- Home Appliances

- Ceiling Tiles Market

Ceiling Tiles Market Size, Share, and Growth Forecast 2026 - 2033

Ceiling Tiles Market by Material Type (Mineral Fiber, Gypsum, Metal, Plastic, Wood & Engineered Wood, Others), Installation Type (Suspended Ceiling Systems, Surface-Mounted Ceiling Systems), Design (Plain, Laminated, Fissured, Patterned, Textured, Coffered), Property Type (Acoustic, Non-Acoustic), Application (Residential, Commercial, Industrial, Institutional, Hospitality), by Regional Analysis, 2026 - 2033

Ceiling Tiles Market Size and Trend Analysis

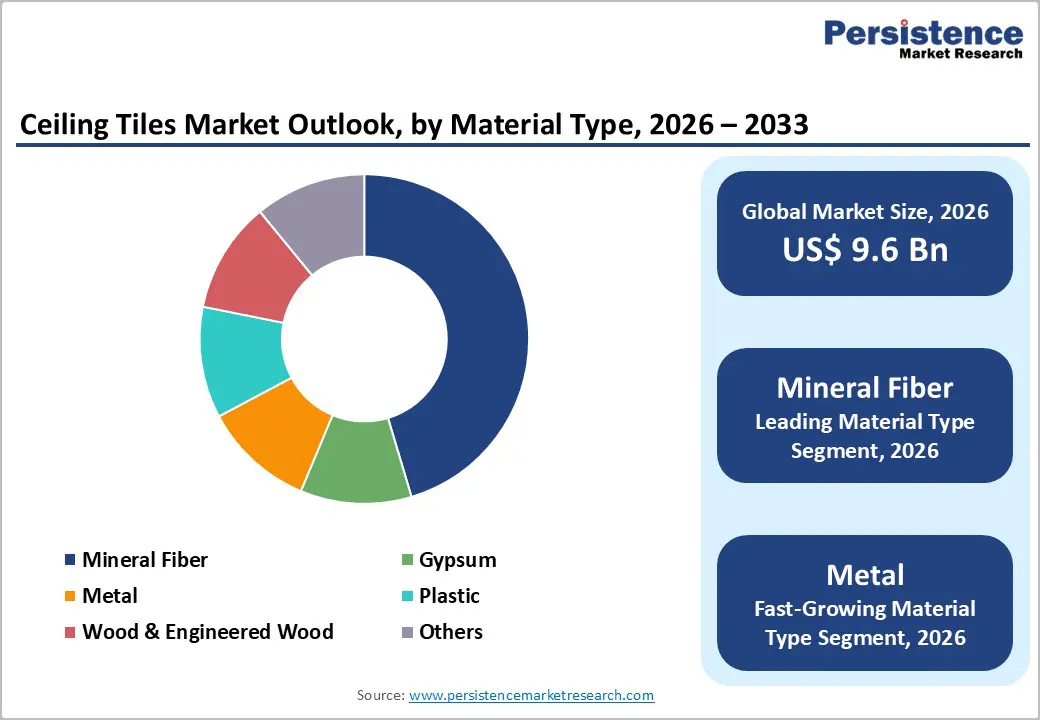

The global ceiling tiles market size is expected to be valued at US$ 9.6 billion in 2026 and projected to reach US$ 15.4 billion by 2033, growing at a CAGR of 7.0% between 2026 and 2033.

The ceiling tiles market is experiencing robust expansion, underpinned by surging global construction activity, rising demand for energy-efficient building systems, and heightened regulatory focus on indoor acoustic comfort. Rapid urbanization across the Asia Pacific and Middle East & Africa, combined with large-scale commercial real estate development in North America and Europe, is reinforcing product adoption. According to the United Nations, approximately 68% of the global population is expected to live in urban areas by 2050, significantly driving demand for structured interior ceiling solutions in residential, commercial, and institutional settings.

Key Industry Highlights

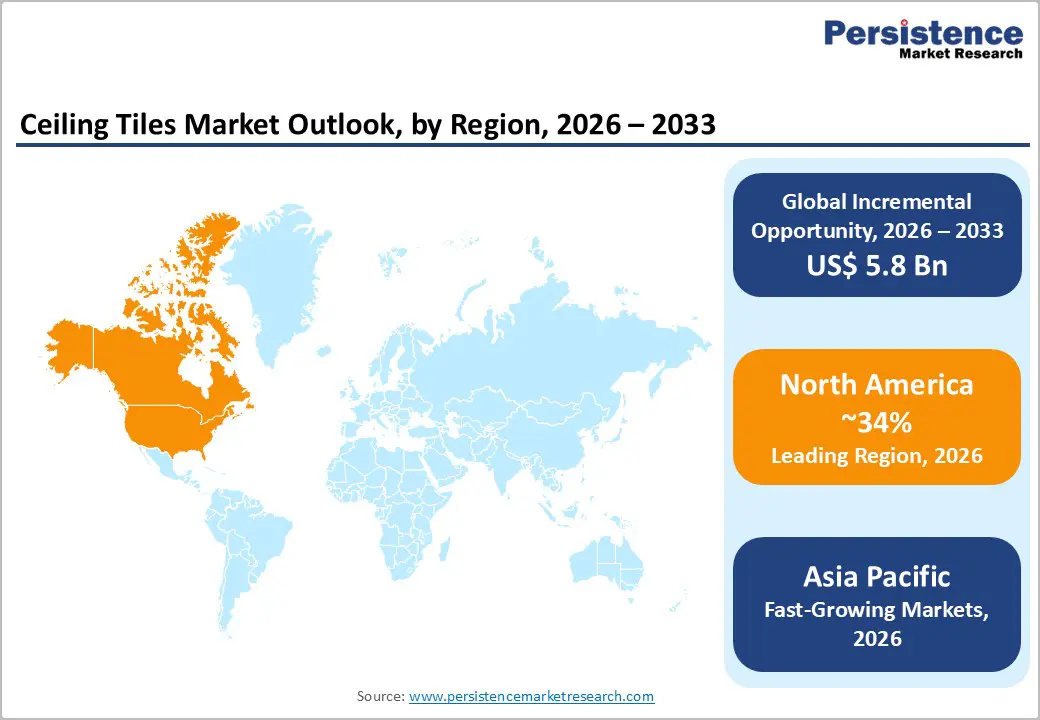

- Leading Region: North America leads the global ceiling tiles market with approximately 34% market share in 2025, underpinned by high commercial construction activity, stringent building codes, and mature renovation markets in the U.S. and Canada.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, driven by rapid urbanization in China and India, smart city initiatives, and surging commercial real estate investment across ASEAN economies.

- Dominant Segment: Mineral fiber ceiling tiles dominate with approximately 44% market share in 2025, owing to superior acoustic performance, fire compliance, and cost-competitiveness across commercial and institutional applications worldwide.

- Fastest Growing Segment: Metal ceiling tiles are emerging as the fastest growing segment through 2033, driven by their durability, modern aesthetic appeal, and suitability for high-humidity environments in hospitality, healthcare, and industrial facilities.

- Key Opportunity: Integrating IoT sensors, LED lighting, and HVAC modules into ceiling tiles represents a high-value growth opportunity as smart building adoption accelerates across commercial real estate globally through 2033.

| Key Insights | Details |

|---|---|

| Ceiling Tiles Market Size (2026E) | US$ 9.6 Billion |

| Market Value Forecast (2033F) | US$ 15.4 Billion |

| Projected Growth CAGR through 2033 | 7.0% |

| Historical Market Growth (2020 - 2025) | 5.5% |

Market Dynamics

Drivers - Rising Construction Activity and Green Building Mandates

The global construction sector is undergoing a significant transformation, with governments worldwide channeling investments into sustainable infrastructure. The U.S. Infrastructure Investment and Jobs Act allocated US$ 1.2 trillion for public infrastructure, directly boosting demand for interior construction materials, including ceiling tiles. Simultaneously, green building certification systems such as LEED (Leadership in Energy and Environmental Design) and BREEAM have made acoustic and energy-efficient ceiling solutions standard requirements for commercial projects. According to the U.S. Green Building Council, LEED-certified building space surpassed 10.5 billion square feet globally, and ceiling tiles play a critical role in achieving thermal, acoustic, and indoor air quality credits. This regulatory tailwind is positively reinforcing market momentum across commercial and institutional applications.

Surge in Commercial Real Estate and Renovation Activities

Post-pandemic recovery has ignited a global wave of commercial real estate development and interior refurbishment, directly benefiting the ceiling tiles market. The International Monetary Fund (IMF) projected global GDP growth of 3.2% in 2024, which should enable construction spending to rebound. Office redesign trends, including collaborative workspaces, healthcare facility expansions, and hospitality sector renovations, are driving sustained product demand. In Europe, the European Commission's Renovation Wave Strategy aims to double annual renovation rates by 2030, targeting 35 million buildings for energy-efficient upgrades. This initiative disproportionately benefits acoustic and thermally insulating ceiling tile products, making renovation-driven demand a key structural growth driver for the foreseeable future.

Restraints - Volatile Raw Material Prices and Supply Chain Disruptions

The ceiling tiles industry is acutely exposed to raw material price volatility, particularly for mineral wool, gypsum, and metal substrates. Global mineral wool prices spiked by approximately 18-22% between 2021 and 2023, driven by energy-intensive manufacturing processes and rising natural gas prices in Europe. The World Bank Commodity Markets Outlook highlighted sustained inflationary pressures on construction materials through 2024, compressing manufacturer margins and making pricing strategies challenging. These cost escalations often deter small-scale contractors and builders from specifying premium ceiling tile products, thereby limiting product penetration in price-sensitive emerging markets.

Environmental Regulations on Volatile Organic Compound (VOC) Emissions

Stringent environmental regulations governing Volatile Organic Compound (VOC) emissions present a significant compliance burden for ceiling tile manufacturers. The U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) have progressively tightened permissible VOC limits in building materials. Manufacturers using conventional adhesives and coatings face costly reformulation requirements, R&D expenditures, and potential product line discontinuities. These regulatory constraints particularly affect plastic and laminated ceiling tile producers, inflating their production costs and creating barriers for market expansion in regulated economies.

Opportunities - Expansion of Smart and Integrated Ceiling Systems

The emergence of smart building technologies is creating a compelling opportunity for ceiling tile manufacturers to integrate lighting, acoustics, HVAC systems, and IoT-enabled sensors into ceiling modules. The global smart building market, valued at about US$ 100 billion, is expected to expand substantially through the decade. Integrated ceiling systems that accommodate LED lighting panels, wireless connectivity, and air diffusion elements are commanding premium price points in commercial construction. Leading manufacturers such as Armstrong World Industries and Hunter Douglas have already launched modular integrated ceiling platforms. As enterprises increasingly prioritize occupant wellness and operational efficiency, the addressable market for smart-enabled ceiling solutions is poised to expand significantly, offering high-margin growth avenues for innovative market participants.

Rising Demand for Acoustic Solutions in Educational and Healthcare Sectors

Growing awareness of noise pollution's adverse effects on cognitive performance and patient recovery has driven a sharp increase in the adoption of acoustic ceiling tiles across the education and healthcare sectors. The World Health Organization (WHO) has identified excessive noise as a significant public health concern, prompting institutional planners to prioritize acoustic performance in interior design specifications. The American National Standards Institute (ANSI) Standard S12.60 mandates specific classroom acoustic performance criteria, driving adoption of high-NRC (Noise Reduction Coefficient) ceiling tiles in school construction and renovation projects. With global healthcare capital expenditure continuing to rise, the OECD estimates health spending represents over 8.8% of GDP across developed nations, the institutional demand pipeline for acoustic ceiling solutions presents a robust and durable growth opportunity.

Category-wise Analysis

Material Type Insights

Mineral fiber ceiling tiles represent the leading segment within the material type category, commanding approximately 44% of the global ceiling tiles market share in 2025. This dominance is attributable to mineral fiber's superior acoustic performance, cost-effectiveness, and compliance with fire safety standards such as ASTM E1264 and EN 13964. Mineral fiber tiles, composed primarily of natural and recycled wool fibers, slag wool, and perlite, deliver Noise Reduction Coefficients (NRC) of up to 0.95, making them the preferred specification in office spaces, educational institutions, and healthcare facilities. Their compatibility with suspended ceiling grid systems, ease of installation, and lower lifecycle costs further reinforce their market leadership. Major manufacturers, including Armstrong World Industries, Rockfon, and Knauf Ceiling Solutions, maintain broad product portfolios in this material category.

Installation Type Insights

Suspended ceiling systems constitute the leading segment in the installation type category, accounting for approximately 71% of total market share in 2025. Also known as drop ceilings or T-bar grid systems, suspended ceiling systems offer significant practical advantages, including concealment of mechanical, electrical, and plumbing (MEP) infrastructure while enabling easy access for maintenance. The system's modular nature allows rapid tile replacement without disrupting adjacent ceiling areas, significantly reducing renovation costs. ASHRAE guidelines for commercial HVAC integration frequently reference suspended ceiling plenums as efficient air distribution conduits, further entrenching this installation format in commercial construction. The growing prevalence of open-plan offices, large retail environments, and hospital builds, all of which require adaptable, serviceable ceiling systems, has cemented suspended systems' market dominance worldwide.

Design Insights

Within the design category, plain ceiling tiles hold the highest market share, accounting for approximately 36% of the global ceiling tiles market in 2025. Plain ceiling tiles are favored for their versatility, compatibility with diverse interior design aesthetics, and ease of large-scale manufacturing. Their adoption is particularly strong across commercial office spaces, educational institutions, and industrial facilities, where functional performance takes precedence over decorative expression. Plain tiles serve as ideal substrates for integrated lighting, HVAC diffusers, and sprinkler systems, reinforcing their universal adoption across project types. Armstrong World Industries and USG Corporation report that plain tiles constitute the majority of volume sales in their commercial ceiling portfolios. Standardized specifications and competitive pricing further sustain the segment's dominant market positioning.

Property Type Insights

Acoustic ceiling tiles represent the dominant segment in the property type category, holding approximately 62% market share in 2025. The superior market position of acoustic tiles is driven by increasing regulatory requirements around indoor noise levels in commercial, healthcare, and educational settings. Acoustic ceiling tiles with high Noise Reduction Coefficient (NRC) and Ceiling Attenuation Class (CAC) ratings are mandated under international standards, including ISO 11654 and ANSI/ASA S12.60. The World Health Organization estimates that chronic noise exposure affects over 1.1 billion people globally, making acoustic mitigation an architectural priority in building design. Rapid growth in the healthcare, corporate office, and education verticals, all high-priority acoustic environments, is sustaining strong, consistent demand for acoustic ceiling tiles worldwide.

Application Insights

The commercial application segment leads the ceiling tiles market, accounting for approximately 41% of total demand in 2025. Commercial spaces, including office buildings, retail outlets, shopping malls, and corporate campuses, are primary consumers of ceiling tiles due to their large floor areas, stringent acoustic requirements, and aesthetic demands. According to the CBRE Global Real Estate Outlook, global commercial real estate investment reached approximately US$ 830 billion in 2023, underscoring the continued vibrancy of office and retail construction. Demand for ceiling tiles in this segment is reinforced by frequent renovation cycles, strict fire-safety codes such as NFPA 101, and the growing emphasis on workplace wellness standards that promote better acoustics, air quality, and lighting in office interiors. Armstrong World Industries and USG Corporation derive the majority of their revenues from commercial ceiling tile sales.

Regional Insights

North America Ceiling Tiles Market Trends and Insights

North America holds the leading position in the global ceiling tiles market, accounting for approximately 34% of the total share in 2025. The United States is the primary contributor, driven by a highly active commercial construction sector, advanced building codes, and a mature renovation market. The U.S. Census Bureau reported construction spending exceeding US$ 2.0 trillion in 2023, with commercial and institutional segments comprising a substantial portion. The Americans with Disabilities Act (ADA) and ANSI acoustic standards mandate minimum ceiling performance specifications in public buildings, compelling consistent demand for compliant ceiling tile products.

The United States also serves as a critical innovation hub for smart ceiling systems, with companies such as Armstrong World Industries, headquartered in Lancaster, Pennsylvania, and USG Corporation leading product development in integrated acoustic-lighting modules. Canada's National Building Code revisions emphasizing energy performance and indoor environmental quality are further expanding the addressable market. The region's well-established distribution infrastructure and design-build contractor ecosystem strongly support the continued growth of ceiling tile adoption.

Europe Ceiling Tiles Market Trends and Insights

Europe represents the second-largest regional market for ceiling tiles, with Germany, the United Kingdom, France, and Scandinavia as key demand centers. The European Commission's Energy Performance of Buildings Directive (EPBD) mandates substantial energy efficiency improvements across the existing building stock by 2030, driving renovation activity that incorporates energy-efficient ceiling solutions. Germany's Gebäudeenergiegesetz (GEG) building energy law has further accelerated the adoption of thermally and acoustically superior ceiling products in both new construction and retrofit projects.

The Nordic countries, particularly Sweden and Denmark, are at the forefront of sustainable construction, with companies like Ecophon and Rockfon manufacturing glass wool and stone wool acoustic tiles that meet ISO 14001 environmental management standards. The EU Taxonomy for Sustainable Activities is increasingly influencing procurement decisions in the construction sector, steering specifiers toward low-carbon, recyclable ceiling tile materials. Harmonized product standards under EN 13964 facilitate cross-border trade and product certification across the EU single market, supporting regional market cohesion.

Asia Pacific Ceiling Tiles Market Trends and Insights

Asia Pacific is the fastest-growing regional market for ceiling tiles, propelled by unprecedented urbanization, rapidly expanding commercial real estate sectors, and large-scale government infrastructure programs. China dominates regional demand, with the country's urban population exceeding 900 million people and ongoing construction of commercial hubs, airports, and transit facilities. India's Smart Cities Mission, targeting 100 smart cities across the country, incorporates modern building specifications that include acoustic and sustainable ceiling systems for public buildings.

Japan's ceiling tile market is driven by seismic safety regulations, with DAIKEN Corporation emerging as a key domestic manufacturer meeting stringent earthquake-resistant ceiling system standards under Japan's Building Standards Act. ASEAN economies, including Vietnam, Indonesia, and Malaysia are witnessing exponential growth in hospitality and institutional construction, generating strong demand for decorative and acoustic ceiling tiles. The region's manufacturing cost advantages have also attracted global ceiling tile manufacturers to establish local production facilities, improving product accessibility and price competitiveness across the Asia Pacific market.

Competitive Landscape

The global ceiling tiles market displays a moderately consolidated structure, where a limited number of large multinational manufacturers account for a substantial share of global supply while several regional producers compete in localized construction markets. Leading suppliers maintain strong positions through extensive product portfolios, established distribution networks, and long-standing relationships with contractors, architects, and building solution providers across commercial and institutional construction sectors.

Competitive strategies increasingly focus on product innovation, particularly in improving acoustic performance, fire resistance, and environmental sustainability. Manufacturers are investing in materials with low volatile organic compound (VOC) emissions, higher recycled content, and compatibility with green building certification standards. Strategic expansions into emerging construction markets and collaborations with building system integrators are also shaping competition. Additionally, companies are introducing service-oriented business models such as ceiling lifecycle management and recycling or take-back programs that support circular economy goals. These approaches not only strengthen sustainability credentials but also help manufacturers build long-term customer relationships and differentiate their offerings in a competitive global construction materials market.

Key Developments

- March 2025: Armstrong World Industries launched its next-generation Sustain ceiling tile collection, incorporating 90% recycled content, aligned with its net-zero carbon commitment under the Science Based Targets initiative (SBTi).

- October 2024: Saint-Gobain announced a strategic capacity expansion of its Gyproc ceiling tile manufacturing facility in India, targeting surging commercial construction demand across South and Southeast Asia.

- June 2024: Rockfon (a subsidiary of ROCKWOOL International) introduced its Blanka Bas stone wool acoustic ceiling line, achieving Class A fire resistance and an NRC of 1.0, targeting the healthcare and education verticals in Europe.

Companies Covered in Ceiling Tiles Market

- Armstrong World Industries

- USG Corporation

- Knauf Ceiling Solutions

- Saint-Gobain

- Rockfon

- CertainTeed

- Ecophon

- Burgess CEP

- Hunter Douglas

- DAIKEN Corporation

- OWA Ceiling Systems

- Techno Ceiling Products

- SAS International

- Lindner Group

- Ceilume

- ROCKWOOL International

- AWI Licensing LLC

- Chicago Metallic Corporation

Frequently Asked Questions

The global ceiling tiles market is estimated to reach US$ 9.6 billion in 2026, supported by rising commercial construction, renovation activities, and increasing demand for acoustic ceiling solutions.

Key demand drivers include rapid urbanization, increasing construction spending, stricter acoustic and energy-efficient building standards, and growing adoption of green building practices.

North America leads the ceiling tiles market, supported by strong commercial infrastructure development, active renovation cycles, and well-established building regulations.

A major opportunity lies in smart ceiling systems integrating IoT sensors, lighting, and HVAC components to support intelligent building infrastructure.

Key players include Armstrong World Industries, USG Corporation, Saint-Gobain, Knauf Ceiling Solutions, Rockfon, CertainTeed, Ecophon, Hunter Douglas, DAIKEN Corporation, OWA Ceiling Systems, SAS International, Lindner Group, Burgess CEP, Techno Ceiling Products, and Ceilume.