- Home Appliances

- Portable Fan Market

Portable Fan Market Size, Share, and Growth Forecast 2026 - 2033

Portable Fan Market by Product Type (Table Fans, Tower Fans, Others), by Material (Metal Shell, Plastic Shell, Others), Application (Residential, Commercial), Distribution Channel (Online Store, Offline Store), and Regional Analysis for 2026 - 2033

Portable Fan Market Size and Trend Analysis

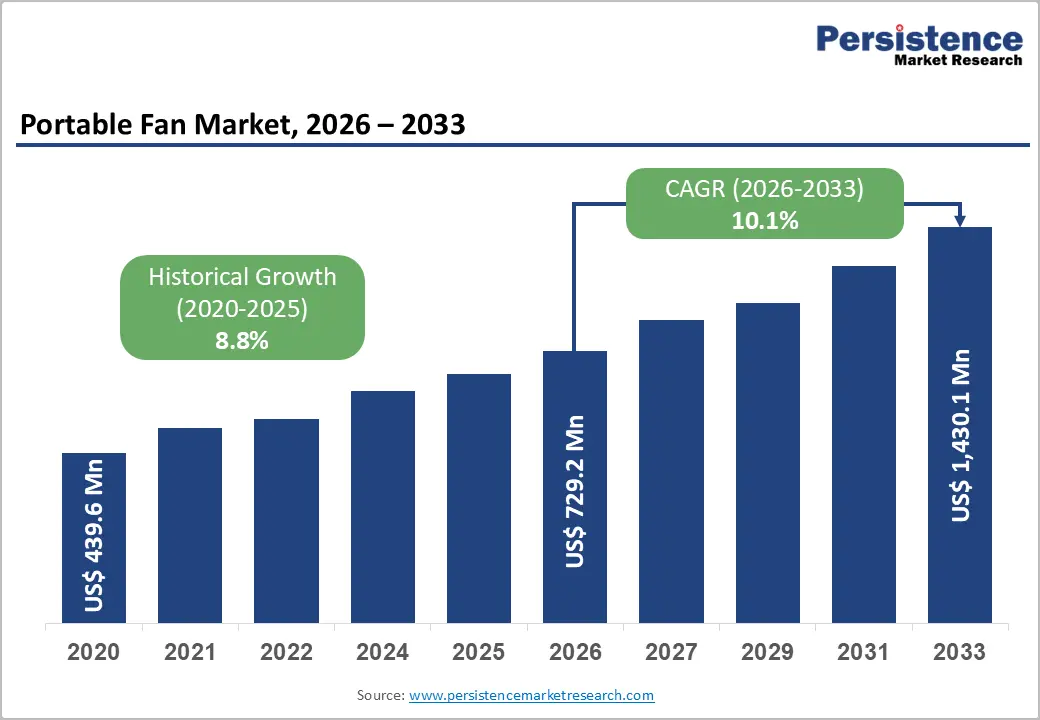

The global portable fan market size is supposed to be valued at US$ 729.2 million in 2026 and is projected to reach US$ 1,430.1 million by 2033, growing at a CAGR of 10.1% between 2026 and 2033.

The market's strong trajectory is driven principally by intensifying global heat stress, accelerating adoption of energy-efficient personal cooling solutions, and the proliferation of remote and outdoor work cultures that demand compact, battery-operated airflow devices.

Rising electricity tariffs across Asia, Europe, and North America are steering consumers away from energy-intensive air conditioning toward cost-effective portable alternatives. The convergence of USB-C charging ecosystems, brushless DC motor technology, and IoT-enabled smart controls is simultaneously elevating product value propositions, attracting premium-tier spending, and broadening the addressable consumer base well beyond traditional warm-climate markets.

Key Industry Highlights:

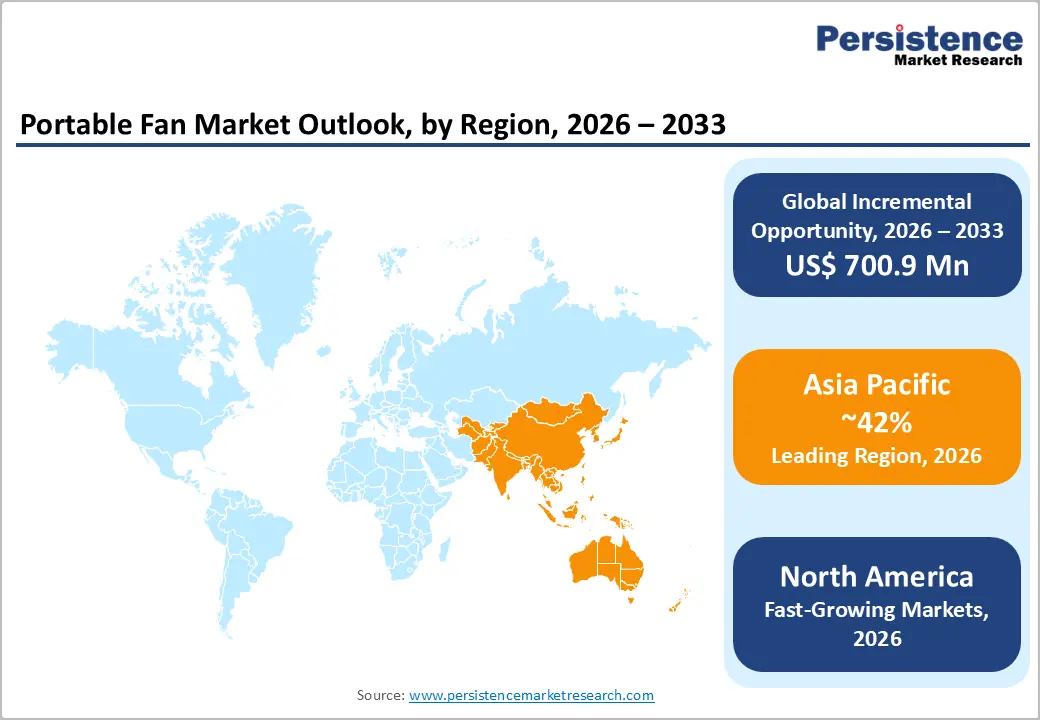

- Climate Change: Rising global temperatures and extreme heat events are accelerating portable fan adoption worldwide. Asia Pacific is likely to dominate with a 42% share in 2026.

- Adoption of Remote Lifestyle: Remote work and outdoor lifestyles are increasing the demand for USB-powered and wearable cooling devices. Around 17.4% of the global workforce engaged in telework during 2023, sustaining year-round portable fan consumption globally.

- Competition from Air Conditioners: The rise in global air-conditioner penetration limits premium portable fan adoption. Global AC stock exceeded 2 billion units in 2022, narrowing price differentiation and constraining growth opportunities for premium bladeless and smart fan categories.

- Smart Fan Innovation: IoT-enabled portable fans with AI sensing, Wi-Fi, and voice-control compatibility are creating premium revenue streams. Smart home industry valuation reached US$ 91.4 billion in 2023, supporting higher-margin connected cooling products globally.

- E-Commerce Sales Growth: Online stores lead distribution with approximately 57% market share in 2025. Rapid e-commerce expansion across India, Southeast Asia, and Latin America enables direct-to-consumer growth and faster product innovation cycles.

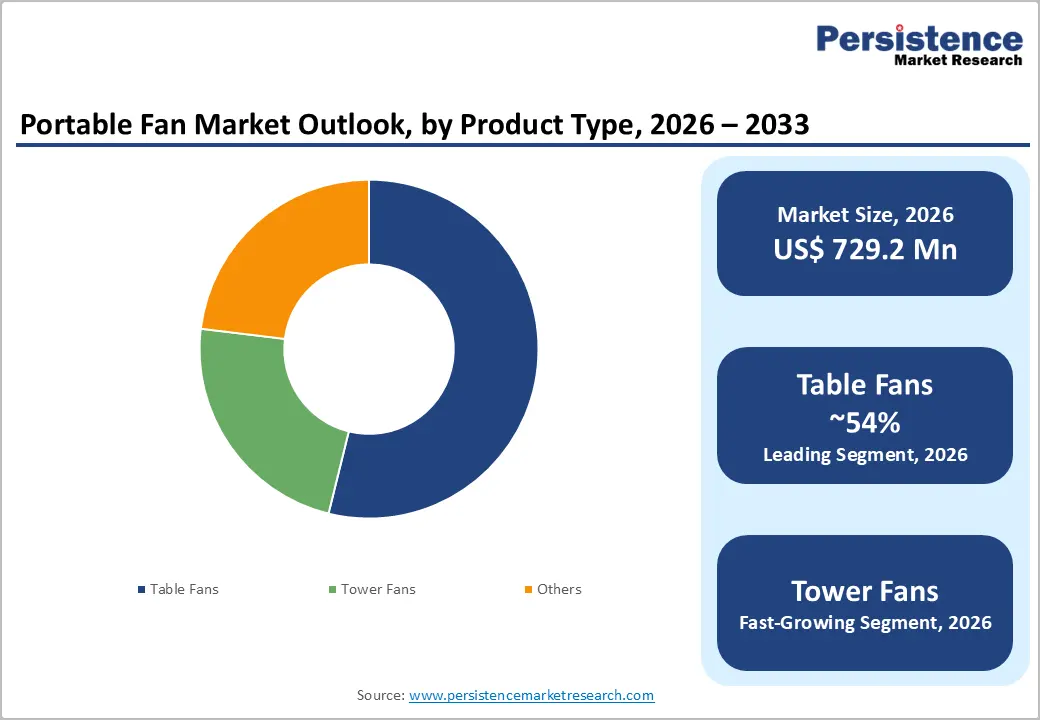

- Dominance of Table Fans: Table fans account for nearly 54% of the total portable fan market share in 2026 due to affordability, versatility, rechargeable functionality, and widespread residential and commercial consumer applications across income groups.

- Fast-growing Product: Tower fans are the fastest-growing product segment, projected to expand at a CAGR of 11.8% in the forecast period, driven by space-saving designs, superior airflow distribution, and increasing bladeless technology adoption.

- Residential Usage Leadership: Residential applications dominate with around 67% market share in 2026, supported by rising electricity costs, work-from-home trends, and growing consumer preference for energy-efficient cooling alternatives over traditional air conditioners.

- Fast-growing Market: China is likely to represent approximately 52% of Asia Pacific portable fan demand in 2025 and is projected to reach a CAGR of 10.5% by 2033, supported by strong manufacturing ecosystems and e-commerce.

Market Dynamics

Drivers - Rise in Global Temperatures Fuelling Demand for Portable Personal Cooling Devices

Climate change-induced heat extremes are structurally expanding the addressable market for portable fans across both developed and emerging economies. The World Meteorological Organization (WMO) confirmed that 2023 was the hottest year on record, with global average temperatures 1.45°C above the pre-industrial baseline, and the European Copernicus Climate Change Service (C3S) verified that every month from June 2023 through May 2024 set a new monthly global temperature record an unprecedented 12-month streak.

In the United States, the National Oceanic and Atmospheric Administration (NOAA) reported that heat-related emergency department visits reached approximately 119,000 in 2023. As heat stress intensifies, portable fans including rechargeable mini fans and smart cooling fans with adaptive speed sensors are increasingly positioned as essential personal health and comfort tools rather than discretionary purchases, sustaining demand even during economic downturns and broadening adoption into previously untapped geographic markets at altitude and in temperate zones.

Shift Toward Remote Work and Outdoor Lifestyles Normalizing On-the-Go Cooling Accessories

The structural normalisation of remote work, hybrid office arrangements, and outdoor recreational activity post-pandemic has materially altered consumer expectations around personal comfort infrastructure. According to the International Labour Organization (ILO), approximately 17.4% of the global workforce was engaged in some form of telework or home-based work as of 2023, creating sustained demand for compact, low-noise, desk-compatible cooling devices.

Simultaneously, outdoor events, camping, festival attendance, and commuter cycling have generated significant demand for wearable neck fans and USB-powered fans that integrate with portable power banks. Japan's Ministry of Internal Affairs and Communications reported that portable fan imports grew by over 22% year-on-year in the summer peak of 2022, illustrating how lifestyle change translates directly into purchasing behaviour. This driver sustains market relevance across four seasons in temperate markets where traditional seasonal peaks previously constrained growth.

Restraints - Competitive Pressure from Air Conditioning and Evaporative Coolers Limiting Premium Uptake

In markets where air conditioning penetration is high or rising rapidly, portable fans face inherent substitution risk at the upper end of the price spectrum. The International Energy Agency (IEA) reported that the global stock of air conditioners surpassed 2 billion units in 2022 and is projected to reach 5.6 billion by 2050, with the fastest adoption concentrated in India, China, and Southeast Asia the same geographies that represent portable fan's highest-growth markets. As room air conditioner prices decline under manufacturing scale economies, the perceived value differential of premium portable fans narrows, constraining average selling price growth and limiting premiumization opportunities for bladeless portable fan and smart cooling fan segments.

Battery Life Limitations and Safety Concerns Constraining Consumer Confidence in Rechargeable Variants

Rechargeable portable fans depend on lithium-ion battery packs that remain constrained by energy density limits, thermal management challenges, and evolving safety regulations. The U.S. Consumer Product Safety Commission (CPSC) reported a significant increase in lithium-ion battery-related incidents from consumer electronics between 2020 and 2023, generating regulatory scrutiny of compact, high-draw devices.

In the European Union, the Battery Regulation (EU) 2023/1542, effective from August 2023, introduces new sustainability, labeling, and due-diligence requirements for batteries in portable products, increasing compliance costs for manufacturers. Shorter operational run-times at high fan speeds often 2 to 4 hours on a single charge for mid-range products remain a persistent consumer dissatisfaction point limiting repeat purchase rates and brand loyalty, particularly in outdoor and travel use cases.

Opportunities - Smart Integration and IoT Connectivity Creating New Premium Product Categories

The integration of wireless connectivity, voice control compatibility, and AI-driven temperature sensing into portable fans is creating a differentiated premium product tier that commands significantly higher average selling prices and margin structures than conventional fan products. Smart cooling fans equipped with Wi-Fi or Bluetooth connectivity, compatible with Amazon Alexa, Google Home, and Apple HomeKit ecosystems, are now commercially available from leading manufacturers and are gaining traction in smart home-oriented consumer segments in North America, Western Europe, and urban Asia Pacific.

The global smart home market was valued at approximately US$ 91.4 billion in 2023 according to the International Telecommunication Union (ITU)-referenced industry data, with personal environment control devices among the fastest-growing sub-categories. For portable fan manufacturers, smart feature integration offers a pathway to price band migration, reducing commoditization risk and creating recurring software and ecosystem revenue opportunities that extend beyond the initial hardware sale.

Rising Penetration of E-Commerce in Emerging Markets Enabling Direct-to-Consumer Brand Building

The rapid expansion of e-commerce infrastructure across Southeast Asia, India, the Middle East, and Latin America is lowering market entry barriers for portable fan manufacturers and enabling direct-to-consumer sales models that structurally improve margin capture compared to traditional offline distribution chains. In India, the Department for Promotion of Industry and Internal Trade (DPIIT) reported that e-commerce retail penetration reached approximately 7.8% of total retail in FY2024, with consumer electronics and personal cooling among the highest-growing categories.

Shopee, Lazada, and Flipkart have each developed dedicated seasonal promotional mechanics including monsoon season and summer sale campaigns that feature portable fans prominently and generate concentrated demand spikes. For brands, these platforms provide access to consumer review data and search trend analytics that can be leveraged to accelerate product iteration cycles for USB powered fans and wearable neck fans, matching evolving consumer preferences with unprecedented speed.

Category-wise Analysis

Product Type Insights

Table fans represent the dominant segment within the portable fan market's product type category, accounting for approximately 54% of total share in 2026. This leadership position is anchored in the segment's superior versatility, affordability, and compatibility with the widest range of consumer use cases from desktop office use and bedside placement to kitchen countertop and outdoor table applications.

Table fans are available across the broadest price range, from sub-US$ 10 mass-market plastic units to premium US$ 80-150 brushless motor models with multi-directional oscillation and LED displays, enabling adoption across virtually all income demographics. The Japan Electrical Manufacturers' Association (JEMA) has consistently reported table fans as the highest-volume portable fan category in its annual shipment data, reflecting the format's enduring relevance. The transition toward rechargeable, cordless table fan designs eliminating the constraint of proximity to power outlets is further reinforcing segment dominance as this product type absorbs functionality previously limited to tower fans.

Tower fans represent the fastest-growing product type segment, projected to reach a CAGR of approximately 11.8% between 2026 and 2033, driven by their space-efficient vertical footprint, superior airflow distribution, and increasing availability of bladeless tower fan formats that eliminate safety concerns for households with children and pets, elevating their appeal in residential and commercial settings.

Material Insights

Plastic shell portable fans dominate the material category, representing approximately 68% of total market share in 2025. Plastic's dominance reflects multiple structural advantages: it is significantly lighter than metal a critical attribute for a product category defined by portability and enables complex aerodynamic blade geometries that optimize airflow efficiency at lower manufacturing cost. Injection-moulded ABS and polypropylene casing supports rapid design iteration cycles, enabling manufacturers to commercialize trend-responsive color schemes and form factors at the speed demanded by fast-moving consumer goods channels.

From a supply chain perspective, plastic shell manufacturing is concentrated in China, Vietnam, and Taiwan, where established tooling ecosystems and skilled labor pools reduce per-unit production costs to levels that sustain mass-market price points. Importantly, advances in recycled-content and bio-based plastics are enabling manufacturers to address sustainability concerns without migrating to heavier, more expensive metal alternatives, extending plastic shell dominance through the forecast period.

Metal shell portable fans are the fast-growing material segment, expected to register a leading CAGR as premiumization trends in North America and Europe drive demand for aesthetically differentiated, durable, and recyclable fan products positioned at the intersection of home décor and personal cooling functionality.

Application Insights

The residential application segment leads the portable fan market, capturing approximately 67% share in 2026. The primacy of residential demand reflects both the category's origins as a home comfort product and the structural growth of work-from-home and stay-at-home economy trends that have materially increased consumers' time in residential settings.

The U.S. Energy Information Administration (EIA) reported that the average U.S. residential electricity prices reached 15.9 cents per kWh in 2023, a 14% increase over 2021 are encouraging households to complement or partially substitute air conditioning with energy-efficient portable fans that consume as little as 5 to 25 watts compared to 900 to 3,500 watts for conventional room air conditioners.

The residential segment also benefits from the broadest distribution reach, being well-served by both online and offline retail channels, including mass merchandisers, home improvement retailers, and e-commerce marketplaces.

The commercial application segment is the fast-growing segment, anticipated to expand at a CAGR of approximately 11.3% propelled by growing deployment of portable fans in open-plan offices, retail spaces, food service establishments, outdoor events, and construction sites where fixed HVAC installation is impractical or cost-prohibitive.

Distribution Channel Insights

Online stores represent the leading distribution channel for portable fans, accounting for approximately 57% of the total share in 2026. E-commerce has become the primary purchase pathway for portable fans across all major markets, driven by the category's high price transparency, ease of product comparison, convenience of home delivery, and suitability for platform-driven impulse purchase mechanics.

Seasonal demand peaks aligned with summer heat events and weather forecast-driven searches are particularly well-served by online channels that can respond to real-time demand signals through targeted search advertising and algorithmic product recommendation. Amazon, Tmall, JD.com, and Flipkart collectively account for a substantial majority of online portable fan sales globally.

The rise of social commerce on platforms including TikTok Shop and Instagram Shopping has further accelerated online channel dominance, with influencer-driven content for wearable neck fans and compact rechargeable mini fans generating viral sales events with minimal paid media investment from emerging brands.

Offline stores remain the fast-growing channel projected at a leading CAGR of approximately 10.6% by 2033, as post-pandemic retail footfall normalization and the expansion of organized retail in Southeast Asia, India, and Latin America restore physical channel relevance, particularly for first-time buyers who value tactile product assessment before purchase.

Regional Insights

North America Portable Fan Market Trends

North America is one of the most technologically advanced and premium-oriented markets for portable fans globally, driven by a combination of intensifying summer heat events, high consumer electronics spend per capita, and strong smart home ecosystem adoption. The region's market is characterized by rapid premiumization, with consumers migrating from commodity plastic fans toward bladeless, IoT-connected, and design-forward products priced at US$ 60 and above.

Major retailers including Best Buy, Target, and Walmart have significantly expanded their portable fan assortments in recent years, with online channels through Amazon.com capturing the majority of incremental growth. The U.S. National Weather Service reported record-breaking heat dome events across the Pacific Northwest and Southwest in 2023 and 2024, directly correlating with seasonal portable fan demand spikes.

The regulatory environment is also shaping product development: California's Title 20 appliance efficiency standards and ENERGY STAR certification programs administered by the U.S. Environmental Protection Agency (EPA) are compelling manufacturers to develop higher-efficiency brushless DC motor designs that perform strongly on both portability and energy consumption metrics.

U.S. Portable Fan Market: North America's Premium Portable Fan Market Transformation

The United States accounts for approximately 78% of North America's total portable fan market revenue in 2025, reflecting the country's scale, consumer spending power, and accelerating heat-related demand. The U.S. market is projected to grow at a CAGR of approximately 9.6% from 2026 to 2033, supported by a combination of climate-driven demand, smart home integration, and e-commerce channel expansion. The U.S. Census Bureau estimates that the U.S. population living in areas experiencing more than 90 days of 90°F+ temperatures annually is projected to double by 2050, underpinning structurally elevated long-term demand.

The proliferation of USB powered fans and smart cooling fans through Amazon's subscription and Prime Day promotional mechanics has also deepened market penetration into mid-income demographic segments that previously relied on fixed ceiling or window fThe U.S. market further benefits from a mature consumer review culture that accelerates product discovery and quality differentiation for premium brands.

Europe Portable Fan Market Trends

Europe represents a high-growth market for portable fans, driven by the region's increasingly hot summers, historically low air conditioning penetration, and strong consumer preference for energy-efficient personal cooling alternatives. The European Environment Agency (EEA) reported that 2022 and 2023 were among the three hottest summers ever recorded in Europe, with heat-related excess mortality exceeding 60,000 deaths in summer 2022 according to research published in Nature Medicine. These events have shifted European consumers' attitudes toward personal cooling preparedness, accelerating portable fan adoption across previously low-penetration markets including Germany, France, and the Nordics.

The EU Energy Efficiency Directive (2023/1791) and Ecodesign Regulation framework are simultaneously shaping product specifications by mandating minimum efficiency standards for electric fan products sold in the EU, effectively accelerating the transition to brushless DC motor technology and incentivizing the development of rechargeable, low-energy portable formats including bladeless and rechargeable mini fans that align with EU sustainability objectives.

Germany Portable Fan Market: Europe's Engineering Hub for Efficient Portable Cooling Innovation

Germany represents approximately 19% of the European portable fan market in 2025, the largest national share in continental Europe, supported by a technologically sophisticated consumer base, high disposable income, and strong preference for certified, energy-efficient appliances. The German market is projected to reach a CAGR of approximately 10.2% from 2026 to 2033.

Germany's Stiftung Warentest product testing certification carries significant purchase influence, and portable fan products that achieve strong ratings in airflow efficiency, noise level, and energy consumption consistently outperform the broader market. The integration of smart controls in premium portable fans is gaining traction within Germany's advanced smart home ecosystem, supported by high household broadband penetration exceeding 92% per the German Federal Network Agency (Bundesnetzagentur).

U.K. Portable Fan Market: Heat Wave Frequency Reshaping British Portable Fan Purchase Patterns

The United Kingdom accounts for approximately 16% of the European portable fan market in 2026, with the market growing at an estimated CAGR of 10.8% from 2026 to 2033 among the fastest within Europe. The UK Met Office confirmed that the summer of 2022 saw the first-ever recorded UK temperature exceeding 40°C, triggering record portable fan sales that persisted into subsequent years as consumers retained purchased units and replacement cycles shortened.

Amazon UK and Argos have consistently listed portable fans among their top summer electronics categories since 2022. The UK market is particularly receptive to compact, design-forward portable fan formats marketed as lifestyle accessories, reflecting the country's strong fashion and design consumer culture.

France Portable Fan Market: Regulatory Drive and Aging Population Powering Portable Fan Necessity

France represents approximately 14% of European portable fan market share in 2026, with a projected CAGR of 9.9% through 2033. The tragic 2003 French heat wave, which caused over 14,000 excess deaths, fundamentally reoriented French public health policy around personal heat protection. France's Canicule (heat wave) alert system, managed by Santé Publique France, explicitly recommends portable fans as a frontline heat protection tool, embedding the product in public health communications annually.

The French market benefits from strong institutional demand through the country's healthcare and elderly care infrastructure: the INSEE estimates that France's population aged 75 and over will reach 9 million by 2030, creating sustained demand for safe, easy-to-use cooling devices in residential care settings.

Italy: Mediterranean Heat Intensity Driving Portable Fan Market Diversification

Italy holds approximately 13% of Europe's portable fan market in 2026, with the market projected to grow at a CAGR of 10.4% from 2026 to 2033, supported by consistently high summer temperatures across the Po Valley, Rome, and the Southern Italian peninsula. The Italian National Institute of Statistics (ISTAT) has documented increasing heat wave frequency and intensity in Italy over the past decade, driving sustained consumer investment in personal cooling.

Italy's design culture also makes it a market receptive to premium aesthetics in portable fans, with local consumers willing to pay a significant premium for products that complement home interiors. This has attracted international premium brands including Dyson to prioritize Italian retail partnerships for bladeless and premium tower fan variants.

Asia Pacific Portable Fan Market Trends

Asia Pacific is the dominant regional market for portable fans globally, holding approximately 42% share in 2026 and serving as both the world's largest consumption base and its primary manufacturing hub. The region's climate profile encompassing tropical, subtropical, and monsoonal zones across China, India, Southeast Asia, Japan, and South Korea creates sustained, year-round demand for portable cooling solutions across all consumer income levels. China, in particular, is both the world's largest producer and consumer of portable fans, with its vast electronics manufacturing ecosystem enabling rapid product innovation at competitive price points for both domestic and export markets.

Regional e-commerce platforms including Alibaba's Taobao and Tmall, JD.com, Shopee, and Lazada have transformed portable fan distribution by enabling direct manufacturer-to-consumer models that compress supply chains and accelerate seasonal product launches. The growth of wearable neck fans pioneered by Japanese and South Korean consumer electronics brands and subsequently mass-manufactured in China has created an entirely new portable fan sub-category that now commands meaningful shelf space on regional platforms.

China Portable Fan Market: World's Manufacturing and Consumption Powerhouse for Portable Fans

China is the single largest national market for portable fans globally, representing approximately 52% of Asia Pacific's total market share in 2025 and projected to reach a CAGR of 10.5% from 2026 to 2033. China's General Administration of Customs data confirms that fan and air circulation device exports have consistently exceeded US$ 2 billion annually, reflecting the country's manufacturing dominance.

Domestically, platform-driven seasonal campaigns on Tmall's 618 Shopping Festival and Double 11 (Singles Day) generate peak portable fan demand surges of 300-400% above baseline, reflecting deep e-commerce integration. China's manufacturing ecosystem anchored in Guangdong, Zhejiang, and Jiangsu provinces enables production cost structures that sustain global competitiveness while domestic brands such as Xiaomi, Midea, and Deerma invest heavily in smart integration and design to capture premium domestic spending.

India Portable Fan Market: Explosive Heat-Driven Demand Transforming Portable Fan Consumption Landscape

India represents approximately 18% of the Asia Pacific's portable fan market in 2025, with the country projected to register a positive CAGR of approximately 12.3% from 2026 to 2033, driven by a combination of climate urgency and rising middle-class income.

The India Meteorological Department (IMD) affirmed that 2024 was the hottest year on record for India, with heat wave conditions affecting over 20 states and temperatures exceeding 50°C in parts of Rajasthan.

India's residential electricity infrastructure, while rapidly expanding, still faces frequent supply interruptions in tier-2 and tier-3 cities, making rechargeable mini fans and battery-operated portable fans essential rather than aspirational products. The DPIIT has identified personal cooling devices as a high-priority consumer electronics category under its Production-Linked Incentive (PLI) scheme, attracting domestic manufacturing investment that is reducing import dependency.

South Korea Portable Fan Market: Technology-First Innovation Hub for Premium Portable Fan Segments

South Korea accounts for approximately 8% of Asia Pacific's portable fan market in 2025 and holds disproportionate strategic importance as the region's leading innovation origin market for next-generation portable fan technology, with a projected CAGR of 11.1% from 2026 to 2033. South Korean consumer electronics brands including Samsung, LG, and specialist personal appliance companies have pioneered the global commercialization of wearable neck fans, bladeless portable fans, and smart cooling fans with biometric temperature sensing.

South Korea's Ministry of Trade, Industry and Energy (MOTIE) supports consumer electronics R&D through targeted innovation grants, and the country's high urban density, long commuting hours, and technology-forward consumer culture create ideal conditions for personal wearable cooling adoption. South Korean product innovations typically enter international markets via Japan and then global platforms within 12 to 18 months of domestic launch.

Competitive Landscape

The global portable fan market is moderately fragmented at the global level but exhibits regional concentration in manufacturing dominated by Chinese producers and brand premiumization led by a small number of well-capitalised multinationals. Dyson, Xiaomi, Midea, Honeywell (a Resideo Technologies brand), and Vornado Air anchor the premium and mid-premium tiers respectively, competing on design differentiation, smart integration, and brand equity.

The mid-market and value tiers are intensely contested by a large number of Chinese original design manufacturers (ODMs) and private-label brands distributed through e-commerce platforms. Key competitive differentiators include motor technology (brushed vs. brushless DC), battery capacity, noise level certification (decibel ratings), smart connectivity, and sustainability credentials. Emerging business models include direct-to-consumer subscription cooling bundles and modular fan systems with replaceable components.

Key Developments:

- In May 2026, Cuktech launched the CP Modular Fan Plus, a portable modular fan with a 33W power bank, magnetic Power-Pin interface, 11 m/s airflow, brushless motor, and energy-efficient vortex cooling technology.

- April 2026: Dyson launched the HushJet™ Mini Cool Fan, a 212g portable wearable fan featuring 25m/s airflow, 6-hour battery life, and a 65,000 RPM brushless DC motor.

- March 2025: Dyson launched the Dyson CSYS Portable Cool, incorporating a refined bladeless air multiplier technology with Bluetooth-enabled temperature sensing and a 70-hour battery life, targeting premium residential and professional users at a retail price point above US$ 400.

- July 2024: Xiaomi introduced its Smart Portable Tower Fan Pro in the Chinese domestic market via Tmall, featuring a Mi Home app integration, 38-speed settings, and a sub-US$ 50 retail price aggressively targeting the high-volume mid-market segment with smart functionality previously confined to premium tiers.

- January 2024: LG Electronics filed multiple patent applications related to wearable neck fan thermal regulation technology with the Korean Intellectual Property Office (KIPO), signalling the company's strategic intention to enter the personal wearable cooling segment with proprietary innovation ahead of the summer 2025 product cycle.

Companies Covered in Portable Fan Market

- Dyson Ltd.

- Midea Group

- Honeywell International

- Xiaomi

- Vornado Air

- Lasko Products

- Rowenta (Groupe SEB)

- Panasonic, Sharp

- LG Electronics

- Samsung Electronics

- Deerma, Comfee'

- De'Longhi

- Tefal, Black+Decker

- AUX Group

- Haier Smart Home

- Philips (Versuni)

- Bionaire

Frequently Asked Questions

The global portable fan market is estimated to be valued at US$ 729.2 million in 2026 and is projected to reach US$ 1,430.1 million by 2033, registering a CAGR of 10.1% over the forecast period. This growth is underpinned by intensifying global heat events, accelerating smart home adoption, and the structural shift toward energy-efficient personal cooling solutions globally.

The primary demand drivers are escalating global average temperatures confirmed by the WMO as reaching a record 1.45°C above pre-industrial levels in 2023 and the structural normalization of remote work and outdoor lifestyle activities that create sustained demand for portable personal cooling. The proliferation of rechargeable battery technology, USB powered fan ecosystems, and IoT-enabled smart cooling fans is further broadening the product's relevance beyond traditional warm-climate seasonal demand.

Table fans are the dominant product type segment, accounting for approximately 54% of global portable fan market share in 2025. Their leadership reflects broad price accessibility, versatile placement options from desk to outdoor settings, and the category's rapid innovation toward cordless rechargeable formats that remove power outlet dependency the primary limitation of traditional table fan utility.

Asia Pacific is the leading region, commanding approximately 42% of global portable fan share in 2026. The region benefits from a combination of the world's largest heat-exposed population base, China's vertically integrated manufacturing ecosystem that produces the majority of global portable fan volume, and rapidly expanding e-commerce infrastructure enabling efficient distribution across diverse consumer income segments in India, Southeast Asia, and beyond.

The highest-value growth opportunity lies in smart IoT-enabled personal cooling specifically smart cooling fans and wearable neck fans for premium residential and on-the-go consumer segments. The global smart home market's rapid expansion and the proliferation of USB powered fans integrated with portable power bank ecosystems in emerging markets collectively represent a structural demand evolution that incumbent manufacturers with only conventional product portfolios are poorly positioned to capture.

Leading companies in the global portable fan market include Dyson Ltd., Midea Group, Honeywell International (Honeywell Home), Xiaomi Corporation, Vornado Air, Panasonic, LG Electronics, Samsung Electronics, Lasko Products, Rowenta (Groupe SEB), De'Longhi Group, and Sharp Corporation, among others. These players compete primarily on motor technology innovation, smart connectivity, energy efficiency certifications, brand equity, and e-commerce channel strength across regional markets.