- Industrial Machinery

- Electric Traction Motor Market

Electric Traction Motor Market Size, Share, and Growth Forecast 2026 - 2033

Electric Traction Motor Market by Motor Type (AC Motor, DC Motor), Power Rating (Below 200kW, 200kW to 400kW, Above 400kW), Application (Railways, Electric Vehicle, Others), and Regional Analysis, 2026 - 2033

Electric Traction Motor Market Size and Trend Analysis

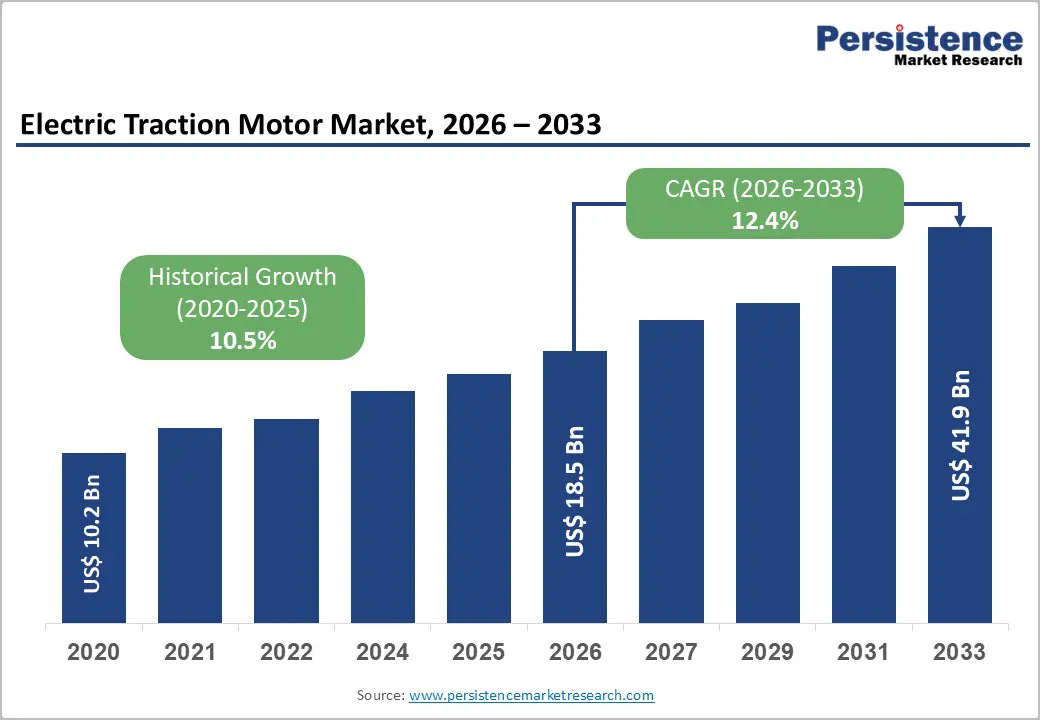

The global electric traction motor market is expected to reach US$18.5 billion in 2026 and US$41.9 billion by 2033, growing at a CAGR of 12.4% over the forecast period from 2026 to 2033. The market's robust expansion is principally driven by the global acceleration of electric vehicle adoption, rapid electrification of railway networks, and increasingly stringent government mandates on carbon emission reductions across transportation sectors.

Key Market Highlights

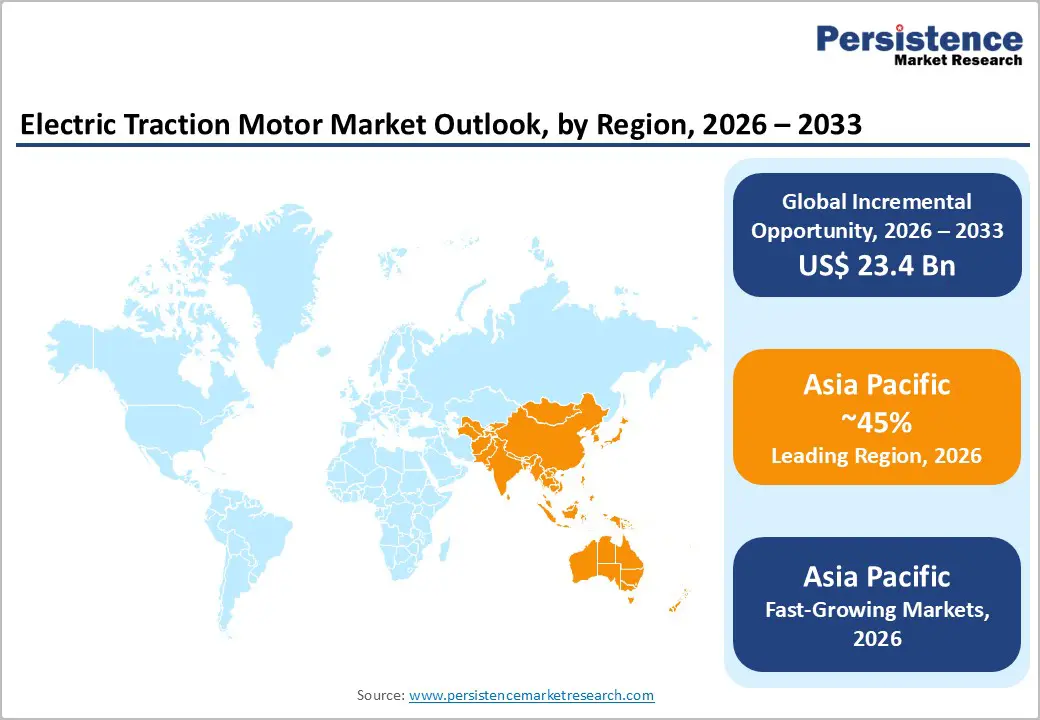

- Leading Region: Asia Pacific leads the global electric traction motor market with approximately 45% revenue share, anchored by China's massive EV and high-speed rail sectors, alongside rapidly expanding railway electrification and urban metro programs in India and Japan

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region through 2033, driven by India's accelerating EV adoption under the PM E-Drive scheme, China's continued rail network expansion, and growing EV manufacturing ecosystems across ASEAN nations including Vietnam, Thailand, and Indonesia

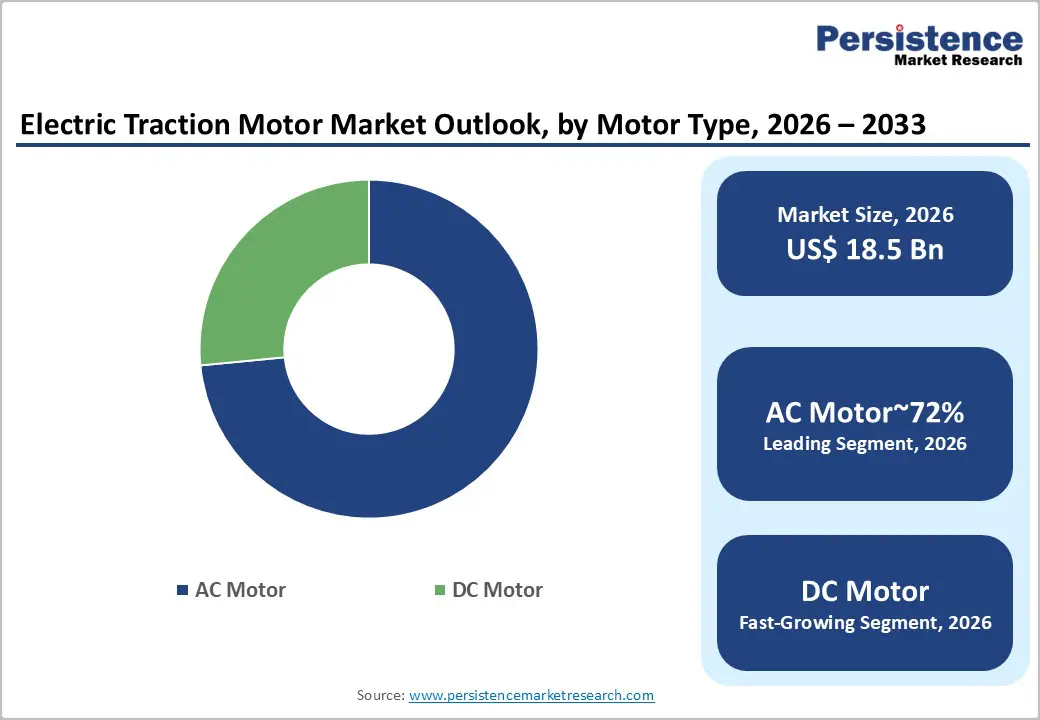

- Leading Segment: AC Motors dominate the By Motor Type category with approximately 72% market share, reflecting the industry-wide preference for permanent magnet synchronous and induction motor architectures that deliver upto 95% energy conversion efficiency in both EV and railway traction applications

- Fastest-Growing Segment: The Electric Vehicle (EV) application segment is the fastest-growing category, driven by the global EV fleet surpassing 40 million units in 2023 and binding zero-emission vehicle mandates across major economies requiring 100% zero-emission new car sales by 2035

- Key Opportunity: Integration of SiC power electronics with advanced axial flux motor architectures represents the most valuable near-term opportunity, enabling 50% volume reduction at equivalent power output and supporting premium EV and next-generation high-speed rail applications through 2033

| Key Insights | Details |

|---|---|

|

Electric Traction Motor Market Size (2026E) |

US$ 18.5 Billion |

|

Market Value Forecast (2033F) |

US$ 41.9 Billion |

|

Projected Growth CAGR (2026–2033) |

12.4% |

|

Historical Market Growth (2020–2025) |

10.5% |

DRO Analysis

Drivers - Surging Global Electric Vehicle Adoption Fueling Unprecedented Demand for Traction Motors

The rapid global shift toward electric mobility is the most important growth driver for the electric traction motor market. Traction motors are essential powertrain components in battery-electric vehicles (BEVs) and hybrid electric vehicles (HEVs), making market growth directly linked to rising EV production. According to the International Energy Agency (IEA) Global EV Outlook 2024, the global EV fleet could reach 300 million vehicles by 2030 under accelerated transition scenarios.

Major economies such as the European Union, the United States, and China are implementing timelines to phase out internal combustion engine vehicles. China alone accounted for nearly 60% of global EV sales in 2023, driving strong demand for domestically produced traction motors. Automotive manufacturers are increasingly adopting permanent magnet synchronous motors (PMSMs), a type of AC motor known for its 92–97% energy efficiency, which helps improve vehicle range and overall performance.

Large-Scale Railway Electrification Programs Across Emerging and Developed Economies

Expanding railway electrification programs are another major driver of demand in the electric traction motor market. Governments around the world are promoting rail transport as a cleaner and more sustainable alternative, investing in high-speed rail, intercity networks, metro systems, and freight corridors. India’s Ministry of Railways achieved 100% electrification of its broad-gauge railway network, covering more than 65,000 route kilometres by 2023, marking a major infrastructure milestone and a steady source of demand for traction motors.

In Europe, the European Commission’s Sustainable and Smart Mobility Strategy aims to double high-speed rail traffic by 2030 and triple it by 2050. This requires large-scale fleet upgrades and procurement of modern electric locomotives and trains equipped with advanced traction motors. Such long-term infrastructure investments create stable, multi-year demand pipelines for manufacturers.

Restraints - High Capital Costs and Supply Chain Dependencies for Rare Earth Materials

One of the key challenges in the electric traction motor market is the heavy reliance on rare-earth materials, such as neodymium, dysprosium, and praseodymium, which are essential for permanent-magnet motors. According to the U.S. Geological Survey (USGS), China controls about 85% of global rare earth processing capacity, creating a highly concentrated supply chain. This dependence leads to price fluctuations that can significantly increase traction motor production costs.

Higher material costs directly impact OEM margins and may delay product development, especially for mid-sized manufacturers with limited risk management strategies. This supply vulnerability has become a strategic concern for regions such as Europe, Japan, and the United States. While efforts are underway to diversify supply sources and reduce dependency, most initiatives are still in early stages, which remains a persistent restraint on market growth.

Technical Complexity of Motor Integration in High-Speed and Heavy-Load Rail Applications

The complexity involved in integrating traction motors into high-speed and heavy-load rail systems remains a significant technical and commercial challenge. These motors must operate reliably under extreme temperatures, high vibration, and varying load conditions, requiring advanced engineering and rigorous testing. Compliance with standards set by organizations such as the International Electrotechnical Commission (IEC) and the European Union Agency for Railways (ERA) further adds to the complexity.

The validation and certification process for new traction motor platforms can take between 18 and 36 months, slowing down the pace of innovation and adoption. These long development cycles also create high entry barriers for new players, as buyers prefer established manufacturers with proven performance records. As a result, procurement decisions tend to favor experienced vendors, thereby limiting market competition.

Opportunities - Electrification of Commercial Vehicles and Last-Mile Logistics Fleets

The electrification of commercial vehicles, including buses, trucks, and last-mile delivery fleets, presents a strong growth opportunity for traction motor manufacturers. According to the International Council on Clean Transportation (ICCT), zero-emission vehicles must account for more than 60% of new commercial vehicle sales in leading markets by 2030 to meet climate goals.

Many cities across Europe and Asia, including London, Paris, Shenzhen, and Singapore, are setting deadlines to phase out diesel buses and transition to fully electric fleets. Electric buses typically require traction motors in the 200kW to 400kW range, making this a high-value and high-volume segment. Companies with expertise in automotive and rail applications are well-positioned to benefit from this shift. Manufacturers that develop scalable and modular motor platforms capable of serving multiple vehicle types with minimal redesign can secure long-term contracts and gain a competitive advantage.

Integration of SiC Power Electronics and Axial Flux Motor Technologies

A major technological opportunity is emerging through the integration of advanced motor designs with next-generation power electronics. Silicon Carbide (SiC)- based inverters offer higher efficiency, improved thermal performance, and greater power density than traditional silicon-based systems. Leading automotive companies such as Tesla, BYD, and Toyota are actively adopting SiC-based technologies in their EV platforms, creating new collaboration opportunities for traction motor manufacturers.

At the same time, axial flux motors are gaining attention for their compact size and the ability to deliver up to 50% higher power density than conventional designs. These motors are especially suitable for premium EVs and specialized applications. Manufacturers investing in SiC-compatible systems and axial flux technologies are likely to capture high-growth and high-margin segments, positioning themselves strongly for the 2026–2033 forecast period.

Category-wise Analysis

By Motor Type Insights

AC motors dominate the global electric traction motor market, accounting for around 72% of total revenue. This strong position reflects a clear shift toward technologies such as permanent magnet synchronous motors (PMSMs) and induction motors, which offer higher efficiency and lower maintenance compared to traditional DC motors. These motors are also compatible with regenerative braking systems, making them ideal for both electric vehicles and railway applications.

Leading companies such as Siemens, ABB, and Alstom have standardized AC motor technologies in their rail platforms, using advanced drive systems to optimize performance across different speeds. According to the IEA, AC motor systems can achieve efficiencies of approx 95%, significantly higher than the 80% typically seen in DC systems. While DC motors are still used in older railway systems and some industrial applications, their overall market share continues to decline steadily.

By Power Rating Insights

The 200kW to 400kW power segment leads the electric traction motor market, contributing approximately 45% of total revenue. This segment is widely used across applications such as electric buses, metro systems, regional trains, and light rail vehicles. It represents an optimal balance between performance, size, and energy efficiency, making it highly suitable for urban and regional transportation needs.

Government initiatives, particularly in Europe, are further boosting demand in this category. For example, the EU Clean Vehicle Directive requires that 45% of public bus purchases meet zero-emission standards by 2025. Meanwhile, the above 400kW segment, though smaller in volume, is the fastest-growing category. It is driven by increasing demand from high-speed rail networks, heavy freight locomotives, and large industrial vehicles such as mining equipment.

By Application Insights

The Electric Vehicle (EV) segment is the largest application area in the electric traction motor market, accounting for about 52% of total revenue. This growth is driven by rapid global EV adoption, supported by stringent emissions regulations and government incentives in regions such as Europe, the United States, China, and South Korea. According to the IEA, the global EV fleet exceeded 40 million vehicles in 2023 and continues to grow each year.

The railway segment is the second-largest application, supported by consistent procurement cycles and higher product value. Traction motors used in railways are designed for long operational lifespans and demanding conditions, which increases their average selling price. As a result, even with lower unit volumes compared to EVs, railway applications contribute significantly to overall market revenue.

Regional Insights

North America Electric Traction Motor Market Trends

North America is a technology-driven and policy-supported market for electric traction motors. The U.S. Inflation Reduction Act (IRA) of 2022 has allocated over USD 370 billion toward clean energy and transportation, including incentives for EV production and zero-emission transit systems. This has encouraged companies such as General Motors and Ford to invest heavily in domestic EV manufacturing and supply chains.

The funding from the Federal Transit Administration (FTA) is supporting the adoption of electric buses across major cities. Canada is also investing in the electrification of rail networks, while the U.S. Infrastructure Investment and Jobs Act is driving modernization of passenger rail systems. The region benefits from strong automotive R&D hubs in states like Michigan, Ohio, and Tennessee, fostering innovation in advanced motor technologies, including axial flux designs and SiC-integrated systems.

Europe Electric Traction Motor Market Trends

Europe has one of the most advanced ecosystems for electric traction motors, supported by strong regulatory frameworks such as the European Green Deal and Fit for 55. Germany leads the region, driven by major automotive manufacturers like Volkswagen, BMW, and Mercedes-Benz, along with significant investments in rail infrastructure. The German government has committed EUR 45 billion toward railway development through 2027, boosting demand for traction motors.

Countries like France and the United Kingdom are also focusing on rail decarbonization, with the UK planning to phase out diesel-only trains by 2040. Spain is emerging as an important EV production hub, attracting investments from global automakers. Additionally, the EU’s target of achieving 100% zero-emission new vehicle sales by 2035 provides long-term demand certainty for traction motor manufacturers.

Asia Pacific Electric Traction Motor Market Trends

Asia Pacific is the largest and fastest-growing region in the electric traction motor market, accounting for approximately 45% of global revenue. China dominates the region, being the largest EV market and home to the world’s most extensive high-speed rail network. The country operates over 42,000 kilometers of high-speed rail and continues to expand rapidly. Domestic companies benefit from strong supply chains and government support.

Japan contributes with advanced technologies through companies like Mitsubishi Electric and Kawasaki Heavy Industries. India is also experiencing rapid growth, supported by large-scale railway electrification and EV initiatives such as the FAME-II and PM E-Drive schemes. Expanding metro networks across major cities like Delhi, Mumbai, and Bengaluru further drive demand for traction motors in the region.

Competitive Landscape

The electric traction motor market is moderately consolidated, with a few major global players such as ABB, Siemens, Alstom, and Mitsubishi Electric holding significant market shares. These companies compete by offering integrated solutions that combine motors, inverters, and control systems, along with strong after-sales services.

Long-term contracts with OEMs and continuous investment in R&D provide them with a competitive edge. Key innovation areas include SiC-compatible systems, axial flux motor designs, and predictive maintenance technologies. At the same time, emerging Chinese manufacturers are gaining market share by offering cost-effective solutions and leveraging strong domestic demand. Their competitive pricing strategies are increasing pressure on established global players, particularly in price-sensitive markets, intensifying competition across the industry.

Key Developments:

- In March 2025: Siemens Mobility secured a framework contract with Deutsche Bahn to supply next-generation high-speed trainsets equipped with advanced permanent magnet traction motors, strengthening its leadership in Europe’s rail electrification and high-speed rolling stock modernization market.

- In January 2025: Nidec Corporation launched its third-generation E-Axle traction motor system, offering 20% higher power density and integrated Silicon Carbide (SiC) inverter compatibility, enhancing efficiency and performance while expanding its competitive position among global electric vehicle OEM suppliers.

- In October 2024: ABB partnered with a major Indian metro rail authority to supply traction converters and motor systems for a 72-train urban fleet, strengthening its presence in South Asia’s rapidly expanding urban rail electrification and smart mobility infrastructure segment.

Companies Covered in Electric Traction Motor Market

- ABB

- Alstom

- Siemens

- Bosch

- Nidec Motor Corporation

- Ametek

- Johnson Electric

- Škoda Transportation a.s.

- Traktionssysteme Austria

- Mitsubishi Electric Corporation

- Kawasaki Heavy Industries, Ltd.

- Vem Group

- CRRC Corporation Limited

Frequently Asked Questions

The global Electric Traction Motor Market is estimated at US$ 18.5 Billion in 2026 and is projected to reach US$ 41.9 Billion by 2033, growing at a CAGR of 12.4%, driven by accelerating EV adoption and global railway electrification programs backed by governments in Asia Pacific, Europe, and North America.

The primary growth drivers are the rapid global adoption of electric vehicles, with the IEA reporting over 14 million EV units sold in 2023, and large-scale government-backed railway electrification programs, such as India's completion of 100% broad-gauge rail electrification across 65,000+ route kilometers in 2023 and Europe's high-speed rail capacity doubling target by 2030.

AC Motors are the dominant segment, commanding approximately 72% of total market share, owing to their superior energy conversion efficiency of 90–97%, compatibility with regenerative braking systems, and widespread adoption by global EV and railway OEMs including Siemens, ABB, Tesla, and BYD in permanent magnet synchronous motor configurations.

Asia Pacific leads with approximately 45% of global market revenues, anchored by China's position as both the world's largest EV market and the operator of over 42,000 kilometers of high-speed rail, alongside rapidly expanding traction motor demand from India's railway electrification and metro network development programs.

The integration of Silicon Carbide (SiC) power electronics with axial flux motor architectures presents the highest-value growth opportunity, enabling up to 50% motor volume reduction, superior power density, and efficiency gains that are critical for premium EV and next-generation high-speed rail platforms, segments where margin potential and technology differentiation are highest.

The leading participants include ABB, Siemens, Alstom, Bosch, Mitsubishi Electric Corporation, Nidec Motor Corporation, Kawasaki Heavy Industries, Škoda Transportation a.s., Traktionssysteme Austria, Johnson Electric, Ametek, and Vem Group, with CRRC Corporation, Hitachi Rail, and Toshiba Infrastructure Systems also maintaining significant market presence in the Asia Pacific region.