- Retail

- Commercial Cooking Equipment Market

Commercial Cooking Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Commercial Cooking Equipment Market by Equipment (Ovens, Cooktops and Ranges, Grills, Fryers, Cook-chill Systems, Broilers, Steamers, Others), Application (Full-Service Restaurants, Quick-Service Restaurants, Others), and Regional Analysis for 2026 - 2033

Commercial Cooking Equipment Market Size and Trend Analysis

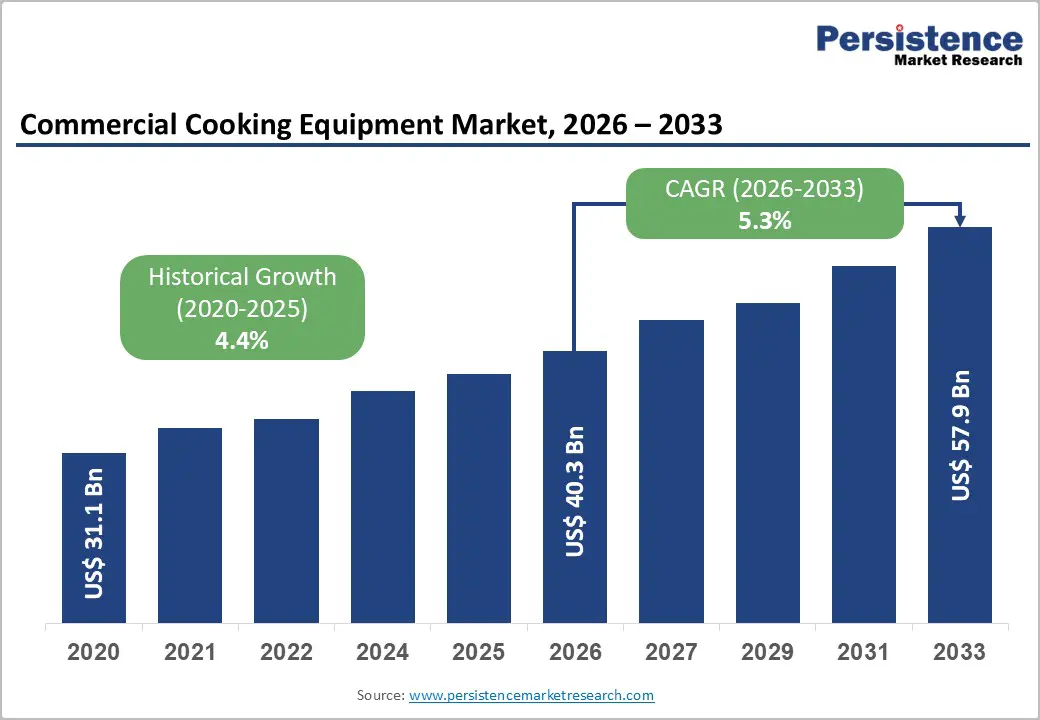

The global commercial cooking equipment market is valued at US$ 40.3 billion in 2026 and is projected to reach US$ 57.9 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. This steady expansion is fundamentally anchored in the continued global expansion of the foodservice industry, driven by surging restaurant industry revenues, the proliferation of cloud kitchens, and the hospitality sector's ongoing investment in modern, energy-efficient, and automated kitchen equipment.

The National Restaurant Association's 2025 State of the Restaurant Industry report confirms that the U.S. restaurant industry surpassed US$ 1.1 trillion in annual sales in 2024 and is projected to reach US$ 1.5 trillion across the total foodservice industry in 2025, a near 82% increase from 2020, directly sustaining robust demand for commercial cooking equipment replacement and capacity expansion.

Key Market Highlights

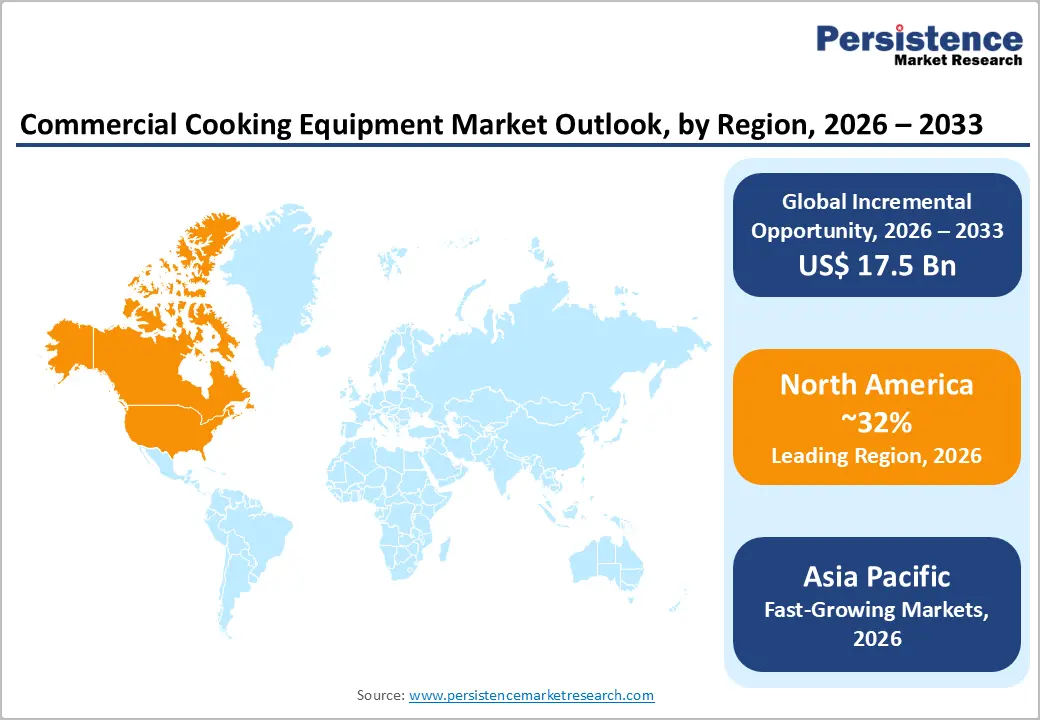

- Leading Region – North America leads the global commercial cooking equipment market with approximately 32% revenue share in 2025, underpinned by the U.S. restaurant industry surpassing US$ 1.1 trillion in sales in 2024 per the National Restaurant Association and sustained new restaurant opening activity.

- Fastest-Growing Region – Asia Pacific is the fastest-growing region, driven by India's foodservice sector projected to grow at approximately 8% CAGR to 2028, China's massive restaurant volume, and rapid QSR chain expansion across ASEAN nations with growing middle-class populations.

- Dominant Segment – Full-Service Restaurants lead the global market with approximately 43% revenue share, as FSRs operate the most complex commercial kitchen infrastructures requiring the broadest equipment portfolio, sustained by 90% of fine dining operators prioritizing on-premise experience per the National Restaurant Association.

- Fastest-Growing Segment – QSRs represent the fastest-growing application segment, propelled by global expansion of fast food chains, technology-driven efficiency demands in high-volume kitchens, and the explosion of QSR formats in emerging economies across Asia Pacific, Latin America, and the Middle East.

- Key Market Opportunity – The global explosion of cloud kitchens, requiring high-throughput, space-optimized, multifunctional cooking equipment, combined with AI-integrated, IoT-connected cooking platforms (combi ovens, smart fryers), is creating high-growth, high-margin equipment categories for forward-investing OEMs.

| Key Insights | Details |

|---|---|

|

Commercial Cooking Equipment Market Size (2026E) |

US$ 40.3 Billion |

|

Market Value Forecast (2033F) |

US$ 57.9 Billion |

|

Projected Growth CAGR (2026–2033) |

5.3% |

|

Historical Market Growth (2020–2025) |

4.4% CAGR |

DRO Analysis

Drivers - Sustained Expansion of the Global Foodservice Industry

The most powerful structural driver of the global commercial cooking equipment market is the sustained and broad-based growth of the worldwide foodservice industry, which directly drives replacement demand, capacity expansion, and technology upgrade cycles across all equipment categories. The National Restaurant Association reports that the U.S. restaurant industry employed over 15.9 million people and generated sales projected to exceed US$ 1.1 trillion in 2025, a landmark milestone, while the entire U.S. foodservice industry, including lodging, bars, and schools, is expected to reach US$ 1.5 trillion in sales.

The National Restaurant Association's 2025 State of the Restaurant Industry report notes that more than 8 in 10 restaurant operators expect 2025 sales to be either higher or the same as in 2024, reflecting sustained confidence in capital investment. Globally, over 691,000 chain restaurant locations were operating in 2024, per Technomic Ignite data, with 29% of operators planning to open new locations in 2025, each new opening requiring fresh commercial cooking equipment investment.

Rising Adoption of Smart, IoT-Enabled, and Energy-Efficient Equipment

Commercial kitchen operators are increasingly replacing aging equipment with smart, connected, and energy-efficient alternatives, driven by rising energy costs, tightening sustainability regulations, and labor-optimization pressures. ENERGY STAR programs administered by the U.S. Environmental Protection Agency (EPA) provide rebates and compliance incentives for certified commercial cooking equipment, with ENERGY STAR warewasher units recording a 9.2% year-on-year volume increase in 2024, and Wi-Fi-enabled combi ovens experiencing 34% growth in chain restaurants during the same period.

RATIONAL AG introduced the iHexagon in February 2024, an innovative commercial cooking system integrating steam, hot air, and microwave technologies in a single platform, enabling food preparation to the desired quality in minimum time with its iClimateBoost cooking assistant. Over 50% of new commercial cooking equipment launches in 2024 emphasized environmental compliance and space-saving design, reflecting the market's structural technology upgrade cycle. Automation and IoT connectivity are also addressing the 70% operator struggle to fill kitchen positions, per the National Restaurant Association, by enabling more efficient, lower-labor kitchen operations.

Restraints - High Initial Capital Expenditure and Budget Constraints

The commercial cooking equipment market faces a significant restraint in the high upfront cost of commercial-grade cooking systems, particularly for small and medium-sized foodservice operators. Advanced combi ovens, high-capacity fryer systems, and cook-chill installations require substantial capital outlays, creating budgetary friction in price-sensitive market segments. Approximately 34% of small contractors and foodservice operators delay equipment investments due to budget constraints, while 78% of restaurants still carry pandemic-era debt loads, according to recent survey data. These financial pressures limit replacement cycle frequency and slow the adoption of premium smart equipment among independent restaurant operators.

Volatility in Raw Material Prices and Supply Chain Disruptions

Commercial cooking equipment manufacturers face ongoing margin pressure from volatility in key raw material costs, particularly stainless steel, aluminum, copper, and electronic components. Stainless steel, the dominant construction material for commercial cooking equipment, experienced significant price fluctuations from 2021 to 2024, raising equipment OEM manufacturing costs and elevating procurement prices for foodservice buyers. Supply chain disruptions of semiconductor components essential to smart and IoT-enabled equipment have caused production delays and inventory constraints, slowing the commercialization timelines for connected cooking platforms and dampening near-term growth in the premium equipment segment.

Opportunities - Cloud Kitchen Expansion and Ghost Restaurant Infrastructure Investment

The explosive global proliferation of cloud kitchens, delivery-only food preparation facilities requiring high-density commercial cooking equipment without front-of-house infrastructure, represents one of the most compelling growth opportunities in the Commercial Cooking Equipment market. Cloud kitchens typically require high-throughput, space-optimized, and multifunctional cooking equipment to maximize output from compact footprints, making them ideal end-markets for advanced combi ovens, fryers, and automated cooking solutions.

Welbilt incorporated self-cleaning technology into 70% of its new units targeted for cloud kitchen setups, reflecting OEM responsiveness to this segment. Food Service India Pvt Ltd announced plans in October 2024 to raise US$ 80–120 crore to fuel global expansion in the HORECA sector, targeting US$ 1,000 billion in revenue by 2027–28, exemplifying the scale of emerging-market cloud kitchen investment flows.

Multifunctional and AI-Integrated Cooking Equipment Innovation

The growing demand for multifunctional and AI-assisted commercial cooking equipment presents a high-value opportunity for manufacturers capable of integrating multiple cooking modalities, baking, roasting, steaming, grilling, and frying, into space-efficient, programmable platforms. RATIONAL AG launched a self-cleaning commercial steamer with AI-assisted menu programming in early 2024 and launched the iHexagon multi-technology platform in February 2024.

Middleby Corporation launched a multi-mode combi oven with IoT capabilities and 20% faster cooking speeds in 2024. Henny Penny Corporation launched the latest generation of Flex Fusion Combi Ovens in January 2024, featuring advanced humidity control and precision cooking capabilities. Alto-Shaam, Inc. expanded into Australia and New Zealand in January 2025 to capture Pacific market demand for high-performance cooking systems.

Category-wise Analysis

Equipment Insights

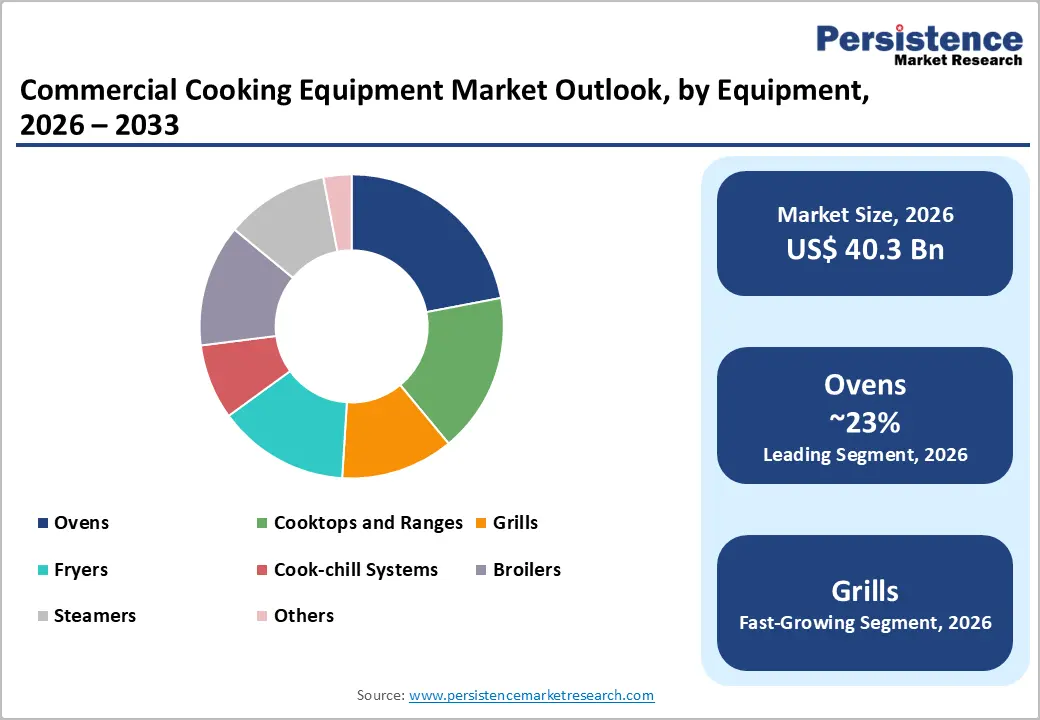

The ovens are leading the global market by equipment type, accounting for approximately 23% of total revenue in 2026. Commercial ovens, including combi-steam, convection, deck, and conveyor ovens, serve as the foundational cooking platform across the broadest range of foodservice operations, from full-service restaurants and hotels to quick-service chains, bakeries, institutional kitchens, and healthcare facilities.

The appliances analysis confirms that the oven segment accounted for the largest revenue share of 21.5% in 2026, driven by strong growth in the foodservice industry, including restaurants, cafes, hotels, catering services, and QSRs. Smart combi ovens with IoT remote monitoring capabilities experienced 34% growth in chain restaurant deployments in 2026. Fryers commanding approximately 18% of equipment revenue, according to some analyses, represent a closely competitive category, particularly within QSR and fast-casual formats where fried food throughput is operationally critical.

Application Insights

The Full-Service Restaurants (FSRs) application segment leads the global Commercial Cooking Equipment market, accounting for approximately 43% of total revenue in 2026, according to Grand View Research's foodservice equipment market data. FSRs encompassing casual dining, fine dining, and family restaurants operate the broadest and most complex commercial kitchen infrastructures, requiring the widest range of equipment across cooking, holding, storage, and warewashing.

These establishments invest in premium multi-functional and connected cooking platforms to deliver complex, high-quality menus with operational efficiency. The National Restaurant Association notes that 90% of fine dining and 87% of casual dining restaurants prioritize building a successful on-premises dining experience, sustaining continuous investment in high-performance commercial cooking systems. Quick-Service Restaurants (QSRs) represent the second-largest segment and the fastest-growing, driven by the global expansion of fast-food chains, the proliferation of QSR formats in emerging economies, and the technology-driven efficiency imperative in high-volume, low-margin foodservice operations.

Regional Analysis

North America Commercial Cooking Equipment Trends

North America is the leading region in the global commercial cooking equipment market, accounting for approximately 32% of total revenue in 2025, anchored by the United States, which has the world's largest and most mature commercial foodservice industry. The National Restaurant Association reports that the U.S. restaurant and foodservice industry surpassed US$ 1.1 trillion in sales in 2024 and is forecast to reach US$ 1.5 trillion for the total foodservice sector in 2025, a figure that directly underpins the most substantial commercial cooking equipment procurement base globally.

The North American regulatory and innovation ecosystem, anchored by ENERGY STAR certification requirements, NSF International food safety standards, and the NRAEF's ServSafe program, drives continuous upgrades in equipment technology toward energy efficiency and hygiene compliance. Middleby Corporation, headquartered in Elgin, Illinois, announced the acquisition of Char-Griller along with Kamado Joe and Masterbuilt brands in February 2025, further consolidating its premium outdoor and commercial cooking portfolio.

Asia Pacific Commercial Cooking Equipment Market Trends

Asia Pacific is the fastest-growing region in the global Commercial Cooking Equipment market, anchored by the world's largest and most dynamic foodservice expansion pipeline across China, India, Japan, and Southeast Asia. China, the world's largest restaurant market by volume, sustains enormous demand for commercial cooking equipment from its massive urban foodservice sector, hotel industry, and institutional catering operations. India's foodservice sector contributes approximately 1.8% of GDP and is projected to grow from US$ 68 billion to over US$ 90 billion by 2028 at approximately 8% CAGR, per industry analysis, generating expanding demand for commercial kitchen equipment across full-service and fast-food formats.

Japan's market is characterized by high-quality, precision-cooking equipment demand from its world-renowned restaurant and hospitality sector. ASEAN nations, particularly Vietnam, Thailand, Indonesia, and the Philippines, are witnessing rapid expansion of QSR chains by both international and regional brands, driving new installations of commercial cooking equipment. Tim Hortons opened its third airport store in India at Terminal 1 of the Indira Gandhi International Airport in February 2024, exemplifying the tier-1 and airport-format expansion, driving new equipment procurement across the region.

Europe Commercial Cooking Equipment Market Trends

Europe is a mature and technologically sophisticated market for Commercial Cooking Equipment, driven by the continent's world-class hospitality industry, stringent energy efficiency and food safety regulations, and the concentration of leading equipment manufacturers in Germany, Italy, France, and the UK. Germany, home to premium OEMs including RATIONAL AG and MKN Maschinenfabrik Kurt Neubauer GmbH & Co. KG, is the region's largest national market, with its foodservice equipment sector projected to register a CAGR of 4.1% through 2035, driven by institutional kitchen upgrades and bakery chain refurbishments.

The UK holds approximately 32% of the European Commercial Cooking Equipment market and is expected to surpass US$ 1,191 million in valuation by 2025, driven by the rapid expansion of QSR chains, delivery platforms, and cloud kitchen infrastructure in major urban centers. The EU's Energy Efficiency Directive and national sustainability policies in France, Spain, and the Nordic countries are compelling commercial kitchen operators to prioritize ENERGY STAR-equivalent rated equipment.

Competitive Landscape

The global commercial cooking equipment market is moderately consolidated at the top, with a small number of large multinational OEMs, including The Middleby Corporation, Illinois Tool Works (ITW) Food Equipment, Welbilt Inc. (now part of Ali Group), RATIONAL AG, and Electrolux Professional holding significant combined market share alongside a long tail of regional and niche manufacturers.

Consolidation through acquisitions has been a defining competitive strategy: Ali Group revived the Welbilt brand in North America in April 2024. Key differentiators among leaders include breadth of equipment portfolio, IoT/connectivity integration, ENERGY STAR certification, global dealer and service network depth, and proprietary software platforms for connected kitchen management.

Key Industry Developments:

- In November 2025, Unox acquired Roboqbo, an Italian manufacturer specializing in robotic food processing systems, to accelerate the development of automated commercial kitchens. The acquisition aimed to integrate Roboqbo’s advanced robotics with Unox’s intelligent ovens, extending automation capabilities to cooking and preparation tasks beyond traditional baking processes.

- In September 2024, Electrolux Professional introduced the NeoBlue Touch under-counter dishwasher, which is expected to provide significant efficiency and performance benefits to fast-food establishments, restaurants, and beverage chains. The dishwasher offers a one-touch button for convenient usage and a companion application for easy selection of wash cycles and detergent ordering.

Companies Covered in Commercial Cooking Equipment Market

- The Middleby Corporation

- ITW Food Equipment

- Welbilt Inc.

- RATIONAL

- Alto-Shaam, Inc.

- Henny Penny Corporation

- Duke Manufacturing Co.

- MKN Maschinenfabrik Kurt Neubauer GmbH & Co. KG

- Electrolux Professional

- Garland Group

Frequently Asked Questions

The global Commercial Cooking Equipment market is estimated to be valued at US$ 40.3 Billion in 2026 and is projected to reach US$ 57.9 Billion by 2033, registering a CAGR of 5.3% during the forecast period 2026–2033.

The primary demand drivers are the sustained global expansion of the restaurant and foodservice industry with the U.S. sector expected to reach US$ 1.5 trillion in 2025 per the National Restaurant Association, India's foodservice sector growing at approximately 8% CAGR, and 29% of restaurant operators planning new openings in 2025 combined with the technology upgrade cycle driven by smart, IoT-enabled, and ENERGY STAR-certified commercial cooking equipment adoption.

The Ovens segment is the leading equipment category, accounting for approximately 23% of global Commercial Cooking Equipment market revenue in 2026, per Grand View Research's commercial kitchen appliances analysis. Commercial ovens including combi-steam, convection, deck, and conveyor ovens serve the broadest range of foodservice operations and are the platform of choice for both FSRs and QSRs.

North America leads the global Commercial Cooking Equipment market with approximately 32% of total revenue in 2025, anchored by the United States' world-leading commercial foodservice industry that surpassed US$ 1.1 trillion in restaurant sales in 2024 per the National Restaurant Association.

The leading companies in the global Commercial Cooking Equipment market include The Middleby Corporation, ITW Food Equipment (Illinois Tool Works), Welbilt Inc. (Ali Group), RATIONAL AG, Alto-Shaam, Inc., Henny Penny Corporation, Duke Manufacturing Co., MKN Maschinenfabrik Kurt Neubauer GmbH & Co. KG, Electrolux Professional Group, and Garland Group.