- Technology

- Biometric Vehicle Access Market

Biometric Vehicle Access Market Size, Share, and Growth Forecast 2026 - 2033

Biometric Vehicle Access Market by Component (Hardware, Software, Services), by Vehicle Type (Passenger Vehicles, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Electric Vehicles), by Authentication Type (Fingerprint, Facial, Voice, Iris, Others), Sales Channel (OEM, Aftermarket), and Regional Analysis, 2026 - 2033

Biometric Vehicle Access Market Size and Trend Analysis

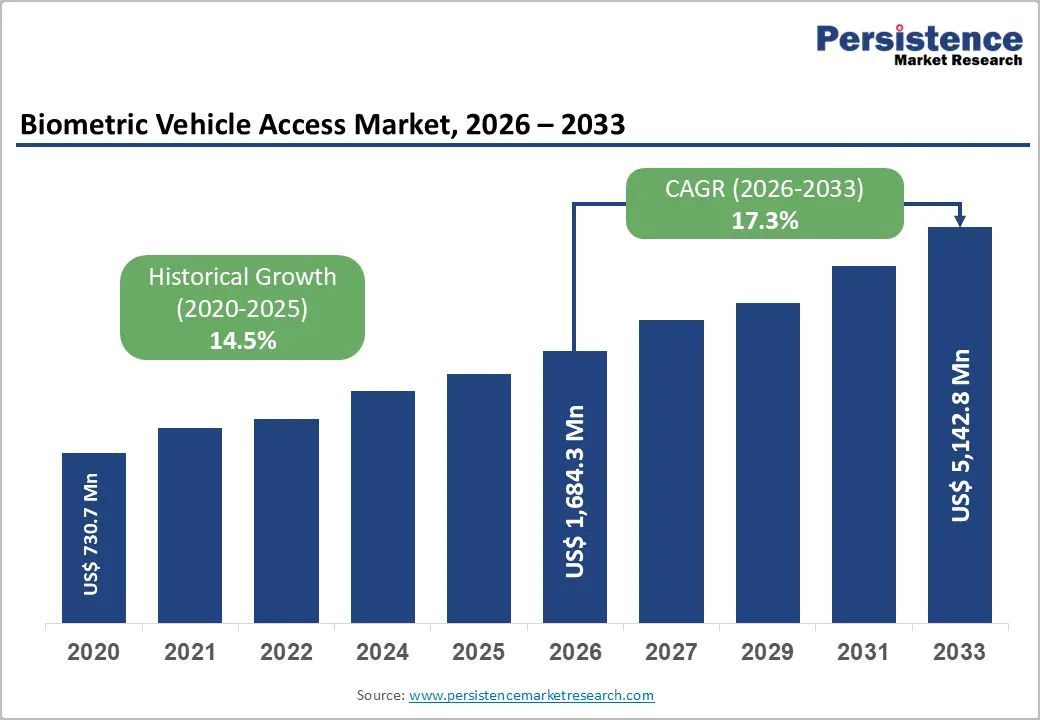

The global Biometric Vehicle Access Market size is expected to be valued at US$ 1,684.3 Million in 2026 and projected to reach US$ 5,142.8 Million by 2033, growing at a CAGR of 17.3% between 2026 and 2033.

The market is experiencing strong growth driven by the increasing integration of advanced driver authentication technologies in next-generation vehicles, particularly electric and connected cars. Rising vehicle theft concerns, growing demand for seamless user experience, and increasing adoption of smart mobility ecosystems are accelerating the deployment of biometric authentication systems. The convergence of falling sensor costs, maturation of AI-driven multi-modal authentication, and regulatory emphasis on vehicular cybersecurity underpins the market's robust expansion.

Key Industry Highlights:

- Leading Component: Hardware dominates the market with over 62% share in 2026, valued at more than US$ 1,044.3 Mn, driven by the essential role of biometric sensors, scanners, and in-vehicle authentication modules enabling secure access and real-time identity verification.

- Leading Vehicle Type: Electric Vehicles (EVs) are the fastest-growing segment, driven by their software-defined architecture, higher integration of connected technologies, and alignment with advanced biometric-enabled access systems.

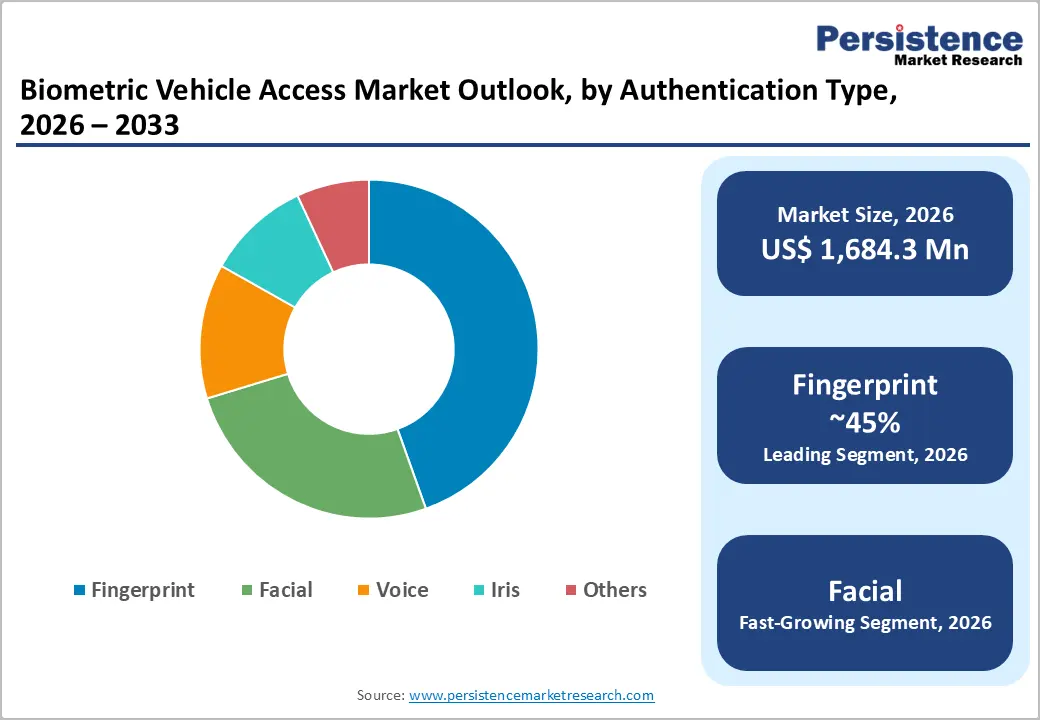

- Leading Authentication Type: Fingerprint recognition holds the largest share at around 45% in 2026, valued at over US$ 757.9 Mn, owing to its cost-effectiveness, reliability, and ease of integration across vehicle segments.

- Leading Sales Channel: The Aftermarket channel is the fastest growing, expanding at a CAGR of 22.6%, driven by increasing demand for retrofit solutions, vehicle upgrades, and cost-effective access to advanced security features in existing vehicles.

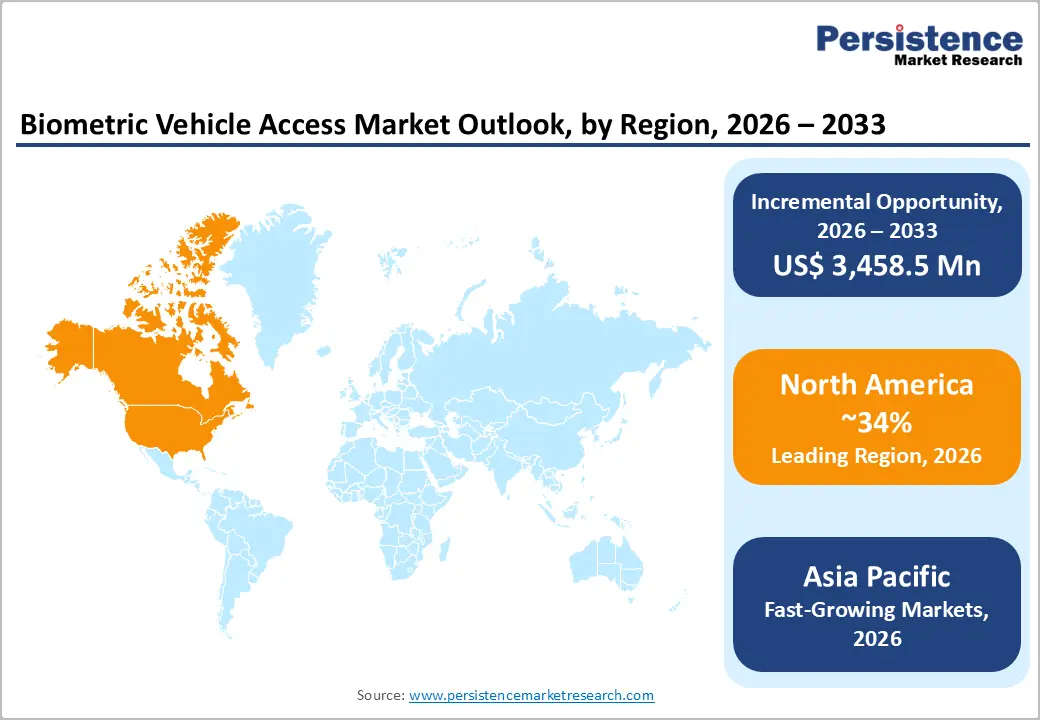

- Leading Region: North America leads the global market with around 34% share in 2026, supported by strong adoption of connected vehicles, advanced automotive ecosystems, and high demand for vehicle security solutions.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, projected to expand at a CAGR of 21.7%, driven by rapid EV adoption, increasing vehicle digitization, and the strong presence of domestic automotive and technology players.

Market Dynamics

Drivers - Rising Global Vehicle Theft Rates and Demand for Advanced Security Solutions

Rising vehicle theft incidents globally are significantly accelerating demand for biometric vehicle access systems, as OEMs and consumers prioritize advanced, tamper-proof authentication solutions. Global vehicle theft incidents are estimated to exceed 7 million in 2026 due to the rise of organized, cyber-enabled theft networks. In the United States alone, the National Insurance Crime Bureau reported over 1.02 million vehicle thefts in 2023, reflecting sustained high-risk levels into 2025. This persistent threat landscape is driving OEMs to integrate biometric authentication, reducing reliance on vulnerable key-based systems and enhancing real-time identity verification within connected vehicles.

Proliferation of Electric Vehicles and Connected Car Platforms Accelerating Integration

The global transition toward electric and software-defined vehicles (SDVs) is profoundly expanding the landscape of biometric vehicle access opportunities. EV manufacturers structurally prioritize cutting-edge features that enhance user experience, security, and in-car personalization. Chinese automakers are deploying facial recognition and fingerprint ignition systems even in mid-tier EV models, while companies such as Tesla and Ford actively explore next-generation biometric authentication for their EV lineups. As biometric hardware moves to automotive-qualified temperature ranges of −40°C to +105°C, as demonstrated by Infineon's October 2024 launch of fingerprint sensor ICs, cost-competitive deployment across broader vehicle segments becomes viable.

Restraints - High Implementation and Integration Costs Creating a Barrier to Mass-Market Penetration

The integration of biometric access systems necessitates specialized hardware components, such as capacitive fingerprint sensors, infrared cameras, and iris scanners, along with software stacks, ECU integration, and cybersecurity compliance meeting standards such as ISO/SAE 21434. These requirements substantially elevate per-vehicle system costs, particularly for entry-level and mid-range vehicle segments. OEM procurement timelines typically span 3–5 years from nomination to production, creating slow technology refresh cycles. Aftermarket retrofit complexity and compatibility challenges with legacy vehicular electronics further constrain the accessibility of biometric systems beyond premium segments, restraining volume growth.

Privacy Concerns and Data Protection Regulations Limiting Consumer Acceptance

Biometric data covering fingerprints, facial geometry, and iris patterns is classified as sensitive personal data under major regulatory frameworks, including the European Union's General Data Protection Regulation (GDPR) and state-level laws such as Illinois's Biometric Information Privacy Act (BIPA). Compliance requirements impose significant overhead on OEMs and Tier-1 suppliers for data governance, storage encryption, and consent management. Consumer wariness around biometric data breaches and unauthorized profiling continues to temper adoption rates in privacy-sensitive markets, particularly in Western Europe and parts of North America, limiting the pace of mainstream deployment.

Opportunities - Multi-Modal Biometrics and AI Integration Unlocking Personalization and In-Car Services Revenue

Biometric vehicle access is evolving into a gateway for in-car personalization and the monetization of services. The integration of AI-powered multimodal biometrics, combining fingerprint, facial, and voice recognition, as well as vital-sign monitoring, allows vehicles to auto-configure seating, infotainment, climate control, and driving modes for individual users. In September 2023, Mercedes-Benz and Mastercard announced a partnership enabling native in-car payments in Germany, allowing customers to authorize fuel payments with a vehicle-embedded fingerprint sensor. As software-defined vehicles increasingly support over-the-air biometric capability upgrades, OEMs unlock subscription revenue streams.

Rising Adoption of Biometric Fleet Management Solutions

Fleet operators are increasingly adopting biometric authentication systems to enhance driver accountability, reduce unauthorized vehicle usage, and improve operational security. With global commercial fleet vehicles exceeding a million units across logistics, ride-hailing, and corporate mobility segments, the need for secure driver identification is accelerating. Biometric access ensures that only authorized drivers operate fleet vehicles, reducing misuse, insurance risks, and operational inefficiencies. Companies are developing enterprise-grade biometric access platforms tailored for fleet management applications. Logistics companies are integrating biometric systems with telematics and GPS platforms to create fully secure mobility ecosystems, improving compliance and reducing theft-related losses.

Category-wise Analysis

Component Insights

Hardware dominates the component segment, accounting for approximately 62% of the market share with a value exceeding US$ 1,044.3 Mn in 2026 due to the fundamental need for physical biometric capture systems such as sensors, scanners, and in-vehicle authentication modules. These components are essential for enabling secure vehicle access and real-time identity verification. Increasing demand for advanced in-vehicle safety systems is pushing automakers to integrate reliable hardware at the manufacturing stage. Hardware also supports multi-modal authentication systems, improving accuracy and user convenience.

Software is emerging as the fastest-growing segment, driven by increasing reliance on AI-driven authentication, cloud connectivity, and continuous system updates. Modern vehicles require intelligent software to process biometric data, detect anomalies, and enhance security protocols. The need for personalization features and seamless user experience is further accelerating software integration. Cybersecurity requirements are also pushing demand for advanced encryption and identity management systems.

Vehicle Type Insights

Passenger vehicles account for over 53% of the 2026 value of over US$ 892.7 Mn, driven by rising consumer demand for enhanced safety, convenience, and personalized access experiences. Biometric systems are increasingly being used for keyless entry, driver identification, and theft prevention. Growing urban mobility needs and premium vehicle adoption are also supporting integration. Consumers prefer advanced security features that simplify access while improving protection.

The electric vehicles segment is witnessing the fastest growth, supported by their inherently digital and software-defined architecture. These vehicles already rely heavily on connected systems, making biometric integration easier and more efficient. The need for advanced access control and user personalization aligns well with EV design philosophy. Frequent OTA updates and smart cockpit systems further support adoption.

Authentication Type Insights

Fingerprint dominates the market, capturing around 45% share & value of over US$ 757.9 Mn in 2026, driven by its simplicity, cost-effectiveness, and proven reliability. It offers quick access with a minimal user learning curve, making it highly suitable for mass adoption. Automotive manufacturers prefer fingerprint systems because they are easier to integrate into existing vehicle interfaces. It also provides a strong balance between security and convenience.

Facial is the fastest-growing segment, driven by its contactless and highly convenient authentication experience. It enhances user comfort by enabling seamless, hands-free vehicle access and driver identification. Advances in AI and camera technologies have significantly improved accuracy and reliability. It also supports additional functionalities such as driver monitoring and fatigue detection.

Sales Channel Insights

OEM leads the sales channel segment, accounting for approximately 76% of the market share in 2026, with a value of US$1,280.1 Mn, due to their ability to integrate biometric systems directly during vehicle manufacturing. This ensures better system reliability, lower installation complexity, and improved safety compliance. Standardization at the production stage ensures consistent performance across models. Strong partnerships between automakers and technology providers further strengthen OEM dominance.

Aftermarket is the fastest-growing end-use segment, with a 22.6% CAGR, driven by rising demand for vehicle upgrades and retrofitting solutions. Consumers with existing vehicles are increasingly adopting biometric systems for enhanced security and convenience. Lower-cost retrofit kits are making advanced features accessible to a wider customer base. Growth in aging vehicle fleets is also contributing to adoption.

Regional Insights

North America Biometric Vehicle Access Market Trends and Insights

North America holds a significant position in the biometric vehicle access market, with an estimated share of around 34% in 2026, driven by strong adoption of connected and premium vehicles, particularly in the U.S. The region benefits from advanced automotive innovation ecosystems and federal-level ITS programs that broadly support smart mobility and in-vehicle security technologies. OEMs such as Tesla, Ford, and General Motors are actively integrating fingerprint and facial recognition systems in next-generation EVs and connected vehicles.

Growth is further supported by rising demand from premium vehicle buyers and expanding fleet digitalization and driver authentication use cases. The U.S. market is expected to grow at a CAGR of ~20.1% during 2026–2033, with fingerprint recognition currently being the most widely used biometric modality in automotive access systems.

Europe Biometric Vehicle Access Market Trends and Insights

Europe holds a significant share of over 26% in 2026, led by Germany, where luxury OEMs such as BMW, Mercedes-Benz, and Volkswagen Group are investing heavily in biometric-enabled vehicle access technologies. The region’s growth is strongly supported by regulatory frameworks such as GDPR and ISO/SAE 21434 cybersecurity standards, which shape secure-by-design automotive authentication systems. Luxury vehicle demand in the UK, led by Jaguar Land Rover, Bentley, and Rolls-Royce, is also accelerating the adoption of fingerprint and facial recognition systems in premium models. Companies are collaborating with payment technology providers to enable in-car biometric authentication for payments across selected service networks.

Asia Pacific Biometric Vehicle Access Market Trends and Insights

Asia Pacific is expected to grow at a 21.7% CAGR, led by China, which is witnessing rapid integration of biometric systems across EVs from BYD, NIO, and Geely, particularly facial recognition and fingerprint-based ignition systems. Growth is driven by large-scale EV adoption, increasing vehicle digitization, and strong domestic AI and sensor supply chains supported by firms such as Hikvision and Dahua in adjacent automotive applications.

India is also emerging as a high-growth market, driven by rising connected-vehicle adoption and security concerns, with OEMs such as Tata Motors, Mahindra & Mahindra, and Hyundai India exploring biometric-enabled premium SUV features. Japan focuses on precision fingerprint authentication systems, while South Korea supports automotive biometric innovation through advanced mobility programs.

Competitive Landscape

The global biometric vehicle access industry exhibits mid-level concentration, with established Tier-1 automotive suppliers bundling biometric sensors, ECUs, and credential management services under long-term OEM nomination contracts. Specialized semiconductor players compete at the component level, while software-focused entrants bring AI-based biometric matching and data security capabilities. Key competitive differentiators include multi-modal authentication accuracy, automotive qualification compliance, and the ability to support software-defined vehicle over-the-air biometric updates.

Key Market Developments

- In September 2025, the U.S. Customs and Border Protection (CBP) announced plans to launch a Vehicle Biometric Capability Evaluation (VBCE) in 2026, aimed at testing facial recognition technology for occupants in vehicles at land border entry points. The initiative will evaluate the use of AI-enabled biometric systems to verify traveler identities in real time and improve border security efficiency.

- In August 2025, Ituran launched Ituran KEY, a smartphone-based vehicle security solution that uses biometric authentication, facial, and fingerprint recognition to enable secure access and engine start. The system replaces traditional keys with a mobile app-driven digital access mechanism, enhancing anti-theft protection and user convenience.

Companies Covered in Biometric Vehicle Access Market

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- Valeo SA

- Hyundai Mobis

- Gentex Corporation

- Magna International

- ZF Friedrichshafen AG

- Synaptics Incorporated

- Fingerprint Cards AB

- Hitachi Ltd.

- NEC Corporation

- Thales Group

- HID Global

- Others

Frequently Asked Questions

The biometric vehicle access market is projected at US$ 1,684.3 million, driven by a shift toward connected and smart vehicles requiring seamless, keyless, and user-friendly authentication systems.

Rising vehicle thefts and the need for stronger, personalized security that traditional keys and fobs cannot provide.

North America leads with 34% share (2026), driven by strong OEM adoption of advanced vehicle security systems, stringent safety and cybersecurity regulations.

Integration of multimodal biometric authentication into connected and electric vehicles, enabling highly secure, personalized, and contactless keyless entry experiences.

Leading players include Continental AG, Robert Bosch GmbH, Denso Corporation, Thales Group, HID Global.