- Smart Packaging

- Heat Transfer Film Market

Heat Transfer Film Market Size, Share, and Growth Forecast, 2026 - 2033

Heat Transfer Film Market by Film Type (Polyurethane-based, Polyester-based, PVC-based, Others), Backing Type (Cold Peel, Hot Peel, Others), Application, and Regional Analysis for 2026 - 2033

Heat Transfer Film Market Size and Trends Analysis

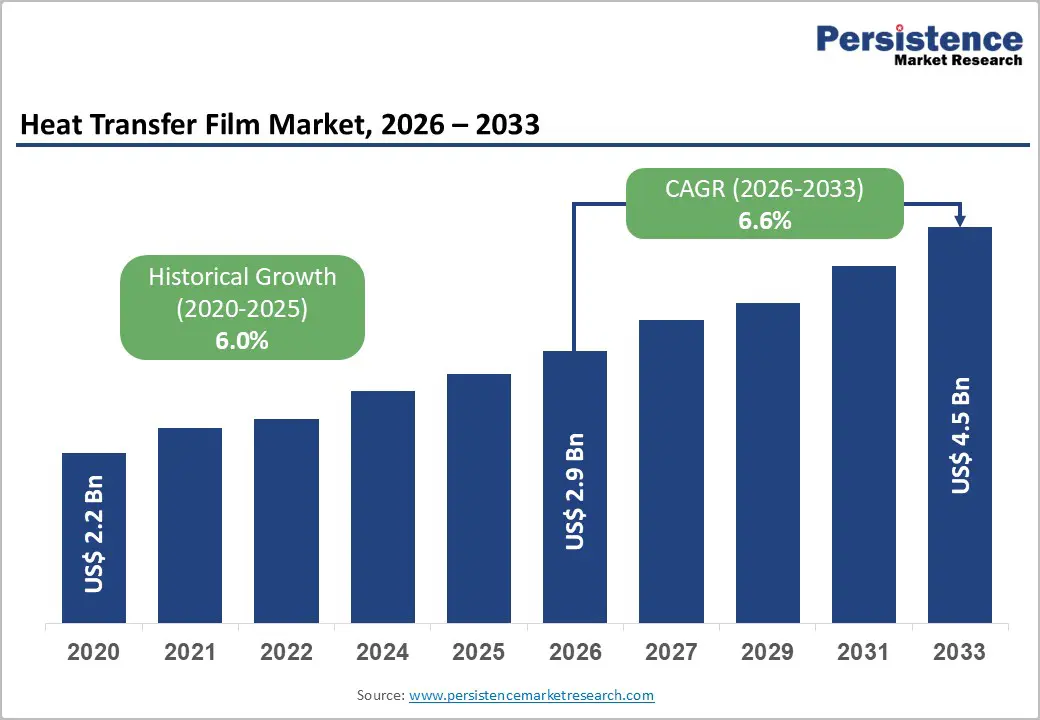

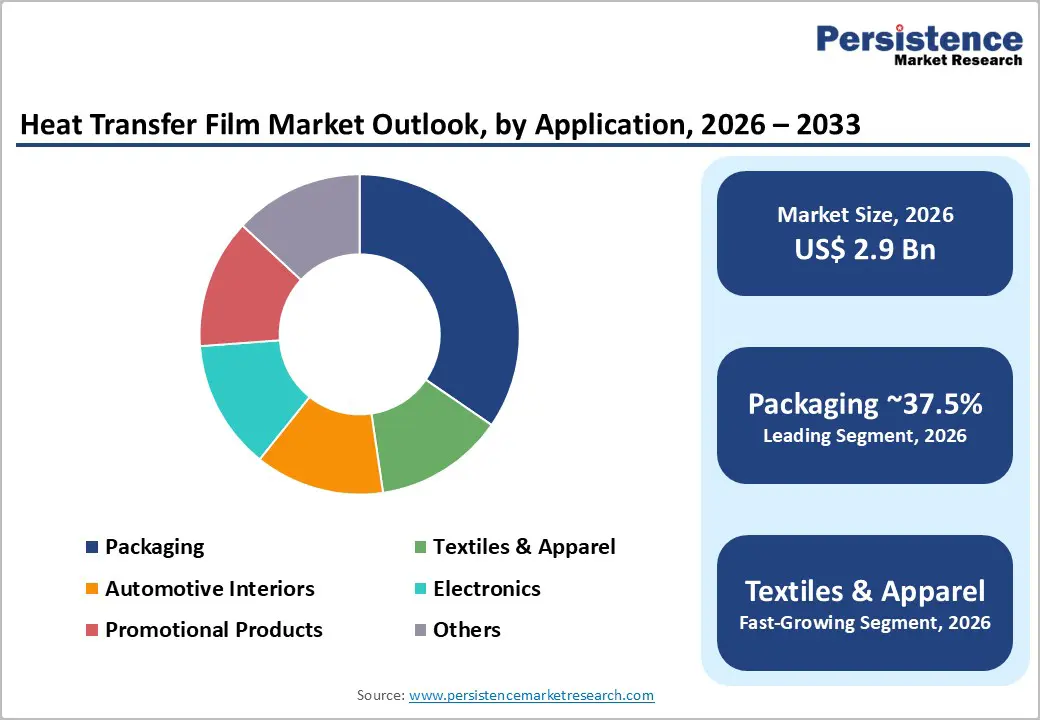

The global heat transfer film market size is likely to be valued at US$ 2.9 billion in 2026 and is expected to reach US$4.5 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033, driven by rising customization in apparel, premiumization in branded packaging, and a material shift toward polyurethane (PU) and polyester-based systems that offer durability and regulatory compliance advantages over legacy PVC films.

Heat transfer films enable the transfer of printed graphics or functional coatings onto substrates such as textiles, packaging materials, electronics components, and automotive interiors through controlled heat and pressure. While raw material volatility and recycling regulations introduce operational complexity, technological innovation and Asia Pacific manufacturing efficiencies sustain long-term expansion.

Key Industry Highlights:

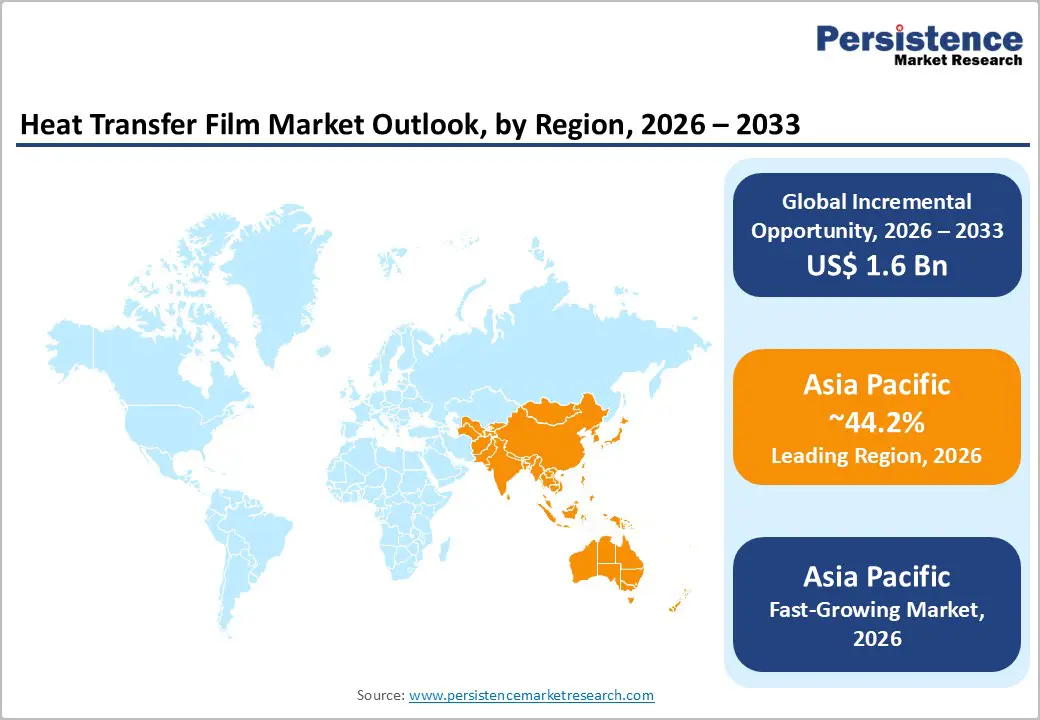

- Leading Region: Asia Pacific is projected to account for approximately 44.2% of the market share, driven by large-scale textile manufacturing in China, strong apparel export growth in India and ASEAN, and expanding PU and polyester production capacity across the region.

- Fastest-growing Region: Asia Pacific is expected to record the highest growth rate over the forecast period, supported by garment export expansion, athleisure demand, and continued investments in automated garment decoration and specialty film extrusion technologies.

- Investment Plans: Focus on PU and polyester capacity expansion, low-VOC adhesive reformulation, and recyclable mono-material film solutions. Companies across North America and Europe are investing in sustainable specialty films aligned with EPR and traceability standards, while Asian manufacturers are upgrading automation and digital transfer technologies.

- Dominant Film Type: Polyurethane-based films are anticipated to hold approximately 53.7% market share due to superior flexibility, abrasion resistance, soft-touch finish, and compatibility with premium sportswear and high-end packaging applications.

- Leading Application: Packaging is expected to account for 37.5% of market share, driven by decorative labeling, metallic finishes, premium FMCG branding, and durable graphics for rigid and flexible packaging formats.

| Key Insights | Details |

|---|---|

| Heat Transfer Film Market Size (2026E) | US$2.9 Bn |

| Market Value Forecast (2033F) | US$4.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Material Substitution toward Polyurethane and Engineered Polyesters

Polyurethane-based heat transfer films account for 53.7% of global demand, making PU the leading material category. The shift from PVC toward PU and polyester systems reflects evolving regulatory standards and performance requirements. PU offers superior flexibility, abrasion resistance, elasticity, and print adhesion compared to PVC, making it particularly suitable for sportswear, athleisure, and high-contact packaging surfaces. In regions with tightening environmental and chemical regulations, brand owners increasingly specify low-VOC and phthalate-free materials. This accelerates PU adoption and supports premium pricing. Polyester-based films are also gaining traction due to thermal stability and solvent resistance. The combined impact of performance differentiation and compliance alignment positions material substitution as a structural driver contributing significantly to the projected 6.6% CAGR through 2033.

Expansion of Branded Packaging and Graphic Differentiation

Packaging represents the largest application segment, accounting for 37.5% of market share in 2026. Consumer packaged goods (CPG) companies increasingly rely on high-quality decorative labeling to enhance shelf visibility and brand recognition. Heat transfer films enable metallic finishes, tactile effects, and durable graphics that are difficult to achieve through direct printing on certain substrates. Premiumization trends across food, beverage, cosmetics, and personal care segments support demand for advanced label finishes. Short production runs and product variants also favor transfer technologies due to cost efficiency in design changes. As packaging volumes grow globally and design complexity increases, heat transfer films benefit from parallel expansion, particularly in specialty and high-margin decorative applications.

Customization and On-Demand Textile Printing

Textiles and apparel represent the fastest-growing application category, accounting for a 25-30% share in 2026. Growth is fueled by athleisure expansion, personalization trends, and the rise of e-commerce-driven small-batch production. Heat transfer films enable flexible production runs with minimal setup time compared to traditional screen printing, particularly for specialty finishes such as metallic, flocked, reflective, or textured effects. Customization is now embedded in apparel business models, especially among digitally native brands. Manufacturers in the Asia Pacific leverage heat transfer technologies to support export-driven garment production with fast turnaround cycles. The ability to deliver high-resolution graphics with durability and wash resistance strengthens long-term demand across both developed and emerging markets.

Barrier Analysis - Raw Material Price Volatility and Supply Chain Exposure

Heat transfer film production depends on petrochemical-derived inputs, including polyols, polyester resins, PVC compounds, adhesives, and release liners. Price fluctuations in crude oil derivatives directly influence input costs. Manufacturers without long-term supply contracts or hedging mechanisms may experience margin compression during price spikes. Supply chain concentration in specific geographic regions further exposes producers to logistical disruptions. Shipping volatility, port congestion, and regional feedstock shortages can delay production cycles and reduce capacity utilization. These structural risks moderate near-term growth and increase capital intensity for smaller manufacturers.

Regulatory Compliance and Recycling Complexity

Regulatory pressure on recyclability and restricted chemical substances particularly affects PVC-based films. In Europe and North America, environmental directives and brand-level sustainability commitments require enhanced traceability and material disclosure. Heat-transfer films that permanently bond to substrates can complicate recycling streams, especially in mono-material packaging systems. Compliance requirements elevate R&D costs and extend customer qualification cycles. Manufacturers must invest in alternative chemistries and recyclable adhesives to remain competitive. Without such investments, suppliers risk exclusion from premium brand supply chains.

Opportunity Analysis - Recyclable and Bio-Based Film Development

The transition toward circular economy frameworks creates significant opportunities for recyclable and bio-based heat transfer films. Solutions compatible with mechanical recycling processes or chemical recovery systems will gain preference among global brands. Innovation in adhesive systems and film separability can address current recycling challenges. Early adoption of certified recyclable grades enables suppliers to secure long-term supply contracts with multinational packaging and apparel brands. Sustainable product portfolios also enhance pricing power and strengthen brand equity among environmentally conscious consumers.

High-Performance Films for Electronics and Automotive Applications

Emerging demand for decorative and functional overlays in electronics and automotive interiors presents a high-margin opportunity. Heat transfer films are used for surface finishes, tactile coatings, branding elements, and lightweight decorative layers in consumer electronics housings and vehicle cabins. Miniaturization trends in electronics and lightweighting initiatives in automotive manufacturing require thin-gauge, heat-stable, and durable films. Suppliers capable of engineering thermally resistant PU- or polyester-based films with advanced adhesion properties can capture specialized niches at higher average selling prices than in textile applications.

Category-wise Analysis

Film Type Insights

Polyurethane (PU)-based films are anticipated to account for approximately 53.7% of the market share in 2026, reflecting their superior balance of flexibility, durability, and aesthetic performance. PU films provide an excellent soft-touch hand feel in textile applications while delivering strong abrasion resistance and elongation properties in packaging and specialty labeling uses. Their compatibility with low-VOC and solvent-free adhesive systems aligns well with tightening environmental regulations across Europe and North America, where compliance with REACH and similar standards remains critical. Converters favor PU due to its high elasticity and recovery characteristics, making it particularly suitable for sportswear, stretch fabrics, and compression garments. For instance, global sportswear brands such as Nike and Adidas extensively use PU-based heat transfer films for logos and performance graphics that withstand repeated washing and stretching. Specialty grades, including breathable, elastic, and matte-finish PU films, enable differentiation in premium apparel and outdoor segments. Higher margins associated with PU products also encourage reinvestment in advanced coating lines, multilayer extrusion technologies, and automated precision slitting systems, reinforcing their leading position.

Polyester-based films represent the fastest-growing segment, supported by their excellent thermal stability, chemical resistance, and mechanical durability. These attributes make polyester films highly suitable for industrial textiles, outdoor signage, automotive interiors, and electronics overlays. In performance apparel, the increasing global use of polyester fabrics, particularly in athleisure collections, creates natural demand synergy for compatible transfer films. Advancements in surface treatment technologies, including corona and plasma coatings, have improved print receptivity, adhesion, and stretch performance, narrowing the functional gap with PU in select textile applications. Polyester films are also widely used for reflective safety graphics compliant with industrial workwear standards. As converters continue transitioning away from PVC-based materials and seek consistent performance at competitive cost points, polyester films are positioned for sustained expansion across both mid-range apparel and technical industrial markets.

Application Insights

Packaging is anticipated to hold approximately 37.5% of the market share in 2026, making it the largest application segment. Heat transfer films are widely used for decorative labeling, brand embellishment, tamper-evident seals, and durable graphics on both rigid containers and flexible packaging. Their ability to deliver metallic finishes, holographic effects, and high-resolution graphics enhances shelf appeal in competitive retail environments. Premium FMCG and personal care brands increasingly adopt advanced transfer technologies to achieve tactile finishes and premium branding effects. Companies such as L'Oréal and Unilever utilize decorative transfer solutions to elevate packaging aesthetics across skincare and personal care portfolios. In crowded retail shelves, visual differentiation significantly influences consumer purchasing decisions, reinforcing the importance of high-quality, durable labeling solutions that resist moisture, abrasion, and handling damage.

Textiles and apparel are projected to be the fastest-growing application segment. Rapid customization trends, fast fashion cycles, and on-demand printing models drive the adoption of heat transfer films. These films enable seasonal launches, limited-edition collections, and personalized graphics without the need for costly screens or molds, reducing time-to-market for apparel manufacturers. Athleisure expansion, particularly in Asia Pacific manufacturing hubs such as China, Vietnam, and India, strengthens volume demand. Global brands and private labels alike rely on heat transfer films for jersey numbering, sponsor logos, and branding elements in sportswear. The continued growth of online apparel retail platforms such as Amazon and Shein further amplifies demand for flexible decoration methods, as small-batch production and personalization become central to competitive differentiation.

Regional Insights

North America Heat Transfer Film Market Trends - Sustainability-Driven Innovation and Digital Customization Growth

North America maintains a strong demand for specialty heat transfer films, with the U.S. serving as the regional leader in both consumption and innovation. Premium packaging across cosmetics, beverages, and personal care continues to drive decorative film usage, while decorated sportswear and licensed apparel support steady textile demand. Major retailers such as Walmart and Target have strengthened sustainability scorecards for private-label suppliers, encouraging adoption of recyclable substrates and low-VOC adhesive systems. These procurement policies are influencing converters to shift toward polyurethane (PU) and polyester films that meet environmental compliance benchmarks. Investment in digital printing and short-run customization remains strong, supported by equipment manufacturers such as HP Inc., whose Indigo digital presses are widely used in specialty packaging and textile decoration. The growth of on-demand decorated apparel through platforms linked to Amazon has further increased demand for flexible heat transfer solutions capable of small-batch production.

Recent developments highlight capacity expansion and sustainability collaboration. In 2024, Avery Dennison expanded its graphics and specialty materials portfolio in North America to enhance pressure-sensitive and transfer film solutions for packaging and apparel applications. At the same time, chemical suppliers such as H.B. Fuller have invested in low-emission adhesive technologies compatible with recyclable mono-material packaging. These initiatives improve recyclability pathways and strengthen compliance with U.S. state-level packaging regulations, reinforcing North America’s position as a high-value, innovation-driven market.

Europe Heat Transfer Film Market Trends - Regulatory Compliance and Circular Economy-Led Material Transition

Europe’s market landscape is shaped by strict regulatory compliance and environmental sustainability mandates. Germany leads in technical textiles, automotive interiors, and industrial film applications, leveraging its strong manufacturing ecosystem. Meanwhile, the U.K., France, Italy, and Spain demonstrate robust demand for apparel decoration and premium packaging solutions across the fashion and cosmetics industries. Regulatory frameworks such as the European Union’s Extended Producer Responsibility (EPR) schemes and REACH chemical regulations are accelerating the transition toward PU and polyester-based systems that comply with solvent restrictions and recyclability criteria. Companies such as Henkel have introduced adhesive formulations tailored for recyclable flexible packaging, helping film converters meet EU packaging waste targets. In parallel, Covestro continues to promote bio-based and partially recycled polyurethane raw materials, strengthening the sustainability profile of PU heat transfer films.

The automotive sector also plays a strategic role. Manufacturers, including BMW, increasingly adopt lightweight interior decoration films with enhanced durability and low-emission coatings to meet EU interior air-quality standards. Collaborative innovation initiatives across packaging and recycling ecosystems, often supported by EU-funded circular economy programs, are accelerating the development of mono-material film structures compatible with existing recycling streams. Suppliers that demonstrate verified environmental compliance and lifecycle transparency gain a clear advantage in European procurement processes.

Asia Pacific Heat Transfer Film Market Trends - Manufacturing Dominance and Export-Led Textile Expansion

Asia Pacific is projected to account for approximately 44.2% of the market share in 2026, making it the leading and fastest-growing regional market. China dominates in both manufacturing capacity and domestic consumption, supported by its extensive textile, packaging, and export-oriented garment industries. Large apparel exporters supplying global brands such as Nike and Adidas rely heavily on heat transfer films for logos, performance graphics, and branding elements.

Japan maintains a strong presence in high-performance specialty films, with companies such as Toray Industries focusing on advanced polyester and functional film technologies for industrial and apparel applications. In India and ASEAN economies, rapid growth in garment exports and domestic athleisure consumption is expanding the demand for cost-effective yet durable transfer films. India’s Production Linked Incentive (PLI) scheme for technical textiles and manufacturing modernization policies across Southeast Asia support capacity expansion and technology upgrades.

Regional producers are investing in PU and polyester extrusion lines, automation in garment decoration facilities, and digital cutting systems to improve throughput and consistency in quality. Chinese chemical major Wanhua Chemical has continued to expand polyurethane production capacity, ensuring a stable supply of raw materials for downstream film manufacturers. Cost-competitive production, vertical integration, and strong export networks underpin Asia Pacific’s dominance, while ongoing government-backed industrial modernization programs strengthen long-term growth prospects across emerging Asian economies.

Competitive Landscape

The global heat transfer film market is moderately fragmented, with a combination of global specialty film manufacturers and regional converters. Leading players collectively account for an estimated low-to-mid 20% market share. Specialty PU film segments exhibit higher concentration, while commodity PVC products remain more dispersed. Competitive positioning is influenced by technological capability, sustainability credentials, and supply chain integration.

Key strategic priorities include sustainable product innovation, vertical integration to control raw material exposure, regional capacity expansion in Asia Pacific, and premium service offerings for brand owners requiring fast customization cycles.

Key Industry Developments

- In July 2025, Avery Dennison Corporation launched an RFID-enabled In-Mold Label (IML) portfolio, designed to embed durable heat transfer films into injection-molded products for enhanced traceability and circular economy applications across packaging, industrial, and consumer goods segments.

- In June 2025, Ritrama introduced a new high-performance line of heat transfer films tailored for sportswear and promotional goods, offering improved elasticity, wash resistance, and color vibrancy for textile applications.

Companies Covered in Heat Transfer Film Market

- Avery Dennison

- 3M

- Siser

- Stahls

- Chemica

- Hexis Group

- Poli-Tape Group

- SEF Textile

- Ritrama

- Dae Ha Co., Ltd.

- Unimark Heat Transfer Co. Ltd.

- FLEXcon Company Inc.

- Toray Industries

- Covestro

- Wanhua Chemical

- Arkema

- H.B. Fuller

- Henkel

Frequently Asked Questions

The global heat transfer film market is valued at approximately US$2.9 billion in 2026.

The heat transfer film market is projected to reach approximately US$4.5 billion by 2033.

Key trends include rising adoption of polyurethane (PU)-based films, transition toward recyclable mono-material solutions, growth in digital and short-run customization, increasing demand from athleisure and sportswear, and regulatory-driven shift toward low-VOC and PVC-free formulations.

Polyurethane-based films lead the market, holding an anticipated 53.7% share, driven by superior flexibility, abrasion resistance, soft-touch finish, and strong compatibility with stretch fabrics and premium packaging.

Packaging is the dominant application, accounting for approximately 37.5% of market share, supported by premium FMCG branding, decorative labeling, and durable graphics on rigid and flexible packaging formats.

The heat transfer films market is expected to grow at a CAGR of 6.6% between 2026 and 2033.

Major players include Avery Dennison, 3M, Siser, Stahls', and Chemica.