- Technology

- Intelligent Virtual Store Design Solution Market

Intelligent Virtual Store Design Solution Market Size, Share, and Growth Forecast 2026 - 2033

Intelligent Virtual Store Design Solution Market by Component (Software, Hardware, Services), by Deployment Mode (Cloud-Based, On-Premise, Hybrid), by Technology (Artificial Intelligence & Machine Learning, Virtual Reality, Augmented Reality, 3D Rendering & Simulation, Data Analytics & Predictive Modeling), Solution Type, End-User, Regional Analysis, 2026 - 2033

Intelligent Virtual Store Design Solution Market Size and Trend Analysis

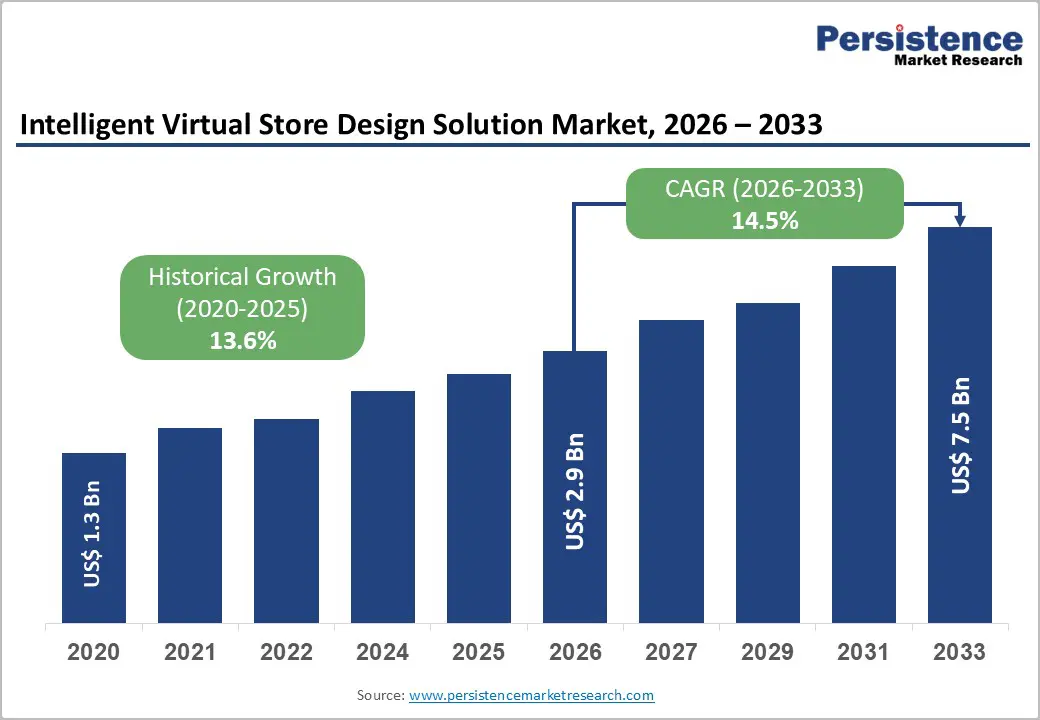

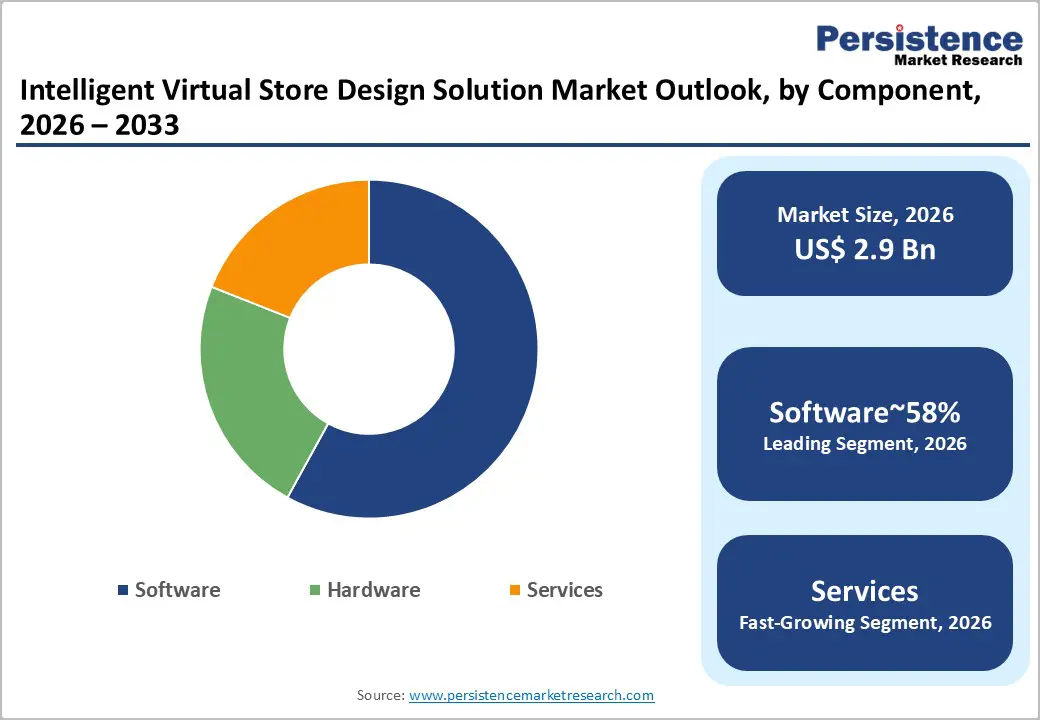

The global intelligent virtual store design solution market size is likely to be valued at US$ 2.9 billion in 2026 and is expected to reach US$ 7.5 billion by 2033, growing at a CAGR of 14.5% during the forecast period from 2026 to 2033.

This robust growth trajectory is primarily driven by the rapid convergence of artificial intelligence, augmented reality, and digital twin technologies within the retail sector, enabling brands and retailers to plan, simulate, and optimize store environments with unprecedented precision.

Key Highlights:

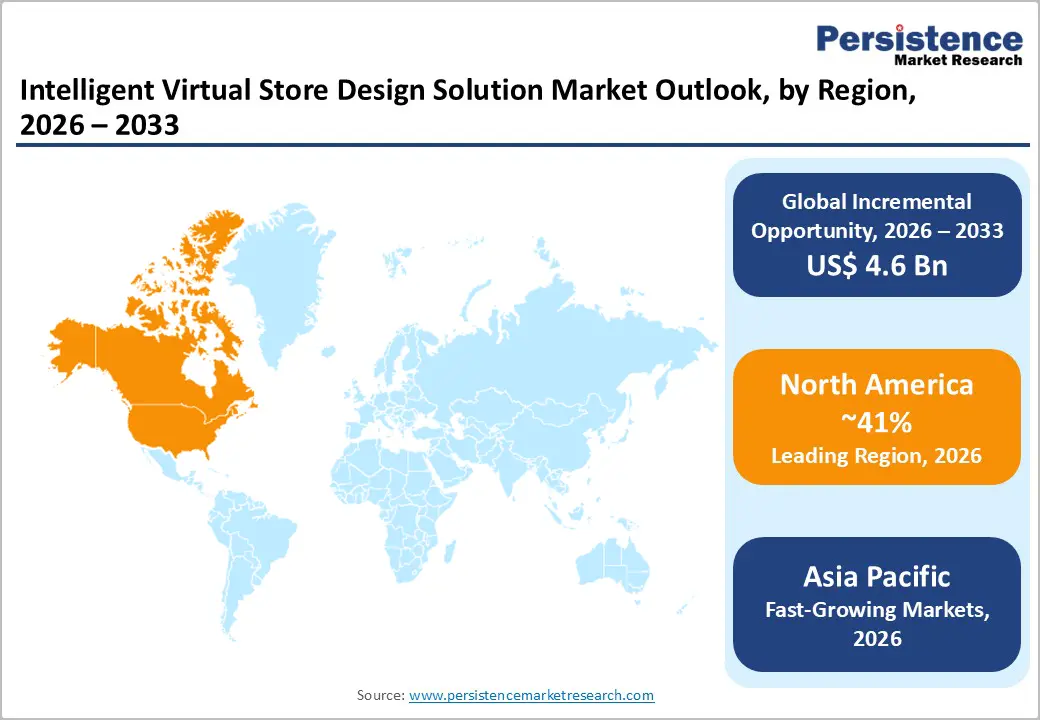

- Leading Region: North America dominates the intelligent virtual store design solution market, holding 41% share, backed by the U.S.'s advanced retail technology ecosystem, high enterprise software spending, and presence of key solution providers, including InContext Solutions and Marxent Labs.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a rising CAGR of 20.7%, driven by China's New Retail innovation wave, India's expanding organized retail sector, and ASEAN's rapid digital infrastructure development, accelerating the adoption of AI-powered virtual store platforms.

- Dominant Segment: The software component segment leads with approximately 58% market share, underpinned by SaaS delivery adoption, continuous AI/ML feature integration, and strong enterprise demand from global CPG manufacturers and grocery chains for cloud-hosted planning tools.

- Fastest-Growing Segment: Digital Twin Platforms within the Solution Type category represent the fastest-growing segment, as retailers and CPG firms invest in live virtual replicas of store environments to enable continuous scenario modeling, inventory simulation, and shopper journey optimization.

- Key Opportunity: CPG manufacturers' accelerating adoption of VR/AR shelf simulation for buyer presentations, replacing costly physical mock stores, presents a multi-billion-dollar opportunity, particularly as CPG trade promotion budgets increasingly shift toward data-validated virtual retail intelligence platforms.

Market Dynamics

Drivers - Rapid Omnichannel Retail Expansion Driving Demand for Advanced Virtual Store Design and Digital Experience Platforms

The global retail sector is rapidly shifting toward omnichannel commerce, making intelligent virtual store design solutions a major driver. Retailers are under increasing pressure to maintain a consistent brand experience across physical stores, e-commerce platforms, and virtual shopping environments. This has created strong demand for solutions that allow digital prototyping of store layouts and merchandising strategies before physical implementation.

According to the National Retail Federation (NRF), more than 67% of U.S. retailers prioritized investments in integrating in-store and digital technologies in 2024. At the same time, the global e-commerce market, valued at over US$ 6.3 trillion in 2024 by UNCTAD, is pushing retailers to replicate physical shopping experiences digitally. As a result, technologies such as 3D rendering, augmented reality visualization, and shopper behavior analytics are seeing significant adoption across global retail ecosystems.

Increasing Adoption of AI-Based Planogram Optimization Enhancing Retail Shelf Efficiency and Sales Performance Globally

Artificial intelligence is transforming how retailers manage shelf space and category planning, making it a key growth driver for the market. AI-powered planogram tools can evaluate thousands of product placement combinations in real time, helping retailers identify underperforming SKUs and recommend optimal shelf arrangements based on historical sales and shopper movement data.

According to the Consumer Goods Forum (CGF), optimized planogram execution can increase category sales by 5% to 15% while reducing out-of-stock incidents by up to 30%. Major consumer goods companies such as Procter & Gamble and Unilever are actively investing in AI-driven virtual store technologies across their retail networks. This trend is significantly boosting demand for intelligent store design platforms, especially in grocery, hypermarket, and convenience store segments, where shelf optimization directly impacts sales performance and operational efficiency.

Restraints - High Implementation Costs and Complex System Integration Limiting Adoption of Virtual Store Design Solutions

Despite strong growth potential, the high cost of implementing intelligent virtual store design platforms remains a key challenge for market adoption. Full-scale deployments, which include AI engines, VR/AR hardware, and enterprise software licensing, can cost between US$250,000 and US$2 million for large retail chains, according to Gartner Technology Advisory. These high upfront investments make it difficult for mid-sized retailers and businesses in emerging markets to adopt such solutions.

In addition to cost concerns, integration with existing systems such as ERP, POS, and supply chain platforms adds another layer of complexity. This often requires skilled technical expertise, longer deployment timelines, and collaboration with specialized implementation partners. As a result, many retailers delay or reconsider adoption decisions due to budget limitations and operational challenges associated with system integration.

Stringent Data Privacy Regulations Restricting Advanced Shopper Analytics and Limiting Virtual Store Platform Capabilities

Data privacy regulations are increasingly limiting the deployment of shopper behavior analytics, which is a core component of intelligent virtual store design platforms. Regulations such as the European Union’s GDPR and the California Consumer Privacy Act (CCPA) impose strict rules on how consumer data is collected, processed, and stored. Non-compliance penalties under GDPR can reach up to €20 million or 4% of global annual revenue, making compliance a top priority for retailers.

These regulations require companies to adopt privacy-by-design approaches, which restrict the amount and type of shopper data that can be used in virtual simulations. As a result, the depth of insights generated from these platforms may be reduced. This creates a challenge for solution providers, as they must balance advanced analytics capabilities with strict regulatory compliance requirements.

Opportunities - Growing Adoption of Digital Twin Technology Creating New Opportunities in Retail Store Simulation and Operations

The rise of digital twin technology is creating significant growth opportunities for providers of intelligent virtual store design solutions. Digital twins enable retailers to create real-time, dynamic replicas of physical store environments, allowing continuous simulation of layouts, inventory, and customer journeys. The World Economic Forum (WEF) has recognized digital twins as a key component of Industry 4.0 transformation in the retail industry. According to the International Data Corporation (IDC), more than 30% of Fortune 2000 retailers are expected to adopt digital twin technologies by 2027.

This trend is opening new revenue opportunities for companies such as Dassault Systèmes and PTC Inc., as retailers increasingly look to integrate virtual planning tools with real-time supply chain and inventory data. Digital twins not only improve operational efficiency but also enable faster decision-making, making them a highly attractive investment for modern retail businesses.

Rising Use of VR and AR by CPG Companies Transforming Shelf Simulation and Buyer Engagement Processes

Consumer packaged goods (CPG) manufacturers are emerging as a key growth segment for virtual store design platforms. These companies are increasingly using virtual reality (VR) and augmented reality (AR) tools to simulate shelf layouts and present them to retail buyers, replacing expensive physical mock store setups that can cost over US$ 500,000. According to McKinsey & Company, virtual store testing can reduce research timelines by up to 60% and lower costs by nearly 40%.

Platforms such as InContext Solutions and Emperia are already leveraging this trend to expand their market presence. With global CPG spending on retail insights and category management exceeding US$5 billion annually, virtual store platforms are well positioned to capture a larger share of this investment. This shift is accelerating adoption across the CPG sector and strengthening long-term market growth potential.

Category-wise Analysis

By Component Insights

The software segment leads the market by component, accounting for approximately 58% of the total share. Software platforms form the core of intelligent virtual store design solutions, offering capabilities such as AI-powered planogram optimization, 3D visualization, shopper analytics, and digital twin management. The growing adoption of Software-as-a-Service (SaaS) models has further strengthened this segment by reducing upfront costs and enabling recurring revenue streams.

The enterprise SaaS adoption among global retailers increased by over 22% between 2021 and 2024. Leading technology providers such as SAP SE, Oracle Corporation, and Adobe Inc. continue to enhance their retail software offerings by integrating advanced AI and machine learning features. This continuous innovation is reinforcing the dominance of the software segment and making it the foundation of modern virtual store design solutions.

By Deployment Mode Analysis

Cloud-based deployment is the leading segment in the market, accounting for approximately 62% of total revenue. This model offers several advantages, including scalability, lower total cost of ownership, automatic updates, and easy integration with third-party platforms such as Google Cloud Retail AI and Microsoft Azure for Retail. According to IDC, by 2023 more than 70% of new enterprise software deployments in retail were cloud-first.

Cloud solutions are particularly preferred by multi-location retail chains and global CPG companies, as they allow real-time collaboration and synchronization across different regions. Retailers can easily update planograms, share simulation results, and manage store layouts from a centralized system. This flexibility and efficiency make cloud-based deployment the preferred choice for modern retail organizations looking to scale their operations.

By Technology Analysis

Artificial intelligence and machine learning represent the leading technology segment, holding an estimated 34% market share. These technologies act as the core intelligence layer, powering key functionalities such as predictive product placement, shopper behavior analysis, and real-time planogram optimization. AI also enhances 3D visualization tools and improves customer journey simulations in virtual environments.

According to a 2024 IBM Institute for Business Value study, 62% of retail executives identified AI-driven analytics and personalization as their top technology investment priority. The integration of generative AI is further accelerating innovation in this space, enabling features like natural language-based store design and automated scenario planning. As retailers continue to prioritize data-driven decision-making, AI and machine learning will remain central to the growth and evolution of virtual store design solutions.

By Solution Type Analysis

Store layout and space planning is the leading solution type, contributing approximately 29% of total market revenue. This segment addresses the fundamental need to optimize retail floor space, improve customer flow, and maximize sales per square foot. Research from Cornell University’s Center for Hospitality Research shows that well-designed store layouts can increase average basket size by 8% to 12% and improve customer dwell time by up to 18%.

Leading platforms from InContext Solutions, Dassault Systèmes, and Unity Technologies provide advanced 3D simulation tools that allow retailers to visualize and test store layouts before implementation. These tools help businesses optimize product placement, aisle design, and checkout configurations, thereby reducing costly trial-and-error. As retail competition intensifies, efficient space utilization remains a key priority, driving continued demand for these solutions.

By End-user Insights

CPG manufacturers represent the largest end-user segment, accounting for approximately 31% of total market demand. These companies rely heavily on effective shelf placement, category management, and retail partnerships to drive sales performance. Virtual store design platforms enable them to simulate product placements and optimize planograms before presenting them to retail partners.

According to the Grocery Manufacturers Association (GMA), large CPG companies spend over US$ 800 million annually on trade promotions and category management activities. Increasingly, a portion of this budget is being allocated to virtual store technologies. Major companies such as Nestlé, PepsiCo, and Coca-Cola are already using these platforms to collaborate with retailers like Walmart and Tesco. This shift reduces reliance on physical mock stores and accelerates decision-making, making virtual store solutions an essential tool for CPG manufacturers.

Regional Insights

North America Intelligent Virtual Store Design Solution Trends

North America holds the largest share of the global intelligent virtual store design solution market, driven by the United States’ advanced retail technology ecosystem and strong enterprise software investment culture. The U.S. retail industry, the world’s second largest with annual sales of around US$ 7.2 trillion, has a high concentration of technology-driven retailers and CPG companies actively adopting AI-powered virtual merchandising and planogram solutions.

Leading companies such as InContext Solutions and Marxent Labs are headquartered in the U.S., highlighting the region’s innovation leadership. On the regulatory side, frameworks from the Federal Trade Commission (FTC) and CCPA are influencing how shopper analytics solutions are designed, encouraging the use of privacy-compliant synthetic data and anonymized simulations. Additionally, the National Retail Federation (NRF) 2024 Big Show demonstrated strong momentum, with over 40% of exhibitors showcasing AI, AR, or digital twin retail solutions, indicating continued enterprise adoption.

Europe Intelligent Virtual Store Design Solution Trends

Europe is the second-largest regional market, with Germany, the United Kingdom, and France acting as key adoption centers. Germany’s retail sector, led by major players such as REWE Group, Lidl, and ALDI, is increasingly adopting virtual store planning tools to efficiently manage complex multi-format store operations. France-based Dassault Systèmes has built a strong regional presence through its 3DEXPERIENCE platform, serving several European grocery and CPG companies. Similarly, SAP SE’s SAP Customer Experience suite is widely used among German and Swiss retailers for integrated category management.

Regulatory frameworks such as GDPR and the European AI Act (2024) are shaping the market by creating both compliance requirements and innovation opportunities, particularly in transparent and explainable AI solutions. Meanwhile, Spain and Italy are emerging as growth markets, supported by grocery modernization initiatives and EU Digital Compass 2030 policies, which are accelerating technology adoption among mid-sized retailers and FMCG companies.

Asia Pacific Intelligent Virtual Store Design Solution Trends

Asia Pacific is the fastest-growing regional market, driven by large consumer populations and rapid digital infrastructure development across China, India, and ASEAN countries. China’s retail technology ecosystem, led by Alibaba’s New Retail concept and JD.com’s smart store initiatives, has been at the forefront of integrating AI-based shelf analytics and virtual reality store planning at scale.

According to the China Ministry of Commerce, technology investment per retail outlet in Tier-1 cities increased by over 28% between 2021 and 2023, with virtual merchandising tools playing a key role. In India, the Ministry of Commerce & Industry’s National Retail Trade Policy and rising e-commerce penetration, expected to reach US$ 200 billion by 2027 (IBEF), are driving demand for virtual store design platforms among organized retailers and D2C brands. Japan and South Korea are also early adopters of AR-enabled retail solutions, supported by strong 5G infrastructure and growing demand for immersive digital shopping experiences.

Competitive Landscape

The intelligent virtual store design solution market is moderately fragmented, with a mix of global technology giants and specialized retail technology providers competing for market share. Major enterprise players such as Microsoft, IBM, Oracle, SAP SE, and Dassault Systèmes compete alongside niche innovators such as InContext Solutions, Emperia, Obsess, and Marxent Labs.

Companies are differentiating themselves based on the strength of their AI capabilities, quality of photorealistic rendering, depth of ERP integration, and scalability of cloud-based platforms. A key emerging trend is the integration of generative AI into virtual store design, with vendors increasingly focusing on embedding large language model (LLM)-based scenario generation features. Additionally, strategic initiatives such as mergers and acquisitions, partnerships with leading CPG companies, and a shift toward platform-as-a-service (PaaS) business models are shaping the competitive landscape and are expected to drive market evolution through 2033.

Key Developments:

- March 2025: Microsoft Corporation expanded its Azure for Retail platform with a new AI-powered virtual store layout module, enabling retailers to generate and simulate photorealistic store designs using generative AI prompts, targeting grocery and hypermarket operators globally.

- November 2024: Dassault Systèmes launched an enhanced version of its 3DEXPERIENCE Retail Twin solution, integrating real-time shopper behavior data feeds from IoT sensors into its digital twin platform, with initial deployments announced across five major European CPG manufacturers.

- June 2024: InContext Solutions announced a strategic partnership with Circana (formerly IRI and NPD Group) to embed syndicated point-of-sale data directly into its virtual store simulation environment, enabling CPG clients to conduct data-validated planogram optimization within a single platform.

Intelligent Virtual Store Design Solution Market Report - Key Insights & Scope

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.3 Bn |

| Current Market Value (2026) | US$ 2.9 Bn |

| Projected Market Value (2033) | US$ 7.5 Bn |

| CAGR (2026 - 2033) | 14.5% |

| Leading Region | North America, 41% share |

| Dominant Component | Software, 58% share |

| Top-ranking Deployment Mode | Cloud-based, 62% |

| Incremental Opportunity | US$ 4.6 Bn |

Companies Covered in Intelligent Virtual Store Design Solution Market

- Microsoft Corporation

- IBM Corporation

- Cisco Systems Inc.

- Oracle Corporation

- SAP SE

- Adobe Inc.

- Dassault Systèmes

- Unity Technologies

- Magic Leap Inc.

- Zebra Technologies

- PTC Inc.

- InContext Solutions

- Marxent Labs LLC

- Emperia

- Obsess

- Trigo Vision Ltd.

- Spacee Inc.

- Retail VR

- Cimagine Media

- Blue Yonder Group Inc.

Frequently Asked Questions

The global Intelligent Virtual Store Design Solution Market is projected to reach US$ 7.5 Billion by 2033, up from US$ 2.9 Billion in 2026, expanding at a compound annual growth rate of 14.5% during the forecast period, reflecting accelerating retail digitalization and AI-driven merchandising adoption worldwide.

The primary demand drivers include the global retail sector's pivot to omnichannel commerce, surging investment in AI-powered planogram optimization, and the adoption of digital twin platforms for real-time store simulation. The imperative to reduce planogram execution failures, estimated to cost retailers over US$ 300 Billion annually, further accelerates enterprise platform procurement.

The Cloud-Based deployment segment is the clear leader, holding approximately 62% of market revenue. Its dominance is driven by lower total cost of ownership, rapid scalability, and seamless integration with retail AI ecosystems such as Microsoft Azure for Retail and Google Cloud Retail AI, enabling real-time cross-team planogram collaboration for global CPG and grocery enterprises.

North America is the leading regional market, anchored by the United States' large retail technology spend, world-class enterprise software ecosystem, and presence of specialized platform providers including InContext Solutions, Marxent Labs, and Obsess. The NRF's ongoing commitment to retail digitalization further sustains the region's dominant position.

The most significant near-term opportunity lies in expanding adoption of Digital Twin platforms among global retailers, as projected by the IDC to be deployed by over 30% of Fortune 2000 retailers by 2027. Additionally, CPG manufacturers' accelerating replacement of physical mock stores with VR/AR shelf simulation environments offers solution vendors a compelling, high-value revenue expansion avenue.

Leading companies in this market include Microsoft Corporation, IBM Corporation, SAP SE, Oracle Corporation, Dassault Systèmes, Adobe Inc., Unity Technologies, PTC Inc., InContext Solutions, Emperia, and Obsess, among others. These players compete through AI model sophistication, photorealistic rendering quality, and the depth of retail ERP and data ecosystem integrations offered on their platforms.