market Value (2026) |

US$ 7.1 Billion |

|

Projected Market Value (2033) |

US$ 12.3 Billion |

|

CAGR (2026–2033) |

8.2% |

|

Leading Region |

Asia Pacific, 41% market share (2026) |

|

Dominant Category – Application |

Eyewear, ~37% market share (2026) |

|

Top-Ranking Category – Product Type |

Multi-layer Coatings, ~68% market share (2026) |

|

Incremental Opportunity (2026–2033) |

US$ 5.2 Billion |

Companies Covered in Anti-reflective Coatings Market

- EssilorLuxottica

- Carl Zeiss AG

- PPG Industries

- Saint-Gobain

- AGC Group

- Corning Incorporated

- Hoya Corporation

- BASF SE

- Nippon Sheet Glass (NSG Group)

- Schott AG

- Rodenstock GmbH

- Brewer Science, Inc.

- Materion Corporation

- Dexerials Group (Sony)

- Nissan Chemical Corporation

Frequently Asked Questions

The global anti-reflective coatings market is valued at approximately US$ 7.1 billion in 2026, growing from US$ 4.6 billion in 2020 at a historical CAGR of 7.5% (2020–2025). The market is projected to reach US$ 12.3 billion by 2033, expanding at a CAGR of 8.2%, driven by solar energy expansion, premium eyewear growth, and rising demand from automotive ADAS and electronics display manufacturing.

The primary demand drivers are the global solar PV expansion, with the IEA reporting a record 295 GW of new solar capacity added in 2022 and projecting over 14,000 GW by 2050 under its Net Zero scenario, rising myopia prevalence driving premium AR-coated lens adoption globally, and the automotive industry's integration of ADAS camera and HUD systems mandated.

Asia Pacific leads the global anti-reflective coatings market with approximately 41% market share in 2026. China is the dominant country within the region, accounting for approximately 55% of regional demand.

The most significant near-term opportunity is in the solar panels application segment, forecast to grow at approximately 10% CAGR through 2033. The EU's REPowerEU 600 GW solar target, India's MNRE 500 GW renewable energy programme, and record U.S. solar deployment under the Inflation Reduction Act are collectively creating unprecedented solar glass procurement volumes.

The leading companies in the anti-reflective coatings market include EssilorLuxottica, Carl Zeiss AG, Hoya Corporation, AGC Group, Saint-Gobain, Corning Incorporated, Schott AG, PPG Industries, Nippon Sheet Glass (NSG Group), Rodenstock GmbH, Materion Corporation, and Dexerials Group (Sony).