- Retail

- Pet Tech Products Market

Pet Tech Products Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Pet Tech Products Market by Product Type (Wearables & Trackers, Smart Feeding Solutions, Smart Hygiene Solutions, Health Monitoring Devices, Pet Cameras & Monitoring Systems, Other Smart Devices), Technology Type (GPS-based Systems, RFID-enabled Devices, Sensor-based Systems, Camera & AI-enabled Systems, Connectivity Platforms), Pet Type (Dogs, Cats, Others), Distribution Channel, and Regional Analysis from 2026 to 2033

Pet Tech Products Market Share and Trends Analysis

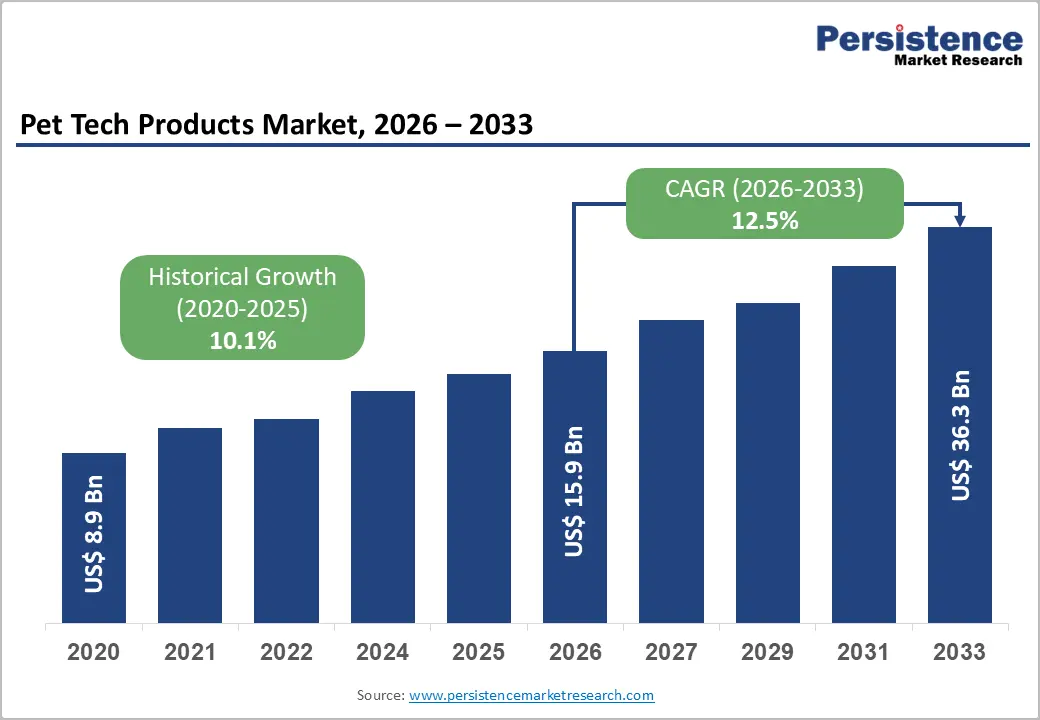

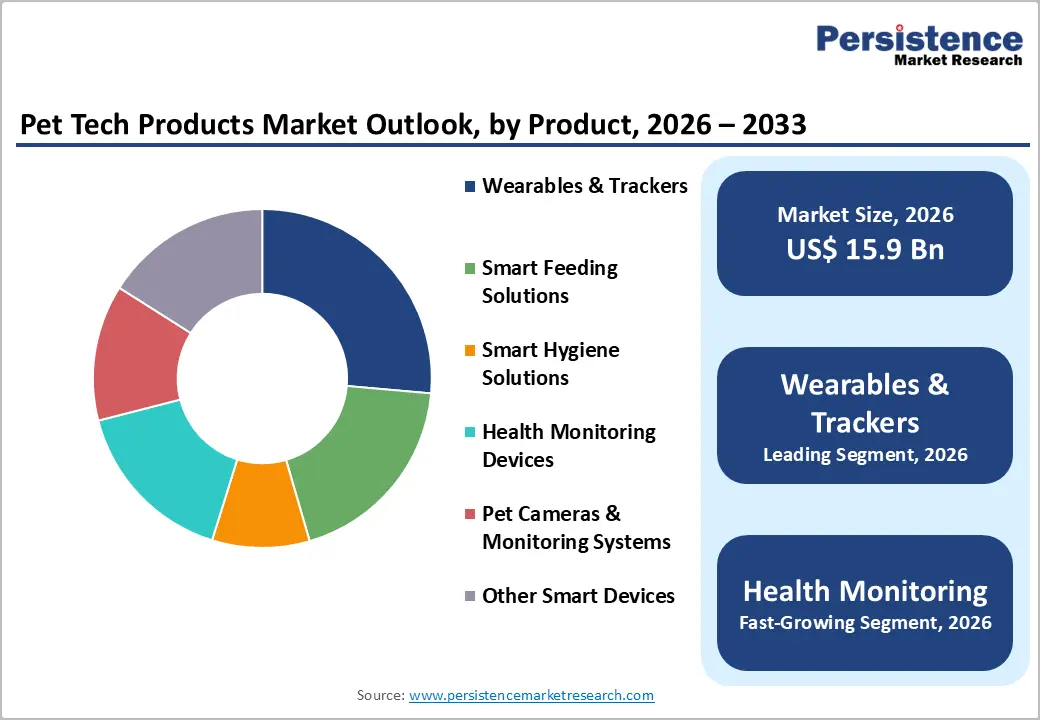

The global pet tech products market size is anticipated at US$ 15.9 billion in 2026 and is projected to reach US$ 36.3 billion by 2033, growing at a CAGR of 12.5% between 2026 and 2033.

Rising pet humanization trends, widespread smartphone adoption, and growing demand for real-time health diagnostics are the primary growth catalysts. The expansion of IoT and AI integration in pet devices, combined with increased veterinary telehealth adoption across North America and Europe, is accelerating consumer spending on connected pet-care solutions.

Key Industry Highlights:

- Leading Products: Wearables & trackers lead product segments with 26.4% share. Pet cameras & monitoring systems are the fastest-growing sub-segment, with a 12.9% CAGR, driven by AI feature integration.

- Leading Technology: GPS-based systems dominate technology at 29.4% share. Connectivity platforms are likely to grow at a 15.1% CAGR, driven by cloud- and app-based subscription models.

- Leading Pet Type: Dogs command 58.6% of the pet type share; Cats represent the fastest-growing segment, with a 13.3% CAGR, unlocking significant new product development potential.

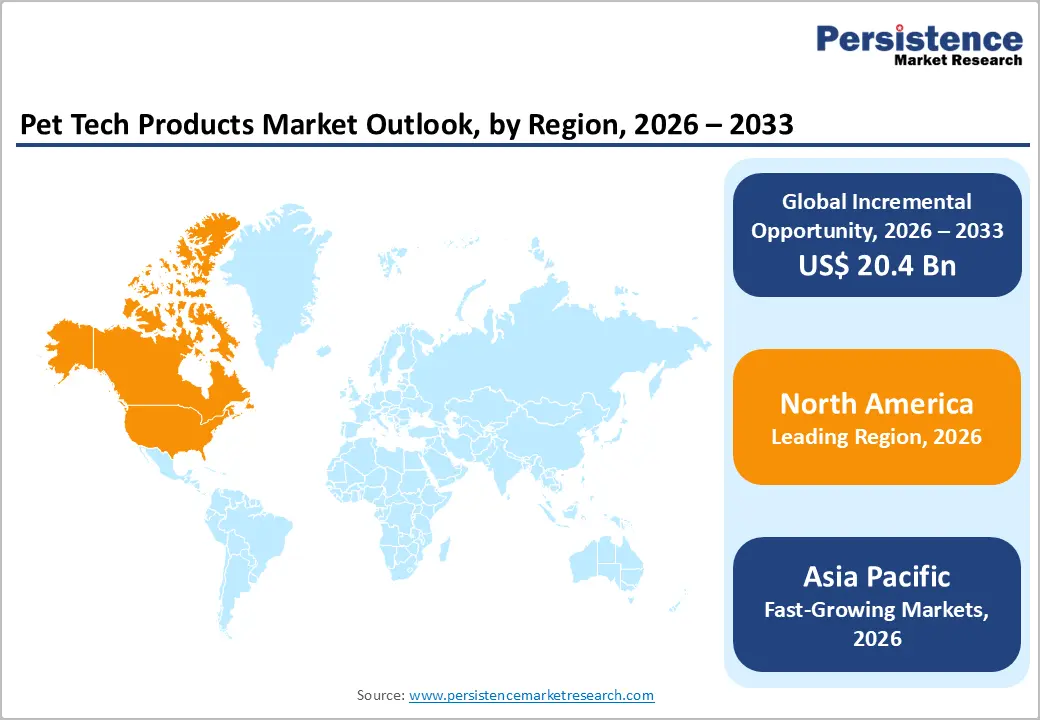

- Regional Leadership: North America holds 41.8% global share; Asia Pacific is the fastest-growing region at 15.4% CAGR, led by China, Japan, and India's expanding pet economies.

- Acquisition: Tractive's acquisition of Whistle (2025) and the CAT 6 Mini launch (April 2026) exemplify accelerating M&A consolidation and species-expansion strategies reshaping the competitive landscape.

| Key Insights | Details |

|---|---|

| Pet Tech Products Market Size (2026E) | US$ 15.9 Bn |

| Market Value Forecast (2033F) | US$ 36.3 Bn |

| Projected Growth CAGR (2026 - 2033) | 12.5% |

| Historical Market Growth (2020 - 2025) | 10.1% |

Market Dynamics Analysis

Drivers - Rising Pet Humanization and Premiumization of Pet Care

The deepening emotional bond between pet owners and their animals is fundamentally reshaping consumer spending behavior. Pet ownership in the U.S. reached approximately 66% of households, according to the American Pet Products Association (APPA), with annual pet industry expenditures exceeding US$ 147 billion in 2023. Millennials and Gen Z, who increasingly view pets as family members, are driving demand for premium, technology-embedded products. This demographic shift directly fuels the adoption of smart collars, health monitors, and automated feeders that prioritize convenience and preventive health outcomes.

Growth in Pet Health Awareness and Tele-Vet Adoption

Growing awareness of preventive pet health, supported by increased veterinary telehealth penetration, is fueling demand for health-monitoring devices. The integration of biometric tracking and diagnostics data into veterinary workflows is a significant market catalyst. Tractive's 2025 partnership with veterinary clinics to integrate tracking data into animal health records exemplifies how the sector is evolving beyond hardware into comprehensive health intelligence platforms. Over 175 countries now have access to Tractive's connected monitoring ecosystem, underscoring global adoption momentum.

Market Restraints

High Product Costs and Limited Consumer Affordability

The premium pricing of advanced pet tech devices remains a significant barrier, particularly in price-sensitive emerging markets. GPS trackers, AI-enabled cameras, and smart health monitors typically retail between US$50 and US$250, with additional recurring subscription fees. This cost structure limits mass-market penetration and skews adoption toward high-income demographics. Supply chain disruptions affect semiconductor availability and further obstruct manufacturers' ability to reduce unit costs, restricting the total addressable market in lower-income regions and among value-oriented consumers.

Data Privacy Concerns and Interoperability Challenges

The collection of sensitive behavioral and location data from connected pet devices is raising growing consumer concerns about data security and third-party use. Absence of standardized IoT protocols across device ecosystems creates interoperability friction, discouraging multi-device adoption. Regulatory scrutiny under frameworks like GDPR in Europe is compelling manufacturers to invest in compliance infrastructure, increasing operational costs. These structural challenges slow enterprise scaling and complicate platform integration with veterinary and insurance data systems.

Opportunities - Expansion of Feline-Focused and Multi-Species Tech Products

Historically, pet tech has been dominated by dog-centric solutions; however, the cat segment is now the fastest-growing pet type, with a 13.3% CAGR, signaling an underserved and commercially viable opportunity. Tractive's April 2026 launch of the CAT 6 Mini, the first collar-integrated GPS and health monitor built for feline physiology, signals a market correction. Developing species-specific wearables, hygiene automation, and health monitors for cats, birds, and small mammals could unlock an incremental addressable market estimated at several billion dollars through 2033.

Emerging Market Penetration in the Asia Pacific

Asia Pacific represents the most dynamic regional growth opportunity, expanding at a 15.4% CAGR through 2033, underpinned by surging pet ownership rates in China, Japan, South Korea, and India. Urbanization, rising disposable incomes, and digital commerce infrastructure are accelerating adoption. China's pet economy exceeded RMB 279 billion (approximately US$ 39 billion) in recent estimates, reflecting structural tailwinds in demand. Local manufacturing cost advantages further enable competitive pricing strategies that can bridge the affordability gap and drive volume growth across mid-tier market segments.

Category-wise Analysis

Product Type Insights

Wearables & trackers are the leading product segment, commanding 26.4% of global revenue share in 2026. Expanding consumer demand for real-time GPS location monitoring and biometric activity data, particularly for dogs in urban environments, underscores the need for trackers. The widespread availability of companion mobile applications, combined with declining hardware costs, has made GPS collars and activity monitors accessible across multiple income brackets, reinforcing this segment's dominant position.

Pet cameras & monitoring systems, featuring AI-enabled cameras and two-way communication, are the fastest-growing sub-segment at 12.9% CAGR. AI-powered behavioral recognition, real-time alert functionality, and remote interaction capabilities are driving adoption among working pet owners seeking continuous oversight.

Technology Type Insights

GPS-based systems lead the technology landscape with 29.4% market share, reflecting the foundational importance of reliable real-time location tracking in the pet tech value proposition. GPS technology's proven reliability in outdoor urban environments, combined with geofencing capabilities and multi-network compatibility, has made it the preferred technology for pet safety applications globally. Consumer trust in GPS accuracy and continuous product innovation by players like Garmin and Tractive reinforces its dominant position.

Connectivity Platforms (App/Cloud-based) represent the fastest-growing technology segment, with a 15.1% CAGR, driven by the convergence of pet health data, veterinary integration, and subscription-based service delivery. Cloud-based platforms enable centralized analytics across multiple devices and pet profiles.

Pet Type Insights

Dogs constitute the dominant pet type, accounting for 58.6% of the global market share. Dog owners represent the most engaged and highest-spending segment of pet tech consumers, driven by high outdoor activity levels that reinforce the utility of GPS trackers, smart collars, and activity monitors. The extensive product ecosystem tailored for canines, supported by strong breed-specific innovation, continues to reinforce this segment's commanding position. Regulatory endorsements from veterinary bodies for wearable health monitoring further validate adoption.

Cats are the fastest-growing pet type segment at 13.3% CAGR, fueled by rising feline adoption globally and a wave of cat-specific product innovation. Tractive's CAT 6 Mini launch in April 2026 exemplifies market response to this underserved opportunity.

Distribution Channel Insights

Online channels dominate distribution, accounting for 58.9% of global market share, driven by e-commerce convenience, broader product assortments, competitive pricing, and direct-to-consumer brand strategies. Digital platforms also facilitate subscription services, firmware updates, and integrated app ecosystems that reinforce customer loyalty. The accelerated shift to online purchasing post-2020 has permanently restructured pet tech retail, with platforms such as Amazon, Chewy, and brand-owned DTC websites leading transaction volumes.

Offline channels, comprising pet specialty stores, veterinary clinics, and supermarkets, are the fastest-growing distribution channel, with a 9.5% CAGR, reflecting the importance of in-person product demonstrations, professional veterinary endorsements, and omnichannel retail strategies.

Regional Market Insights

North America Pet Tech Products Market Insights

North America holds the dominant global share of approximately 41.8% in the Pet Tech Products Market, underpinned by the highest per-capita pet spending globally and a sophisticated innovation ecosystem centered in the U.S. The American Pet Products Association reported record U.S. pet industry expenditures, providing robust commercial demand for advanced tech products. A mature regulatory environment, high smartphone penetration, and strong veterinary telehealth infrastructure accelerate device adoption. The U.S. leads in both GPS-based wearable uptake and AI-powered camera deployment, with North American startups and established players alike investing heavily in subscription-integrated platforms.

Canada reinforces regional strength through high pet ownership rates and increasing digitally connected pet-care spending. Innovation clusters in California and New York remain the primary hubs for pet tech R&D and venture capital activity.

Europe Pet Tech Products Market

Europe accounts for 27.6% of global market share and is expected 11.3% CAGR, with Germany, the U.K., and France serving as the primary demand centers. Stringent GDPR data protection regulations compel manufacturers to implement robust privacy frameworks, raising the compliance bar and creating a competitive moat for established players. The U.K. leads in smart feeding and health monitoring adoption, while Germany demonstrates strong demand for GPS-enabled pet safety solutions.

Spain and France are emerging as high-growth markets, driven by rising urban pet ownership and increased veterinary telehealth accessibility. Regulatory harmonization under EU digital health frameworks is progressively facilitating cross-border device certification, reducing market entry barriers.

Asia Pacific Pet Tech Products Market Insights

Asia Pacific is the fastest-growing regional market at 15.4% CAGR, representing the most significant long-term growth opportunity in the global Pet Tech Products Market. China dominates regional volume, with its rapidly expanding pet economy and a tech-savvy urban consumer base driving strong demand for smart feeders, cameras, and GPS trackers. Japan leads in premium product adoption, supported by high disposable incomes and cultural affinity for advanced consumer electronics. India and ASEAN markets are emerging rapidly on the back of rising pet adoption and expanding e-commerce infrastructure.

Local manufacturing advantages, particularly in China and South Korea, enable competitive pricing and rapid product iteration cycles, supporting export-led growth alongside strong domestic consumption.

Competitive Landscape

Market leaders in the Pet Tech Products space are prioritizing platform-driven innovation over standalone hardware, embedding subscription ecosystems into connected devices to maximize recurring revenues. Differentiation increasingly hinges on AI-enabled health analytics, veterinary data integration, and seamless app experiences. Emerging business model trends include DTC channel expansion, white-label OEM partnerships, and strategic M&A to consolidate user bases and proprietary datasets.

Key Developments:

- In April 2026, Tractive GmbH launched the DOG 6 XL and CAT 6 Mini, the first collar-integrated GPS and health tracker for cats, alongside enhanced app capabilities, expanding its comprehensive pet health intelligence platform to over 175 countries.

- In July 2025, Tractive completed the acquisition of Whistle from Mars Petcare, consolidating Whistle's customer base and connected wearable technology to significantly strengthen Tractive's global market leadership in GPS tracking.

- In November 2024, Traini secured approximately US$ 7.5 million in strategic funding to accelerate AI-driven pet communication and wearable technology development, signaling strong investor confidence in next-generation biometric platforms.

Companies Covered in Pet Tech Products Market

- Garmin International Inc.

- Tractive GmbH

- Whistle Labs Inc

- Petcube Inc

- Mars Petcare (Kinship Division)

- FitBark Inc.

- Sure Petcare

- PetSafe LLC

- PETKIT

- Fi (Fi Smart Collar)

- Furbo

- PetPace LLC

- Dogness International Corporation

- Dogtra Co.

- WOPET

Frequently Asked Questions

The global Pet Tech Products Market is valued at US$ 15.9 Bn in 2026, projected to reach US$ 36.3 Bn by 2033.

Rising pet humanization, AI/IoT integration, and growing demand for real-time remote health monitoring are the primary market growth engines.

The market is projected to grow at a CAGR of 12.5% from 2026 to 2033, accelerating from the 10.1% historical growth rate.

Feline-focused product innovation, subscription-based platform models, and Asia Pacific market penetration represent the most actionable high-growth opportunities.

Leading players include Garmin International, Tractive GmbH, Petcube, Mars Petcare (Kinship), FitBark, PetSafe, PETKIT, Fi, Furbo, and PetPace, among others.