- Communication Infrastructure & Services

- Data Center Insulation Market

Data Center Insulation Market Size, Share, and Growth Forecast, 2026 - 2033

Data Center Insulation Market by Material (Mineral Wool, Flexible Elastomeric Foam, Others), Insulation Type (Thermal Insulation, Acoustic Insulation, Others), Application, End-user, and Regional Analysis for 2026 - 2033

Data Center Insulation Market Size and Trends Analysis

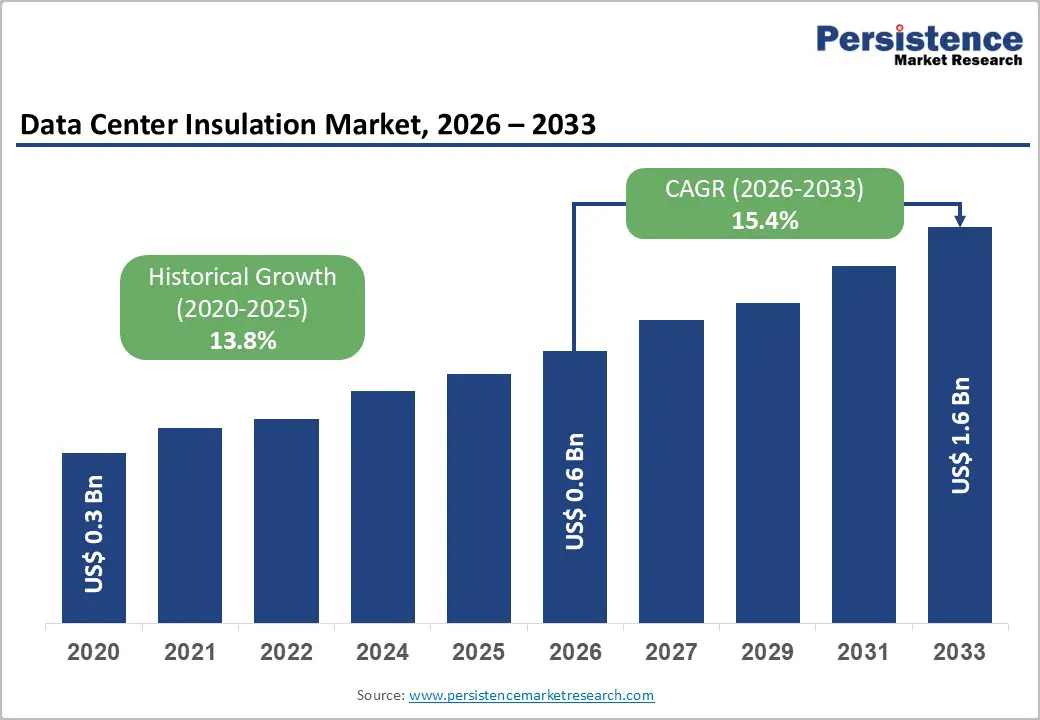

The global data center insulation market size is likely to be valued at US$0.6 billion in 2026 and is expected to reach US$1.6 billion by 2033, growing at a CAGR of 15.4% between 2026 and 2033, driven by rapid hyperscale and AI-focused data center expansion, stricter energy-efficiency regulations, and rising demand for fire-resistant, thermally stable, and acoustically optimized infrastructure.

Cooling systems account for a significant share of data center energy consumption, and the growing density of servers is increasing the importance of advanced insulation systems. Governments and regulatory authorities are also encouraging higher-performance building envelopes, creating stronger demand for insulation across walls, roofs, ducts, pipes, and raised-floor assemblies.

Key Industry Highlights

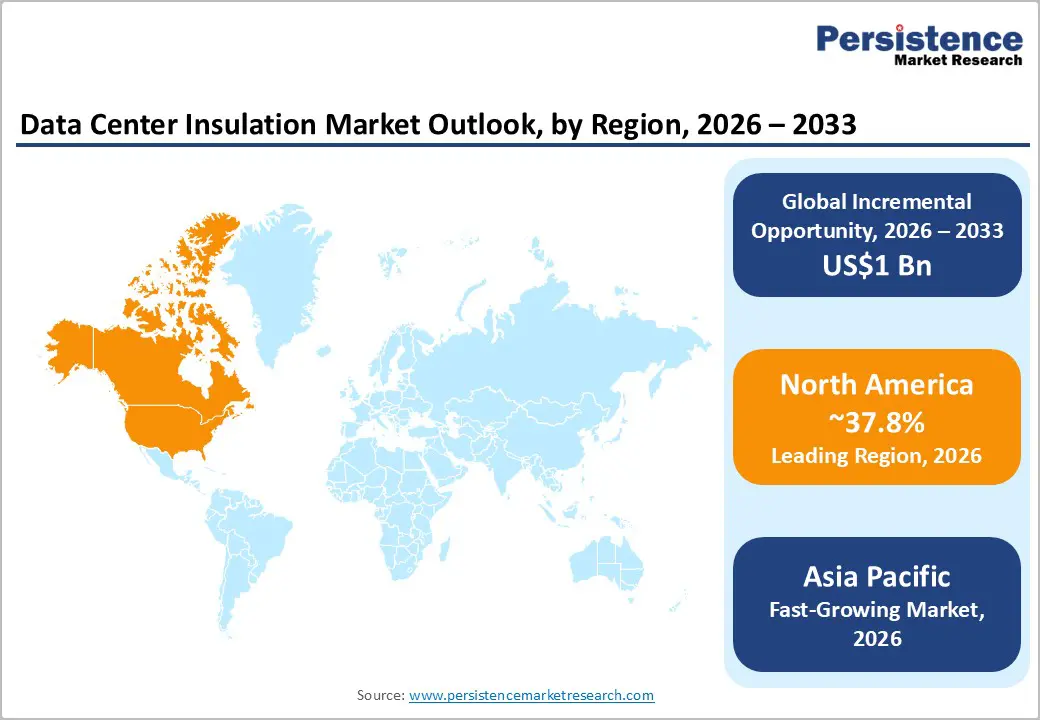

- Leading Region: North America is projected to lead with approximately 37.8% market share in 2026, supported by strong hyperscale investments, AI-driven infrastructure expansion, and advanced energy-efficiency standards across the U.S. and Canada.

- Fastest-growing Region: Asia Pacific is projected to register the fastest growth, driven by rapid cloud adoption, digital transformation, hyperscale expansion, and rising investments across China, India, Singapore, and Southeast Asia.

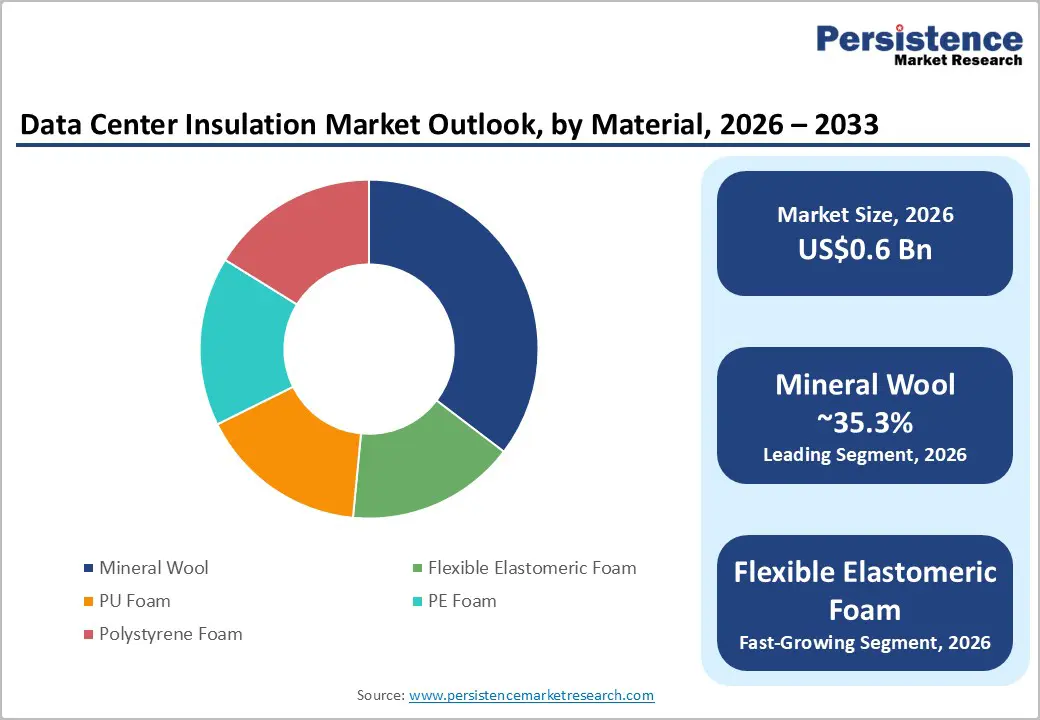

- Dominant Material: Mineral wool remains the leading material segment with an anticipated 35.3% market share in 2026, supported by superior fire resistance, thermal stability, and acoustic insulation performance in mission-critical environments.

- Leading Insulation Type: Thermal insulation is estimated to dominate with 74.5% of market share in 2026, reflecting growing emphasis on cooling efficiency, thermal containment, and energy optimization in hyperscale and colocation data centers.

DRO Analysis

Drivers- AI-Led Capacity Expansion is Increasing Thermal Loads and Insulation Intensity

The rapid expansion of artificial intelligence workloads, cloud computing infrastructure, and hyperscale facilities is significantly increasing thermal loads inside data centers. Global data-center electricity consumption is projected to exceed 945 TWh by 2030, with AI workloads emerging as a major contributor to energy demand growth. Cooling and environmental control systems already represent a considerable portion of operational energy consumption, especially in enterprise facilities with lower energy efficiency standards.

This trend is directly strengthening demand for advanced insulation materials because improved thermal management reduces cooling losses, stabilizes internal temperatures, and minimizes condensation risks. High-density computing environments require precise environmental control to maintain operational reliability and prevent equipment failure. As a result, operators are investing in high-performance insulation systems for HVAC piping, walls, roofs, and server room infrastructure.

Government agencies and industry organizations are also prioritizing energy-efficient cooling technologies and sustainable infrastructure development. These initiatives are encouraging data center developers to integrate insulation systems that improve thermal efficiency while lowering long-term operating expenses.

Regulation and Design Standards are Turning Insulation into an Efficiency Requirement

Regulatory frameworks focused on energy efficiency and sustainability are becoming increasingly important for data center operators worldwide. In Europe, energy-efficiency regulations now require large data centers to monitor and report operational performance metrics, including energy use and cooling efficiency. Similar standards are influencing infrastructure development in North America and Asia Pacific.

Industry standards for energy-efficient data center design are also supporting the adoption of advanced insulation solutions. These frameworks encourage operators to improve HVAC performance, reduce heat transfer, and strengthen thermal containment strategies. Insulation is no longer viewed as a secondary construction material but as a critical component of operational efficiency and sustainability compliance.

The growing emphasis on environmental performance is also increasing demand for certified insulation systems with verified fire resistance, acoustic control, and moisture management capabilities. Data center developers are prioritizing solutions that support lower energy intensity, improved resilience, and reduced lifecycle operating costs. This regulatory shift is expected to strengthen long-term demand for premium insulation products across both new construction and retrofit projects.

Restraint - High Installation Costs and Complex Performance Requirements

One of the primary restraints in the market is the high cost and technical complexity associated with advanced insulation systems. Mission-critical facilities require insulation materials capable of delivering multiple performance characteristics simultaneously, including fire resistance, moisture protection, thermal stability, acoustic control, and compatibility with HVAC infrastructure.

These requirements increase engineering complexity, testing procedures, and coordination among contractors responsible for cooling systems, structural components, and fire protection. Installation quality is also critical as poor workmanship can reduce insulation effectiveness and increase operational risks.

Supply-chain volatility in specialty insulation materials, technical foams, and laminated products can further increase procurement costs and project delays. Smaller operators may hesitate to invest in premium insulation systems because of higher upfront expenditures, even when lifecycle energy savings are favorable. Consequently, adoption rates are generally stronger among hyperscale and large colocation operators with greater financial flexibility and long-term efficiency objectives.

Opportunity - Hyperscale and Colocation Expansion in Asia Pacific

Asia Pacific represents one of the most significant growth opportunities for the Data Center Insulation Market. Rapid digitalization, cloud adoption, e-commerce expansion, and AI deployment are accelerating demand for new hyperscale and colocation facilities across China, India, Japan, Singapore, South Korea, and Southeast Asia.

Regional data-center capacity is projected to increase substantially through 2030, supported by strong investment activity from global cloud providers and colocation operators. Since many of these facilities are newly constructed, developers have greater flexibility to integrate modern insulation systems into walls, roofs, ducts, cooling systems, and plant-room infrastructure.

Manufacturing expansion within the region is also improving material availability and reducing supply-chain dependence on imports. Several insulation manufacturers are investing in new production facilities across India and Southeast Asia to strengthen local supply networks. These developments are creating long-term opportunities for insulation vendors specializing in fire-resistant, thermally efficient, and acoustic-control solutions tailored for large-scale digital infrastructure projects.

Retrofit and Energy-Efficiency Upgrade Projects

Retrofit and modernization projects are emerging as another major growth opportunity for insulation providers. Many existing data centers were designed before current energy-efficiency standards became widespread, creating significant opportunities for upgrades focused on thermal management and cooling optimization.

Operators are increasingly investing in duct insulation, pipe insulation, acoustic barriers, and thermal containment systems to improve power usage efficiency and reduce operating costs. Noise reduction is becoming particularly important in urban colocation facilities and mixed-use developments where acoustic performance influences site approvals and operational compliance.

The growing emphasis on sustainability reporting and energy monitoring is also encouraging operators to modernize existing facilities with higher-performance insulation materials. Advanced products such as mineral wool and flexible elastomeric foam are gaining popularity because they provide thermal efficiency, fire safety, moisture resistance, and acoustic control within a single integrated solution.

Category-wise Analysis

Material Insights

Mineral wool is anticipated to account for approximately 35.3% of the market share in 2026, making it the leading material segment. Its dominance is supported by strong fire resistance, thermal stability, and acoustic insulation performance, which are critical for mission-critical facilities. The material is widely used in walls, roofs, raised floors, and firestop systems in hyperscale facilities operated by companies such as Equinix and Digital Realty. Its ability to withstand high temperatures and support operational safety makes it highly suitable for high-density computing environments.

Flexible elastomeric foam is anticipated to witness the fastest growth. Growth is driven by superior moisture resistance, thermal efficiency, and flexibility in HVAC and chilled-water applications. The closed-cell structure minimizes condensation and energy loss, making it ideal for cooling-intensive AI and colocation facilities. Companies such as Armacell are expanding elastomeric foam solutions for advanced HVAC insulation, while hyperscale operators increasingly adopt these systems to improve cooling efficiency and lower operational costs.

Insulation Type Insights

Thermal insulation is anticipated to hold more than 74.5% of the market share in 2026, maintaining its position as the dominant insulation type. The segment leads as effective temperature management is essential for reducing cooling demand, improving energy efficiency, and maintaining stable server performance.

Thermal insulation is extensively integrated into walls, roofs, ducts, pipes, and raised floors in large-scale facilities operated by cloud providers such as Amazon Web Services and Microsoft Azure. Rising server density and AI-driven workloads are further increasing demand for high-performance thermal management systems.

Acoustic insulation is anticipated to be the fastest-growing segment during the forecast period, supported by increasing demand for noise reduction in colocation and urban data center environments. Cooling systems, generators, and high-density server infrastructure create substantial noise levels, encouraging operators to invest in sound-absorbing insulation materials.

Growth is particularly strong in densely populated regions across Europe and Asia Pacific, where compliance with noise-control regulations is becoming more important. Mineral wool and specialized acoustic insulation products are gaining adoption because they provide both sound absorption and thermal performance benefits.

Regional Insights

North America Data Center Insulation Market Trends

North America accounts for approximately 37.8% of the market share in 2026, making it the leading regional market. Strong demand for hyperscale infrastructure, AI-focused computing capacity, and cloud services continues to support large-scale construction activity across the U.S. and Canada.

U.S. Data Center Insulation Market Trends

The U.S. dominates the market due to its strong concentration of hyperscale facilities, AI infrastructure investments, and cloud service providers. Major data center hubs, including Virginia, Texas, Arizona, and Georgia, continue to attract large-scale investments because of favorable connectivity, tax incentives, and access to power infrastructure.

Rising server density and increasing electricity consumption are strengthening demand for advanced thermal insulation systems that improve cooling efficiency and reduce operational costs. Sustainability initiatives and energy-efficiency standards are also accelerating the adoption of high-performance insulation materials across hyperscale and colocation facilities.

Canada Data Center Insulation Market Trends

Canada is emerging as a significant market for data center insulation solutions due to growing cloud adoption, renewable energy availability, and favorable climatic conditions for free cooling. Cities such as Toronto, Montreal, and Vancouver are witnessing increased data center investments supported by strong connectivity infrastructure and government-backed digital initiatives.

Cooler ambient temperatures help reduce cooling costs, although operators still require advanced insulation systems to improve thermal management and energy efficiency. The country’s focus on sustainable infrastructure development is also encouraging the adoption of environmentally friendly insulation materials.

Europe Data Center Insulation Market Trends

Europe represents a highly regulated and sustainability-focused market for data center insulation solutions. Demand is concentrated in major digital infrastructure hubs, including the U.K., Germany, France, and the Netherlands.

Germany Data Center Insulation Market Trends

Germany represents one of the largest data center markets in Europe, supported by strong industrial digitalization, enterprise IT demand, and hyperscale expansion. Frankfurt remains a leading regional data center hub due to its connectivity advantages and large colocation ecosystem. Strict energy-efficiency regulations and sustainability requirements are driving demand for advanced insulation systems capable of improving thermal performance and reducing energy consumption. Fire-resistant mineral wool products are particularly popular because of stringent building safety standards.

U.K. Data Center Insulation Market Trends

The U.K. continues to be a major contributor to the European Data Center Insulation Market, with London serving as one of the region’s largest colocation and cloud infrastructure hubs. Rising demand for AI computing, cloud storage, and enterprise outsourcing is driving the expansion of hyperscale and colocation facilities. Operators are increasingly investing in advanced thermal and acoustic insulation systems to improve cooling efficiency and comply with environmental regulations. Retrofit activity is also growing as older facilities modernize infrastructure to meet sustainability targets.

France Data Center Insulation Market Trends

France is witnessing steady growth in data center infrastructure investments due to expanding cloud adoption and government support for digital transformation. Paris remains a key market for colocation and enterprise data centers. Sustainability policies and energy-efficiency requirements are encouraging operators to adopt high-performance insulation materials that reduce cooling demand and operational costs. Increasing interest in waste-heat recovery systems is also supporting demand for advanced thermal insulation solutions.

Spain Data Center Insulation Market Trends

Spain is becoming an attractive destination for hyperscale data center development because of improved renewable energy availability, lower land costs, and strategic connectivity advantages. Madrid and Barcelona are emerging as important data center locations for cloud providers and colocation operators. Rising construction activity is creating demand for insulation systems that support thermal management and energy optimization in cooling-intensive environments.

Asia Pacific Data Center Insulation Market Trends

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of approximately 16.2% during the forecast period.

China Data Center Insulation Market Trends

China leads the Asia Pacific data center insulation market in terms of infrastructure expansion and capacity additions. Strong domestic demand for cloud computing, AI services, and digital platforms is driving the construction of large-scale hyperscale facilities. Government initiatives focused on digital infrastructure modernization and energy efficiency are encouraging the adoption of advanced thermal insulation systems. High-density computing environments and rising cooling requirements are increasing demand for HVAC insulation and fire-resistant materials.

India Data Center Insulation Market Trends

India is one of the fastest-growing markets in the region due to rapid digitalization, rising internet penetration, and strong investment activity from hyperscale operators. Major cities, including Mumbai, Chennai, Hyderabad, and Bengaluru, are witnessing significant data center construction activity.

Government support for digital infrastructure development and increasing localization of insulation manufacturing are improving market growth prospects. High ambient temperatures are also increasing demand for advanced thermal insulation systems that reduce cooling energy consumption.

Japan Data Center Insulation Market Trends

Japan remains an important market for data center insulation solutions because of its advanced technology ecosystem and strong enterprise demand. Tokyo and Osaka continue to attract investments in colocation and cloud infrastructure. Operators are focusing on energy-efficient cooling systems and earthquake-resilient infrastructure, increasing demand for durable and high-performance insulation materials. Space constraints in urban environments are also driving the adoption of compact and efficient insulation solutions.

Competitive Landscape

The global data center insulation market is moderately fragmented, with competition spread across global insulation manufacturers, HVAC solution providers, and fire-protection material suppliers. The market includes a wide range of products such as mineral wool, elastomeric foam, aerogel insulation, PU foam, and acoustic insulation systems. Leading companies are focusing on innovation, localized manufacturing, and specification-driven sales strategies.

Market participants are investing in advanced insulation materials that combine fire protection, thermal efficiency, moisture resistance, and acoustic performance within integrated systems. Digital engineering tools, sustainability-focused product development, and partnerships with data center developers are becoming increasingly important competitive differentiators.

Key Industry Developments:

- In March 2026, ROCKWOOL Group released a new technical bulletin titled “Designing Resilient Data Centers with Stone Wool Insulation,” focused on improving fire protection, acoustic control, and thermal performance for hyperscale and AI-driven data center facilities.

- In May 2026, ROCKWOOL Group signed an agreement to acquire Ravago’s stone wool factory in Hungary to strengthen its manufacturing footprint in Central and Eastern Europe and improve supply capabilities for growing regional insulation demand.

Companies Covered in Data Center Insulation Market

- ROCKWOOL Group

- Armacell

- Kingspan Group

- Saint-Gobain

- Owens Corning

- Knauf Insulation

- Johns Manville

- Promat

- Recticel

- URSA

- Aspen Aerogels

- BASF

- NMC

- Celotex

- Huntsman Corporation

- K-FLEX

Frequently Asked Questions

The global data center insulation market is anticipated to be valued at US$0.6 billion in 2026.

The market is expected to reach approximately US$1.6 billion by 2033.

The data center insulation market is projected to grow at a CAGR of 15.4% between 2026 and 2033.

Key trends include increasing adoption of AI-ready hyperscale facilities, growing use of energy-efficient thermal insulation systems, rising demand for acoustic insulation in urban colocation centers, expansion of retrofit projects, and stronger regulatory emphasis on sustainability and fire safety compliance.

Mineral wool is anticipated to remain the leading material segment with approximately 35.3% market share, supported by its superior fire resistance, thermal stability, and acoustic insulation performance.

Major companies include ROCKWOOL Group, Armacell, Kingspan Group, Saint-Gobain, and Owens Corning.