- Biotechnology

- Cell Culture Media and Cell Lines Market

Cell Culture Media and Cell Lines Market Size, Share, and Growth Forecast 2026 - 2033

Cell Culture Media and Cell Lines Market by Product Type (Traditional Cell Lines, Classical Media), Application (Biopharmaceutical Production, Diagnostics), End-user (Large Biopharmaceutical Companies), and Regional Analysis, 2026 - 2033

Cell Culture Media and Cell Lines Market Size and Trends Analysis

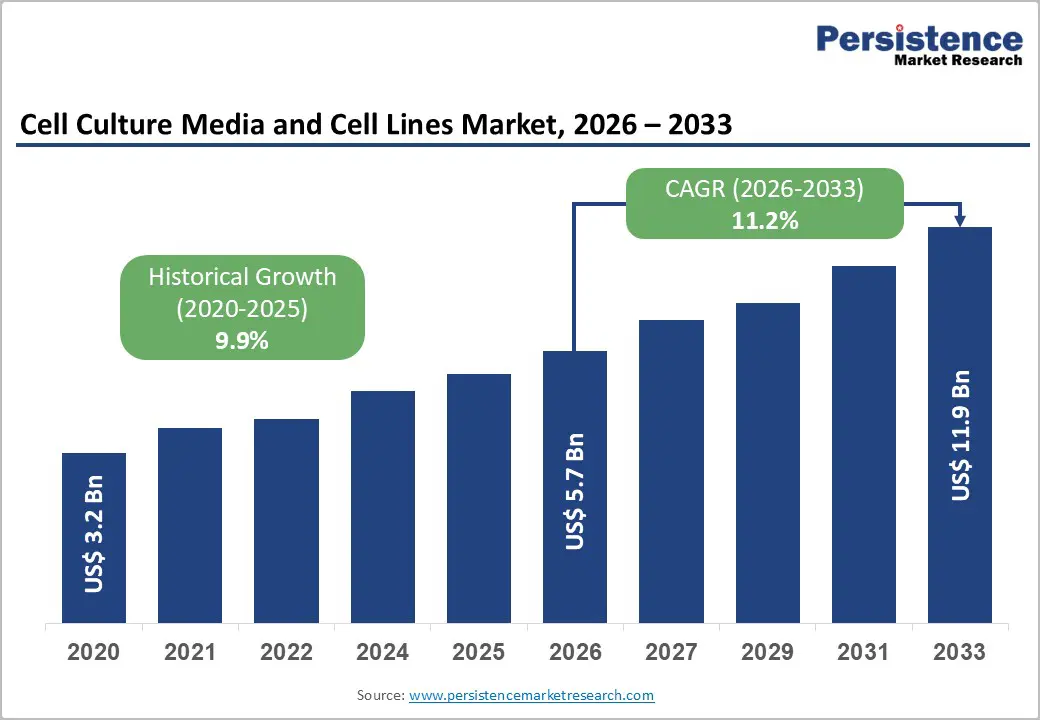

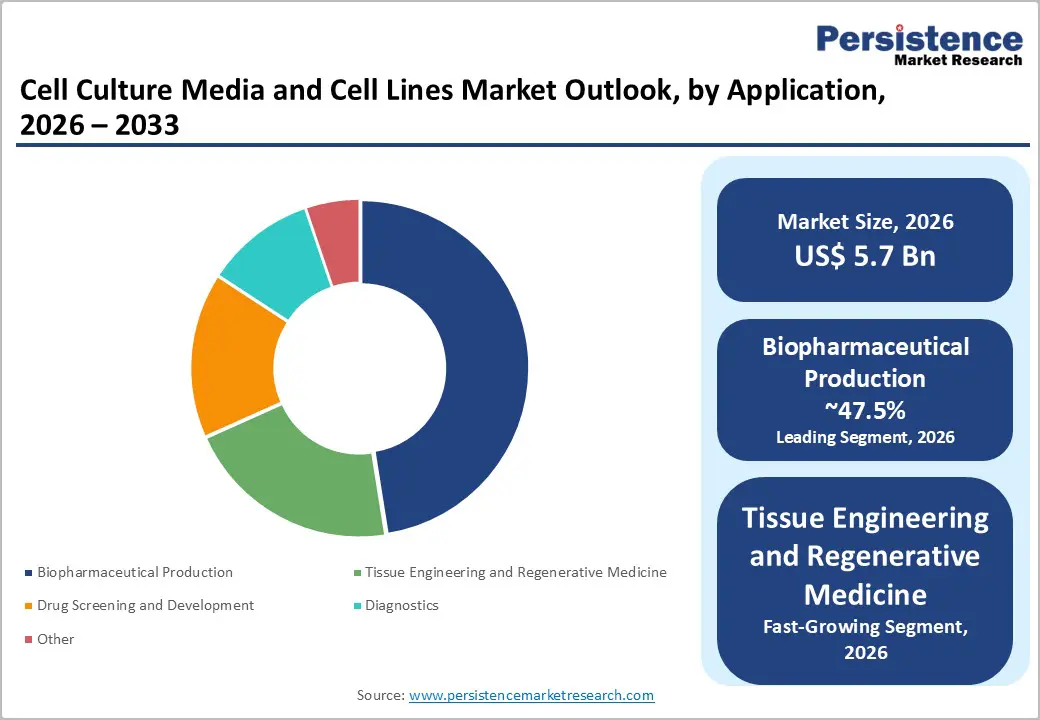

The global cell culture media and cell lines market size is likely to be valued at US$5.7 billion in 2026 and is estimated to reach US$11.9 billion by 2033, growing at a CAGR of 11.2% during the forecast period from 2026 to 2033, driven by rising use of biologics such as monoclonal antibodies and vaccines that depend on cell culture systems. Increasing pipeline of cell and gene therapies, including CAR-T treatments, is also raising the demand for specialized media and high-performance cell lines.

Key Industry Highlights

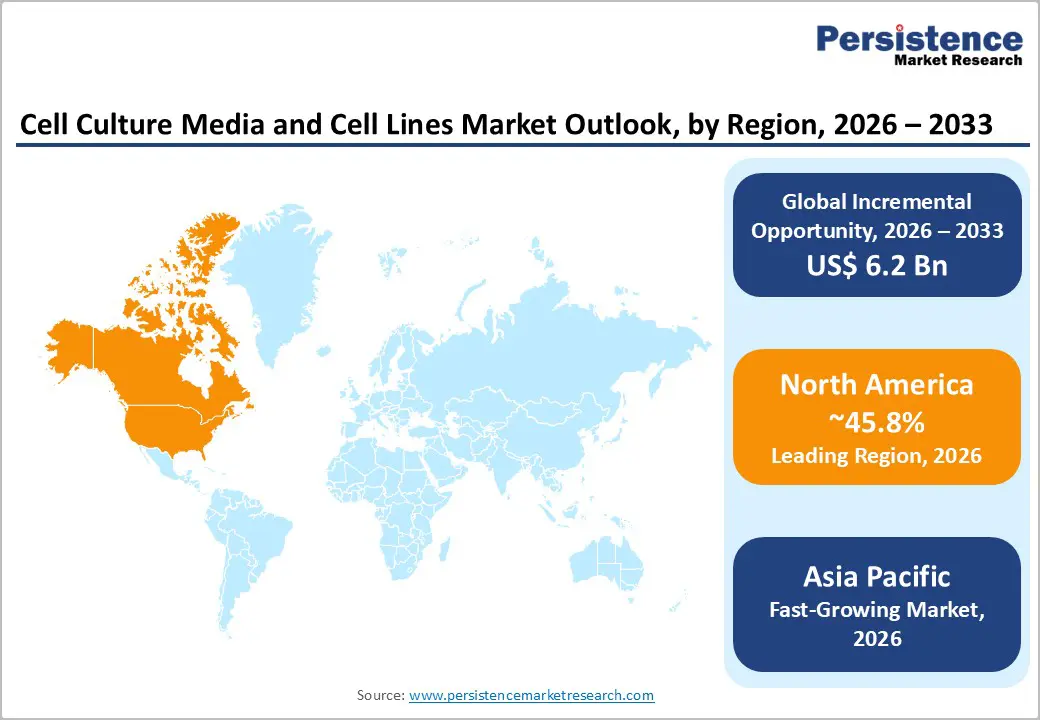

- Leading Region: North America, with about a 45.8% share in 2026, owing to a well-established biologics manufacturing base and a high number of approved cell and gene therapies.

- Fast-growing Region: Asia Pacific, fueled by ongoing expansion in biomanufacturing and government-backed biotech initiatives.

- Leading Product Type: Specialty media products, approximately 44.2% share in 2026, as they provide chemically defined compositions that reduce variability.

- Dominant Application: Biopharmaceutical production, with a nearly 47.5% share in 2026, as most modern drugs require cell-based manufacturing systems.

- Latest Divestiture: In June 2025, FUJIFILM Irvine Scientific completed the divestiture of its Medical Media Business Unit to Astorg. The company noted that the transaction would allow it to concentrate resources on life science markets, particularly cell culture media, bioprocessing, and advanced therapeutic applications.

DRO Analysis

Driver - Cell-Derived Vaccine Manufacturing to Propel Demand

The push to prevent infectious diseases and strengthen pandemic preparedness has prompted a shift toward cell-based vaccine platforms. Unlike egg-based methods, cell-based production allows manufacturers to respond to market needs faster and in shorter production cycles, while also allowing greater surge capacity, greater process control, and a more reliable and well-characterized product. This advantage matters in outbreak scenarios, where egg supply is often the bottleneck.

The performance edge is also documented in real-world data. A 2025 study by CSL Seqirus, published in Infectious Diseases and Therapy, analyzed data from 106,779 vaccinated and influenza-tested patients. It found that cell-based quadrivalent influenza vaccines offered approximately 19.8% greater relative vaccine effectiveness compared to standard egg-based vaccines during the 2023/24 U.S. season. This consistency across multiple seasons and age groups strengthens why cell culture media designed to support vaccine production lines continues to see high procurement.

Biopharmaceuticals and mAb Therapies to Foster Specialized Media Demand

The rise of targeted biologics and biosimilars has made Chinese Hamster Ovary (CHO) cells the dominant production platform in biopharma. As per a 2025 peer-reviewed article published in Frontiers in Bioengineering and Biotechnology, around 70% of therapeutic recombinant proteins are produced using mammalian cells, with CHO being the preferred expression system, especially for mAb production. These cells require precisely balanced culture media to sustain productivity and ensure proper glycosylation, which affects drug safety and efficacy.

Media formulation is not a one-time task, as it requires ongoing optimization for each cell line and target molecule. Proper protein glycosylation, crucial for mAb stability, safety, and efficacy, heavily relies on cell culture conditions. Standardized optimal media/feed combinations necessary for different cell lines are often lacking, necessitating individualized optimization. This demand for customized and high-performance media fuels steady demand across the mAb manufacturing pipeline.

Restraint - Inconsistency in Animal Serum-Supplemented Media

Fetal Bovine Serum (FBS) remains widely used in cell culture, but its undefined composition creates a persistent problem for consistency. There is no standard method to evaluate the potential adverse effects of experiments due to unknown factors in the complex composition of FBS. The ingredients and origins of FBS from different batches and brands are unknown to users, with no recognized standard for cell cultures existing. This undermines reproducibility across labs and manufacturing sites.

GMP-grade FBS undergoes extensive testing for sterility, endotoxins, and viral contaminants. However, unavoidable batch-to-batch variability can still affect reproducibility and increase production costs. Beyond inconsistency, there are safety concerns too. Serum may contain viruses that could affect experimental outcomes or provide a potential health hazard if cultured cells are intended for implantation in humans. These combined risks have made FBS-supplemented media a regulatory and operational liability, pushing manufacturers toward chemically defined alternatives.

Opportunity - Human Plasma-Like Media for Cell Research

Standard cell culture formulations such as Dulbecco's Modified Eagle Medium (DMEM) and Roswell Park Memorial Institute (RPMI) were designed decades ago, based on rodent metabolic requirements. They often contain glucose and glutamine at levels far exceeding what is found in actual human physiology. Human Plasma-Like Medium (HPLM) addresses this gap. HPLM is a synthetic physiologic medium containing over 60 metabolites and small ions at concentrations reflective of adult human plasma.

Studies have shown it improves the structural and metabolic maturation of human pluripotent stem cell-derived cardiomyocytes compared to conventional basal media. This translational accuracy is important in disease research. Standard media such as DMEM contain a non-physiological excess of nutrients, including glucose and glutamine, while being low on uric acid. It is a critical imbalance given that nutrient availability is a prominent regulator of the mTOR signaling pathway. As drug discovery pipelines depend more heavily on human cell models, HPLM-type formulations deliver a meaningful improvement over classical media in capturing how human cells actually behave.

Process-Intensified Media for High-Density Biologics Production

The market’s shift toward perfusion and intensified fed-batch cultures is creating rising demand for media built to sustain extreme cell densities. According to an article by Evotec, as of early 2025, there are over 200 therapeutic mAbs on the market with another 1,400 investigational product candidates in development. The biotherapeutics manufacturing industry has increasingly shifted toward intensified perfusion over fed-batch formats, as it allows significantly higher cell densities and the delivery of higher product mass, reducing the total cost of goods.

Media components play a decisive role here. Poloxamer 188 (P188), a surfactant included in perfusion media, protects cells from mechanical shear stress inside bioreactors. U.S. patent data show that increasing poloxamer-188 concentration from 1.8 g/L to 6.8 g/L in perfusion cultures enabled viable cell densities exceeding 100×10? cells/mL, compared to 50×10? cells/mL in cultures using only the standard concentration. These formulation advances make high-density culture operationally viable and are central to next-generation biologics manufacturing.

Category-wise Analysis

Product Type Insights

Specialty media products are predicted to lead with a share of approximately 44.2% in 2026 as they improve consistency, performance, and regulatory compliance in advanced cell-based workflows. Unlike classical media, specialty media are chemically defined and optimized for specific cell types such as CHO, HEK293, or stem cells. This removes variability caused by serum. The U.S. Food and Drug Administration (FDA) has clearly encouraged the use of serum-free and animal-component-free materials in biologics manufacturing to reduce contamination risks. This shift is visible in industry practice.

Stem cells and blood-derived cells are estimated to be the fastest-growing segment over the forecast period, as they are central to next-generation therapies and precision medicine. These cells are used in CAR-T therapies, stem cell transplants, and gene editing workflows. The National Institutes of Health (NIH) highlights that hematopoietic stem cells remain the backbone of approved cell therapies globally. Blood-derived immune cells, especially T-cells, are widely used in cancer treatments. For instance, CAR-T therapies targeting leukemia rely on patient-derived T-cells expanded in controlled media systems.

Application Insights

The biopharmaceutical production segment is anticipated to dominate with a share of nearly 47.5% in 2026, as most modern drugs are biologics that require cell-based manufacturing. Monoclonal antibodies, vaccines, and recombinant proteins cannot be produced without cell culture systems. The World Health Organization (WHO) reported that biologics play a prominent role in treating cancer, autoimmune diseases, and infectious diseases. CHO cells alone are used in the majority of antibody production pipelines. Companies such as Lonza Group and Cytiva have extended large-scale biomanufacturing facilities since 2024 to meet demand for biologics and biosimilars.

The tissue engineering and regenerative medicine segment is expected to remain in the second position in 2026, as they aim to repair or replace damaged tissues, which traditional drugs cannot do. This field depends heavily on advanced cell culture systems, including 3D culture, organoids, and scaffold-based growth. The National Health Service (NHS) has supported clinical programs using engineered skin and cartilage for patients with severe injuries. These are real-world applications, not early-stage research. A 2025 journal study published in Nature Biotechnology reported successful use of lab-grown organoids for drug testing and disease modeling, reducing reliance on animal testing.

Regional Insights

North America Cell Culture Media and Cell Lines Market Trends

North America is predicted to dominate in 2026 with a share of approximately 45.8%, as it combines high biologics manufacturing capacity with early adoption of advanced cell culture technologies. The region hosts leading players such as Thermo Fisher Scientific and Danaher Corporation, which continuously invest in media innovation and large-scale production. The U.S. Food and Drug Administration (FDA) has approved a high number of biologics and cell-based therapies in recent years, which increases demand for culture media and cell lines.

The NIH also remains one of the largest funders of cell biology and regenerative medicine research. This creates a superior pipeline from lab research to commercial production, which keeps the region ahead.

U.S. Cell Culture Media and Cell Lines Market Trends

A share of nearly 62.3% is expected to be held by the U.S. in 2026, owing to its dominance in cell and gene therapy development and commercialization. The country leads in CAR-T therapies, stem cell trials, and mRNA platforms. According to the CDC, biologics and advanced therapies are expanding in clinical use, especially in oncology and rare diseases. From 2024 to 2025, companies such as Lonza Group and Cytiva expanded U.S.-based manufacturing facilities to meet demand. The U.S. also benefits from high venture funding. Various biotech start-ups are focusing on cell-based therapies, which require specialized media and validated cell lines, propelling steady demand.

Asia Pacific Cell Culture Media and Cell Lines Market Trends

Asia Pacific is anticipated to be the fastest-growing region in 2026 with a share of nearly 29.7%, owing to steady expansion in biomanufacturing and low-cost production capabilities. Governments are actively supporting biotech infrastructure. For example, the Ministry of Economy, Trade and Industry has funded regenerative medicine programs, while South Korea has invested in large biologics clusters. The region is also becoming a preferred outsourcing destination.

Global companies are shifting parts of their production to Asia Pacific due to cost advantages and skilled labor. This has increased demand for cell culture inputs across Contract Manufacturing Organizations (CMOs) and research labs.

China Cell Culture Media and Cell Lines Market Trends

China will likely lead Asia Pacific in 2026 with a share of around 39.6%, due to constant government support and a rising domestic biologics industry. The National Medical Products Administration has accelerated approvals for biologics and biosimilars in recent years. The country’s Made in China 2025 strategy includes biotech as a priority sector. Local companies are extending production of monoclonal antibodies and vaccines. For instance, several local firms have built large CHO-based production facilities since 2023. This expansion increases the demand for high-quality media and cell lines.

India Cell Culture Media and Cell Lines Market Trends

In 2026, India is projected to account for a share of approximately 23.5%, owing to its expanding vaccine and biosimilar production base. The country is home to key vaccine manufacturers and is increasing its focus on biologics. The Department of Biotechnology has launched funding programs to support cell and gene therapy research. India played a prominent role in global vaccine supply during the COVID-19 period, and that infrastructure is now being used for other biologics. Companies are also investing in research and development for monoclonal antibodies and recombinant products. This creates steady demand for culture media, especially cost-effective formulations suited for large-scale production.

Europe Cell Culture Media and Cell Lines Market Trends

Europe will likely see decent growth over the forecast period, with a share of nearly 14.8% in 2026, due to the favorable regulatory support and established research networks. The European Medicines Agency has approved several Advanced Therapy Medicinal Products (ATMPs), which rely on cell culture systems. The region has a well-established biopharma industry and superior academic collaboration. Programs funded by the European Commission are supporting regenerative medicine and cell therapy research. Growth is steady rather than fast as the market is already well-developed, but innovation remains consistent.

Germany Cell Culture Media and Cell Lines Market Trends

Germany will likely register a substantial share of approximately 33.7% in 2026, fueled by its expanding bioprocessing and equipment manufacturing base. Companies such as Sartorius AG play a key role in supplying media, bioreactors, and process solutions. Germany also has an extensive network of research institutes and biotech clusters. Government-backed initiatives are supporting cell therapy and industrial biotechnology. This combination of manufacturing strength and research capability keeps Germany as a key contributor in Europe.

U.K. Cell Culture Media and Cell Lines Market Trends

A share of around 19.2% is predicted to be held by the U.K. in 2026, supported by innovation in cell and gene therapy and rising clinical research activity. NHS has adopted advanced therapies, including CAR-T treatments for cancer patients. The Medicines and Healthcare products Regulatory Agency has also introduced flexible frameworks to speed up approvals for innovative therapies. Initiatives such as the Cell and Gene Therapy Catapult are further helping broaden manufacturing. These factors are predicted to sustain demand for specialized media and cell lines in the next ten years.

Competitive Landscape

The global cell culture media and cell lines market is moderately consolidated, with a handful of multinational life science companies controlling a substantial share of revenue. The competitive landscape is led by Thermo Fisher Scientific, Merck KGaA, Sartorius AG, Danaher (Cytiva), Lonza Group, and FUJIFILM Irvine Scientific. These companies dominate through extensive product portfolios that cover cell culture media, cell lines, bioprocessing technologies, reagents, and manufacturing services.

The market is witnessing rising competition from specialized innovators such as STEMCELL Technologies, ATCC, PromoCell GmbH, and AllCells. These companies focus on high-value applications such as primary cells, stem cell media, immune cell culture, and disease-specific cell models. Their specialized portfolios enable them to compete effectively despite the expansion advantages of large corporations.

Key Industry Developments:

- In February 2026, Sartorius reported continued investment in innovative cell culture technologies, especially organoids, microtissues, and 3D cell models. The company noted that these platforms are becoming increasingly important for drug discovery, disease modeling, and reducing dependence on animal testing, strengthening the industry's shift toward advanced cell-based research systems.

- In January 2026, FUJIFILM Irvine Scientific officially changed its name to FUJIFILM Biosciences. The company stated that the rebranding shows its evolution from a traditional cell culture media supplier into a broad life sciences solutions provider serving customers across discovery, development, and commercial manufacturing.

- In May 2025, NextCell Pharma and FUJIFILM Irvine Scientific announced a strategic collaboration focused on Mesenchymal Stromal Cells (MSCs). The companies combined NextCell’s standardized MSC products with FUJIFILM’s culture media and cryopreservation technologies to provide integrated solutions for researchers and developers working in regenerative medicine and cell therapy.

Companies Covered in Cell Culture Media and Cell Lines Market

- Sartorius AG

- Danaher

- Merck KGaA

- Thermo Fisher Scientific, Inc.

- FUJIFILM Corporation

- Lonza

- STEMCELL Technologies

- PromoCell GmbH

- ATCC

- AllCells

Frequently Asked Questions

The global cell culture media and cell lines market is projected to be valued at US$5.7 billion in 2026.

The cell culture media and cell lines market is expected to reach US$11.9 billion by 2033.

Key market trends include the rising adoption of serum-free media and increasing demand for cell and gene therapies.

Specialty media products are expected to be the leading product type with a share of nearly 44.2% in 2026, as they can be customized for specific cell types.

The cell culture media and cell lines market is expected to grow at a CAGR of 11.2% from 2026 to 2033.

Sartorius AG, Danaher, and Merck KGaA are a few key market players.