- Communication Infrastructure & Services

- Executive Education Program Market

Executive Education Program Market Size, Share, and Growth Forecast, 2026 - 2033

Executive Education Program Market by Program Type (Customized, Pre-Designed), Delivery Mode (In-Person, Online, Blended/Hybrid, Corporate On-Site Training, Webinars & Virtual Workshops), Course Type (Management & Leadership, Finance & Accounting, Strategic Leadership & Innovation, Marketing & Sales Leadership, Business Operations & Entrepreneurship, Digital Transformation & AI Leadership), and Regional Analysis for 2026 - 2033

Executive Education Program Market Share and Trends Analysis

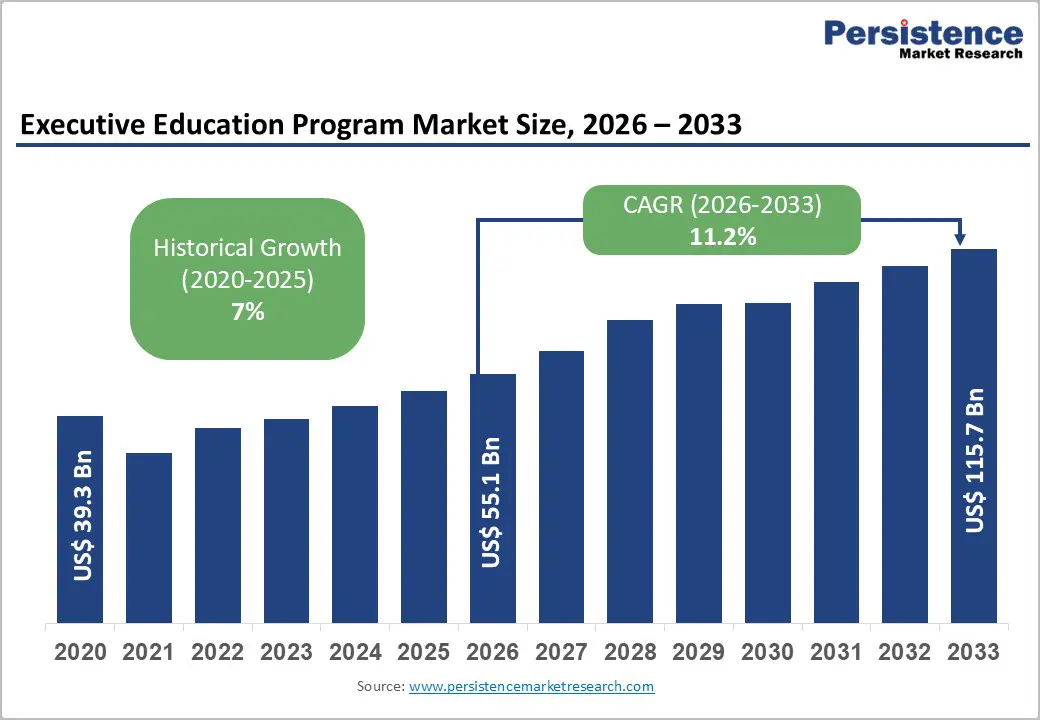

The global executive education program market size is likely to be valued at US$ 55.1 billion in 2026, and is projected to reach US$ 115.7 billion by 2033, growing at a CAGR of 11.2% during the forecast period 2026 - 2033.

Market expansion is being supported by sustained corporate reskilling expenditure, rising executive turnover risk, and regulatory pressure on governance, sustainability, and digital accountability, particularly across advanced and emerging economies. Corporations are reallocating learning and development budgets toward shorter, outcome-linked executive programs rather than degree-centric education. Executive roles are being reshaped by artificial intelligence (AI), environmental, social, & governance (ESG) compliance, and geopolitical volatility, increasing the demand for continuous executive upskilling rather than seeking one-time credentials. Digital delivery models are further reducing marginal costs and expanding cross-border participation, improving market accessibility without proportionally diluting pricing power. For program providers, revenue visibility is improving through multi-year corporate contracts, while fragmentation persists across providers, limiting pricing commoditization. Institutions with strong enterprise partnerships, proprietary content, and hybrid delivery capabilities are capturing disproportionate value.

Key Industry Highlights

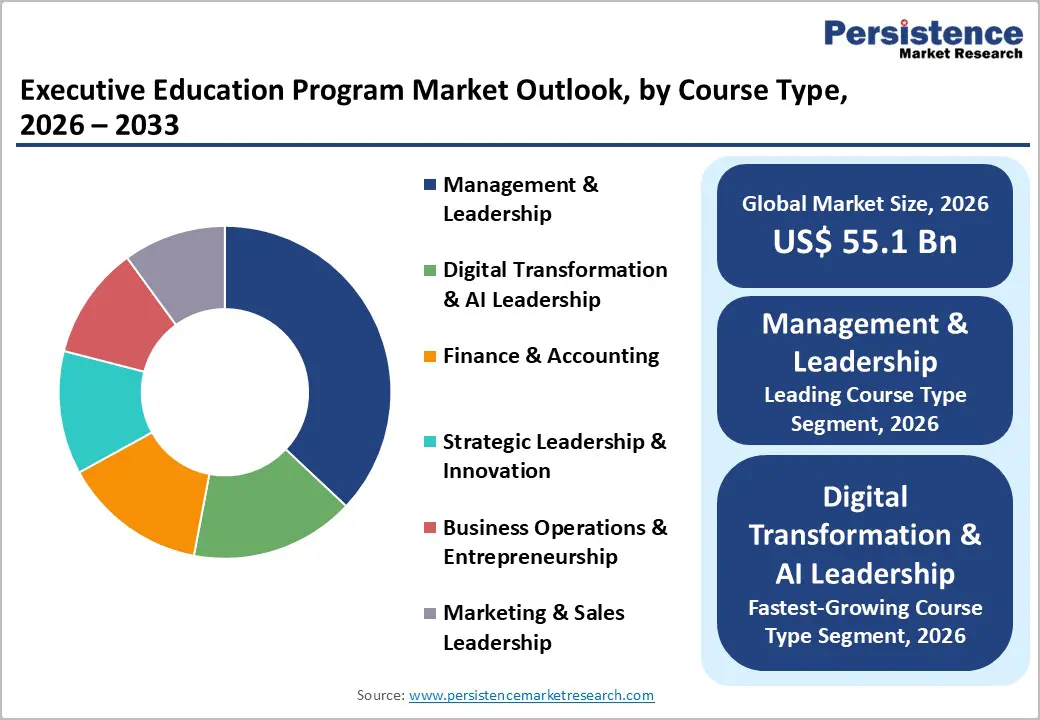

- Leading Course Type: Management and leadership programs are expected to account for around 37% of total market revenue in 2026, driven by succession planning and leadership pipeline needs

- Fastest-growing Course Type: Digital transformation and AI leadership programs are projected to grow at the highest CAGR during 2026 - 2033, underpinned by regulatory accountability and board-level oversight requirements.

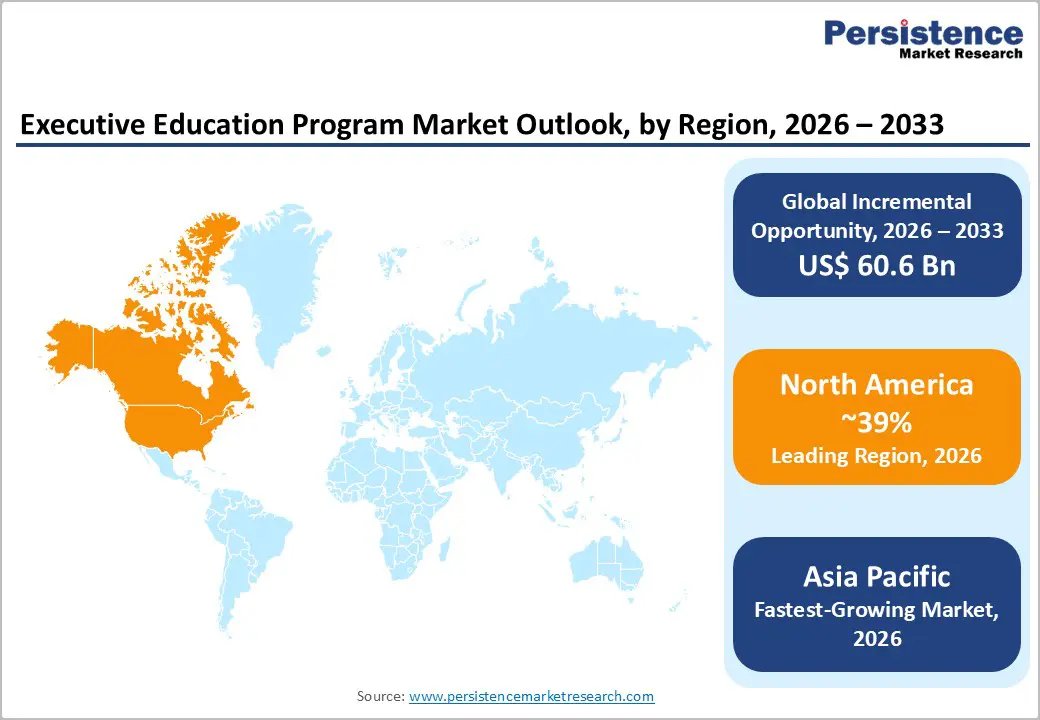

- Dominant Region: North America is projected to command approximately 39% of the market share in 2026, owing to high corporate training expenditure and mature accreditation frameworks.

- Fastest-growing Market: The Asia Pacific market is set to be the fastest-growing through 2033, on account of rapid corporate internationalization and accelerating adoption of digitally delivered executive education across India, China, and Southeast Asia.

- Delivery Mode Dominance: Blended and hybrid learning formats are anticipated to dominate with nearly 50% market share in 2026, reflecting enterprise preferences for cost-efficient yet immersive learning,

- Fastest-growing Delivery Mode: Fully online executive education is forecast to be the fastest-growing segment through 2033 as digital credential acceptance widens among enterprises.

- Prime Opportunity: The expansion of scalable, digitally enabled executive education platforms tailored for emerging-market corporations is creating a high-growth opportunity, as leadership capability gaps persist amid rising cross-border business activity.

- September 2025: XLRI Delhi announced a new Indo-French-Danish academic collaboration with top institutions to launch joint degrees and specialized full-time, part-time, and executive programs.

| Key Insights | Details |

|---|---|

| Executive Education Program Market Size (2026E) | US$ 55.1 Bn |

| Market Value Forecast (2033F) | US$ 115.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Enterprise-Mandated Leadership Reskilling under Regulatory and Technological Pressure

Enterprise-mandated leadership reskilling is becoming a structurally embedded growth driver rather than a cyclical training response. Regulatory agencies and international institutions are tightening accountability standards across corporate governance, sustainability disclosure, data protection, and financial oversight, which is directly increasing skill expectations at senior leadership levels. The European Union Corporate Sustainability Reporting Directive (CSRD), evolving United States Securities and Exchange Commission (SEC) climate disclosure requirements, and International Financial Reporting Standards (IFRS)-aligned environmental, social, & governance (ESG) frameworks are requiring boards and C-suite executives to demonstrate measurable oversight capabilities. For example, in September 2025, PRI Academy and Wharton Executive Education came out with the “Wharton/PRI Executive Certificate: Impact, Value and the Materiality of Sustainability”, a global program to equip investment professionals with tools for navigating complex financial landscapes through responsible investing. As regulatory exposure is increasing, enterprises are prioritizing executive education programs that are directly aligned with compliance, fiduciary responsibility, and strategic risk management. This shift is making leadership reskilling a recurring operational requirement rather than a discretionary investment, particularly in highly regulated industries.

At the same time, AI adoption is reshaping executive accountability structures. Analysis from the Organisation for Economic Co-operation and Development (OECD) and the International Labour Organization (ILO) indicates that senior leaders are increasingly holding responsibility for AI governance, algorithmic risk oversight, and ethical deployment decisions. This shift is redirecting demand away from broad leadership development toward specialized, regulation-aware executive education. Corporations are reallocating learning budgets toward executive cohorts as leadership risk becomes more concentrated at the top of organizations. Demographic pressure is reinforcing this trend. World Bank data is showing that more than 35 percent of senior corporate leaders in OECD economies will have exited executive roles by 2035, which is increasing succession risk. Enterprises are responding by institutionalizing leadership pipelines supported by recurring executive education engagements. As a result, corporate-sponsored programs are increasing in duration and contract value, improving revenue visibility for providers and reinforcing the long-term resilience of this demand driver.

Cost-Intensity and Uneven ROI Measurement in Executive Education Procurement

Executive education faces structural adoption constraints that are primarily driven by cost intensity and inconsistent return-on-investment measurement. High-quality programs are requiring senior faculty involvement, proprietary research inputs, low participant-to-faculty ratios, and customized delivery models, which are collectively increasing per-participant costs. Short-duration executive programs frequently range from US$ 8,000 to US$ 15,000 per participant, while extended engagements are requiring significantly higher investment. This cost structure is limiting adoption among mid-sized enterprises and firms operating in emerging markets, where learning and development budgets are more tightly constrained. As pricing pressure is increasing, executive education is remaining concentrated among large multinational organizations with higher discretionary training spend.

Procurement complexity is further intensifying due to weak standardization of impact measurement. Unlike technical certifications with clearly defined skill outcomes, executive education benefits are often manifesting through leadership effectiveness, decision quality, and organizational culture shifts, which are difficult to quantify within annual budget cycles. Regulatory fragmentation is compounding this challenge. Cross-border delivery is increasingly encountering data localization requirements, professional accreditation constraints, and tax treatment disparities. Providers are facing compliance complexity when delivering digital programs across jurisdictions such as the European Economic Area (EEA) and several Asian markets with varying credential recognition frameworks. These constraints are suppressing penetration beyond large multinationals and are concentrating value among providers that are developing scalable digital infrastructure and enterprise-grade analytics to demonstrate outcome-linked impact and cost efficiency.

Scalable Executive Education Platforms for Emerging-Market Corporate Leadership

A high-value growth opportunity is emerging at the intersection of emerging-market corporate expansion and digitally scalable executive education delivery. Economies across Asia Pacific, parts of the Middle East, and selected African markets are experiencing sustained growth in domestically headquartered multinational firms. This trend is expanding the demand for leadership teams that are capable of managing cross-border strategy, regulatory compliance, and multicultural organizations. For instance, in September 2025, UAE's AI Academy launched its first Executive Program for Chief AI Officers, a two-week course in Abu Dhabi, in collaboration with Abu Dhabi School of Management and Polynome AI Academy. Aimed at C-suite leaders, it covers AI architecture, ethics, governance, and policy, with optional international extensions, aligning with UAE's AI Strategy 2031 to drive regional transformation. As corporate structures are becoming more complex, enterprises are actively seeking executive education programs that are globally aligned while remaining locally relevant.

Despite this momentum, executive education penetration in emerging markets is low. United Nations Educational, Scientific and Cultural Organization (UNESCO) education finance data is showing that executive and professional education accounts for a small fraction of total tertiary education spending in most emerging economies. This disparity is creating a sizable addressable market. Digitally enabled and hybrid executive education platforms are offering a scalable entry point by combining global faculty, localized case studies, and modular delivery formats. Providers are reducing per-participant costs by a substantial margins compared to traditional residential models. Policy support is reinforcing this opportunity. Governments in India, Southeast Asia, and Gulf economies are expanding public-private partnerships, executive skilling grants, and innovation mandates. Market players that are aligning with national leadership development priorities while maintaining international credibility are expected to capture sustained, high-margin growth.

Category-Wise Analysis

Program Type Insights

Customized executive programs are set to account for an estimated 56% of the executive education program market revenue share in 2026. Large enterprises are increasingly shifting away from open-enrollment formats and are adopting organization-specific programs that are aligning closely with strategic priorities such as enterprise transformation, governance strengthening, and leadership succession planning. Corporate disclosures and surveys from the Association to Advance Collegiate Schools of Business (AACSB) are indicating higher renewal rates and longer contract durations for customized engagements. These programs are becoming embedded within enterprise talent and leadership architectures, which is improving revenue visibility and contract stability for education providers. As organizations are formalizing leadership development as a core operational function, customized executive education is continuing to reinforce its position as the dominant revenue contributor.

Pre-designed modular programs are set to be the fastest-growing segment during the 2026 to 2033 forecast period, driven by mid-sized enterprises and individual executives who are seeking flexible, stackable credentials without extended residential commitments. Digital delivery models and broader recognition of micro-credentials are expanding the addressable learner base, particularly across emerging markets. These programs are allowing participants to build leadership capabilities incrementally while balancing professional responsibilities. Providers with scalable content libraries, strong institutional brands, and efficient digital platforms are capturing rising enrollment volumes while preserving pricing discipline. As modular learning adoption is increasing, this segment is becoming a critical growth lever within the executive education market.

Delivery Mode Insights

Blended and hybrid learning models are likely to emerge as the leading mode of delivery in 2026, accounting for an estimated 49% of the executive education market share. This shift is reflecting a structural transformation in corporate learning preferences rather than a temporary response to pandemic-driven constraints. Enterprises are increasingly prioritizing delivery formats that preserve peer interaction, collaborative problem-solving, and direct faculty engagement while simultaneously reducing travel expenses and opportunity costs. Hybrid programs are enabling organizations to structure cross-regional executive cohorts, which is enhancing knowledge exchange, cultural exposure, and strategic alignment across geographies. As corporations are institutionalizing flexible learning models, hybrid delivery is continuing to strengthen its dominance by offering both experiential depth and operational efficiency.

Fully online executive education is slated to exhibit the highest 2026 - 2033 CAGR, owing to continuous improvements in synchronous learning platforms, analytics-driven personalization, and rising enterprise acceptance of digital executive credentials. These advancements are improving learner engagement, assessment precision, and program scalability. Although pricing remains lower than traditional residential formats, margin scalability is improving due to higher enrollment volumes and reduced fixed infrastructure costs. Providers that are investing in proprietary digital platforms and data-driven learning architectures are strengthening their competitive positioning, enabling them to expand reach while preserving instructional quality and long-term profitability.

Course Type Insights

Management and leadership programs are poised to be the dominant course type in 2026, capturing an estimated 37% of the executive education program market share. The demand for these courses is being sustained by enterprise succession planning requirements and the formalization of leadership pipelines across large organizations. These programs are increasingly integrating governance frameworks, ethical decision-making, and leadership under uncertainty to reflect evolving executive responsibilities. As regulatory scrutiny and stakeholder expectations are rising, enterprises are relying on core leadership curricula to reinforce decision quality, accountability, and organizational resilience. This sustained relevance is enabling management and leadership programs to maintain their position as the primary revenue anchor within the course portfolio.

Digital transformation and AI leadership programs are projected to register a CAGR of roughly 17% from 2026 to 2033. The growth of this segment is being driven by regulatory accountability for AI deployment, data governance requirements, and increasing board-level oversight obligations. Senior leaders are seeking applied programs that address algorithmic risk, ethical use of AI, and technology-enabled business model transformation. Providers that are offering governance-oriented and application-focused AI curricula are achieving premium pricing and strong enterprise adoption. As digital accountability continues to shift toward senior leadership, this segment is expected to remain a critical growth driver across global executive education markets.

Regional Insights

North America Executive Education Program Market Trends

North America is anticipated to represent the largest regional market for executive education programs, accounting for an estimated 39% of global revenue in 2026. High corporate training expenditure, mature executive education ecosystems, and strong institutional credibility are supporting sustained demand across the region. Large enterprises are actively investing in executive capability development as leadership accountability is expanding across governance, technology oversight, and regulatory compliance. Demand is remaining particularly strong in regulated industries such as financial services, healthcare, and energy, as well as in technology-driven sectors where strategic decision-making cycles are accelerating.

The executive education program market growth in North America is forecasted to be steady through 2033 as a result of well-established accreditation standards and institutional rankings that are reinforcing pricing power for leading providers. Enterprises are increasingly favoring providers with proven outcome measurement frameworks and long-standing corporate partnerships. As a result, competition is remaining concentrated among top-tier institutions, while investment is flowing toward digital platforms and enterprise-integrated learning models. By the end of the forecast period, North America will have maintained its leadership position through a combination of regulatory-driven demand, high executive turnover risk, and continued corporate emphasis on leadership resilience.

Europe Executive Education Program Market Trends

Europe is expected to hold around 27% of the executive education program market share in 2026, supported by a complex regulatory environment and high cross-border leadership mobility within the European Union (EU). The uptake of these programs is increasing in the region as enterprises are responding to expanding ESG regulations, particularly under EU sustainability and reporting frameworks. Executive mobility across member states is reinforcing the need for standardized yet regionally adaptable leadership capabilities. Public-private skilling initiatives and EU-supported lifelong learning programs are further strengthening institutional demand for executive education across the region.

Competitive dynamics are favoring institutions that are offering multilingual delivery models and deep regulatory expertise across financial reporting, sustainability compliance, and corporate governance. Providers are increasingly integrating region-specific case studies and policy-aligned curricula to address diverse market requirements. As regulatory complexity continues to increase and leadership accountability expands, Europe is expected to maintain steady growth while gradually increasing its share of globally mobile executive learners and cross-border corporate training contracts.

Asia Pacific Executive Education Program Market Trends

Asia Pacific is likely to capture a market share of roughly 25% in 2026, reflecting the region’s expanding corporate base and increasing integration into global value chains. Enterprises across the region are actively investing in leadership capability development as business operations are becoming more international and structurally complex. Government-supported leadership development initiatives, national skilling programs, and public-private partnerships are reinforcing institutional demand for executive education. Digital delivery adoption is accelerating access to global faculty and content, which is supporting rapid market expansion across both developed and emerging economies.

The Asia Pacific market is projected to be the fastest-growing globally, expanding at a CAGR of approximately 13.5% during the 2026-2033 forecast period. Market growth here is being led by major markets such as China, India, Singapore, and Australia, where corporate internationalization and regulatory modernization are increasing leadership skill requirements. Providers are increasingly tailoring programs to regional governance structures, cultural contexts, and industry priorities while maintaining global academic standards. As digital platforms and hybrid delivery models continue to scale, Asia Pacific is expected to strengthen its position as a critical growth engine for the global executive education market.

Competitive Landscape

The global executive education program market structure is moderately fragmented, without being dominated by a single provider. Competition is intensifying among leading institutions as they are differentiating through brand credibility, depth of enterprise relationships, faculty expertise, and digital delivery capability. Established providers are leveraging long-standing corporate partnerships and proprietary intellectual capital to secure multi-year engagements, which is strengthening their competitive positioning. At the same time, newer entrants are facing higher barriers due to accreditation requirements, reputation thresholds, and the rising cost of digital platform development.

Market concentration is increasing gradually as top-tier institutions are expanding through strategic partnerships, technology investments, and selective collaboration with enterprise clients. Providers are investing in proprietary learning platforms, data-driven outcome measurement tools, and global faculty networks to enhance scalability and client retention. These investments are allowing leading players to capture a larger share of high-value corporate contracts while maintaining pricing discipline. As consolidation pressures continue, the competitive landscape is expected to favor institutions that combine academic credibility with enterprise integration and digital execution capability.

Key Industry Developments

- In January 2026, IIT Delhi launched a five-month Executive Programme in Healthcare Entrepreneurship and Management via its Continuing Education Programme (CEP) to equip bachelor's degree holders with skills in design thinking, prototyping, regulatory compliance, commercialization, and venture scaling. Delivered through weekend live online sessions and project-based learning on real-world problems, the program targets professionals to innovate in digital health, AI diagnostics, wearables, and patient-centered care amid India's evolving healthcare challenges.

- October 2025, Wharton Executive Education rolled out "AI in Marketing: Creating Customer Value in an AI-Driven Enterprise," a blended program for senior leaders featuring self-paced online modules, live virtual sessions, and an on-campus immersion. The curriculum covers AI applications in customer experience, search/LLMO, branding, pricing, insights, new product development, and B2B/B2C journeys to drive measurable business outcomes.

- In October 2025, Udacity (part of Accenture) and Woolf launched a fully accredited, project-based Master of Science in Artificial Intelligence degree, costing as little as US$ 3,500 and recognized via ECTS across 60+ countries including the US, Canada, Australia, and Europe. The flexible program comprises 12 Udacity Nanodegrees plus a capstone, enabling prior learners to fast-track via Recognition of Prior Learning.

Companies Covered in Executive Education Program Market

- Harvard Business School Publishing

- INSEAD

- IMD Business School

- London Business School

- Wharton School, University of Pennsylvania

- MIT Sloan Executive Education

- Stanford Graduate School of Business

- CEIBS

- IESE Business School

- HEC Paris

- Kellogg School of Management

- Said Business School, University of Oxford

- ISB Executive Education

- Bocconi School of Management

Frequently Asked Questions

The global executive education program market is projected to reach US$ 55.1 billion in 2026.

Steady rise in corporate reskilling expenditure, high executive turnover risk, and regulatory pressure on governance, sustainability, and digital accountability are driving the market.

The market is poised to witness a CAGR of 11.2% from 2026 to 2033.

Channeling of learning and development budgets by corporate entities toward shorter, outcome-linked executive programs rather than degree-centric education, proliferation of AI, tightening ESG compliance requirements, and geopolitical volatility are key market opportunities.

Harvard Business School Publishing, INSEAD, IMD Business School, and London Business School are some of the key players in the market.