- Metals & Minerals

- Copper Strips Market

Copper Strips Market Size, Share, and Growth Forecast 2026 - 2033

Copper Strips Market by Strip Thickness (Below 6mm, 6-10mm, Above 10mm), Application (Electric Appliances, Industrial Machines, Construction, Others), and Regional Analysis for 2026 - 2033

Copper Strips Market Size and Trend Analysis

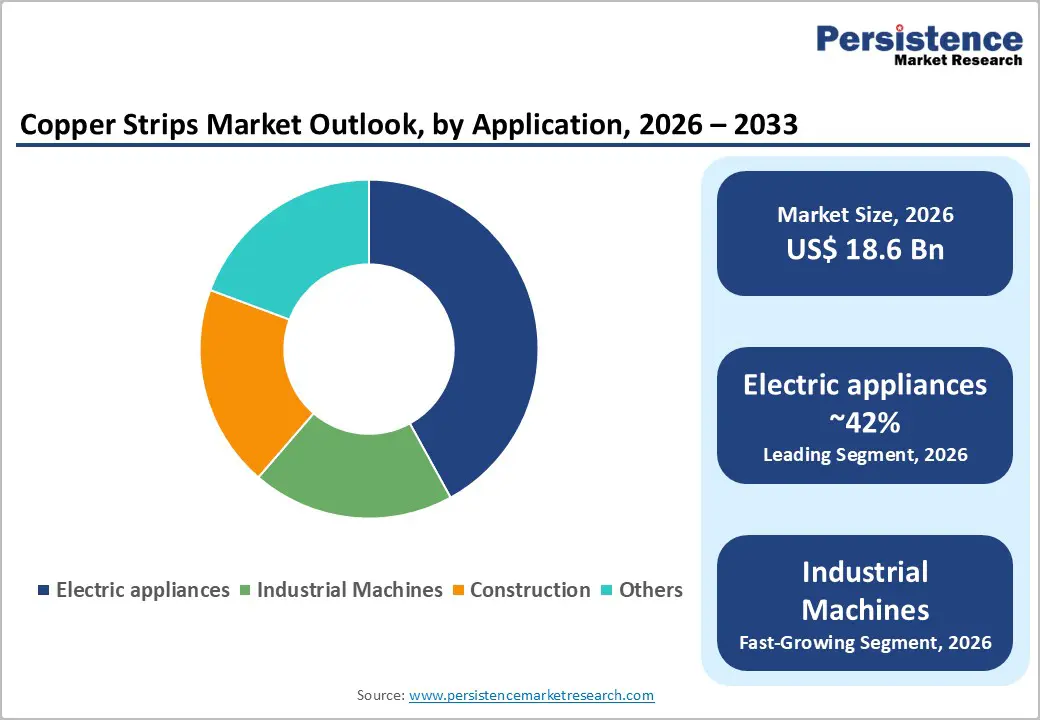

The global copper strips market is valued at US$ 18.6 billion in 2026 and is projected to reach US$ 24.3 billion by 2033, growing at a CAGR of 3.9% between 2026 and 2033.

This growth is underpinned by a convergence of powerful structural forces reshaping global industrial demand. Copper strips, owing to their unmatched electrical and thermal conductivity, are indispensable across electric vehicle (EV) battery systems, renewable energy infrastructure, smart grid networks, and precision electronics manufacturing.

The accelerating global energy transition, backed by policy mandates such as the European Green Deal and the U.S. Inflation Reduction Act, is catalyzing sustained investment in power transmission and clean energy technologies, both of which rely heavily on high-conductivity copper strips. Simultaneously, rapid urbanization across the Asia Pacific and expanding smart city initiatives are broadening the addressable market for copper strips in construction and infrastructure applications.

Key Industry Highlights:

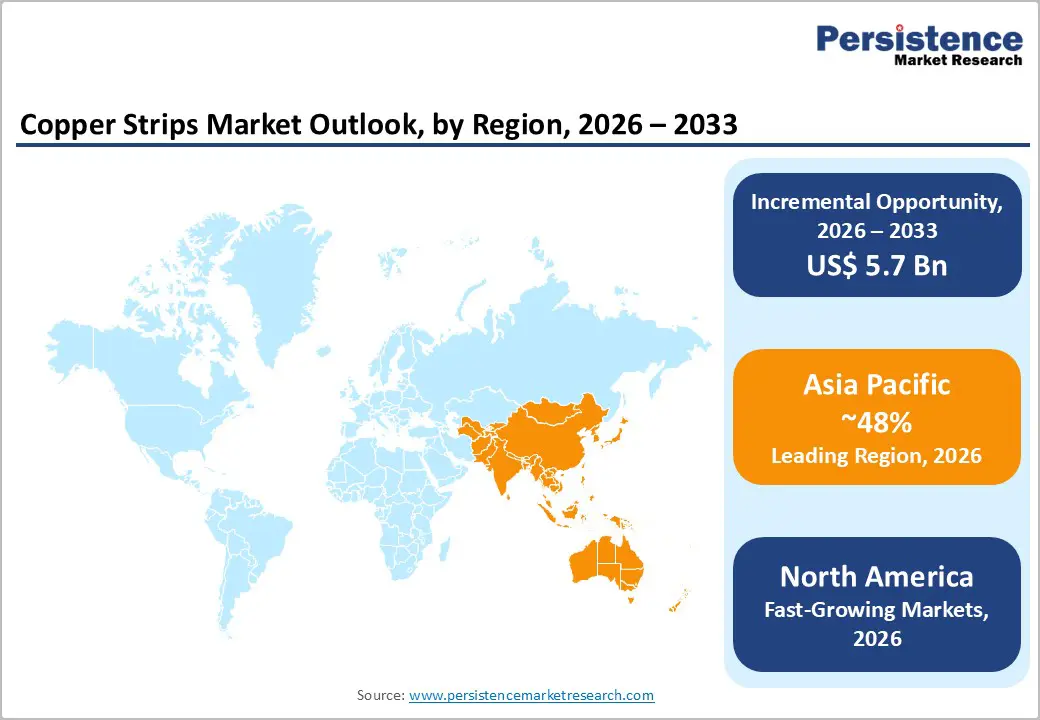

- Leading Region: Asia Pacific dominates the global Copper Strips market, commanding approximately 48% share, driven by China's unparalleled electronics manufacturing base, large-scale renewable energy installations, and robust EV production ecosystem.

- Fastest Growing Region: North America is the fastest-growing region, supported by the developed electrification ecosystem of the United States.

- Dominant Segment: The Below 6mm copper strip segment leads by thickness with 56% share, underpinned by extensive demand from PCBs, connectors, transformers, and precision electronic components across the global electronics industry.

- Fastest Growing Segment: The Electric Appliances application segment is the fastest growing, propelled by rising global electricity demand, energy transition infrastructure build-out, and expanding household electrification, especially across emerging economies in Asia and Africa.

- Key Market Opportunity: The rapid global expansion of EV manufacturing and AI data centres presents a high-value opportunity, with Wood Mackenzie projecting EV-related copper demand to grow at 10% annually through 2035, creating sustained volume demand for precision copper strips.

| Key Insights | Details |

|---|---|

| Copper Strips Market Size (2026E) | US$ 18.6 Bn |

| Market Value Forecast (2033F) | US$ 24.3 Bn |

| Projected Growth CAGR (2026 - 2033) | 3.9% |

| Historical Market Growth (2020 - 2025) | 3.5% |

DRO Analysis

Drivers - Electrification of Transportation and Renewable Energy Expansion

The global energy transition is among the most consequential drivers of copper strip demand. The electric vehicles (EVs) require approximately 2.9 times more copper than conventional internal combustion engine vehicles, with copper strips serving as the primary conductive material in battery packs, busbars, and charging infrastructure. Global EV sales surpassed 17 million units annually as of 2024, a trajectory that directly amplifies copper strip consumption.

Furthermore, the International Energy Agency (IEA) notes that renewable energy infrastructure, spanning solar photovoltaic panels, wind turbines, and battery storage systems, requires 2.5 to 7 times more copper than fossil fuel-based technologies. With over 412 GW of new renewable capacity added globally in 2023-2024, demand for copper strip-based busbars, connectors, and grounding systems is accelerating, creating a durable, long-term growth catalyst for the global Copper Strips market.

Expansion of Smart Grid Infrastructure and Power Transmission Networks

Governments worldwide are making unprecedented investments in grid modernization and smart power transmission infrastructure, driving robust demand for copper strips. According to S&P Global, a cumulative US$ 7.5 trillion investments is required in transmission and distribution lines between now and 2040 to meet growing electricity demand. Copper strips are integral to transformer windings, switchgear, busbars, and distribution panels that form the backbone of these networks.

Copper constitutes approximately 66% of total cable weight in underground distribution cables, a segment gaining share as urban infrastructure upgrades accelerate. In developing economies across Asia Pacific, Africa, and Latin America, new grid connectivity programmes backed by multilateral development banks, including the World Bank and Asian Development Bank (ADB), are expanding the reach of electrification projects that rely on precision copper strip components.

Restraints - Copper Price Volatility and Raw Material Supply Uncertainty

Copper strips are manufactured from refined copper cathodes, rendering the market highly sensitive to fluctuations in global copper commodity prices. Volatility in London Metal Exchange (LME) copper prices, which has exceeded 21% on a year-on-year basis in recent periods, has materially disrupted cost forecasting, procurement planning, and margin stability for downstream copper strip manufacturers and end users.

These challenges are further compounded by supply-side risks, including labour strikes and operational disruptions in major copper-producing countries such as Chile and Peru, which collectively account for more than 40% of global mined copper output. Such uncertainties constrain investment visibility, exert sustained pressure on operating margins, and limit capacity expansion across the copper strips value chain.

Competitive Threat from Aluminum Substitution

Is aluminum increasingly being considered as a cost-effective alternative to copper in selected applications, particularly power cable conductors, automotive wiring harnesses, and heat exchangers. Owing to its significantly lower density and substantially lower cost per kilogram compared with copper, aluminum is attracting interest from cost-sensitive manufacturers across the automotive and construction sectors.

Research published in Resources Policy (2025) identifies aluminum as a key substitute influencing long-term copper demand dynamics. Although copper continues to dominate high-performance applications due to its superior electrical conductivity and lower resistivity, the growing adoption of aluminum in commodity-grade applications represents a structural constraint on volume growth within the global copper strips market.

Opportunities - Rapid Growth of Electric Vehicle Manufacturing and EV Charging Infrastructure

The accelerating adoption of electric vehicles (EVs) constitutes a significant and rapidly expanding demand driver for copper strip manufacturers. According to Wood Mackenzie, copper consumption linked to EV applications is projected to more than double by 2035, increasing from approximately 1.7 million metric tons per annum to 4.3 million metric tons, reflecting an annual growth rate of nearly 10%. Copper strips play a critical role across key EV components, including battery cell interconnects, power electronics thermal management systems, busbars, and charging infrastructure.

As EV penetration continues to rise across North America, Europe, and the Asia Pacific region, demand for high-performance copper strips is expected to intensify. Manufacturers that invest in advanced rolling technologies, thinner-gauge production, and high-conductivity alloy development will be strategically positioned to capture value from this high-growth, premium market segment, particularly in battery electric vehicles (BEVs) and grid-connected fast-charging applications.

Emergence of AI Data Centers and 5G Network Infrastructure

The rapid expansion of artificial intelligence (AI) data centers and fifth-generation (5G) telecommunications networks is emerging as a significant high-growth end-use segment for high-conductivity copper strips. Modern data centres require substantial volumes of copper strip-based busbars to support power distribution, server rack interconnections, and efficient thermal management systems. In its 2025 strategic outlook, Aurubis AG identified AI infrastructure and data centers as a key growth area for copper demand in North America.

Furthermore, the International Copper Association notes that 5G base stations consume significantly more copper than legacy 4G infrastructure. As global hyperscaler investments in AI capabilities and cloud computing continue to accelerate, copper strip manufacturers are well-positioned to develop application-specific products featuring enhanced thermal performance, dimensional precision, and reliability tailored to data center and telecommunications applications.

Category-wise Analysis

Strip Thickness Insights

The Below 6mm segment dominates the global Copper Strips market by strip thickness, accounting for approximately 56% of the total market share. This dominance is attributable to the segment's extensive applicability across the electronics and electrical industries, where miniaturization and precision are paramount. Thin copper strips below 6mm are the material of choice for printed circuit boards (PCBs), connectors, terminals, lead frames, and transformer windings, applications that collectively constitute the largest volume demand base for the Copper Strips market.

According to the International Copper Association (ICA), over 61% of global copper strip demand is attributable to high-conductivity applications where dimensional precision is critical. Manufacturers such as Mitsubishi Materials Corporation and Furukawa Electric Co., Ltd. have invested significantly in rolling mill technologies capable of producing ultra-thin strips below 0.05mm for flexible electronics and wearable devices, further entrenching the segment's leading position.

Application Insights

The Electric Appliances segment leads the global copper strips market by application, commanding an estimated 42% share of total demand. Copper strips are foundational components in the manufacture of transformers, motors, heat exchangers, switchgear, and household electrical appliances, all of which are experiencing robust global demand growth. Rising electricity consumption, expanding residential and commercial construction, and widespread household appliance penetration across the Asia Pacific and Africa are key tailwinds.

The International Energy Agency (IEA) projects global electricity demand will grow by 86% by 2050, necessitating massive expansion in appliance and transformer production. Industrial Machines constitute the second-largest application segment, with approximately a 29% share, driven by demand for CNC machinery, robotics, industrial motors, and automated manufacturing lines, sectors that are growing rapidly in tandem with global manufacturing reshoring and Industry 4.0 adoption.

Regional Insights

North America Copper Strips Market Trends

North America constitutes a strategically important market for copper strips, supported by the highly developed electrification ecosystem of the United States. The U.S. consumes approximately 2 million metric tons of copper annually while importing nearly half of its total requirements, underscoring structural supply dependencies. More than 120 GW of renewable energy capacity installed annually in the United States continues to generate consistent demand for copper busbars and conductive strips.

Heightened geopolitical uncertainty, including escalating U.S.-Iran tensions, has reinforced policy emphasis on domestic supply-chain resilience for critical minerals. The U.S. Department of Energy has designated copper as a critical material for the energy transition, prompting capacity expansions such as Aurubis AG’s Richmond recycling facility and Wieland Group’s USD 500 million rolling mill investment in Illinois.

Europe Copper Strips Market Trends

Europe represents a mature and technologically advanced market for copper strips, with demand driven by the region’s strong automotive manufacturing base, precision engineering capabilities, and ambitious decarbonization agenda. Germany leads regional consumption, supported by its export-oriented automotive and industrial machinery industries. The European Green Deal, which mandates climate neutrality by 2050, necessitates substantial investment in renewable energy and grid modernization, both of which are highly copper-intensive.

Ongoing geopolitical uncertainties, including U.S.-Iran tensions, have accelerated energy security initiatives and reduced reliance on fossil fuels, further stimulating investment in renewable and nuclear power infrastructure. Rapid expansion of solar and offshore wind capacity in France and Spain, alongside regulatory measures such as the EU Critical Raw Materials Act, is strengthening domestic recycling and supporting capacity investments by leading producers.

Asia Pacific Copper Strips Trends

Asia Pacific remains the dominant region in the global copper strips market, accounting for approximately 48% of total demand, underpinned by the region’s extensive electronics manufacturing base, accelerating electric vehicle adoption, and large-scale industrialization. China is the world’s largest consumer of refined copper, representing over half of global consumption, with domestic solar and wind installations driving substantial demand for copper strip-based components.

Japan continues to lead in high-precision copper strip manufacturing, supported by technologically advanced producers such as Mitsubishi Materials Corporation and Furukawa Electric Co., Ltd. India is the fastest-growing market within the region, benefiting from national initiatives including PM Gati Shakti and the National Solar Mission. Additionally, emerging electronics manufacturing hubs across ASEAN, particularly Vietnam and Indonesia, are generating incremental demand, while capacity expansions by Hindalco Industries Ltd. and Jiangxi Copper Co., Ltd. are positioning suppliers to capitalize on sustained regional growth.

Competitive Landscape

The global copper strips market exhibits a moderately consolidated competitive structure, with the top ten producers accounting for approximately 60-70% of global production. Key market leaders such as Aurubis AG, Wieland Group, and KME Group SpA differentiate on precision manufacturing capability, alloy development expertise, and sustainability credentials. Strategic consolidation through mergers and acquisitions is reshaping competitive boundaries. Emerging business model trends include circular economy-aligned production using recycled copper feedstock, vertical integration across the copper value chain, and product co-development partnerships with tier-1 automotive and electronics OEMs. Companies investing in Industry 4.0-enabled rolling mills for ultra-thin gauge production hold a notable competitive advantage as electronics miniaturization accelerates.

Key Market Developments

- January 2026: Wieland officially broke ground at its Montpelier facility, Wieland Chase, the largest brass rod manufacturing company in North America, to build a new $27 million plant dedicated to expanding semi-finished brass and copper production exclusively in the U.S.

- January 2026: Hudbay Minerals Inc. announced the closing of the strategic investment from Mitsubishi Corporation for a 30% joint venture interest in Copper World LLC, which owns the fully-permitted Copper World project in Arizona. Mitsubishi contributed approximately $420 million of cash to Copper World LLC, and it will contribute an additional $180 million in cash to complete its initial investment within 18 months in accordance with the terms of the definitive subscription agreement.

- December 2025: Zhejiang Hailiang Co., Ltd. announced that its subsidiary, Gansu Hailiang New Energy Materials Co., Ltd., plans to invest approximately USD 732 million to establish a 67,500 tpa electrolytic copper foil production facility in Zhuji. The project will be executed in three phases over 60 months through a newly formed entity, Zhejiang Hailiang New Energy Materials Co., Ltd. Phase-wise capacities include 17,500 tons (Phase I), 32,500 tons (Phase II), and 17,500 tons (Phase III), with construction of Phase I expected to begin in July 2026.

Top Companies in the Copper Strips Market

- Aurubis AG (Hamburg, Germany) is one of the world's leading non-ferrous metals companies and the largest copper recycler globally, with operations spanning Europe and North America. With a strategic focus on sustainable copper production, multimetal recycling, and smelter network efficiency, Aurubis serves the electronics, automotive, and energy infrastructure industries with a broad portfolio of copper and alloy products.

- Wieland Group (Ulm, Germany) is a globally recognized manufacturer of semi-finished copper and copper alloy products with a strong presence across Europe and North America. Following the acquisition of Aurubis's Buffalo plant in August 2024 and the USD 500 million expansion at its East Alton facility, Wieland has significantly reinforced its position as a leading copper strip supplier for the EV, renewables, and precision electronics markets globally.

- KME Group S.p.A. (Florence, Italy) is a major European copper and copper alloy manufacturer operating production facilities across Germany, France, Italy, and the United States, with annual production capacity approaching 200,000 metric tons. Following its 2022 acquisition of Aurubis' European flat-rolled product sites, KME has emerged as a dominant supplier of precision copper strips for the electrical, electronics, and automotive industries. In February 2024, KME listed its Cunova business unit on the New York Stock Exchange (NYSE) to enhance investment appeal.

Companies Covered in Copper Strips Market

- Aurubis AG

- Wieland Group

- KME Group SpA

- Mitsubishi Materials Corporation

- Poongsan Corporation

- Jiangxi Copper Co., Ltd.

- Furukawa Electric Co., Ltd.

- Hailiang Group

- Hindalco Industries Ltd.

- Chalco

- Dowa Metaltech

- Ningbo Jintian Copper (Group) Co., Ltd.

Frequently Asked Questions

The global Copper Strips market is valued at US$ 18.6 Bn in 2026 and is projected to reach US$ 24.3 Bn by 2033, growing at a CAGR of 3.9% over the forecast period.

The primary demand drivers include the accelerating global electrification of transportation (EVs requiring 2.9x more copper than conventional vehicles), the rapid expansion of renewable energy infrastructure requiring copper-intensive busbars and connectors, and growing investment in smart grid and power transmission networks projected to require US$ 7.5 trillion globally through 2040.

The Below 6mm strip thickness segment is the dominant category, accounting for approximately 56% of global market share. This segment leads due to its extensive use in precision electronic applications, including printed circuit boards, connectors, terminals, and transformer windings, where dimensional accuracy and high conductivity are critical requirements.

Asia Pacific leads the global Copper Strips market with an estimated 48% share, driven by China's position as the world's largest copper consumer, Japan's precision strip manufacturing capabilities, and India's rapidly growing status as the fastest-growing country market, supported by national infrastructure and renewable energy programmes.

Key opportunities include the rapid expansion of EV manufacturing (Wood Mackenzie projects EV-related copper demand to reach 4.3 Mtpa by 2035), the deployment of AI data centres requiring copper busbars for power distribution, and the global 5G network rollout demanding high-conductivity copper strip components across base station infrastructure.

The leading companies include Aurubis AG, Wieland Group, KME Group SpA, Mitsubishi Materials Corporation, Poongsan Corporation, Jiangxi Copper Co., Ltd., Furukawa Electric Co., Ltd., Hailiang Group, Hindalco Industries Ltd., and Ningbo Jintian Copper (Group) Co., Ltd., among others.