- Travel and Tourism

- Catering Services Market

Catering Services Market Size, Share, and Growth Forecast 2026 - 2033

Catering Services Market by Service Type (Contract Catering, Event Catering, Concession Catering, Transport Catering), Service Mode (On-Premise Catering, Off-Premise Catering), Pricing (Budget Catering, Mid-Range Catering, Premium Catering), Service Format (Buffet Service, Sit-Down Service, Packaged Meals, Live Cooking / Food Station), End-User (Corporate Offices, Healthcare, Educational Institutions, Industrial, Sports & Entertainment Venues, Defense & Government, Airlines, Railways, Cruise Lines, Others), and Regional Analysis, 2026 - 2033

Catering Services Market Size and Trend Analysis

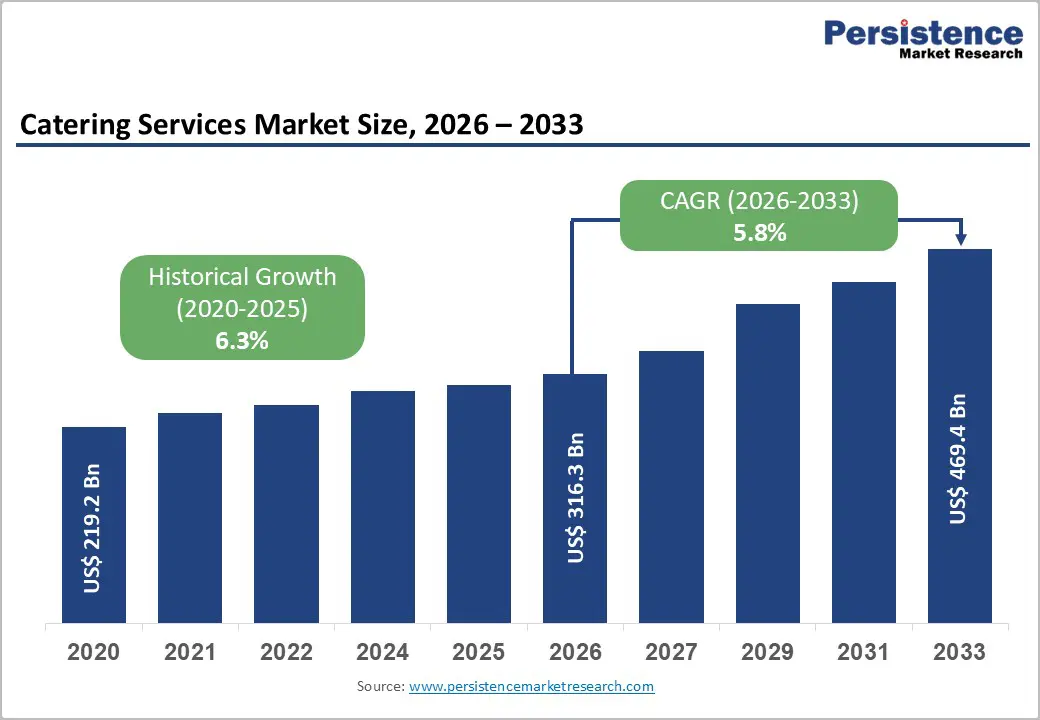

The global catering services market size is expected to reach US$ 316.3 billion in 2026 and US$ 469.4 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

The catering services industry is on a robust growth trajectory driven by rising outsourcing of institutional food services, accelerating global corporate activity, and a post-pandemic resurgence in events, travel, and hospitality. Contract catering, which enables organizations across healthcare, education, and corporate sectors to reduce operational overhead while improving food quality standards, remains the primary demand engine.

Supportive trends, including workforce re-entry into physical office environments, expansion of organized healthcare infrastructure across emerging economies, and growing consumer expectations for diverse, health-oriented menus, are reinforcing consistent revenue expansion across all major service types and geographies.

Key Industry Highlights:

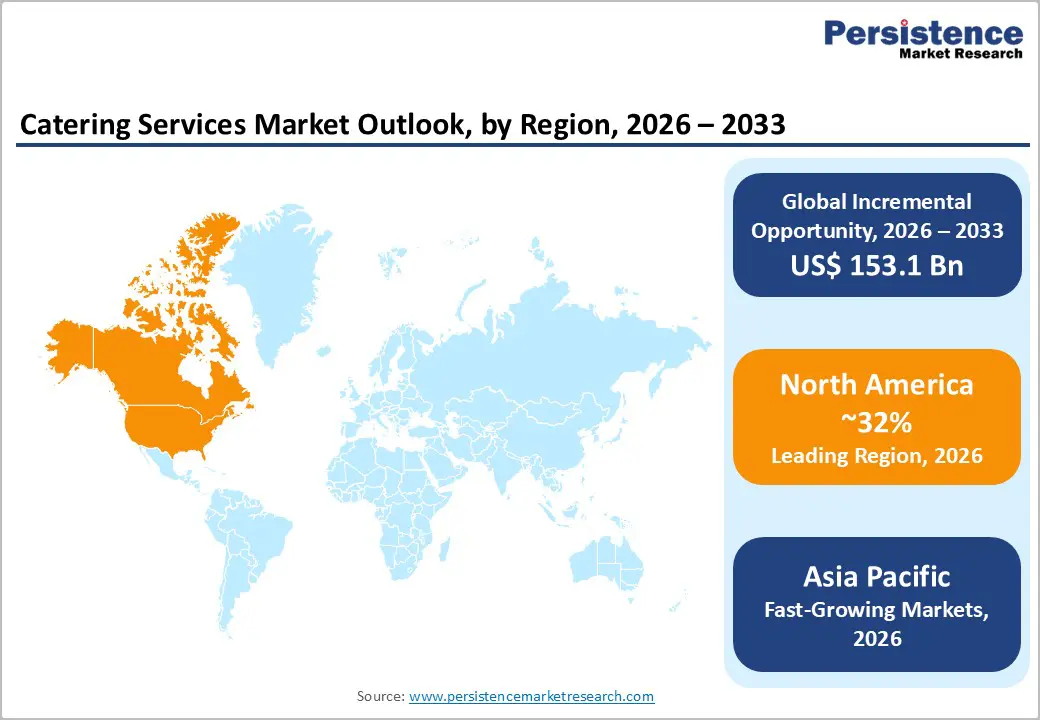

- Leading Region: North America leads the global catering services market with approximately 32% share in 2025, anchored by the United States' mature institutional catering ecosystem, large-scale corporate campus contracts, and regulatory-driven food safety innovation investments by operators such as Aramark and Sodexo.

- Fastest Growing Region: Asia Pacific is the fastest-growing catering services region, projected at approximately 7.2% CAGR through 2033, driven by China's expanding corporate and healthcare infrastructure, India's booming food services sector projected at US$ 125 billion by 2029, and rapid ASEAN industrial growth.

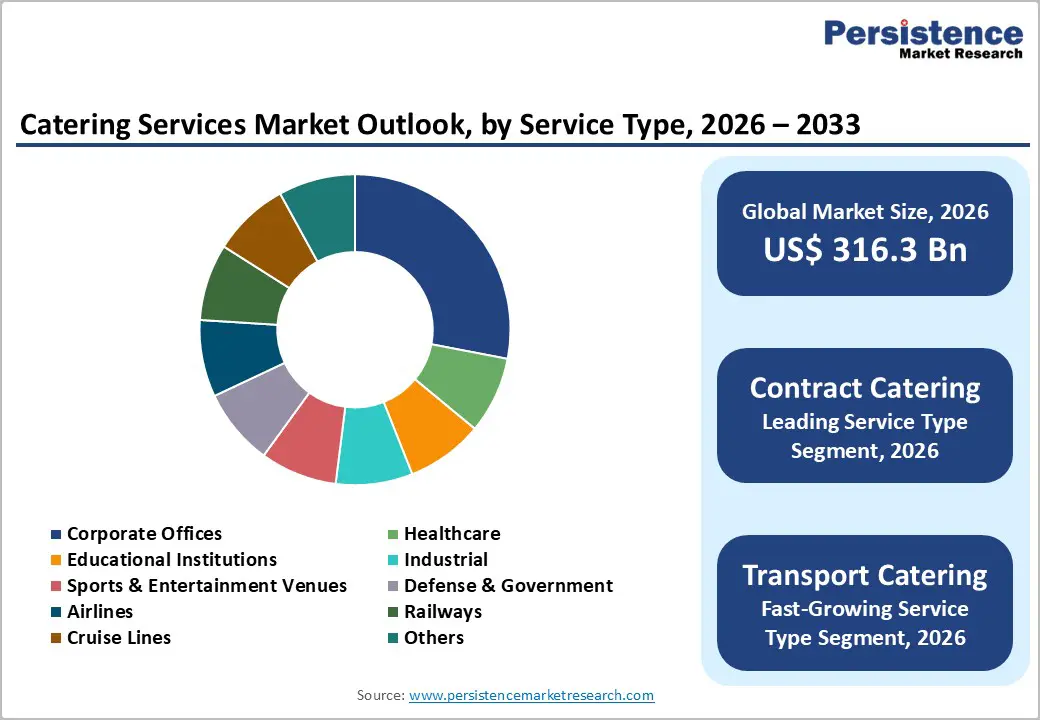

- Dominant Segment: Contract catering dominates the global market with approximately 46% share in 2025, underpinned by high institutional contract renewal rates exceeding 90%, multi-year revenue visibility, and the operational depth of multinational operators serving healthcare, corporate, and defense clients globally.

- Fastest Growing Segment: Healthcare catering is the fastest-growing end-user segment through 2033, fueled by aging global demographics, with the UN projecting 1.6 billion people aged 65+ by 2050, and rising institutional demand for specialist clinical nutrition and therapeutic diet catering programs.

- Key Opportunity: The convergence of AI-powered menu planning, digital ordering platforms, and sustainability-driven food waste reduction represents the defining market opportunity, enabling operators to achieve 20-30% food waste reductions through smart demand forecasting and creating compelling ESG value propositions for institutional procurement teams.

| Key Insights | Details |

|---|---|

| Catering Services Market Size (2026E) | US$ 316.3 Billion |

| Market Value Forecast (2033F) | US$ 469.4 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.8% |

| Historical Market Growth (2020 - 2025) | 6.3% |

Market Dynamics

Drivers - Accelerating Outsourcing of Institutional and Corporate Food Services

The systemic shift toward outsourced catering services among large institutions, including corporates, healthcare facilities, universities, and government bodies, is one of the most powerful structural growth drivers in the global catering services market. Organizations increasingly recognize that outsourcing food and beverage operations to specialist caterers enables significant cost efficiencies, labor management simplification, compliance with food safety regulations, and access to nutritionally balanced, culinarily diverse menus that in-house teams cannot replicate at scale.

According to the British Hospitality Association, outsourced catering currently accounts for less than 50% of the total addressable institutional food services market in the United Kingdom alone, indicating substantial remaining headroom. Compass Group plc, Sodexo S.A., and Aramark Corporation, the three largest global contract caterers, collectively operate across 50+ countries and have consistently reported contract renewal rates above 90%, underscoring the stickiness and long-term revenue predictability that outsourced institutional catering generates for market participants.

Post-Pandemic Recovery in Events, Aviation, and Transport Catering

The full-scale recovery of global events, aviation, and passenger rail sectors is providing powerful demand stimulus for event and transport catering segments after the severe disruptions of 2020-2021. The International Air Transport Association (IATA) reported that global air passenger traffic reached approximately 94% of pre-pandemic 2019 levels in 2023 and is expected to fully surpass prior peaks by 2025, generating commensurate demand recovery for airline catering services. Simultaneously, the global events industry, encompassing corporate conferences, sporting events, weddings, and music festivals, has rebounded robustly.

The global events industry is growing at a mid-to-high single-digit CAGR, with large-scale events driving significant catering outsourcing activity. DO & CO AG and LSG Group, key airline and premium event caterers, have both publicly reported order-book recovery surpassing pre-pandemic levels, confirming the breadth and momentum of this sector-wide demand resurgence.

Restraints - Persistent Labor Shortages and Rising Wage Pressures

The catering services industry is acutely exposed to structural labor market challenges, particularly in North America and Western Europe, where hospitality and food services sectors face chronic staffing deficits. The U.S. Bureau of Labor Statistics (BLS) reported that the accommodation and food services sector sustained a monthly job opening rate consistently above 6% throughout 2022-2023, among the highest across all major U.S. industry sectors.

Minimum wage legislation increases, enacted across multiple U.S. states and EU member countries, are simultaneously compressing operating margins for caterers, which are already structurally thin at 3-5% for contract catering operators. The inability to fully pass labor cost escalations to institutional clients within fixed-price contract frameworks further erodes profitability, constraining capacity expansion and investment in service quality enhancements.

Food Safety Compliance Costs and Regulatory Complexity

Catering service providers operate under increasingly stringent and jurisdiction-specific food safety, hygiene, and allergen disclosure regulatory frameworks, creating significant compliance cost burdens, particularly for operators managing multi-country or multi-site portfolios. In the European Union, Regulation (EU) No 1169/2011 on food information to consumers mandates comprehensive allergen labeling and disclosure, requiring caterers to implement robust ingredient traceability and staff training systems at scale.

The U.S. Food Safety Modernization Act (FSMA), enforced by the U.S. Food and Drug Administration (FDA), imposes preventive controls, supply chain management requirements, and recall protocols that demand dedicated food safety management investments. Non-compliance penalties, including operational shutdowns, contract terminations, and reputational damage, impose existential risks, particularly for smaller and mid-sized regional catering operators that lack the compliance infrastructure of multinational players.

Volatile Rise of LPG Price

The global catering services market is increasingly vulnerable to LPG price volatility amid geopolitical tensions near the Strait of Hormuz, a key transit route for global energy supplies. Disruptions in LPG trade flows are driving sustained fuel cost inflation, significantly increasing operational expenses for commercial kitchens, especially in large-scale institutional catering. This cost pressure is particularly acute in fixed-price contracts across education, healthcare, and government sectors, limiting immediate cost pass-through.

In response, catering providers are accelerating the adoption of energy-efficient cooking systems, alternative fuels, and centralized kitchen models to optimize fuel consumption. Additionally, contract renegotiations and dynamic pricing mechanisms are gaining traction. Prolonged instability is expected to reshape cost structures, intensify margin pressures, and drive strategic shifts toward energy diversification and operational resilience.

Opportunities - Technology-Driven Transformation: Digital Ordering, AI-Powered Menu Planning, and Sustainability Platforms

The integration of digital technologies across catering service delivery presents a transformative commercial opportunity for forward-thinking operators to differentiate, expand margins, and attract premium institutional contracts. Cloud-based catering management platforms, mobile ordering and pre-order applications, AI-driven menu optimization tools, and IoT-enabled food temperature monitoring systems are rapidly reshaping operational capabilities across the industry. Compass Group plc has invested substantially in its proprietary digital infrastructure, including its Feedr platform acquisition, which enables corporate clients to access pre-ordered, personalized meal delivery services with real-time nutritional tracking.

The United Nations Environment Programme (UNEP) estimates that one-third of all food produced globally is lost or wasted, and institutional caterers deploying AI-based demand forecasting tools are reporting food waste reductions of 20-30%, generating measurable ESG credentials that are increasingly required by institutional procurement teams. This convergence of technology, sustainability, and convenience positions digitally-enabled caterers for a significant contract capture advantage.

Healthcare and Aging Population Demographics Creating Sustained Demand for Specialist Nutrition Catering

The global demographic shift toward older populations is generating a structurally growing and high-value demand segment for specialist clinical and therapeutic nutrition catering services within hospitals, long-term care facilities, assisted living centers, and rehabilitation units. The United Nations projects the global population aged 65 and above will reach approximately 1.6 billion by 2050, up from 783 million in 2023, a near-doubling that will dramatically expand healthcare facility populations globally.

According to the World Health Organization (WHO), malnutrition among hospitalized patients remains a critical clinical challenge, with studies indicating that 20-50% of hospital patients across Europe experience some form of nutritional deficiency. This has elevated specialized therapeutic catering, encompassing texture-modified diets, allergen-free meal programs, and clinical nutrition meal services, to a strategic priority for healthcare procurement teams. Companies including Sodexo S.A. and Elior Group have developed dedicated healthcare catering divisions that command significant pricing premiums over standard institutional catering contracts, positioning the healthcare end-user segment as the highest-growth opportunity within the catering services market.

Category-wise Analysis

Service Type Insights

Contract catering is the unequivocal leading segment within the service type category, commanding approximately 46% of the global catering services market share in 2025. Its dominance is rooted in the long-term, high-volume, and recurring revenue model that institutional clients, including multinational corporations, national health services, universities, and defense establishments, provide to contracted caterers.

The predictability of contract catering revenues, typically secured through multi-year agreements with renewal rates consistently exceeding 90% as reported by leading operators Compass Group plc and Sodexo S.A., makes this segment structurally superior in terms of financial stability. The British Contract Catering Association (BCCA) estimates the UK contract catering market alone serves over 500 million covers annually.

The segment's resilience was further demonstrated through the COVID-19 pandemic, where healthcare and defense contract catering maintained operations throughout global lockdowns, reinforcing long-term institutional confidence in outsourced food service models.

Service Mode Insights

On-premise catering dominates the service mode category, representing approximately 62% of the global catering services market share in 2025. On-premise delivery, wherein caterers operate dedicated kitchens, dining halls, and food service facilities within client locations such as corporate campuses, hospitals, schools, and defense establishments, underpins the contract catering model and is the standard delivery mechanism for the overwhelming majority of institutional catering contracts globally.

The structural advantages of on-premise operations include tighter quality control, real-time menu customization, direct client relationship management, and the ability to build embedded, long-term service relationships that drive high contract renewal rates.

The significant capital investment in on-premise kitchen infrastructure by caterers creates high switching costs for institutional clients, further entrenching on-premise catering's market leadership. Major operators, including Aramark Corporation, ISS A/S, and BaxterStorey, derive the majority of their revenues from on-premise institutional contracts.

Pricing Insights

Mid-range catering is the leading pricing tier, accounting for approximately 45% of the global catering services market share in 2025. This segment serves the broadest addressable institutional client base, encompassing mid-sized corporate offices, regional hospitals, state universities, and municipal government facilities that require professionally managed food service operations with cost structures compatible with organizational food budgets. Mid-range catering balances quality, menu diversity, and operational efficiency, offering institutional clients a compelling value proposition that neither the budget nor premium tiers can replicate.

The U.S. Bureau of Labor Statistics data confirms that corporate food service expenditure per employee has grown steadily in the US$ 8-15 per meal range for mid-range contracts, creating attractive revenue-per-cover metrics for caterers. Companies including Guckenheimer, Bon Appétit Management Company, and CH&CO Catering Group have built market-leading positions primarily serving this institutionally dominant mid-range pricing tier.

Service Format Insights

Buffet service is the leading service format, capturing approximately 38% of the global catering services market share in 2025. The format's dominance stems from its operational efficiency, scalability, and broad applicability across diverse catering settings, from corporate office dining and educational institution cafeterias to large-scale event and hospitality catering. Buffet operations enable caterers to serve high volumes of covers with proportionally lower front-of-house labor requirements compared to sit-down service, improving labor cost ratios in an industry facing persistent staffing pressures.

The National Restaurant Association (NRA) has consistently highlighted buffet and self-service formats as operationally preferred by institutional clients managing high daily cover volumes. Post-pandemic hygiene innovations, including individually wrapped stations, transparent sneeze guards, and contactless serving technologies, have successfully restored institutional client confidence in buffet formats, enabling continued dominance through the forecast period.

End-User Insights

The corporate offices segment leads the end-user category, holding approximately 28% of the global catering services market share in 2025. Corporate catering represents the single largest addressable client category for global contract caterers, driven by the vast scale of multinational corporate campuses across North America, Europe, and Asia Pacific, the organizational imperative to provide high-quality employee food benefits as a retention and productivity tool, and the growing corporate commitment to workforce wellness programs that mandate nutritionally balanced, diverse meal offerings. It is usually found that employer-provided food benefits contribute measurably to employee satisfaction and productivity, incentivizing continued corporate investment in premium on-site catering services.

Major operators Compass Group plc, Sodexo S.A., and Aramark Corporation derive substantial portfolio revenues from long-term Fortune 500 corporate campus contracts, with global tech giants in Silicon Valley, London, and Singapore representing flagship anchor clients.

Regional Insights

North America Catering Services Market Trends and Insights

North America holds the leading position in the global catering services market, commanding approximately 32% of global market share in 2025, with the United States accounting for the dominant share of regional revenues. The U.S. market is characterized by a highly evolved outsourced catering ecosystem, anchored by major operators including Aramark Corporation, Compass Group's North American division, and Sodexo North America. The National Restaurant Association reported U.S. food service industry revenues of approximately US$ 1.1 trillion in 2023, with institutional and contract catering representing a significant and growing portion. Corporate wellness mandates, diversity of dietary preferences, and technology-enabled ordering platforms are key innovation drivers across the U.S. market.

Regulatory frameworks including the U.S. Food Safety Modernization Act (FSMA) and state-level nutritional disclosure requirements are driving systemic food safety infrastructure investment among catering operators, while the Healthy, Hunger-Free Kids Act has transformed educational institution catering standards nationwide. Canada's growing multicultural population is simultaneously creating demand for diverse, ethnically inclusive menus across institutional settings, with Government of Canada food policy guidelines increasingly shaping healthcare and government facility catering specifications.

Europe Catering Services Market Trends and Insights

Europe is the second-largest regional market, with Germany, the United Kingdom, France, and Spain collectively constituting the core demand centers. The UK hosts the most mature contract catering market in Europe, with data from the British Contract Catering Association (BCCA) indicating that the sector directly employs over 400,000 people and serves hundreds of millions of institutional covers annually. BaxterStorey, CH&CO Catering Group, and Amadeus Catering are prominent UK-headquartered players serving corporate, healthcare, and event catering segments. France, home to Elior Group and the European operations of Sodexo S.A., benefits from a deeply embedded institutional catering culture with long-standing government procurement frameworks.

Regulatory harmonization under the EU Food Safety Authority (EFSA) standards and the Farm to Fork Strategy under the European Green Deal are compelling European caterers to invest in sustainable sourcing, organic ingredients, and carbon footprint reduction across their supply chains. Germany's robust manufacturing and industrial catering sector, combined with its landmark Supply Chain Due Diligence Act (LkSG) enacted in 2023, is creating new compliance requirements for caterers sourcing ingredients across international supply chains, driving consolidation toward larger, compliance-capable operators.

Asia Pacific Catering Services Market Trends and Insights

Asia Pacific is both the second-largest and the fastest-growing regional market, projected to expand at a CAGR of approximately 7.2% between 2026 and 2033, driven by rapid urbanization, expanding organized corporate and healthcare infrastructure, and rising discretionary food service expenditure. China dominates regional consumption, with its vast and growing corporate sector, state-owned enterprise campuses, and rapidly expanding hospital and educational institution networks generating enormous institutional catering demand. Japan's highly regulated and quality-focused institutional catering market, particularly in healthcare and transport catering, continues to grow steadily, with Japan Catering Service Association members reporting consistent demand recovery across airline and railway catering segments.

India is emerging as one of the highest-potential growth markets globally, with the India Brand Equity Foundation (IBEF) projecting India's food services industry to reach US$ 125 billion by 2029, supported by the rapid expansion of Special Economic Zones, IT parks, and organized retail and hospitality infrastructure. Southeast Asian markets, including Indonesia, Vietnam, and Thailand are experiencing significant growth in industrial and corporate catering driven by foreign direct investment inflows and expanding manufacturing sector activity. The ASEAN region's young and urbanizing population demographic, with a median age below 30 years in several key markets, creates sustained long-term demand for diverse, affordable institutional catering services across educational and corporate segments.

Competitive Landscape

The global catering services market exhibits a moderately consolidated structure, with a few multinational operators commanding a significant share through long-term, large-scale contracts across healthcare, corporate, education, defense, and transportation sectors. These players leverage global procurement networks, operational scale, and integrated service models to maintain competitive advantage across multiple geographies.

Strategic differentiation is increasingly driven by digital integration, including data-led menu planning, automated service management platforms, and technology-enabled customer engagement. Sustainability initiatives, such as food waste reduction, local sourcing, and low-carbon menus, are also becoming central to competitive positioning. Additionally, growing demand for specialized services, particularly in healthcare and clinical nutrition, is encouraging capability expansion.

Mid-tier and regional providers compete by focusing on niche segments, premium offerings, and localized expertise. Emerging trends such as ghost kitchens, plant-based menus, and flexible catering formats are further reshaping competition across institutional and event catering segments globally.

Key Developments

- August 2025: DRRK Foods announced its strategic expansion into India’s HoReCa sector, targeting INR 100 crore in domestic revenue by supplying premium-quality basmati rice to hotels, restaurants, and catering services across major cities, strengthening its institutional market presence.

- March 2025: Compass Group plc announced the acquisition of a majority stake in a leading technology-enabled workplace food services platform, strengthening its digital catering delivery capabilities across its North American and European corporate campus contract portfolio.

- June 2023: Aramark Corporation completed the spin-off of its uniform services division, enabling full strategic refocus on food and facilities management services and allocating incremental capital toward healthcare catering expansion across emerging markets in Asia Pacific and Latin America.

Companies Covered in Catering Services Market

- Compass Group plc

- Sodexo S.A.

- Aramark Corporation

- Elior Group

- ISS A/S

- Delaware North

- DO & CO AG

- BaxterStorey

- CH&CO Catering Group

- Mitie Catering Services

- Amadeus Catering

- Camst Group

- Guckenheimer

- Bon Appétit Management Company

- Thomas Franks Ltd

- LSG Group

- Eurest (Compass Group)

- Scolarest

- Newrest Group Services

- ICTS Europe

Frequently Asked Questions

The catering services market is projected to reach US$ 316.3 billion in 2026, growing from US$ 219.2 billion in 2020 at a CAGR of 6.3%.

Growth is driven by rising outsourcing of food services, recovery in air travel, and increasing demand for diverse and health-focused catering solutions.

North America leads the market with around a 32% share, supported by a mature contract-catering ecosystem in the U.S.

Major opportunities lie in digital and healthcare catering, including AI-driven personalization and growing demand for clinical nutrition services.

Leading players include Compass Group plc, Sodexo S.A., and Aramark Corporation, along with several other global and regional operators.