- Display Technologies

- Smart Home Solutions Market

Smart Home Solutions Market Size, Share, and Growth Forecast, 2025 - 2032

Smart Home Solutions Market by Material (Villas/Bungalows, Apartments and Others), by Component (Hardware, Software and Services), by Application (New Construction and Retrofit), and Regional Analysis for 2025 - 2032

Smart Home Solutions Market Size and Trends Analysis

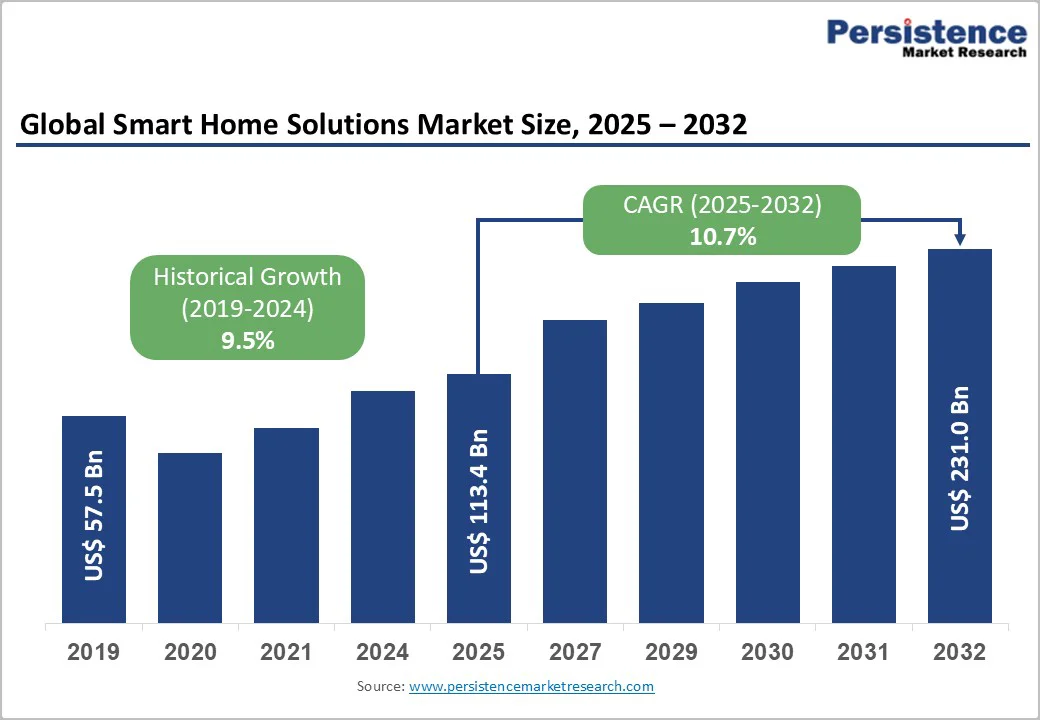

The global smart home solutions market size was valued at US$113.4 billion in 2025 and is projected to reach US$231.0 billion by 2032, growing at a CAGR of 10.7% between 2025 and 2032.

This robust expansion reflects accelerating IoT device proliferation, reaching 21.1 billion connected devices globally in 2025 with 14% annual growth, household penetration at 77.6%, driven by voice assistant adoption across Amazon Alexa and Google Assistant platforms, and energy efficiency imperatives reducing utility costs by 20% through automated climate control and smart lighting.

Key Industry?Highlights:

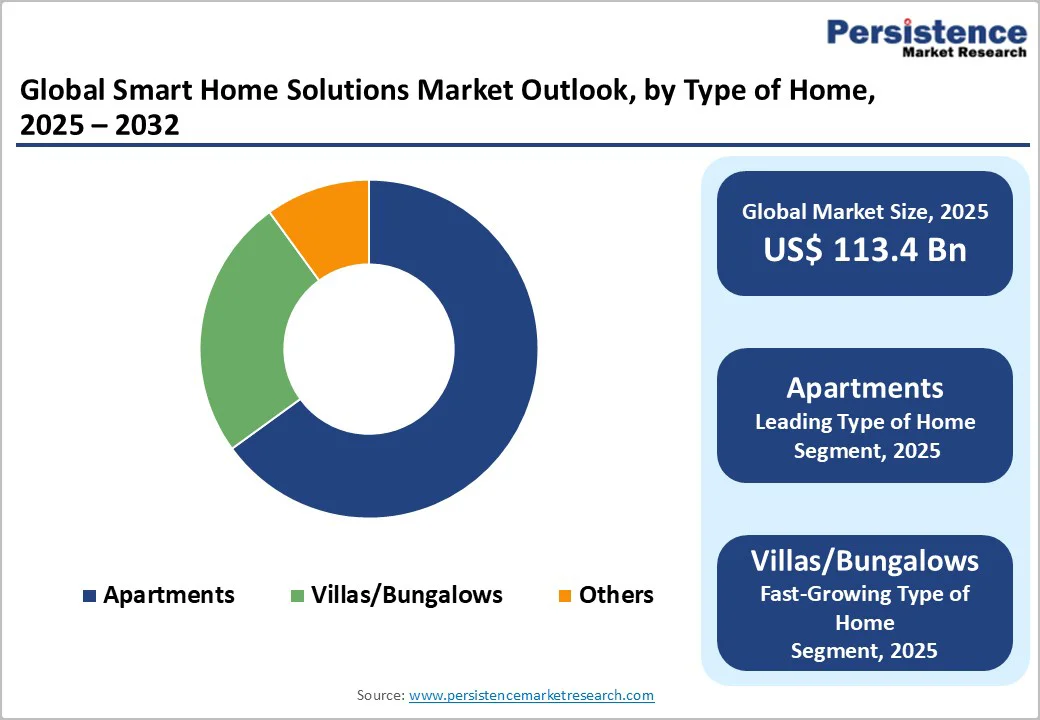

- Property Type Segmentation Leadership: Apartments dominate with 48.3% market share, supported by high urban density, tech-savvy consumers, and strong adoption of connected home devices in multi-dwelling units. Villas and bungalows are the fastest-growing segment, expanding at a 12% CAGR, driven by larger comprehensive automation budgets (US$8,000-25000 per home) and increasing demand for whole-home integrated solutions.

- Component Dynamics: Hardware leads with 42.2% share, reflecting continued dominance of device procurement, including smart speakers, sensors, hubs, and security systems. Software is the fastest-growing component segment, with a 12-15% CAGR, driven by AI-enabled automation, rising adoption of cloud-based analytics, and subscription services priced at US$15-40 per month.

- Application Market Trends: Retrofit installations dominate with 67.3% share, serving the world’s 1.2 billion existing homes seeking incremental smart upgrades. New construction is the fastest-growing segment, with a 14-18% CAGR, supported by builder partnerships that enable 40-60% installation cost savings and rising demand for “smart-ready” homes, which command 3-5% price premiums.

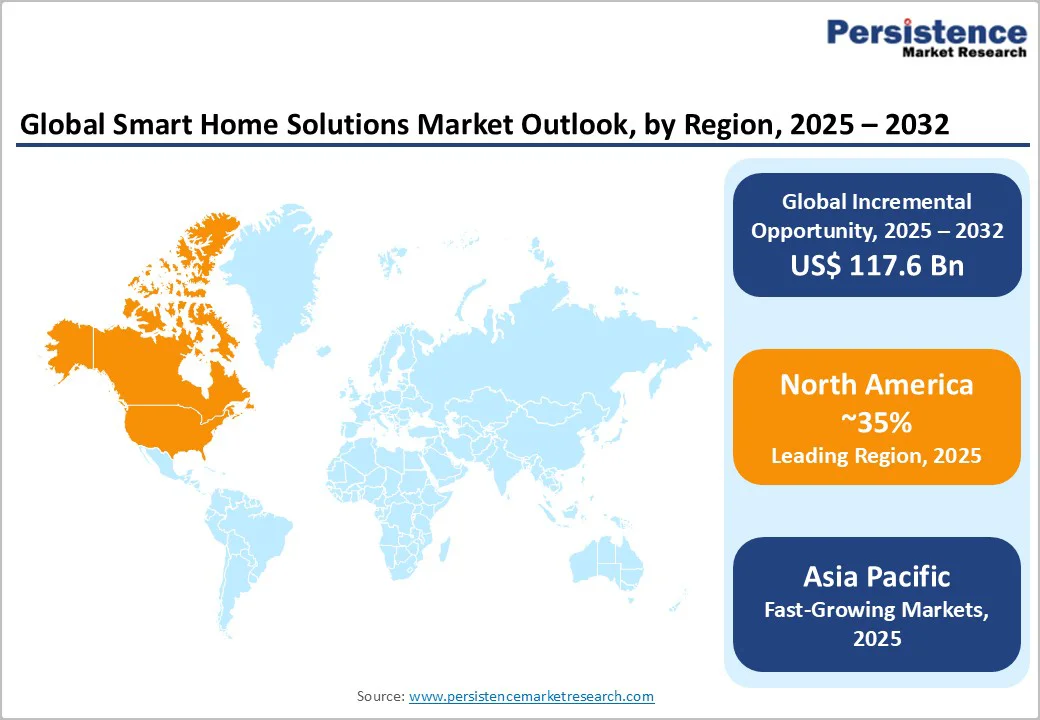

- Regional Growth Patterns: North America leads with a 35% global share, a 9.8% CAGR, driven by technology leadership and a US$43 billion U.S. smart home market. Asia Pacific is the fastest-growing region, with a 28% CAGR, led by China (40% regional share) and India (25% CAGR), supported by rapid urbanization and expanding middle-income households.

- Strategic Market Developments: Amazon dominates with 28% share through its Alexa ecosystem, while Google (24%), Apple (12%), and Samsung (12%) maintain strong competitive positions. Industry-wide adoption of the Matter standard is accelerating cross-platform interoperability, while emerging markets represent a US$45 billion opportunity by 2032, driven by affordable, localized smart-home solutions.

| Global Market Attributes | Key Insights |

|---|---|

| Smart Home Solutions Market Size (2025E) | US$113.4 Bn |

| Market Value Forecast (2032F) | US$231.0 Bn |

| Projected Growth (CAGR 2025 to 2032) | 10.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 9.5% |

Market Dynamics

Growth Drivers

Internet of Things (IoT) Proliferation and Connected Device Ecosystem Expansion

Global IoT device deployment is reaching 21.1 billion connected units in 2025, with 14% year-over-year growth, creating a foundational infrastructure for comprehensive smart home automation. Connected home devices represent 30-35% of the total IoT ecosystem, supporting lighting, security, climate control, and entertainment integration.

Smart speaker penetration, achieving 35-40% household adoption through Amazon Echo, Google Nest, and Apple HomePod platforms, establishes voice control as a mainstream interface, with 200+ million smart speakers deployed globally, enabling natural language interaction for device management, information retrieval, and entertainment control.

AI-powered voice assistants, including Amazon Alexa, Google Assistant, and Apple Siri, supporting 10,000+ third-party integrations (called "skills" or "actions") enable comprehensive ecosystem control where a single voice command manages multiple devices through automated routines (e.g., "Good morning" activating lights, adjusting thermostat, brewing coffee, reading news).

Energy Efficiency Regulations and Consumer Cost Reduction Imperatives

Rising residential energy costs, with average U.S. household electricity spending exceeding $1,500 annually, create a compelling economic case for smart home automation, which can achieve 20-30% energy cost reduction through intelligent climate control, automated lighting management, and appliance scheduling optimization.

Smart thermostats, including Nest, Ecobee, and Honeywell, achieve 10-23% heating and 15% cooling energy savings through learning algorithms that adapt to occupancy patterns, weather forecasts, and user preferences. They create a measurable ROI with $180-350 annual savings, justifying $150-250 device cost within 12-18 months.

Automated lighting systems using occupancy sensors, daylight harvesting, and scheduled dimming reduce lighting energy consumption by 30-50%. LED smart bulbs consume 75% less energy than incandescent equivalents and provide color tuning, brightness control, and integration with home automation platforms.

Market Restraints

High Initial Investment and Installation Complexity

A comprehensive smart home system deployment commanding an initial investment of $3,000-15,000, including devices, professional installation, and network infrastructure, creates a substantial financial barrier that constrains adoption, particularly among price-sensitive demographics and in emerging markets.

Professional installation services, adding $500-2,000 cost for structured wiring, device mounting, system configuration, and network optimization, create complexity deterring DIY-oriented consumers, while retrofit installations facing existing home constraints including limited electrical circuits, inadequate network coverage, and structural modifications elevate installation complexity and costs 30-50% versus new construction deployments.

Interoperability challenges among competing smart home ecosystems (Amazon Alexa, Google Home, Apple HomeKit), requiring consumers to select a primary platform before device purchases, create vendor lock-in concerns and limit flexibility, with cross-platform compatibility remaining limited despite the emerging Matter standard attempting a unified protocol.

Privacy Concerns and Cybersecurity Vulnerabilities

Smart home devices collecting extensive personal data, including occupancy patterns, voice recordings, video surveillance footage, and usage behaviors, create privacy concerns, with 60-70% of consumers expressing discomfort regarding data collection practices and 40-50% citing privacy as the primary adoption barrier.

Cybersecurity vulnerabilities affecting IoT devices through firmware exploits, weak default passwords, and unpatched security flaws create hacking risks, with Mirai botnet demonstrating IoT device compromise potential affecting 600,000+ devices and enabling distributed denial-of-service attacks disrupting major internet services.

Data breach incidents affecting major smart home providers, including Ring camera footage exposure and Google Nest microphone vulnerability revelations, erode consumer trust and create regulatory scrutiny, with GDPR and California Consumer Privacy Act (CCPA) imposing stringent data protection requirements and substantial penalties for non-compliance.

Market Opportunities

Emerging Market Urbanization and Middle-Class Expansion

Asia Pacific middle class expansion reaching 3.5+ billion population by 2030, with rising disposable incomes, creates a substantial addressable market for smart home solutions, particularly in China, India, and ASEAN nations experiencing rapid urbanization and technology adoption.

India's smart home market is projected to grow at a 25-30% CAGR, driven by government Digital India initiatives, increasing internet penetration reaching 900+ million users, and a rising affluent urban population seeking modern lifestyle amenities, creating an estimated $8-12 billion opportunity by 2032.

China's smart city initiatives, supported by government investment and technology giants Alibaba, Tencent, and Baidu, are developing comprehensive smart home ecosystems, creating a favorable regulatory environment and established distribution channels that support rapid adoption. The Chinese smart home market is projected to reach $25-35 billion by 2032.

Affordable smart device proliferation through local manufacturers offering $10-30 smart plugs, $25-60 smart bulbs, and $80-150 smart speakers (versus $100-300 international brand equivalents) democratizes smart home access for middle-income consumers and accelerates mainstream adoption.

New Construction Integration and Developer Pre-Installation

New residential construction offering optimal smart home deployment opportunity through pre-wiring structured cabling, centralized control panels, and integrated system design eliminates retrofit complexity while reducing installation costs by 40-60% creating a developer differentiation opportunity.

Builder partnerships enabling bulk procurement discounts (30-50% below retail pricing) and streamlined installation through specialized contractors create economic viability for standard smart home fitment in new construction, with premium developments incorporating $8,000-20,000 smart home packages as standard amenities.

ABB-free@home system deployment across 400+ new construction homes in the UK, demonstrating a scalable integration model combining a hardwired backbone with wireless expansion flexibility, completing installation within standard construction timelines without schedule disruption.

Modular smart home architectures enabling future expansion without costly rewiring create a future-proof value proposition justifying initial investment, with systems supporting incremental device additions as homeowner needs evolve and technology advances.

Segmentation Analysis

Property Type Analysis

Apartments hold a 48.3% market share due to their large presence in urban markets, younger tech-savvy residents, and strong compatibility with wireless retrofit systems that require minimal structural changes. Multi-dwelling units benefit from centralized high-speed internet, integrated security, and builder partnerships that enable bulk installation of smart devices. Urban apartment residents also display higher adoption of energy-efficient and security-focused technologies, supporting strong demand.

Villas and bungalows are the fastest-growing segment, with a ~12% CAGR, driven by affluent homeowners investing in comprehensive automation. Larger property footprints support advanced systems such as whole-home lighting, shading, audio, and security. Higher budgets (US$8,000-25,000) and long-term ownership enhance ROI through efficiency gains and property value uplift.

Component Analysis

Hardware components hold 42.2% market share, as they form the core of smart home systems, including speakers, thermostats, lighting, locks, cameras, and sensors, which account for most upfront costs. Growing device specialization-such as video doorbells (US$120-250), smart locks (US$150-300), and cameras (US$50-300)-boosts hardware revenue, while 4-7-year replacement cycles ensure recurring demand.

Software is the fastest-growing segment, with a 12-15% CAGR, driven by AI-enabled automation, cloud analytics, and feature upgrades via over-the-air updates. Subscription services generate recurring monthly revenue of US$15-40 per household through professional monitoring, cloud storage, and premium automation. Continuous AI-driven enhancements deliver predictive and personalized automation, strengtheningthe software’s long-term value and premium positioning.

Application Analysis

Retrofit installations dominate due to the massive base of 1.2 billion existing residential units compared with only 15-20 million new homes built annually. Wireless technologies enable easy, low-cost adoption without rewiring, while plug-and-play devices using standard power outlets and Wi-Fi support widespread DIY installation. A modular upgrade path allows households to begin with a single device, such as a smart speaker or thermostat, and expand gradually, lowering upfront commitment and accelerating adoption.

New construction is the fastest-growing segment, with a ~14% CAGR, supported by builder partnerships and lower installation costs from pre-wiring during construction. Smart-ready homes gain 3-5% valuation premiums, while structured wiring enables robust hybrid architectures that combine hardwired reliability with wireless flexibility.

Regional Market Insights

North America

North America generates approximately US$40.6 billion market value in 2025 representing 30% global market share growing at 9.8% CAGR through 2032, driven by high disposable incomes, technology adoption leadership, and established smart home ecosystems.

The United States dominates regional market with 85% North American share through tech company headquarters including Amazon, Google, and Apple developing smart home platforms, high internet penetration exceeding 90% of households, and consumer technology affinity. U.S. smart home market reaching $43 billion in 2025 demonstrates mature adoption with 77.6% household penetration of at least one smart device.

The Canadian market is contributing 8-11% regional share through similar technology adoption patterns and integrated North American market dynamics.

Europe

Europe represents a US$28.4 billion market in 2025, capturing 20% global market share, growing at a 26% CAGR through 2030, characterized by energy efficiency prioritization, sustainability consciousness, and regulatory support for smart home adoption. Germany leads the European market with 28-34% regional share through engineering excellence, premium residential construction, and strong environmental regulations driving energy efficiency adoption.

The United Kingdom is contributing 18-24% European share through smart meter deployment mandates, government energy efficiency incentives, and technology adoption affinity. France, Spain, and Nordic markets are demonstrating growth through EU energy efficiency directives, renewable energy integration, and smart grid development, supporting home automation adoption.

Asia Pacific

Asia Pacific represents fastest-growing region at approximately 28% CAGR through 2030, with estimated market value reaching US$65 billion by 2032 comprising 25% global market share by 2032, driven by urbanization, rising middle class, and government smart city initiatives.

China dominates Asia Pacific with 40-46% regional share through domestic technology giants Alibaba, Tencent, and Baidu developing smart home ecosystems, government smart city initiatives, and the world's largest middle class population exceeding 400 million households.

India is emerging as a high-growth market at a 25-30% CAGR through Digital India initiatives, smartphone penetration reaching 900+ million users, and rising disposable incomes, creating technology adoption acceleration. Japan and South Korea together account for 14-18% of the regional share through technology leadership, high urbanization rates, and a sophisticated consumer electronics market.

Southeast Asia accounts for 10-14% of regional GDP through ASEAN economic integration, urbanization, and rising affluence, creating an emerging market opportunity.

Smart Home Solutions Market Competitive Landscape

The smart home solutions market exhibits moderate-to-high fragmentation with leading platform providers commanding approximately 35% combined market share through ecosystem control, while device manufacturers, software providers, and service companies capture remaining segments.

Amazon emerges as platform leader with estimated 28-32% smart speaker market share through Alexa ecosystem, Echo device portfolio, and 100,000+ third-party integrations. Google maintains competitive positioning with 24-28% smart speaker share through Google Assistant, Nest devices, and seamless Android integration.

Key Industry Developments

- In February 2025, Amazon.com, Inc. unveiled Alexa+, its upgraded AI-powered virtual assistant. Alexa+ integrates generative AI capabilities, powered by Amazon Bedrock models like Nova and Anthropic’s Claude AI, enabling more natural conversations, improved contextual understanding, and multi-command handling.

- In September 2024, Schneider Electric SE launched an AI-powered energy management feature in its Wiser Home app to optimize energy consumption for water heaters and EV chargers. This feature, developed in-house, uses AI to learn from user habits, weather forecasts, and tariff data to automatically manage energy loads and reduce bills.

Companies Covered in Smart Home Solutions Market

- Siemens AG

- United Technologies Corporation

- General Electric Company

- Schneider Electric Se

- Honeywell International, Inc.

- Ingersoll-Rand PLC

- Johnson Controls, Inc.

- ABB Ltd.

- Legrand S.A.

- Samsung Electronics Co., Ltd.

- Lutron Electronics Co., Inc.

- Leviton Manufacturing Company, Inc.

- Acuity Brands, Inc.

- Others Key Players

Frequently Asked Questions

The Smart Home Solutions market is estimated to be valued at US$ 113.4 Bn in 2025.

The key demand driver for the Smart Home Solutions market is the rapid adoption of connected automated living driven by convenience, energy efficiency, and security needs.

In 2025, the North America region will dominate the market with an exceeding 30% revenue share in the global Smart Home Solutions market.

Among the Type of Home, Apartments holds the highest preference, capturing beyond 48.3% of the market revenue share in 2025, surpassing other Type of Home.

The key players in Smart Home Solutions are Siemens AG, United Technologies Corporation, General Electric Company and Schneider Electric Se.