- Agrochemicals

- Crop Micronutrient Market

Crop Micronutrient Market Size, Share, and Growth Forecast 2026 - 2033

Crop Micronutrient Market by Nutrient (Zinc, Boron, Iron, Manganese, Copper, Others), Form (Chelated, Non-Chelated), Crop Type (Cereals & Grains, Fruits & Vegetables, Oilseeds & Pulses, Plantation Crops, Others), Regional Analysis, 2026 - 2033

Crop Micronutrient Market Share and Trends Analysis

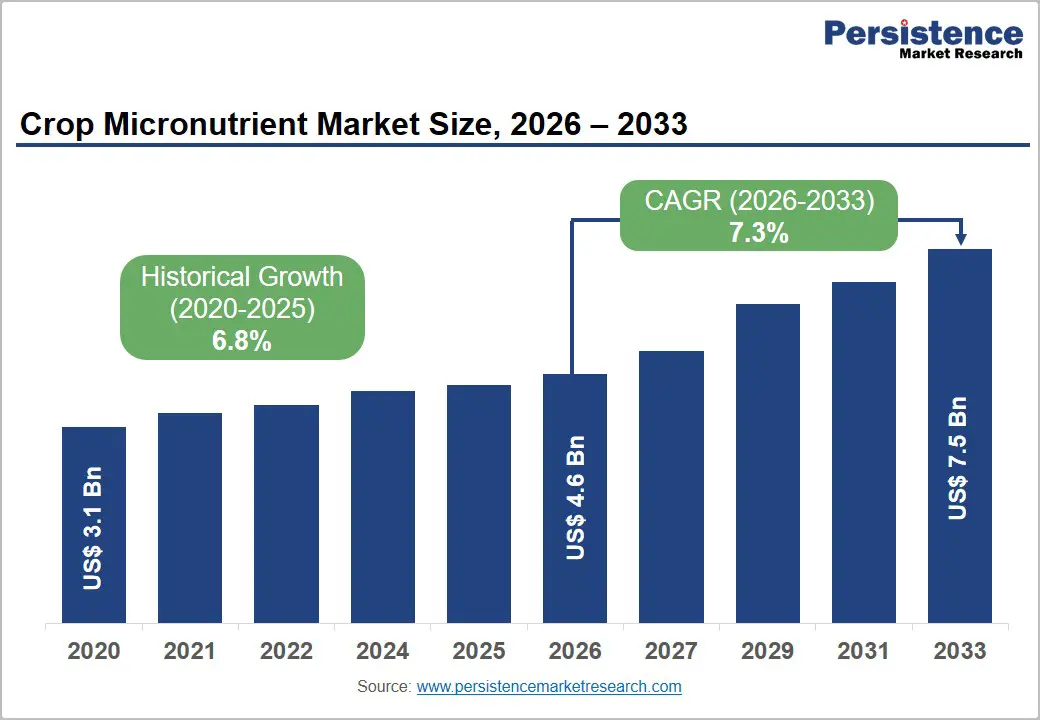

The global crop micronutrient market size is expected to be valued at US$ 4.6 billion in 2026 and is projected to reach US$ 7.5 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033. This growth is driven by the rise in need for global food security, widespread micronutrient deficiency in agricultural soils, and increasing adoption of precision nutrition practices by commercial farmers.

The Food and Agriculture Organization of the United Nations (FAO) estimates that over 50% of the world's agricultural soils are deficient in one or more essential micronutrients, directly undermining crop yields and quality. Intensified crop production cycles, declining soil organic matter, and shrinking arable land are compelling farmers across Asia Pacific, Latin America, and North America to invest systematically in micronutrient supplementation as a yield optimization strategy.

Key Industry Highlights:

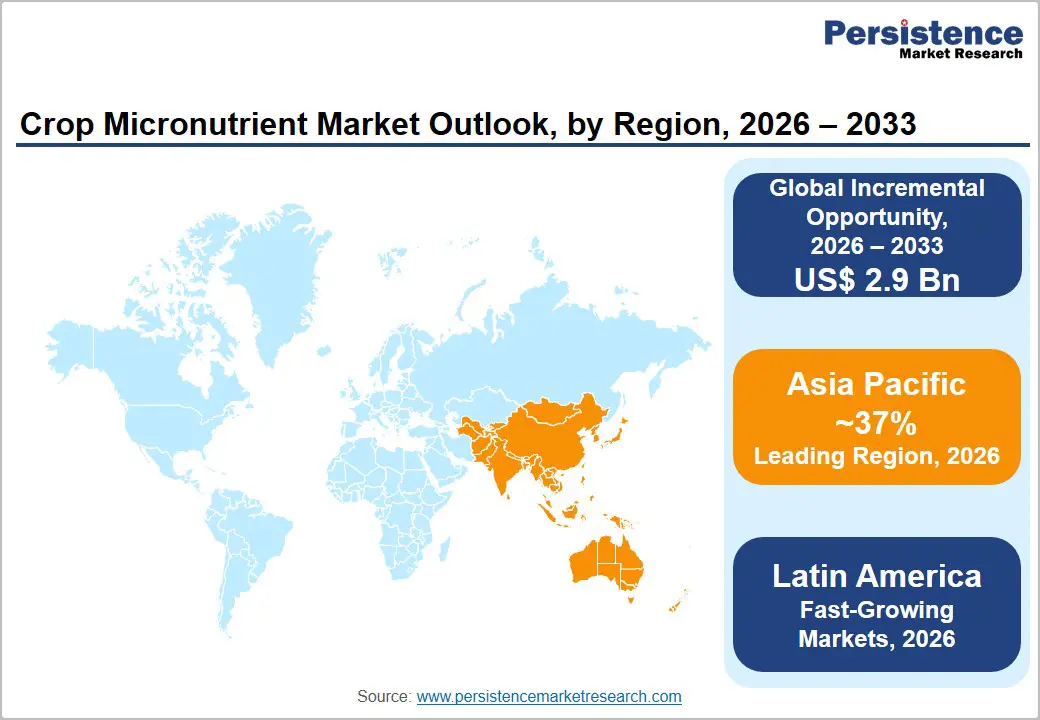

- Leading Region: Asia Pacific is likely to dominate the global crop micronutrient market with a 37% share in 2026, driven by massive agricultural scale in China and India, government-backed soil correction programs, and growing commercial farm intensification.

- Fast-Growing Market: Latin America is the fastest-growing regional market, powered by Brazil and Argentina's expanding high-value commodity agriculture and rising demand for boron, zinc, and manganese in tropical soil systems.

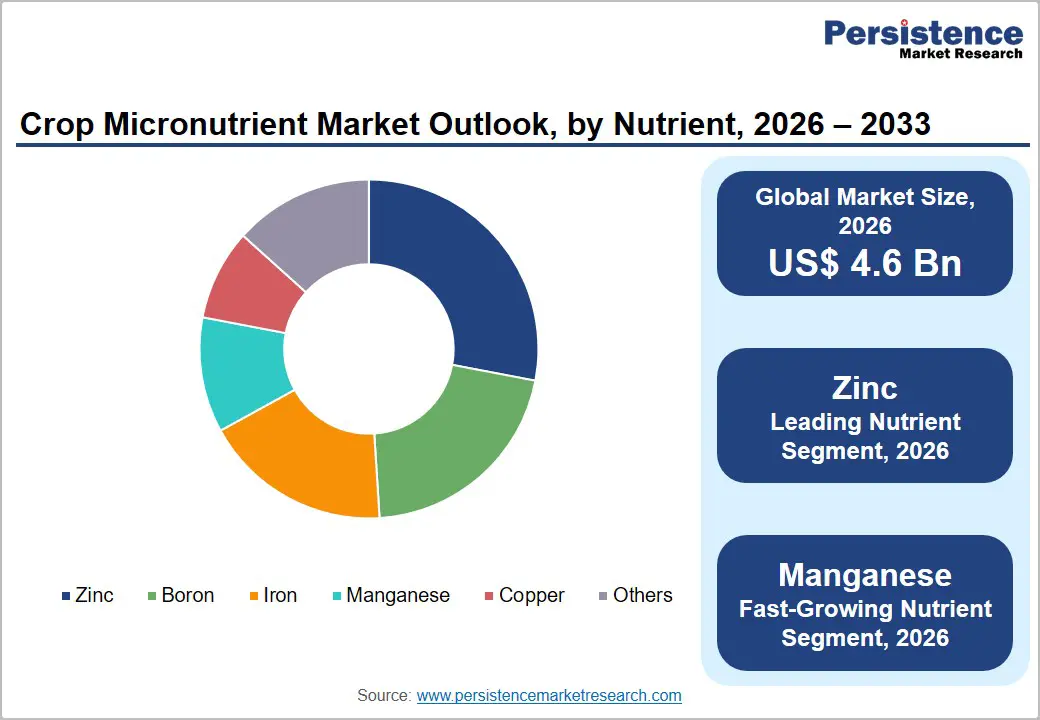

- Dominant Nutrient Segment: Zinc leads the Nutrient category with a 28% share in 2026, driven by its status as the world's most widespread agricultural soil deficiency and institutionalized national supplementation programs across Asia.

- Fastest Growing Nutrient Segment: Manganese is the fast-growing nutrient segment, reflecting growing recognition of its critical role in addressing soil acidification-related deficiencies in intensively farmed cereal and oilseed systems globally.

- Key Opportunity: Biostimulant-micronutrient combination products represent the highest-value growth frontier, aligned with EU Farm to Fork Strategy sustainability mandates and delivering superior crop uptake efficiency versus conventional micronutrient formulations.

Market Dynamics

Drivers – Rise in Soil Micronutrient Depletion and Crop Yield Pressures

Progressive soil degradation and intensive monoculture farming practices have severely depleted micronutrient reserves across global agricultural land, creating a persistent demand for the crop micronutrient market. The International Zinc Association (IZA) identifies zinc deficiency as the most widespread micronutrient deficiency in agricultural soils worldwide, affecting more than 50% of cereal-growing soils globally.

A study published in the journal Nature Plants documented that micronutrient deficiencies collectively reduce global crop yields by an estimated 10–15% annually. Government soil health surveys in India conducted by the Indian Council of Agricultural Research (ICAR) found that over 48% of sampled soils exhibited zinc deficiency, while boron deficiency was noted in 33% of tested areas. As governments and agribusinesses align behind food security goals, systematic micronutrient correction programs have become a policy and commercial priority.

Growing Adoption of Precision Agriculture and Fertigation Technologies

The global transition toward precision agriculture is materially expanding the addressable market for specialty micronutrient formulations, particularly chelated and foliar-applied products that deliver measurable agronomic efficiency gains. Precision agriculture technologies, including soil testing platforms, satellite-guided variable-rate applicators, and digital farm management systems, enable targeted micronutrient application that maximizes return on input investment.

The European Commission's Farm to Fork Strategy targets a 20% reduction in fertilizer use while maintaining productivity, creating strong commercial incentives for high-efficiency chelated micronutrient products. Furthermore, the FAO estimates that global irrigated agriculture, the primary channel for fertigation-based micronutrient delivery, covers over 300 million hectares and accounts for more than 40% of global food production, providing a large and growing platform for advanced micronutrient application technologies.

Restraints - Lack of Farmer Awareness and Access in Developing Economies

Despite compelling agronomic evidence supporting micronutrient supplementation, limited awareness among smallholder farmers who collectively manage over 84% of the world's farms, according to the FAO remains a significant barrier to market penetration in key growth regions, including Sub-Saharan Africa, South Asia, and parts of Southeast Asia. Inadequate agricultural extension services, fragmented distribution networks, and low technology adoption impede market-building efforts for specialty micronutrient products. Price sensitivity among smallholder farmers’ further compounds adoption challenges, limiting the addressable market for premium formulations.

Regulatory Heterogeneity Across Key Agricultural Markets

The crop micronutrient market operates within a complex and inconsistent global regulatory environment, in which permitted micronutrient sources, maximum application rates, and labeling requirements vary substantially across jurisdictions. In the European Union, the EU Fertilising Products Regulation (EU) 2019/1009 has introduced significant reformulation requirements for manufacturers seeking CE marking for micronutrient fertilizers. Compliance costs, lengthy registration processes for new chelated formulations, and the risk of regulatory divergence between major export markets, including the U.S., EU, India, and Brazil, collectively suppress innovation velocity and increase market entry barriers for regional manufacturers.

Opportunities - Biostimulant-Micronutrient Combination Products as Next-Generation Crop Nutrition Solutions

The convergence of micronutrient technology with the fast-growing biostimulants sector presents a significant growth opportunity for manufacturers capable of developing synergistic combination products. Biostimulants, including humic acids, amino acids, and seaweed extracts, enhance the efficiency of micronutrient uptake at the root zone, enabling lower application rates and superior crop response.

The European Biostimulants Industry Council (EBIC) projects that the global biostimulants market will continue to expand at double-digit annual rates, driven by the EU Farm to Fork Strategy and growing organic farming adoption. Companies such as Valagro and UPL Limited are already investing in biostimulant-micronutrient product lines. Regulatory harmonization under EU Regulation 2019/1009 has further facilitated market entry for such combination products in Europe, providing a regulatory pathway that creates first-mover advantages for innovators in this space.

Latin America's Expanding High-Value Agriculture as a Fast-Growth Market Frontier

Latin America represents the fastest-growing regional market for crop micronutrients, powered by rapid expansion of high-value agricultural commodity production in Brazil, Argentina, and Colombia. Brazil alone is the world's largest exporter of soybeans, sugar, and coffee crops with documented and well-established micronutrient requirements for yield optimization.

The Brazilian Agricultural Research Corporation (EMBRAPA) has published extensive research linking boron, zinc, and manganese supplementation with yield improvements of 15–30% in tropical soil conditions. As Brazilian and Argentine farmers intensify production on the Cerrado and Pampas regions, demand for both foliar and soil-applied micronutrient products is accelerating. The region's growing network of agricultural cooperatives and digital agronomy platforms is also improving distribution reach and farmer education, systematically reducing the awareness and access barriers that historically constrained market growth.

Category-wise Analysis

Nutrient Insights

Zinc leads the global crop micronutrient market by nutrient type, accounting for approximately 28% of total market revenue in 2026. Zinc's dominance is rooted in the exceptional breadth and severity of its deficiency across global agricultural soils, a challenge comprehensively documented by the International Zinc Association (IZA), which identifies zinc deficiency as the most prevalent micronutrient limitation for crop production globally.

Zinc plays essential physiological roles in enzyme activation, protein synthesis, chlorophyll formation, and pollen viability, making its supplementation agronomically critical across all major crop systems. National zinc biofortification programs in India, Pakistan, and Bangladesh, supported by the HarvestPlus initiative, have further institutionalized zinc application as a standard agronomic practice. Manganese is the fastest-growing nutrient segment, driven by increasing recognition of its role in combating soil acidification-related deficiencies in high-intensity farming systems.

Form Insights

The chelated form segment leads the crop micronutrient market, capturing approximately 56% of the total market share in 2025. Chelated micronutrients, in which metal ions are bonded to organic ligands such as EDTA, EDDHA, DTPA, or amino acids, deliver substantially superior agronomic performance compared to inorganic salt forms under challenging soil conditions, including high pH, excessive moisture, and competitive ion environments.

Research published in the Journal of Plant Nutrition and Soil Science consistently demonstrates that chelated zinc and iron formulations achieve 40–70% higher plant uptake efficiency versus equivalent inorganic sulfate applications. The premium efficacy profile of chelates justifies their higher price point for commercial and high-value crop growers. The non-chelated segment retains a significant share in price-sensitive markets and where soil conditions are less restrictive.

Crop Type Insights

Cereals & grains represent the leading crop type segment in the global crop micronutrient market, accounting for approximately 38% of the total share in 2026. This dominance reflects the enormous global cultivation area dedicated to wheat, rice, maize, and barley, collectively representing over 700 million hectares of harvested area annually according to FAO STAT data. Micronutrient deficiencies, particularly zinc in rice and wheat, and manganese in barley, are extensively documented across Asian, South Asian, and Eastern European cereal belts, creating a large and consistent demand base.

Government programs in India, China, and Pakistan subsidize or mandate zinc application for rice and wheat cultivation as part of national food security strategies. Fruits & Vegetables is emerging as the fast-growing crop type segment, driven by expanding protected cultivation and the premium micronutrient requirements of high-value horticulture.

Regional Insights

North America Crop Micronutrient Market Trends and Insights

North America is a mature and technologically advanced market for crop micronutrients, characterized by high adoption of precision agriculture, fertigation, and soil health monitoring systems. U.S. EPA and USDA sustainability programs are driving demand for efficient, reduced-waste micronutrient formulations aligned with regenerative agriculture principles. Chelated products and foliar sprays dominate commercial adoption.

U.S. Crop Micronutrient Market Size

The United States accounts for approximately 78% of the North American crop micronutrient market, underpinned by large-scale commercial corn, soybean, and wheat cultivation. USDA data confirms widespread zinc and boron deficiencies across Midwest and Great Plains soils, sustaining consistent demand for specialty micronutrient products across both broadacre and high-value horticulture sectors.

Europe Crop Micronutrient Market Trends and Insights

Europe's crop micronutrient market is shaped by the EU Fertilising Products Regulation 2019/1009, which has harmonized product standards while incentivizing innovation in chelated and organic-certified micronutrient formulations. Sustainable farming mandates under the Farm to Fork Strategy are accelerating demand for high-efficiency, low-application-rate micronutrient products across Germany, France, and the U.K.

Germany Crop Micronutrient Market Size

Germany is likely to register approximately 22% of the European crop micronutrient market. Its intensive agricultural sector, centered on cereals, sugar beet, and oilseeds, drives consistent demand for boron and manganese supplements. German Farmers' Association (DBV) data reflects strong farmer investment in soil diagnostics and precision nutrient management, supporting premium chelated product adoption across the country.

U.K. Crop Micronutrient Market Size

The United Kingdom accounts for approximately 14% of the European crop micronutrient market. Post-Brexit regulatory alignment with legacy EU standards and AHDB (Agriculture and Horticulture Development Board) soil health programs sustain demand for zinc, manganese, and copper supplements across the U.K.'s cereal and oilseed-dominated agricultural landscape.

France Crop Micronutrient Market Size

France represents approximately 18% of the European market revenue. As Europe's largest agricultural producer by area, France's diverse crop portfolio spanning cereals, vineyards, sugar beet, and horticulture creates broad micronutrient demand across multiple segments. INRAE (Institut National de Recherche pour l'Agriculture) research programs underpin evidence-based micronutrient application recommendations adopted by French agronomy advisory services.

Asia Pacific Crop Micronutrient Market Trends and Insights

Asia Pacific is the dominant region in the global crop micronutrient market with 37% of global market share in 2025, driven by the massive agricultural scale of China, India, and Southeast Asia. China's government-backed Soil Testing and Fertilizer Recommendation program covering over 200 million farmers has systematically driven zinc and boron adoption across rice and wheat systems, making it one of the world's largest national micronutrient programs.

India Crop Micronutrient Market Size

India is likely to account for approximately 28% of the Asia Pacific crop micronutrient market. With over 140 million hectares of net sown area and documented zinc deficiency in nearly half of tested soils per ICAR surveys, India represents one of the highest-growth national markets. Government subsidy schemes for zinc sulfate application under the National Food Security Mission further structurally support demand.

Competitive Landscape

The crop micronutrient market is highly competitive, driven by continuous product innovation, expanding agricultural input portfolios, and increasing focus on improving crop productivity and soil health. Market participants compete through advanced formulations such as chelated and specialty micronutrients to enhance nutrient absorption and crop yield. Companies are strengthening distribution networks, investing in research and development, and expanding manufacturing capacities to meet rising demand from precision farming and sustainable agriculture.

Key Developments:

- In April 2026, BASF and Nutrien announced a strategic collaboration to expand farmer access to low-carbon biofuel markets. The partnership integrated BASF’s digital farming platforms, including xarvio FIELD MANAGER and xarvio BIOENERGY, with Nutrien’s agronomic expertise to help growers measure and document crop carbon intensity.

- In July 2024, Syngenta and Intrinsyx Bio entered into a strategic partnership to develop and commercialize biological solutions aimed at improving crop nutrient use efficiency. The collaboration focused on utilizing proprietary endophyte formulations that enhance nitrogen fixation and increase the uptake of phosphorus and micronutrients in crops.

Companies Covered in Crop Micronutrient Market

- BASF SE

- Yara International

- Nutrien Ltd.

- The Mosaic Company

- ICL Group

- Coromandel International

- UPL Limited

- Koch Agronomic Services

- Nufarm Limited

- Haifa Group

- Akzo Nobel N.V.

- Aries Agro Limited

- Valagro

Frequently Asked Questions

The global crop micronutrient market is projected to be valued at US$ 4.6 billion in 2026.

The leading demand drivers include widespread and escalating soil micronutrient deficiencies with the FAO estimating over 50% of agricultural soils deficient in one or more essential micronutrients, combined with intensifying pressure to maximize crop yields on shrinking arable land. Government-backed soil correction programs in India, China, and Brazil, as well as the EU Farm to Fork Strategy's mandate for precision, high-efficiency fertilization, are further structurally reinforcing micronutrient demand across all major agricultural markets.

Asia Pacific is the leading region, holding approximately 37% of global crop micronutrient market share in 2025.

A significant growth opportunity lies in biostimulant-micronutrient combination products that enhance uptake efficiency and align with EU Farm to Fork sustainability mandates, offering premium agronomic performance with lower application rates. Additionally, Latin America's rapidly expanding high-value commodity agriculture particularly in Brazil and Argentina represents a high-growth market frontier, with EMBRAPA research documenting yield improvements of 15–30% from micronutrient supplementation in tropical soil systems.

The global crop micronutrient market is served by leading multinational agrochemical and specialty fertilizer companies, including BASF SE, Yara International, Nutrien Ltd., The Mosaic Company, and ICL Group. Strong regional players include Coromandel International, UPL Limited, Aries Agro Limited, and Valagro, alongside specialists such as Haifa Group, Koch Agronomic Services, and Nufarm Limited.