- Industrial Machinery

- Dairy Filtration Systems Market

Dairy Filtration Systems Market Size, Share, and Growth Forecast 2026 - 2033

Dairy Filtration Systems Market by Filtration Type (Reverse Osmosis (RO), Ultrafiltration (UF), Microfiltration (MF), Nanofiltration (NF), Cross-flow Filtration), by Module Design (Spiral Wound, Tubular, Plate & Frame, Hollow Fiber), Application (Processed Milk, Milk Powder, Cheese, Yogurt, Cream, Whey Protein, Others), End-user, and Regional Analysis, 2026 - 2033

Dairy Filtration Systems Market Size and Trend Analysis

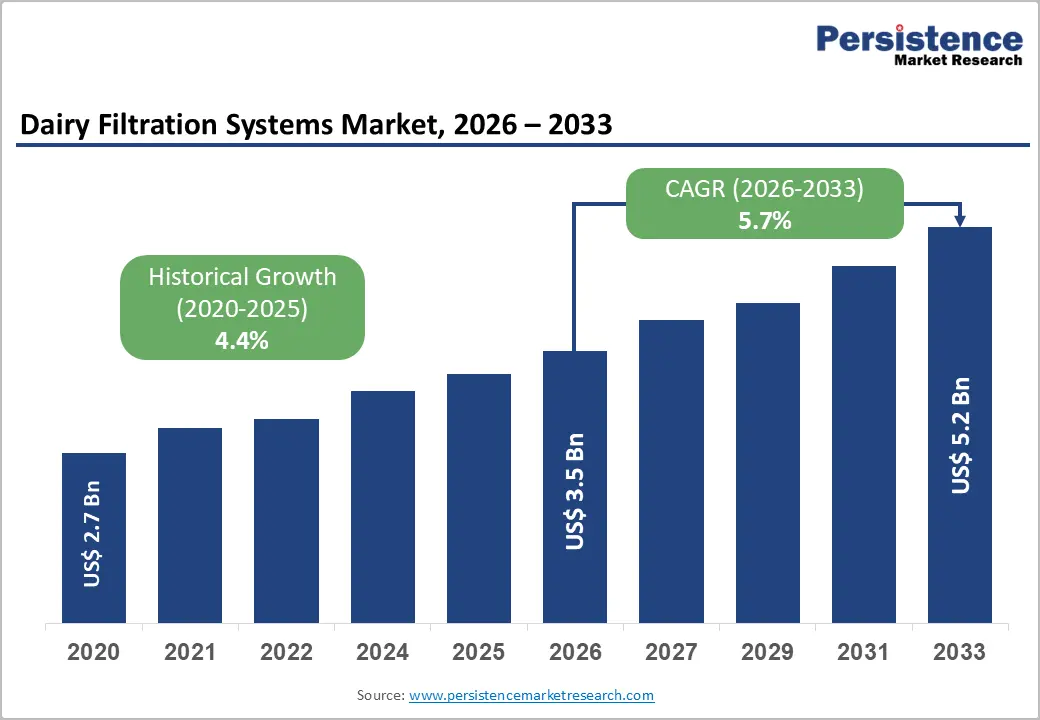

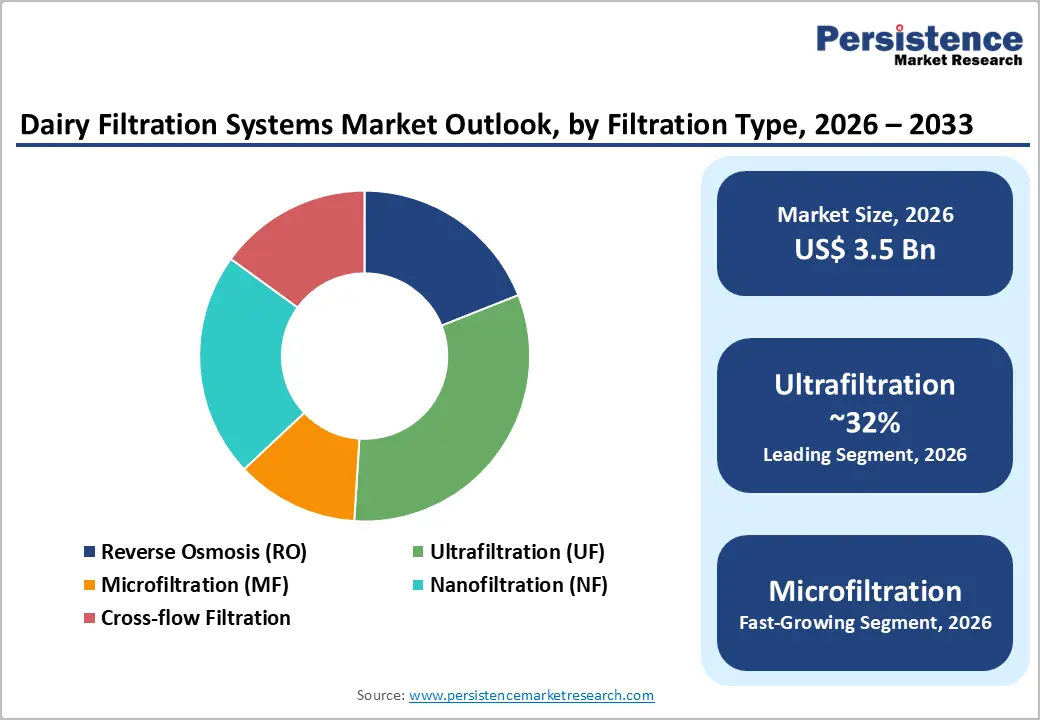

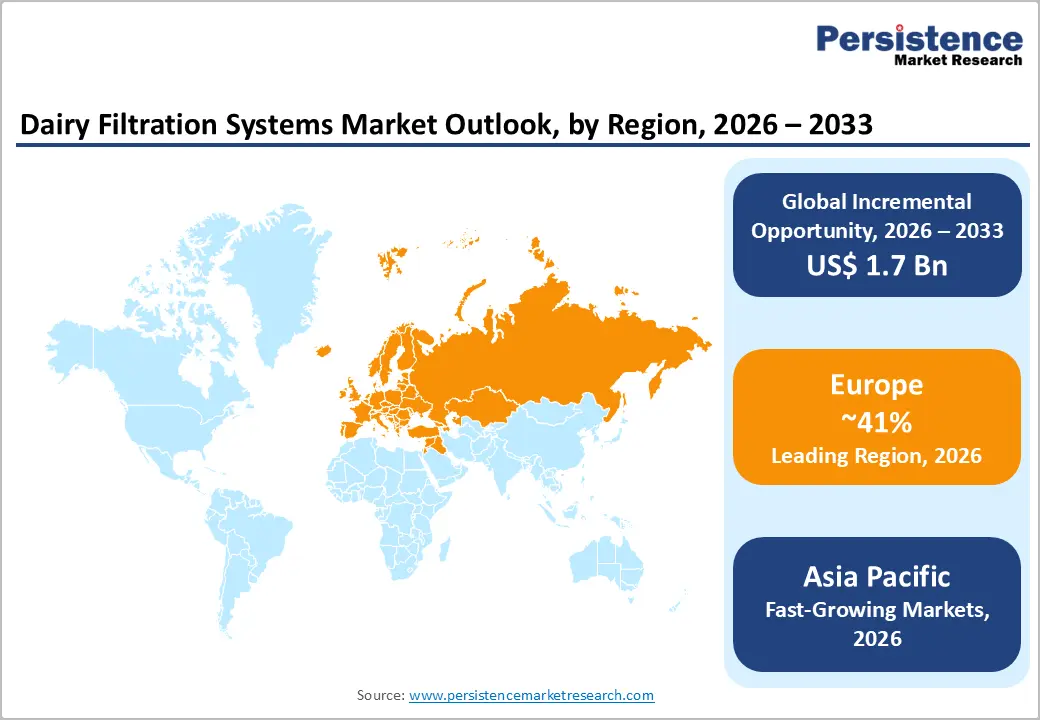

The global dairy filtration systems market size is likely to be valued at US$ 3.5 billion in 2026 and is expected to reach US$ 5.2 billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033.

The dairy filtration systems market is experiencing accelerating growth, driven by the convergence of surging global dairy consumption, the explosive rise of high-protein and functional dairy product categories, and increasingly stringent food safety and hygiene regulations that mandate advanced membrane-based processing.

Key Industry Highlights:

- Leading Region: Europe leads the dairy filtration systems market, holding 41% share, as the world's largest dairy exporter with over 155 million tonnes of annual milk production, supported by harmonized EU hygiene regulations, strong whey ingredient exports, and global equipment manufacturers including GEA Group and Alfa Laval.

- Fastest Growing Region: Asia Pacific is the fastest growing region with rising CAGR driven by China's processing modernization under the 14th Five-Year Plan, India's vast under-filtered 230-million-tonne milk production base, and expanding ASEAN dairy consumption generating strong filtration equipment investment demand.

- Dominant Segment: Ultrafiltration (UF) leads with approximately 32% share as a universally adopted technology for dairy protein concentration, whey processing, and milk standardization in cheese and functional dairy ingredient manufacturing globally.

- Fastest Growing Segment: Nutraceutical manufacturers are fast-growing segment, driven by a high demand for dairy-derived bioactives, lactoferrin, and immunoglobulins that require GMP-certified precision membrane filtration systems meeting pharmaceutical-grade purity specifications.

- Key Market Opportunity: Lactose-free dairy product processing represents a compelling growth opportunity, with nanofiltration systems enabling lactose reduction for a consumer category growing at over 12% annually as global lactose intolerance awareness rises, and pharmaceutical-grade dairy ingredient manufacturing driving premium filtration investment.

| Key Insights | Details |

|---|---|

| Dairy Filtration Systems Market Size (2026E) | US$ 3.5 Billion |

| Market Value Forecast (2033F) | US$ 5.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.7% |

| Historical Market Growth (2020 - 2025) | 4.4% |

Market Dynamics

Drivers - Surging Global Demand for Whey Protein and High-Value Dairy Ingredients

The global sports nutrition and functional food industries are driving strong and sustained demand for high-purity whey protein concentrates and isolates, which rely heavily on advanced membrane filtration technologies. With the sports nutrition market valued at over US$ 50 billion and growing at more than 8% annually, whey protein has become a premium dairy co-product that requires significant processing investments.

Technologies such as ultrafiltration (UF) and microfiltration (MF) play a critical role in producing whey protein concentrates (WPC 80) and isolates (WPI 90+). Industry data highlights continuous growth in global whey ingredient exports, particularly from major regions such as Europe, the United States, and New Zealand. This rising demand for high-quality dairy ingredients is encouraging processors worldwide to expand or upgrade their membrane filtration capacities, thereby increasing the need for new equipment and replacement systems across the industry.

Stringent Food Safety Regulations and Hygiene Standards Mandating Membrane Processing

Strict food safety regulations across key dairy-producing and consuming regions are making membrane filtration an essential part of dairy processing. In Europe, Regulation (EC) No 853/2004 and related hygiene directives set clear standards for dairy safety, including pathogen reduction requirements that microfiltration systems can effectively meet without damaging product quality.

In the United States, the Food Safety Modernization Act (FSMA) requires dairy processors to implement preventive controls, where advanced filtration systems are often used as critical control points within HACCP plans. These regulatory frameworks are mandatory and leave little room for alternatives, ensuring steady demand for certified filtration systems. As compliance is not optional, dairy processors must continuously invest in reliable filtration technologies, creating a stable and long-term demand base for membrane systems regardless of fluctuations in milk production or pricing cycles.

Restraints - High Capital and Operational Costs of Membrane Filtration Systems

Dairy membrane filtration systems require significant upfront investment, which can range from US$ 500,000 to several million dollars depending on the scale of operations. This high capital requirement is a major barrier, especially for small and medium-sized dairy processors. In addition to initial costs, ongoing operational expenses further increase the financial burden.

These include periodic membrane replacement every 3-5 years, the cost of cleaning chemicals, high energy consumption for pressure-driven processes, and the need for skilled technical maintenance. Together, these factors raise the total cost of ownership and can discourage adoption in cost-sensitive markets. As a result, many smaller dairy cooperatives and processors in developing regions delay or limit investments in advanced filtration systems, which slows overall market growth and reduces penetration in emerging economies where affordability remains a key concern.

Membrane Fouling and Performance Degradation Challenges

Membrane fouling is a common and ongoing challenge in dairy filtration processes, caused by the buildup of proteins, fats, minerals, and microbial residues on membrane surfaces. This issue reduces filtration efficiency by lowering flow rates and increasing energy consumption, while also shortening the lifespan of the membranes. Dairy processing environments are particularly prone to fouling due to the complex composition of milk.

To maintain performance, processors must frequently carry out cleaning-in-place (CIP) cycles, which increase the use of chemicals, water, and downtime. These additional requirements add operational complexity and costs, making the system less attractive for some users. Over time, performance degradation can impact productivity and profitability, leading some processors to hesitate before investing in membrane filtration technology despite its benefits in product quality and yield improvement.

Opportunities - Lactose-Free and Specialized Dairy Product Processing Boom

The rapid growth of lactose-free dairy products is creating strong opportunities for membrane filtration technologies such as nanofiltration (NF) and reverse osmosis (RO). Consumer awareness of lactose intolerance, which affects a large portion of the global adult population, is driving demand for these products. As a result, lactose-free product launches have been increasing steadily, especially in Europe and North America. Nanofiltration systems are particularly valuable because they can remove lactose while retaining important minerals, making the process both efficient and cost-effective.

This technological advantage supports the production of high-quality lactose-free dairy products. As these products become more common in mainstream markets, dairy processors are investing in specialized filtration systems to meet demand. Companies that develop advanced NF solutions tailored for dairy applications have a strong opportunity to gain market share and benefit from this growing segment.

Pharmaceutical and Nutraceutical Grade Dairy Ingredient Manufacturing

The growing overlap between dairy processing and the pharmaceutical and nutraceutical industries is creating a high-value opportunity for advanced filtration systems. Dairy-derived ingredients such as bioactive peptides, immunoglobulins, lactoferrin, and high-grade casein require precise filtration processes that meet strict Good Manufacturing Practice (GMP) standards. As the global nutraceutical market continues to expand rapidly, demand for these specialized dairy ingredients is also increasing.

This trend is encouraging equipment manufacturers to develop filtration systems that meet both dairy and pharmaceutical requirements. Such systems allow producers to achieve higher purity levels and consistent product quality. Companies investing in GMP-certified filtration technologies can access premium markets, secure long-term supply agreements, and achieve higher profit margins. This shift toward high-value applications is positioning advanced dairy filtration as a critical enabler of innovation in both food and health-related industries.

Category-wise Analysis

By Filtration Type Insights

Ultrafiltration (UF) is the leading filtration technology in the dairy industry, accounting for approximately 32% of the total market share. With pore sizes ranging from 0.01 to 0.1 microns, UF systems are highly effective in separating proteins from smaller molecules such as lactose, water, and minerals. This makes them essential for applications like whey protein concentration, milk standardization, and microbial reduction.

UF technology is widely used in producing high-value dairy ingredients such as whey protein concentrates and milk protein concentrates. Its reliability and efficiency have made it a standard component in modern dairy processing plants worldwide. Industry bodies recognize UF as a validated and accepted processing method, further strengthening its market position. As demand for protein-rich dairy products continues to grow, UF systems are expected to remain the backbone of dairy filtration processes across both developed and emerging markets.

By Module Design Insights

Spiral wound modules dominate the dairy filtration market, holding around 45% of the total share due to their efficiency and cost-effectiveness. These modules offer a high membrane surface area within a compact design, allowing for effective filtration without requiring excessive space. Their compatibility with automated cleaning-in-place systems makes them easy to maintain and operate.

Spiral wound modules are commonly used in reverse osmosis and nanofiltration applications, including milk concentration, water recovery, and lactose removal. Their modular design allows processors to scale capacity easily by adding more units as needed. This flexibility makes them suitable for both small and large dairy operations. Additionally, their relatively lower manufacturing cost compared to other designs makes them a preferred choice for processors aiming to balance performance with investment efficiency, reinforcing their strong position in the market.

By Application Insights

Whey protein processing is the largest application segment, contributing approximately 27% of the total market share. Whey, a by-product of cheese production, requires multiple filtration steps to convert it into valuable protein ingredients. These steps include ultrafiltration for concentration, diafiltration for purity, microfiltration for removing fats and bacteria, and nanofiltration or reverse osmosis for lactose management.

This multi-stage process makes whey processing highly dependent on advanced filtration systems. The increasing demand for whey protein in sports nutrition, clinical nutrition, and functional foods has significantly boosted this segment. As global consumption of protein-rich products continues to rise, efficient whey processing has become a key focus for dairy producers. This trend ensures steady demand for advanced filtration systems that can improve yield, enhance quality, and support large-scale production requirements.

By End-User Industry

Dairy processing plants are the largest end-users of filtration systems, accounting for about 52% of the total market share. These facilities are responsible for transforming raw milk into a wide range of products, including cheese, yogurt, milk powders, and whey-based ingredients. As a result, they require extensive filtration infrastructure across various stages of production. Large dairy companies and cooperatives operate multiple processing units, each equipped with advanced filtration systems to ensure efficiency and product quality.

The steady growth in global milk production and the expansion of industrial-scale processing facilities have increased the installed base of filtration systems. This, in turn, drives continuous demand for system upgrades, maintenance, and replacements. The central role of processing plants in the dairy value chain ensures their dominance as the primary consumers of membrane filtration technologies.

Regional Insights

North America Dairy Filtration Systems Market Trends

North America is a well-established and technologically advanced market for dairy filtration systems, led by the United States, one of the world’s largest milk producers. The region benefits from strong demand for high-value dairy ingredients, particularly whey protein used in sports nutrition products. Strict food safety regulations also encourage the use of advanced filtration systems.

Dairy processors in the region have been early adopters of technologies such as ultrafiltration, microfiltration, and reverse osmosis to improve product quality and operational efficiency. Canada also contributes to market growth through investments in specialty dairy products and modernization initiatives supported by industry organizations. Additionally, the presence of leading technology providers in the region supports innovation and the development of next-generation filtration systems, further strengthening North America’s position in the global market.

Europe Dairy Filtration Systems Market Trends

Europe represents the largest and most mature market for dairy filtration systems, supported by a highly developed dairy industry. The region is a major global exporter of dairy products, with strong production volumes across several countries. Leading equipment manufacturers and advanced processing technologies are widely present, making Europe a hub for innovation in dairy filtration.

Countries such as Germany, France, the Netherlands, and Ireland are key contributors, with strong demand for whey processing and specialty dairy ingredients. A unified regulatory framework across the region ensures consistent quality and safety standards, encouraging widespread adoption of certified filtration technologies. The combination of advanced infrastructure, strong export demand, and supportive regulations continues to drive steady growth in the European dairy filtration market.

Asia Pacific Dairy Filtration Systems Market Trends

Asia Pacific is the fastest-growing region in the dairy filtration systems market, driven by rising dairy consumption and increasing investments in processing infrastructure. Countries such as China and India are at the forefront, with large-scale milk production and growing demand for processed dairy products. Government initiatives aimed at improving food quality and modernizing the dairy sector are supporting the adoption of advanced filtration technologies.

While developed markets like Japan and Australia focus on high-value products, emerging economies present significant growth opportunities due to lower current adoption levels. The expansion of regional manufacturing capabilities for membrane components is also helping reduce costs, making filtration systems more accessible. This combination of demand growth, policy support, and improving affordability is driving rapid market expansion across the region.

Competitive Landscape

The global dairy filtration systems market is moderately consolidated, with a few large industrial players dominating the industry. These companies offer complete dairy processing solutions that include advanced membrane filtration technologies. Their strong market position is supported by broad product portfolios, global service networks, and deep industry expertise. Key factors that differentiate competitors include innovation in membrane materials, energy efficiency, system integration, and ease of maintenance through automated cleaning systems.

There is also a growing focus on digital solutions, such as real-time monitoring and process optimization tools. Sustainability is another important trend, with companies developing membranes that reduce chemical use and energy consumption. Additionally, modular system designs are becoming popular as they allow flexible capacity expansion. Strategic acquisitions of smaller technology firms are further strengthening the capabilities of leading players and increasing overall market concentration.

Key Developments:

- February 2025: GEA Group AG launched an enhanced ultrafiltration membrane system for whey protein processing, featuring a new polymeric membrane material delivering 20% higher flux rates and extended service life compared to its predecessor generation.

- October 2024: Alfa Laval AB introduced an integrated cross-flow microfiltration module specifically engineered for cold microfiltration of skim milk, enabling extended shelf-life production with minimal heat treatment and reduced energy consumption versus conventional pasteurization.

- April 2024: Sartorius AG expanded its dairy-pharmaceutical crossover filtration portfolio with GMP-certified hollow fiber ultrafiltration modules targeting lactoferrin and immunoglobulin purification, addressing the fast-growing nutraceutical dairy ingredient manufacturing segment.

Companies Covered in Dairy Filtration Systems Market

- Alfa Laval AB

- GEA Group AG

- SPX FLOW, Inc.

- Tetra Pak International S.A.

- Pall Corporation

- 3M Company

- Veolia Water Technologies

- Pentair plc

- DowDuPont Inc.

- Evoqua Water Technologies LLC

- Graver Technologies, LLC

- Porvair Filtration Group

- Donaldson Company, Inc.

- Parker Hannifin Corporation

- Sartorius AG

- Koch Separation Solutions

- Synder Filtration

- Evonik Industries AG

Frequently Asked Questions

The global Dairy Filtration Systems Market is projected to reach US$ 5.2 Billion by 2033, expanding from US$ 3.5 Billion in 2026 at a CAGR of 5.7% during the 2026-2033 forecast period.

The primary growth drivers are surging global demand for whey protein concentrates and isolates driven by the US$ 50+ billion sports nutrition market, and increasingly mandatory food safety regulations, including FDA FSMA in the U.S. and EU Regulation (EC) No 853/2004, that institutionalize membrane filtration as a critical control point in dairy processing operations.

Ultrafiltration (UF) leads the By Filtration Type category with approximately 32% of total market share. UF is the foundational membrane technology for dairy protein concentration, whey processing, and milk standardization, recognized and endorsed by the International Dairy Federation and Codex Alimentarius Commission as the standard processing method for dairy ingredient production.

Europe is the leading region, underpinned by its status as the world's largest dairy exporter with over 155 million tonnes of annual milk production, a harmonized regulatory framework under EU Regulation (EC) No 853/2004, and the presence of globally dominant equipment manufacturers including Alfa Laval AB, GEA Group AG, and Tetra Pak International S.A.

Key opportunities include the lactose-free dairy segment growing at over 12% annually, requiring nanofiltration systems for selective lactose removal, and the rapidly expanding pharmaceutical and nutraceutical end-use segment requiring GMP-certified filtration for lactoferrin, immunoglobulin, and bioactive peptide purification, which offers significant premium pricing and long-term contract revenue potential.

The key market participants include Alfa Laval AB, GEA Group AG, SPX FLOW Inc., Tetra Pak International S.A., Pall Corporation, 3M Company, Veolia Water Technologies, Pentair plc, DowDuPont Inc. (DuPont Water Solutions), Evoqua Water Technologies LLC, Graver Technologies LLC, Porvair Filtration Group, Donaldson Company Inc., Parker Hannifin Corporation, and Sartorius AG.