- Renewable Energy

- India Energy Storage Systems Market

India Energy Storage Systems Market Size, Share, and Growth Forecast, 2026 - 2033

India Energy Storage Systems Market by Technology (Electrochemical (BESS), Mechanical (Pumped Hydro), Thermal Energy Storage, Chemical, and Electrical.), Application (Grid-Scale Storage, Commercial & Industrial (C&I) Storage, Residential Storage, Renewable Energy Integration (Dedicated Storage for Wind/Solar), Microgrids & Off-Grid Storage, and Other Applications.), and Regional Analysis for 2026 - 2033

India Energy Storage Systems Market Size and Trends Analysis

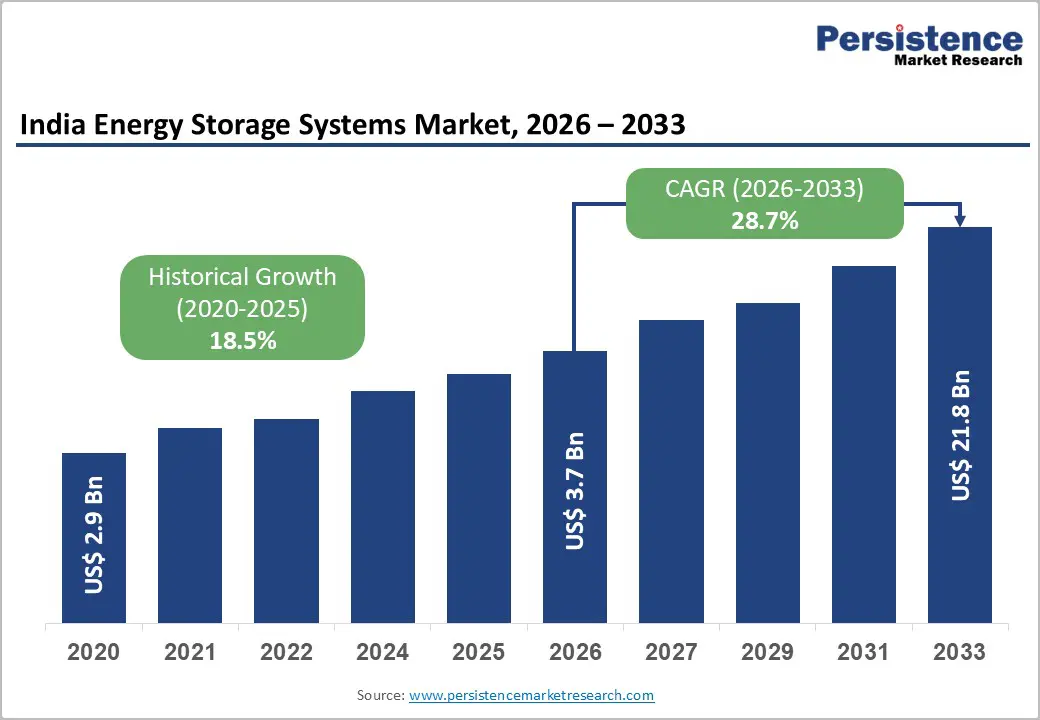

India energy storage systems market size is likely to be valued at US$ 3.7 billion in 2026 and is projected to reach US$ 21.8 billion by 2033, growing at a CAGR of 28.7% between 2026 and 2033. Anchoring this trajectory is India's ambitious target to achieve 500 GW of non-fossil fuel-based power capacity by 2030, which requires rapid scaling of storage infrastructure to manage intermittency across solar and wind assets.

The Government of India's National Electricity Plan 2023 projects national energy storage capacity requirements escalating from 82.37 GWh in 2026-27 to 411.4 GWh by 2031-32, and further to 2,380 GWh by 2047, quantifying the structural demand underpinning market expansion. Sustained policy momentum, including Viability Gap Funding (VGF) for BESS, the Production-Linked Incentive (PLI) scheme for advanced chemistry cell manufacturing, and the Energy Storage Obligation (ESO) framework, collectively establish a conducive investment environment that is attracting both domestic conglomerates and global technology integrators to the India energy storage systems market.

Key Industry Highlights:

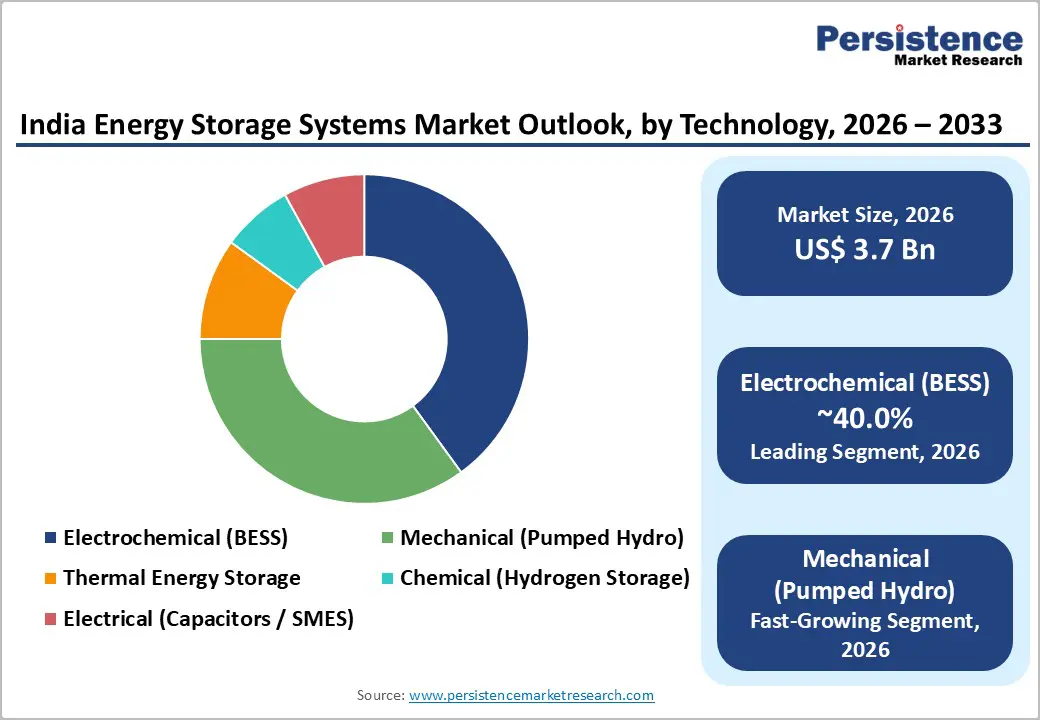

- Leading Technology Segment: Electrochemical Battery Energy Storage Systems (BESS) lead the technology segment with approximately 40% market share in 2026, driven by lithium-ion (LFP and NMC) deployment across grid-scale, C&I, and distributed renewable integration projects.

- Fastest-Growing Technology Segment: Pumped Hydro Storage (PHS) is the fastest-growing segment, supported by India’s 176 GW technical potential and the CEA’s 51.24 GW development target by 2032 for long-duration grid balancing.

- Leading Application Segment: Grid-scale storage dominates with nearly 35% market share in 2026, anchored by large tenders from SECI, NTPC Renewable Energy Limited, and GUVNL shaping national utility-scale procurement.

- Fastest-Growing Application Segment: Renewable energy integration is the fastest-growing application, propelled by MNRE’s mandate to include battery storage in new solar and wind projects starting at 10% of plant capacity.

- Policy-Driven Growth Catalyst: The Energy Storage Obligation (1% in FY24 scaling to 4% by FY30) and Viability Gap Funding support of up to 40% capital cost have institutionalized long-term demand visibility for BESS deployment.

- Manufacturing Expansion Opportunity: The 50 GWh ACC PLI scheme and new gigafactories, including Waaree Energies’ 16 GWh facility, are accelerating domestic battery manufacturing and supply chain localization.

| Key Insights | Details |

|---|---|

| India Energy Storage Systems Market Size (2026E) | US$ 3.7 Bn |

| Market Value Forecast (2033F) | US$ 21.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 28.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 18.5% |

Market Dynamics

Drivers - National Renewable Energy Targets and Grid Integration Imperatives

India's commitment to deriving 50% of its cumulative installed power capacity from non-fossil fuel sources by 2030 and reducing GDP emission intensity by 45% from 2005 levels places grid-integrated energy storage at the center of national energy policy. At the core of this driver is the fundamental mismatch between variable renewable generation solar, wind and the continuous nature of electricity demand, a challenge that only large-scale storage can resolve effectively.

India's installed non-fossil fuel capacity rose from 81 GW before 2014 to 250 GW as of September 2025, reflecting an extraordinary pace of clean energy buildout. Renewables accounted for approximately 19.9% of power generation in 2023, with the solar and wind share in the electricity generation mix having doubled from 4% to 8% between 2016 and 2018 alone a trend that has continued to accelerate. Per the Central Electricity Authority (CEA), India requires 336 GWh of storage by 2029-30 and 411 GWh by 2031-32 to maintain grid stability at these renewable penetration levels.

The India Energy Storage Systems Market directly benefits from these mandates, as hybrid (renewable + BESS) tendered capacity rose from 12% in 2021 to over 49% in 2024, confirming that co-located storage is now standard practice in large renewable procurement.

Government Policy, Regulatory Frameworks, and Financial Incentives

A structured and layered policy architecture implemented by the Government of India has substantially reduced investment risk and improved project economics across the India Energy Storage Systems Market. This driver encompasses a coordinated suite of demand-side mandates, supply-side manufacturing incentives, and financial de-risking instruments that together mobilize public and private capital.

The Ministry of Power introduced a long-term Energy Storage Obligation (ESO) trajectory starting at 1% in FY 2023-24 and scaling to 4% by FY 2029-30 requiring that at least 85% of stored energy originate from renewable sources, creating a durable demand signal for BESS and hybrid project developers. The Government of India approved a Viability Gap Funding (VGF) scheme in September 2023, providing up to 40% capital cost support for BESS projects targeting 4,000 MWh capacity by 2030.

The PLI scheme supports 50 GWh of Advanced Chemistry Cell (ACC) manufacturing, directly strengthening domestic supply chains and cost competitiveness. Regulatory recognition of ESS under the Electricity Rules (2022), inclusion in the Harmonised Master List of Infrastructure, and the National Framework for Promotion of Energy Storage Systems provide legal standing for asset financing, project structuring, and revenue certainty. The Ministry of New and Renewable Energy (MNRE) in December 2024 further announced plans to mandate inclusion of battery storage in new solar and wind projects initially at 10% of plant capacity, with potential escalation to 30-40% as battery costs decline.

Technological Advancement and Declining Battery Costs

Technological maturation across lithium-ion chemistries particularly Lithium Iron Phosphate (LFP) and Lithium Nickel Manganese Cobalt Oxide (NMC) has dramatically improved the commercial feasibility of BESS in the India Energy Storage Systems Market. This driver reflects the convergence of falling hardware costs, improved energy density, longer cycle life, and the development of indigenous manufacturing capacity.

Lithium-based technologies remain the most commercially viable options in India due to competitive pricing, reliable warranties, and performance suitability across both grid-scale and distributed applications. A landmark demonstration of this cost trajectory is visible in India's first commercially approved standalone BESS project at BRPL's Kilokari substation (20 MW / 40 MWh), which set a levelized capacity tariff of INR 57.6 lakh/MW approximately 55% below previous benchmarks confirming that BESS economics have crossed a critical inflection point.

In February 2026, Waaree Energies announced plans to build a 16 GWh integrated lithium-ion battery gigafactory in Andhra Pradesh, investing approximately INR 8,175 crore to cover the full battery value chain including cells, packs, and large-scale BESS significantly boosting domestic manufacturing capacity. Analysis using India's Energy Storage India Tool (ESIT) indicates a base-case energy storage requirement of approximately 9.4 GWh for safely accommodating high levels of distributed rooftop solar, underscoring the structural scale of technology deployment needed. These dynamics collectively accelerate adoption across the India Energy Storage Systems Market.

Market Restraining Factors

High Capital Costs, Financing Barriers, and Supply Chain Dependency

Despite declining unit costs, the high upfront capital investment required for utility-scale BESS projects remains a significant barrier to deployment in the India Energy Storage Systems Market. Critical raw materials such as lithium, cobalt, and manganese are predominantly import-dependent, exposing projects to global supply chain disruptions and price volatility. India's limited domestic cell manufacturing base means that only 219 MWh of BESS capacity is operational from 12.8 GWh auctioned between 2022 and May 2025, largely reflecting execution gaps driven by high financing costs and aggressive underbidding. This mismatch between contracted and commissioned capacity remains a structural constraint on near-term market realization.

Regulatory Complexity, Grid Connection Bottlenecks, and PPA Delays

The India Energy Storage Systems Market faces operational friction from PPA signing delays, evolving contract structures, and grid connection bottlenecks that lengthen project timelines and elevate development risk. Distribution grids at low- and medium-voltage levels remain technically inflexible, presenting challenges such as reverse power flow, voltage rise, and transformer overloading when high shares of distributed storage are deployed alongside rooftop solar. Issues such as project cancellations, weak domestic manufacturing infrastructure, and unclear revenue stacking frameworks further complicate the commercial case for storage-only developers, particularly new entrants and C&I-focused operators. Integrating 40 GW of rooftop solar PV in India requires careful feeder planning and targeted interventions as illustrated by Germany's experience managing 45 GW of solar PV pointing to the technical complexity ahead.

Opportunity - Domestic Battery Manufacturing and the PLI-Driven Supply Chain Buildout

The Government of India's Production-Linked Incentive (PLI) scheme for Advanced Chemistry Cell (ACC) manufacturing represents a transformative structural opportunity for the India Energy Storage Systems Market, directly addressing the supply-side constraints that have historically limited domestic BESS deployment. At its core, this opportunity involves converting India's dependence on imported battery cells into a vertically integrated domestic manufacturing ecosystem capable of serving utility, C&I, and residential storage at internationally competitive cost points.

The PLI scheme supports 50 GWh of ACC battery manufacturing, with the potential to unlock significant cost reductions as domestic scale increases. Reinforcing this momentum, Waaree Energies announced 16 GWh gigafactory in Andhra Pradesh backed by an investment of approximately INR 8,175 crore and covering cells, packs, and full BESS integration signals serious private sector commitment to indigenous manufacturing. In June 2025, Lineage Power inaugurated India's first fully automated 5 GWh BESS factory in Bengaluru, Karnataka, further validating the industrial buildout underway. These developments position the India Energy Storage Systems Market not only as a deployment center but as an emerging hub for battery technology manufacturing in Asia, with downstream benefits for export competitiveness and supply chain resilience.

Pumped Storage Projects as Long-Duration Grid Storage at National Scale

The large-scale development of Pumped Hydro Storage (PHS) presents a distinct and complementary opportunity within the India Energy Storage Systems Market, particularly for meeting long-duration storage requirements where BESS economics remain challenged. India holds a total pumped storage potential of approximately 176 GW, and the Central Electricity Authority (CEA) has set a target of 51.24 GW of pumped storage capacity by 2032, with Greenko (13.2 GW), Adani Green (11.4 GW), and JSW Energy (7.7 GW) together accounting for nearly two-thirds of this pipeline.

Unlike BESS assets, which carry a lifecycle of approximately 15 years, commissioned pumped storage projects can operate reliably for 70 to 100 years, providing highly durable, low-carbon grid balancing services. Greenko Group won India's largest technology-agnostic long-duration energy storage tender from NTPC Renewable Energy Limited in December 2022, securing 500 MW / 3,000 MWh of standalone pumped storage capacity establishing a replicable procurement benchmark. In Maharashtra and Andhra Pradesh alone which together hold nearly 40% of India's pumped storage potential Andhra Pradesh is expected to add 16 GW and Maharashtra 13 GW by 2032. Regulatory relaxations for PSP development, co-location advisories with solar projects, and flexible ownership models further accelerate this segment's role within the India Energy Storage Systems Market.

Category-wise Analysis

Technology Insights

Electrochemical (Battery Energy Storage Systems) holds the dominant technology position in the India Energy Storage Systems Market, commanding approximately 40.0% of total market share in 2026. This leadership reflects the technology's unmatched flexibility BESS can be installed virtually anywhere, making it ideal for grid-scale tenders, C&I deployments, distributed rooftop solar integration, and remote microgrid applications. Lithium-based chemistries, particularly LFP and NMC, are the most commercially deployed variants, supported by declining costs, improving cycle warranties, and growing domestic manufacturing. Landmark projects such as Adani's 1,126 MW / 3,530 MWh BESS at Khavda, Gujarat, Tata Power Solar's 100 MW solar + 120 MWh BESS in Chhattisgarh, and ENGIE's 280 MW / 560 MWh project under GUVNL tender underscore BESS's dominance across the project development pipeline in India.

Mechanical energy storage led by Pumped Hydro Storage (PHS) is the fastest-growing technology segment in the India Energy Storage Systems Market, driven by the government's recognition of pumped hydro as the most economically viable long-duration storage solution for large-scale grid balancing. India's total pumped hydro potential stands at approximately 176 GW, and the CEA has mapped 51.24 GW of PSP capacity to be developed by 2032.

Application Insights

Grid-Scale Storage leads the application segmentation of the India Energy Storage Systems Market, holding approximately 35% of total market share in 2026. This dominance is structurally anchored by national procurement through entities such as NTPC Renewable Energy Limited, SECI, and GUVNL, whose large-scale tenders define the pipeline of utility-grade storage infrastructure. The IFC-IndiGrid 180 MW / 360 MWh BESS project in Gujarat backed by INR 4.6 billion (~$55 million) from the Climate Investment Funds' Clean Technology Fund and ENGIE's 280 MW / 560 MWh project under GUVNL's national tender represents the caliber of grid-scale investments shaping this segment. With the CEA projecting a storage requirement of 336 GWh by 2029-30, grid-scale procurement will continue to set the commercial tone for the India Energy Storage Systems Market over the medium term.

Renewable Energy Integration encompassing dedicated co-located storage for wind and solar projects is the fastest-growing application segment in the India Energy Storage Systems Market, propelled by evolving policy mandates and the operational necessity of smoothing variable generation profiles. The MNRE's December 2024 announcement to mandate storage inclusion in new solar and wind projects, initially at 10% of plant capacity with potential escalation to 30-40%, institutionalizes dedicated renewable-coupled storage as a standard project requirement.

Competitive Landscape

India Energy Storage Systems (ESS) market is moderately consolidated, with a few large players dominating the landscape while numerous smaller providers operate regionally. Leading companies such as Tata Power Renewable Energy Ltd., AES Corporation / Fluence (Fluence JV), Reliance New Energy Ltd., Exide Energy Solutions Ltd., Amara Raja Energy & Mobility Ltd., and Adani Energy Solutions Ltd. control a significant portion of utility-scale and grid-connected projects, leveraging strong financial backing, advanced technology, and strategic partnerships. These key players primarily focus on lithium-ion and lead-acid battery solutions for industrial, commercial, and large-scale renewable integration, including hybrid solar-plus-storage applications.

The residential and small commercial segment is highly fragmented, with smaller players like HBL Power Systems, Livguard Energy, and Waaree Technologies offering cost-competitive and niche solutions. This creates opportunities for innovation in battery management systems, modular ESS, and off-grid applications. The market also displays oligopolistic traits in large-scale projects, as only a few companies can meet technical complexity and high capital requirements. International companies such as LG Energy Solution, BYD Co. Ltd., Panasonic Holdings, and Hitachi Energy India Ltd. further intensify competition by supplying advanced technologies and collaborating with local developers. Overall, the India ESS market reflects a hybrid competitive structure, combining consolidation among major players with fragmentation at smaller scales, making it both competitive and opportunity rich.

Key Industry Developments

- November 2025, Adani Group announced its entry into India’s BESS market with a landmark 1126 MW / 3530 MWh project at Khavda, Gujarat, slated for commissioning by March 2026. The deployment of over 700 lithium-ion BESS containers will make it the largest single-location BESS in India and among the world’s largest. This project strengthens grid reliability, enables round-the-clock clean power, manages peak loads, and supports large-scale renewable energy integration, reflecting a major expansion of utility-scale energy storage in India.

- February 2026, Waaree Energies unveiled plans to build a 16 GWh integrated lithium-ion battery gigafactory in Andhra Pradesh, investing around INR 8,175 crore. The facility will cover the full battery value chain, including cells, packs, and large-scale BESS, significantly boosting domestic manufacturing capacity. This development addresses India’s need for local energy storage production, reducing reliance on imports and supporting the country’s renewable energy transition and net-zero goals.

- June 2025, Cummins India Limited launched its modular and scalable Battery Energy Storage Systems (BESS) in Pune, using lithium ferrophosphate (LFP) batteries. Designed to integrate solar and wind energy, these systems enhance grid stability, enable peak shaving and energy shifting, and provide reliable power for industrial, commercial, and data center applications. This marks a strategic step in supporting India’s clean energy transition and highlights growing commercial and industrial adoption of ESS solutions.

Companies Covered in India Energy Storage Systems Market

- Tata Power Renewable Energy Ltd.

- AES Corporation / Fluence (Fluence JV)

- Reliance New Energy Ltd.

- Exide Energy Solutions Ltd.

- Amara Raja Energy & Mobility Ltd.

- Adani Energy Solutions Ltd.

- JSW Energy Ltd.

- Waaree Technologies / Waaree Energies Ltd.

- HBL Power Systems Ltd.

- Luminous Power Technologies

- Livguard Energy

- Avaada Group

- Rays Power Infra Ltd.

- Delta Electronics India Pvt Ltd.

- BYD Co. Ltd.

- LG Energy Solution / LG Chem

- Panasonic Holdings Corp.

- Samsung SDI Co., Ltd.

- Hitachi Energy India Ltd.

- Siemens Energy India / Siemens Energy AG

- GE Vernova (Grid Solutions) / General Electric

- Kokam

- Saft

- Sungrow Power Supply Co., Ltd.

- NEC Energy (India JV)

Frequently Asked Questions

The India Energy Storage Systems Market is projected to be valued at US$ 3.7 Bn in 2026.

The Electrochemical (BESS) segment is expected to account for approximately 40% of the India Energy Storage Systems Market by Technology in 2026.

The market is expected to witness a CAGR of 28.7% from 2026 to 2033.

The Energy Storage Systems Market growth is driven by India’s ambitious renewable energy targets and grid stability needs, strong government policies and financial incentives (including ESO, VGF, and PLI schemes), and rapid technological advancements coupled with declining lithium-ion battery costs that improve commercial viability.

The key market opportunities in the Energy Storage Systems Market lie in rapid domestic battery manufacturing expansion under the PLI-driven ACC ecosystem and large-scale development of pumped hydro storage projects to meet India’s long-duration grid balancing requirements.

Key players in the Energy Storage Systems Market include Tata Power Renewable Energy Ltd., AES Corporation / Fluence (Fluence JV), Reliance New Energy Ltd., Exide Energy Solutions Ltd., Amara Raja Energy & Mobility Ltd., and Adani Energy Solutions Ltd.