- Home Care & Utilities

- Carpet and Rugs Market

Carpet and Rugs Market Size, Share, and Growth Forecast 2026 - 2033

Carpet and Rugs Market by Product Type (Tufted, Needle Punched, Knotted, Woven, Others), Material Type (Polyester, Nylon, Cotton, Polypropylene, Others), End Use (Residential, Commercial), and Regional Analysis for 2026 - 2033

Carpet and Rugs Market Size and Trend Analysis

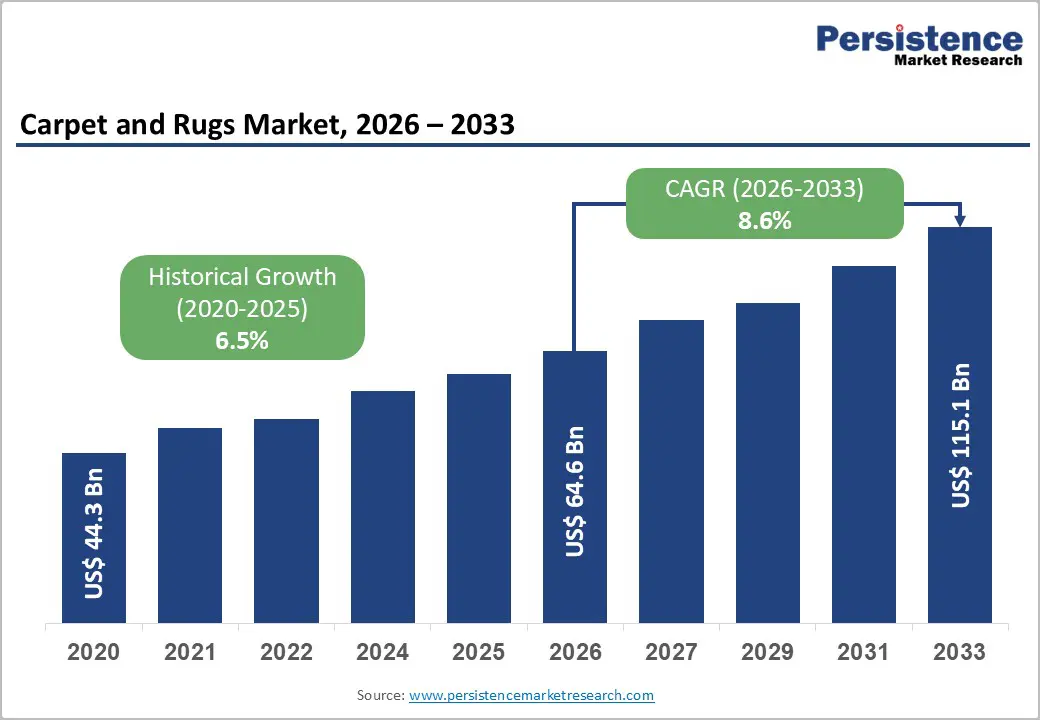

The global carpet and rugs market size is estimated to be valued at US$ 64.6 Bn in 2026 and is projected to reach US$ 115.1 Bn by 2033, growing at a CAGR of 8.6% between 2026 and 2033.

This robust growth trajectory is primarily driven by accelerating urbanization globally, sustained expansion in residential and commercial construction, and a growing consumer appetite for aesthetic interior spaces. According to the United Nations' World Urbanization Prospects 2025, 45% of the global population resides in cities, fuelling demand for well-designed, functional living spaces that incorporate stylish flooring solutions.

Key Market Highlights

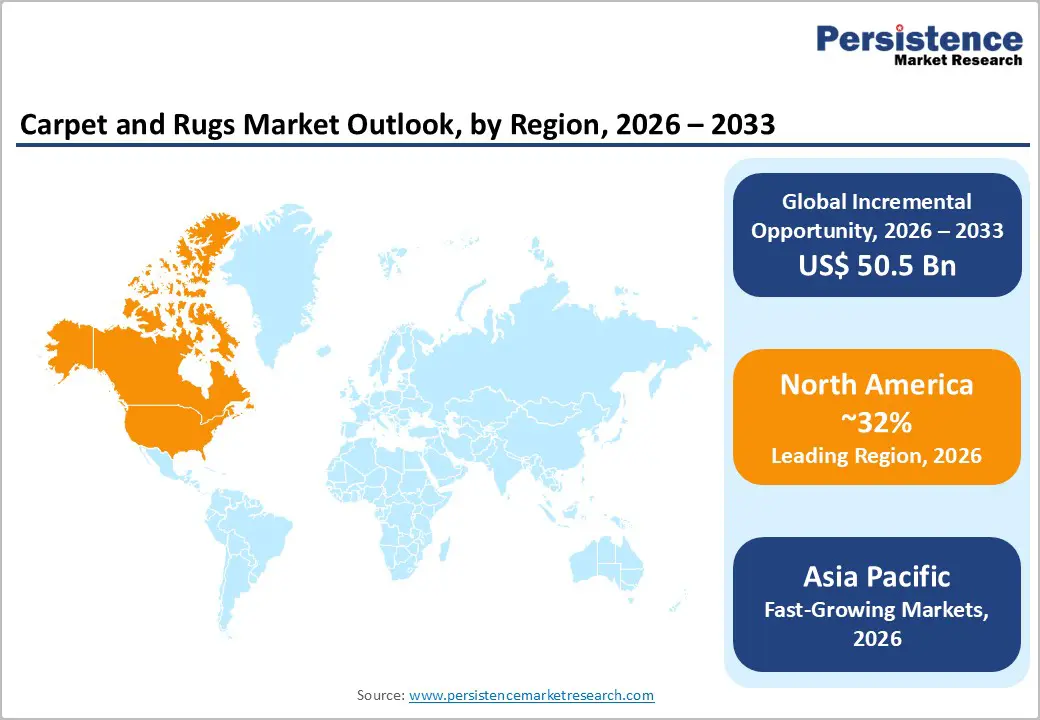

- Leading Region - North America remains the dominant region with over 32% of global revenue, driven by high per-capita renovation spending, a mature housing replacement cycle, and strong presence of major manufacturers including Mohawk Industries and Shaw Industries.

- Fastest Growing Region - Asia Pacific is the fastest-growing region, expanding at a CAGR of over 7%, propelled by rapid urbanization in China, India, and ASEAN nations, rising middle-class incomes, and a robust export-oriented manufacturing base in India's hand-knotted rug segment.

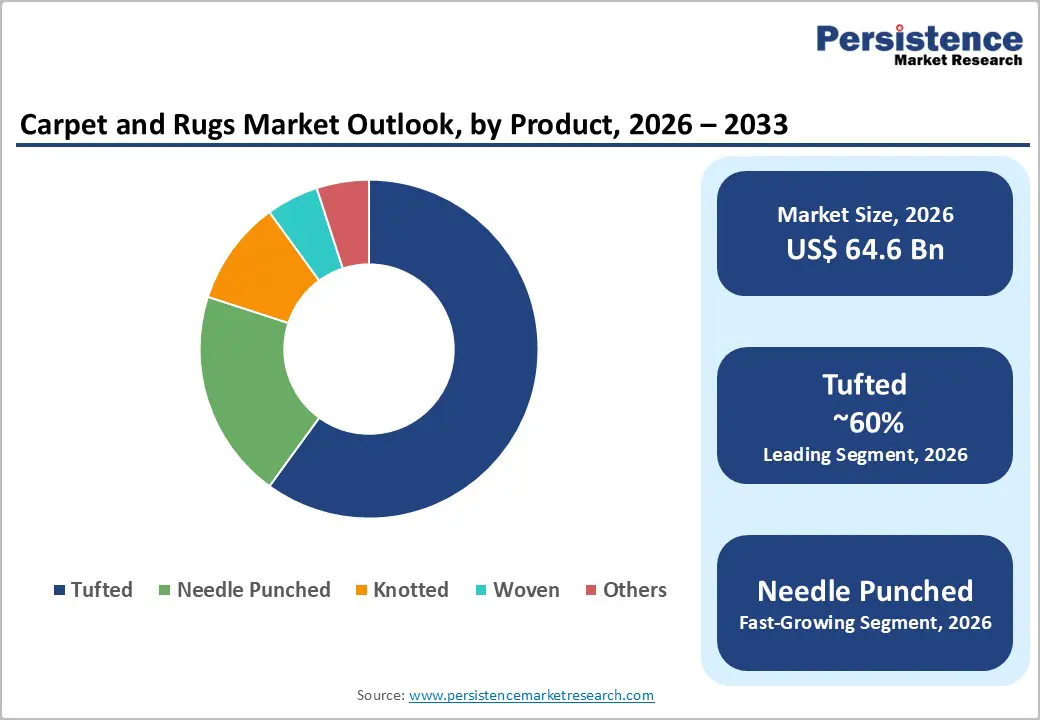

- Dominant Segment - Tufted carpets command approximately 60% market share by product type, driven by cost-effective mass production, design flexibility, compatibility with synthetic fibres, and strong adoption across both residential and commercial end-use sectors globally.

- Fastest Growing Segment - The polyester segment is projected to grow at a CAGR of 8.1% through 2033, supported by affordability, vibrant colour retention, growing availability of recycled PET-based fibres, and rising demand from eco-conscious consumers and rental residential markets.

- Key Market Opportunity - The proliferation of e-commerce and direct-to-consumer channels recording a 22% rise in online carpet sales combined with growing demand for customizable, machine-washable, and subscription-model rug offerings, presents significant revenue growth opportunity for digitally agile brands.

| Key Insights | Details |

|---|---|

| Carpet and Rugs Market Size (2026E) | US$ 64.6 Billion |

| Market Value Forecast (2033F) | US$ 115.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 8.6% |

| Historical Market Growth (2020 - 2025) | 6.5% |

DRO Analysis

Market Growth Drivers

Rising Residential and Commercial Construction Activities

The sustained boom in residential and commercial construction globally remains the most pivotal growth driver for the Carpet and Rugs market. Newly constructed homes, office complexes, hotels, educational institutions, and retail spaces consistently require flooring solutions that balance aesthetics with functionality. According to the Harvard Joint Centre for Housing Studies (JCHS), annual spending on home remodelling in the U.S. surged from USD 404 billion in 2019 to USD 611 billion in 2022 and is projected to remain above USD 600 billion through 2025.

The National Association of Realtors (NAR) noted that existing-home sales were expected to rise by 13.5% to 4.71 million units. Each home transaction triggers replacement flooring demand directly benefiting the carpet and rug segment. In emerging markets, growing infrastructure investments and urbanization in countries such as India, Vietnam, and Indonesia are creating new volume pools for carpets across both residential apartments and large commercial facilities.

Growing Consumer Preference for Interior Aesthetics and Eco-Friendly Products

Evolving consumer lifestyles, amplified by social media influence and interior design trends, have significantly elevated demand for premium, customized, and sustainable carpet and rug products. A 2024 consumer survey indicated that 73% of consumers worldwide prefer home products manufactured sustainably, supported by certifications such as LEED and BREEAM. The sustainability index for key EU markets rose by 22% in 2023.

Simultaneously, innovations such as digitally printed rugs which recorded a 41% rise in new product introduction stain-resistant coatings (present in approximately 63% of carpets launched recently), and smart carpet technologies with embedded sensors are redefining product value propositions. These factors collectively attract a broader, more quality-conscious consumer base, supporting premium pricing and higher revenue realization.

Market Restraints

Increasing Competition from Hard Surface Flooring Alternatives

The growing consumer preference for hard surface flooring including hardwood, luxury vinyl tiles (LVT), ceramic tiles, and laminate presents a persistent threat to carpet and rug adoption. According to industry data from Floor Covering News (FCNews), carpet's share of the total flooring market has declined from 62.1% a decade ago to 43.8% in 2024, a reduction of nearly 30%.

Total U.S. carpet sales fell 4.1% to USD 7.15 billion in 2024. Hardwood and tile are perceived as more hygienic, lower maintenance, and compatible with modern minimalist interiors, limiting carpet adoption particularly in high-traffic commercial environments.

Volatile Raw Material Prices and Macroeconomic Headwinds

Fluctuating costs of synthetic fibres such as nylon and polyester derived from petrochemicals along with natural materials like wool and cotton, significantly affect production economics. Additionally, macroeconomic challenges such as high interest rates dampen the housing market that underpins replacement carpet demand.

The OECD reported that headline inflation in member countries remained around 4.7% in late 2024, constraining discretionary consumer spending on non-essential home products. High mortgage rates further limit housing turnover one of the primary triggers for flooring replacement creating near-term demand headwinds in mature Western markets.

Market Opportunities

Expanding Hospitality and Commercial Sectors in Emerging Economies

The rapid expansion of hospitality, retail, and commercial real estate in emerging markets represents a high-growth opportunity for carpet and rug manufacturers. In the Middle East, Saudi Arabia's Vision 2030 initiative is driving massive investments in residential, luxury hotel, and commercial infrastructure including landmark projects such as NEOM and Red Sea Development, which generate substantial demand for high-quality floor coverings.

Similarly, India's booming hospitality and real estate sector, supported by government initiatives under Smart Cities Mission and PMAY (Pradhan Mantri Awas Yojana), is creating robust pipeline demand. Hotel renovations, airport terminal expansions, and corporate office fit-outs across Southeast Asia and GCC nations offer manufacturers the opportunity to supply premium, custom-designed carpet and rug products at higher margins.

Rise of E-Commerce and Direct-to-Consumer Channels

The rapid proliferation of e-commerce and direct-to-consumer (DTC) models is unlocking new revenue streams for carpet and rug brands. Online channels have seen a 22% rise in carpet sales, with 48% of newly launched products now offering customization tools enabling consumers to select colour palettes, patterns, and sizes online.

Companies like Ruggable LLC and Rugs USA have pioneered machine-washable and custom-sized rug offerings through DTC channels, disrupting traditional retail models. In February 2024, Rugs USA launched its 'Custom by Rugs USA' program in collaboration with Shaw Industries, enabling made-to-measure rug orders. The DTC model reduces distribution costs, improves margin capture, and enables personalized consumer engagement creating differentiation in an increasingly competitive landscape.

Category-wise Analysis

Product Type Insights

The tufted segment is the leading product type in the global Carpet and Rugs market, commanding approximately 60% of the overall market share. Tufted carpets are manufactured by inserting yarn loops into a primary backing material process that enables high-volume output at significantly lower costs compared to woven or knotted alternatives. According to data from the global carpet trade, world trade in tufted rugs was valued at approximately USD 7.21 billion in 2022.

In North America alone, the tufted segment generated revenues of USD 8.3 billion in 2024, reinforcing its dominance. The segment benefits from design versatility offering a wide range of textures, pile heights, and colour options making it suitable for both residential and commercial applications. The availability of advanced stain-resistant treatments and synthetic fiber compatibility further enhances the functional appeal of tufted carpets, particularly in high-traffic areas such as offices, hotels, retail spaces, and multi-family housing developments.

Material Type Insights

Nylon dominates the material segment of the global Carpet and Rugs market, accounting for approximately 41% of the overall market share. Nylon's supremacy is attributed to its exceptional durability, resilience, and stain resistance properties that make it the fiber of choice for high-traffic residential and commercial applications. According to industry analysis, nylon carpets and rugs accounted for a revenue share of 41.25% in 2025. The fibber’s ability to recover from compression and maintain structural integrity over time gives it a competitive edge over polyester and polypropylene in premium market segments.

Continuous innovation in solution-dyeing techniques and the growing adoption of recycled nylon which aligns with circular economy principles and LEED certification requirements for commercial interiors further reinforces nylon's market position. Key players such as Interface, Inc. have earmarked capital specifically toward expanding capacity for 100% recycled nylon carpet tile production.

End Use Insights

The residential segment dominates the global Carpet and Rugs market by end use, holding approximately 61-67% of total market share. This leadership is rooted in the universal consumer desire for comfort, thermal insulation, acoustic performance, and interior aesthetics within living spaces. Post-pandemic behavioural shifts with homeowners converting living areas into multi-functional environments, including home offices, gyms, and classrooms, have reinvigorated demand for soft flooring solutions.

In North America, the residential segment represented 72% of the market in 2024, driven by rising renovation spending. The Harvard Joint Centre for Housing Studies reports that U.S. homeowners collectively spent approximately USD 827 billion on remodelling over two years through 2023. The commercial sub-segment, including offices, hospitality, retail, and healthcare, continues to generate incremental volume, particularly as hybrid work models drive office redesign and hotel refurbishments necessitate regular carpet replacement.

Regional Analysis

North America Carpet and Rugs Market Trends

North America remains the largest regional market for Carpet and Rugs globally, led by the United States, which accounted for approximately 74% of the regional market share with revenues of USD 9.8 billion in 2024. The U.S. market benefits from a mature housing stock with consistent replacement cycle demand, strong remodelling activity, and a well-developed distribution infrastructure. The Joint Centre for Housing Studies (JCHS) at Harvard confirmed that remodelling expenditures in the U.S. are projected to remain above USD 600 billion through 2025.

The U.S. innovation ecosystem in flooring continues to set global benchmarks. In February 2025, Shaw Floors launched the Pet Perfect+ lineup featuring LifeGuard Spill-Proof technology combined with ANSO High-Performance fibres and R2X stain-and-soil protection.

Asia Pacific Carpet and Rugs Market Trends

Asia Pacific is the fastest-growing region in the global Carpet and Rugs market, with key expansion driven by China, India, and Southeast Asian nations. China dominates the regional landscape, holding approximately 37.6% of the Asia Pacific market share in 2024, supported by its massive urbanization drive and rapidly growing middle-class population. Urban population in Indonesia reached 59.2% in 2024 (World Bank), illustrating the urbanization-led demand trend across the region.

India stands out as a unique dual-role player, both a significant consumer market and a global manufacturing powerhouse for hand-knotted and tufted rugs, with clusters in Rajasthan and Uttar Pradesh serving as major export hubs. In July 2025, Jaipur-headquartered startup Asterlane expanded into carpet manufacturing, blending traditional craftsmanship with modern design sensibilities.

Europe Carpet and Rugs Market Trends

Europe is the second-largest market for Carpet and Rugs, accounting for approximately 31.5% of global revenue in 2025. The region benefits from robust housing renovation activity, stringent sustainability mandates, and a strong design heritage across key markets including Germany, the U.K., France, and Spain. Germany's position as a manufacturing and design hub drives innovation in digitally printed and modular carpet products aligned with EU sustainability directives.

In December 2024, Brintons a heritage U.K.-based carpet brand launched its first collection in collaboration with the V&A Museum, featuring designs inspired by French artist Emile-Allain Séguy's works. Such collaborations between carpet manufacturers and cultural institutions reflect Europe's emphasis on design differentiation and premium positioning. Regulatory harmonization under the EU Green Deal and Extended Producer Responsibility (EPR) frameworks are pushing manufacturers toward circular economy models, including recyclable backing technologies and reduced-VOC manufacturing creating both compliance challenges and innovation opportunities.

Competitive Landscape

The global carpet and rugs market exhibits a moderately fragmented structure, with a mix of large vertically integrated multinationals and numerous regional and niche specialists. The top 5 players, including Mohawk Industries and Shaw Industries, collectively account for approximately 20% of the global market. Market leaders are investing heavily in R&D focused on sustainable fibres, digital printing, and smart textiles. Key differentiators include proprietary fiber technologies (e.g., SmartStrand by Mohawk), eco-certified backing systems (e.g., EcoWorx by Shaw), and omnichannel distribution models.

Key Developments:

- In July 2025, Jaipur-headquartered home décor and lifestyle startup Asterlane expanded into carpet manufacturing, marking a strategic broadening of its product portfolio to tap into the growing demand for contemporary and traditional floor décor in India’s interiors market.

- In May 2025, Oriental Weavers launched a polyester yarn dyeing unit to boost in-house yarn capacity, reflecting vertical integration efforts that align with growth strategies. Interface has made a significant investment of USD 45 million to expand modular carpet tile production utilizing 100% recycled nylon, combining innovation and sustainability.

Companies Covered in Carpet and Rugs Market

- Jaipur Rugs

- Carpet Planet

- Mohawk Industries, Inc.

- Anderson Tuftex (Shaw Industries Inc.)

- Beaulieu International Group

- Rugs USA

- Ruggable LLC

- Kaleen

- The Natural Carpet Company

- The Dixie Group

- Interface, Inc.

- Mannington Mills

- Oriental Weavers Carpet Co.

- Balta Industries NV

- Tarkett Group

- Victoria PLC

- Tai Ping Carpets International Ltd.

Frequently Asked Questions

The global Carpet and Rugs market is projected to reach US$ 115.1 Billion by 2033, up from an estimated US$ 64.6 Billion in 2026, growing at a CAGR of 8.6% during the 2026-2033 forecast period.

Primary growth drivers include sustained residential and commercial construction activity, rising consumer expenditure on home renovation (U.S. remodelling spending remained above USD 600 billion through 2025 per JCHS), growing urbanization especially across Asia Pacific (45% urban population globally per UN World Urbanization Prospects 2025), and innovations in eco-friendly, stain-resistant, and digitally customizable carpet and rug products.

The tufted segment is the leading product type, holding approximately 60% of the global market share. Its dominance is attributed to cost-effective mass production processes, superior design flexibility, and widespread adoption across both residential and commercial end uses worldwide.

North America is the leading region, accounting for approximately 32% of the global market, with the United States as the primary driver. High per-capita home renovation spending, a well-established manufacturing base anchored by companies like Mohawk Industries and Shaw Industries, and strong demand for premium sustainable carpets underpin regional market leadership.

Prominent companies operating in the global Carpet and Rugs market include Mohawk Industries, Inc. (market leader with over 6% global share), Shaw Industries Group (Anderson Tuftex), Jaipur Rugs, Beaulieu International Group, Ruggable LLC, Rugs USA, The Dixie Group, Interface, Inc., Oriental Weavers, Kaleen, and Tarkett Group, among others.