- Electrical Equipment & Services

- C4ISR Market

C4ISR Market Size, Share, and Growth Forecast, 2026 - 2033

C4ISR Market by Platform (Land, Space, Others), Component (Hardware, Software, Services), Application (Intelligence Surveillance & Reconnaissance, Command & Control, Others), and Regional Analysis 2026 - 2033

C4ISR Market Size and Trends Analysis

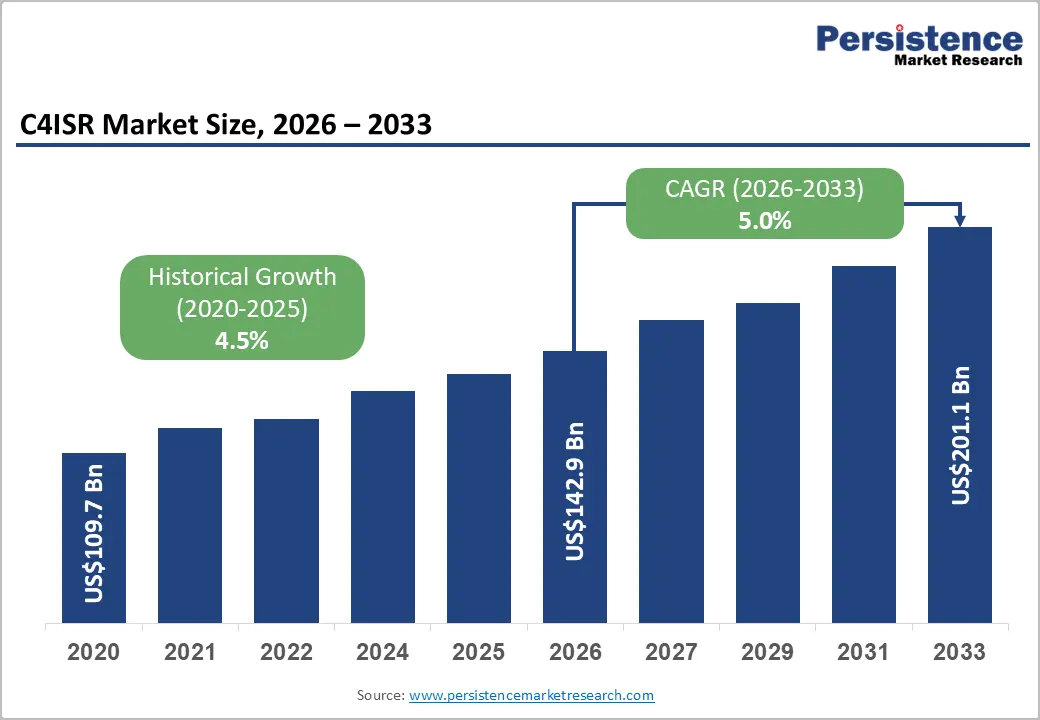

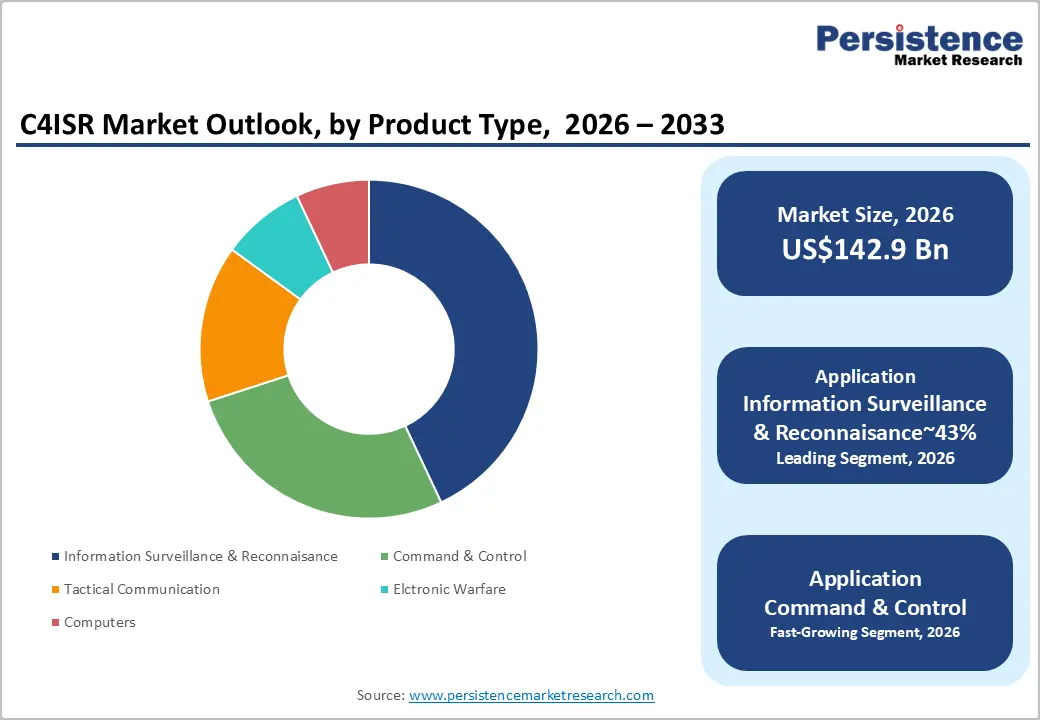

The global C4ISR Market size is likely to be valued at US$142.9 billion in 2026 and is expected to reach US$201.1 billion by 2033, growing at a CAGR of 5.0% during the forecast period from 2026 to 2033, driven by increased procurement of advanced intelligence, surveillance, and communication systems as defense forces prioritize network-centric and multi-domain operations.

Military organizations are focusing on interoperability across diverse tactical communication frameworks, which is further accelerating demand for integrated platforms. Rising investments in resilient digital infrastructure and advancements in sensor technologies and data fusion are supporting market expansion. Increasing geopolitical tensions continue to reinforce the need for enhanced situational awareness capabilities.

Key Industry Highlights:

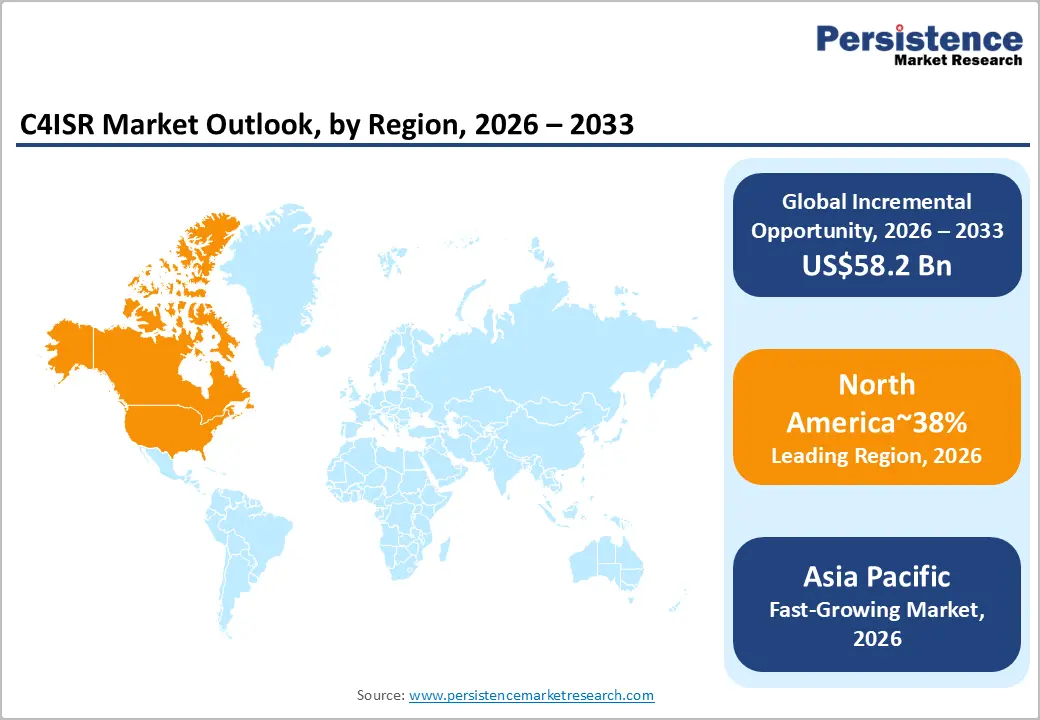

- Leading Region: North America is projected to lead, accounting for approximately 38% share in 2026, supported by robust institutional defense budgets and established procurement pipelines.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, driven by territorial security initiatives and accelerating regional military modernization programs.

- Leading Platform: Land is expected to lead, accounting for approximately 31% share in 2026, anchored by persistent ground force upgrades and mobile command center requirements.

- Leading Application: Intelligence Surveillance & Reconnaissance (ISR) is projected to dominate, holding approximately 43% share in 2026, driven by continuous situational awareness demands and persistent surveillance requirements.

| Key Insights | Details |

|---|---|

|

C4ISR Market Size (2026E) |

US$142.9 Bn |

|

Market Value Forecast (2033F) |

US$201.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Multi-Domain Integration Requirements

Modern military doctrines heavily prioritize multi-domain operational convergence across allied forces. This strategic shift necessitates seamless data exchange between disparate warfare platforms. Converging threats necessitate seamless data sharing to enable rapid decision-making in contested environments. This structural shift reinforces procurement across joint forces seeking operational superiority. Commanders require unified operational pictures to orchestrate complex joint force maneuvers. Disconnected legacy networks create critical vulnerabilities during rapid tactical engagements. Therefore, defense agencies actively mandate cross-domain communication standards within new procurements.

Integrated network architectures resolve these operational silos through standardized data protocols. Lockheed Martin, with C2BMC, illustrates this transition toward unified theater-level coordination. Software-defined routing systems dynamically allocate bandwidth across contested electromagnetic environments. Northrop Grumman, with IBCS, provides modular command frameworks supporting joint engagements. Raytheon with RIOTS 2.0 integrates real-time intelligence feeds into command systems for enhanced battlespace awareness. Such advancements sustain uptake as militaries prioritize networked capabilities over siloed solutions. This convergence of sensors and effectors fundamentally accelerates threat response timelines.

Advanced Real-Time Tactical Data and Communication Resilience

Exponential growth in sensor-generated data has created critical pressure on traditional analytical architectures, as manual processing fails to deliver actionable insights within compressed operational windows. Tactical forces require instantaneous environmental awareness to sustain mission effectiveness, particularly in hostile or rapidly evolving theaters. Delays in information dissemination undermine decision superiority and jeopardize forward-deployed units, making high-throughput, low-latency processing infrastructure a strategic necessity. Upgraded computing architectures, including distributed server frameworks and edge processing nodes, enable localized analysis directly at the operational perimeter, reducing reliance on centralized data centers and mitigating latency risks. These advancements also support continuous situational awareness, allowing commanders to integrate multi-source intelligence streams into real-time decision cycles under severe operational constraints.

Decentralized computing is complemented by resilient communication systems capable of withstanding electronic warfare, cyber threats, and spectrum congestion. Frequency-agile waveforms and adaptive networking platforms provide secure voice and data transmission across contested environments, preserving connectivity during high-intensity operations. Integration of edge-enabled processing with deployable, adaptive communication networks accelerates frontline information sharing, strengthens command-and-control structures, and maintains operational tempo. These combined capabilities create a technologically sophisticated ecosystem in which data processing and secure communications mutually reinforce tactical effectiveness, shaping investment priorities across defense technology suppliers and battlefield infrastructure planners.

Restraint Analysis - Legacy System Interoperability Hurdles

Decades of fragmented procurement strategies leave defense agencies managing disjointed infrastructures. Older proprietary communication protocols resist integration into modern digital networking ecosystems. Upgrading these isolated systems demands extensive custom engineering and integration efforts. Physical hardware constraints limit retrofitting options for aging combat vehicle platforms. These structural integration bottlenecks systematically delay comprehensive digital transformation timelines.

Financial resource allocation heavily skews toward maintaining these outdated operational platforms. Leonardo, with SWave tactical radios, attempts to bridge these generational technology gaps. Extensive customized middleware development drains budgets initially designated for innovation programs. General Dynamics with Mission System architectures encounters friction when connecting archaic nodes. This technical inertia prevents the rapid deployment of next-generation unified command capabilities.

Escalating Cybersecurity Vulnerabilities in Defense Networks

The expansion of digital network footprints across modern defense architectures has proportionally increased exposure to advanced persistent threats, making critical intelligence and strategic communications highly vulnerable. Weaponized malware targeting industrial control systems within military installations magnifies operational risk, while continuous probing of network nodes exploits architectural weaknesses. Ensuring secure connectivity across distributed command, control, communications, computers, intelligence surveillance, and reconnaissance (ISR) systems requires persistent cryptographic enhancement and real-time threat monitoring. Failure to address these vulnerabilities compromises mission data integrity and undermines operational effectiveness, necessitating integrated cybersecurity protocols across all hardware and software layers.

Implementing these measures imposes substantial developmental and operational burdens on system integrators. Rheinmetall with TacNet and Indra with Lanza 3D radar systems exemplify solutions requiring continuous patching, zero-trust architectures, and advanced encryption to mitigate spoofing and infiltration risks. Lifecycle maintenance costs escalate as interoperability expansions create broader attack surfaces, while extended testing and validation cycles, such as those experienced by Northrop Grumman with IBCS, delay platform rollouts and constrain active deployment utilization. These dynamics collectively reinforce cybersecurity as a critical structural restraint on defense network modernization and operational readiness.

Opportunity Analysis - AI-Enabled Predictive Analytics Driving Defense Modernization

The growing imperative for anticipatory intelligence is creating structural demand for AI-enabled predictive analytics capable of processing vast, heterogeneous datasets into actionable foresight. Data-centric warfare policies are accelerating the adoption of edge computing platforms in forward-deployed operations, enabling autonomous decision aids to function within compressed operational timelines. Algorithmic pattern recognition identifies subtle threat indicators concealed within routine surveillance feeds, while automated intelligence triage reduces analyst cognitive load across multi-source inputs. Predictive models further forecast adversary movements based on historical operational patterns, enhancing operational tempo and strategic planning. This evolution reinforces investment in AI infrastructure as a core enabler of modernization and battlefield decision superiority.

Providers operationalize these capabilities by embedding scalable algorithms directly into command software and sensor pipelines. BAE Systems with TITAN leverages AI for all-source data fusion supporting army modernization, while BAE Systems with Intelligence Data Suite accelerates targeting through rapid machine learning-driven insights. Lockheed Martin, with AI Aegis, enhances combat system responsiveness against high-speed threats, and automated translation modules support coalition intelligence interoperability. Collectively, this integration of autonomous cognitive processing into hardware and software architectures establishes AI as a structural procurement requirement for contemporary and future defense operations.

Cloud-Based Tactical Networks

Decentralized cloud architectures provide scalable infrastructure for dynamic military operational requirements. Distributed server networks ensure data redundancy during targeted attacks on physical facilities. Cloud environments facilitate seamless information access across geographically separated command echelons. Virtualized network functions reduce the physical hardware footprint required in mobile headquarters. Establishing these secure digital environments creates continuous revenue streams for service providers.

Enterprise technology vendors partner with defense contractors to harden commercial cloud solutions. Northrop Grumman with Forward Edge implements virtualized command environments for expeditionary forces. Encrypted data lakes consolidate intelligence feeds for comprehensive strategic analysis protocols. RTX with Multi-Domain System architectures leverages distributed cloud resources for coordinated engagements. This transition away from localized servers reshapes underlying procurement and maintenance budgets.

Category–wise Analysis

Platform Insights

The land segment is expected to lead, accounting for approximately 31% share in 2026, reinforced by sustained ground force modernization programs. Tactical terrestrial units require uninterrupted connectivity during complex distributed military operations. Mobile command centers demand ruggedized hardware capable of enduring severe environmental conditions. This operational necessity drives continuous procurement of vehicle-mounted communication network nodes.

Robust sensor networks accelerate critical decision cycles for forward-deployed infantry battalions. L3Harris, with Falcon IV radios, exemplifies tactical voice and data workflow integration. Defense ministries consistently allocate substantial budgets toward terrestrial network infrastructure resilience. Upgraded electronic warfare modules protect maneuvering ground forces from adversarial spectrum interference. These combined capabilities establish terrestrial segments as foundational defense pillars globally.

The space segment is anticipated to be the fastest-growing, driven by critical requirements for resilient global surveillance coverage. Orbital platforms provide unhindered strategic observation capabilities across denied or hostile territories. Low Earth Orbit satellite constellations significantly reduce data transmission latency for commanders. Lockheed Martin, with LM 400 satellite buses, illustrates this transition toward rapid deployment. Hardened satellite communications ensure continuous connectivity when terrestrial networks experience catastrophic failures.

Defense agencies increasingly prioritize space domain awareness to protect critical orbital infrastructure. This shifting strategic focus accelerates investments in orbital intelligence and communication frameworks.

Application Insights

Intelligence surveillance & reconnaissance (ISR) is anticipated to dominate, holding approximately 43% share in 2026, driven by continuous situational awareness demands across all theaters. Anticipatory defense postures require persistent observation to detect adversarial mobilization efforts early. High-resolution geospatial imaging provides foundational maps for tactical planning and target acquisition. Airborne surveillance platforms gather essential electronic intelligence regarding enemy radar installations.

Northrop Grumman, with Global Hawk, delivers persistent high-altitude strategic intelligence gathering capabilities. Signal interception networks monitor hostile communications to identify hidden organizational structures. Leonardo with Osprey AESA radar exemplifies advanced targeting and surveillance for maritime environments. Continuous intelligence collection forms the prerequisite basis for any subsequent military engagement. Defense doctrines prioritize information superiority to maintain tactical advantages during conflict scenarios. This foundational role ensures surveillance capabilities consistently secure maximum institutional funding allocations.

The command & control sgement is expected to be the fastest-growing, as complex multi-domain operations require synchronized execution frameworks. Disconnected tactical elements cannot effectively concentrate combat power without unified centralized orchestration. Modern warfare demands instantaneous coordination between naval, aerial, and terrestrial combat assets. Lockheed Martin, with C2BMC, provides this essential synchronization across distributed missile defense networks.

Automated battle management systems reduce the cognitive load on commanders during engagements. Saab with 9LV Combat Management System integrates diverse shipboard weapons into unified interfaces. Cloud-based tactical headquarters allow leaders to disperse physically while maintaining operational control. Secure data links consolidate diverse intelligence feeds into single interactive situational displays. As operations become more distributed, robust coordination platforms become critical failure points. This necessity for seamless operational orchestration accelerates investments in advanced management systems.

Regional Insights

Asia Pacific C4ISR Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as rising geopolitical tensions accelerate market expansion across regional defense networks. Territorial disputes prompt rapid investments in maritime domain awareness and border surveillance. Economic expansion enables significant increases in sovereign defense capital expenditure across developing nations. Coastal security initiatives necessitate the deployment of advanced radar and signal interception arrays.

Regional militaries actively transition from legacy analog systems toward integrated digital battlefield architectures. Infrastructure scaling supports proliferated sensor networks over vast areas. Urbanization concentrates demand in joint training facilities.

India drives acceleration via indigenous defense corridors promoting local C4ISR manufacturing. Atmanirbhar Bharat initiatives fund networked systems for border surveillance. Bharat Electronics, with Akash NG, integrates radar data for air defense. Investments in quad partnerships enhance interoperability standards. Bilateral security agreements accelerate the integration of allied communication standards within domestic forces. L3Harris with Falcon IV addresses critical requirements for secure tactical interoperability during joint exercises.

Expanding maritime patrol operations demand enhanced persistent surveillance networks to monitor vast territories. Domestic defense manufacturing initiatives support localized production of essential intelligence processing hardware.

North America C4ISR Market Trends

North America is expected to remain the leading regional market, accounting for approximately 38% share in 2026, supported by concentrated defense spending, vendor innovation hubs, and mature integration standards. Dense procurement pipelines fund multi-year programs for joint operations. This consistent funding sustains extensive procurement across complex tactical communication nodes. Operational readiness requirements accelerate the deployment of next-generation command and control infrastructure.

Cross-domain integration initiatives demand continuous upgrades to secure continental defense perimeters effectively. Technology adoption embeds AI across platforms, enhancing data dominance in exercises. Policy alignment sustains high utilization through sustained budgets.

The U.S. is projected to anchor regional dominance through sustained investments in Joint All-Domain Command and Control frameworks. Government-led defense initiatives mandate seamless interoperability across all active military branches domestically. Lockheed Martin with C2BMC benefits directly from these massive federal digital modernization appropriations. Raytheon, with NGWS, benefits from F-35 integration contracts emphasizing sensor fusion.

Regulatory frameworks around spectrum allocation reinforce secure comms procurement. Domestic procurement policies strengthen local defense contractors while expanding secure supply chains. Persistent global security obligations necessitate continuous technological superiority across all deployed network assets.

Europe C4ISR Market Trends

Europe is expected to remain a mature and structurally stable regional market, approximating a stable share, with demand primarily anchored in NATO interoperability upgrades and replacement cycles. Collaborative frameworks drive standardized platforms for collective defense. Aging inventories necessitate refreshes with resilient electronics. Service contracts expand as alliances prioritize cyber-hardened networks. Multinational coalition exercises require standardized data exchange protocols to ensure operational cohesion. Border security enhancements drive sustained investments in persistent territorial surveillance sensor networks.

The U.K. sustains momentum through commitments to integrated air and missile defense under AUKUS pillars. Ministry of Defense budgets target C4ISR enhancements for carrier strike groups. BAE Systems, with Tempest sensors, aligns with future combat air programs. Export controls tighten around dual-use tech, spurring domestic production. Joint military initiatives encourage the deployment of software-defined networking across expeditionary forces. Heightened regional threat perceptions maintain steady procurement momentum for upgraded command capabilities.

Competitive Landscape

The global C4ISR market exhibits a highly consolidated structure, dominated by established tier-one defense contractors and specialized aerospace integrators. This concentration results directly from the immense capital requirements necessary for complex systems engineering. Leading entities maintain vast functional influence through deeply entrenched relationships with global defense ministries. BAE Systems, with the Intelligence Data Suite, and Lockheed Martin, with C2BMC, establish critical functional benchmarks for multi-domain orchestration. However, major prime contractors generally absorb these innovators to expand their proprietary platform capabilities. Strict security clearances and regulatory compliance frameworks create formidable barriers preventing new market entrants.

Competitive positioning relies heavily upon horizontal integration, combining discrete sensor feeds into unified battle management platforms. Premium vendors differentiate through comprehensive ecosystem support, delivering end-to-end network resilience and continuous cryptographic updates. RTX with RIwP demonstrates vertical capability by integrating threat detection directly with kinetic response mechanisms. Moving forward, competitive intensity is positioned to center around open-architecture software capabilities and cloud-based tactical network deployments. Vendors prioritizing modular, upgradable architectures will systematically outpace providers reliant on static legacy hardware configurations.

Key Industry Developments:

- In March 2026, Northrop Grumman convened its 2026 Integrated Battle Command System (IBCS) Supplier Summit on Capitol Hill. The summit emphasized the move toward "Any Sensor, Best Shooter" capabilities, solidifying the IBCS as the central nervous system for the U.S. Army’s multi-domain operations.

- In January 2026, RTX (Raytheon) secured a US$197 million contract from the U.S. Air Force for the MS-110 airborne reconnaissance system for Poland. This marks a major expansion of NATO’s eastern flank surveillance capabilities, providing high-resolution, long-range multispectral imagery to allied forces.

Companies Covered in C4ISR Market

- Lockheed Martin

- Raytheon Technologies

- Northrop Grumman

- Bharat Electronics

- BAE Systems

- L3Harris Technologies

- Boeing

- Thales Group

- Leonardo

- Rheinmetall

- Elbit Systems

- Israel Aerospace Industries

- General Dynamics

- Saab AB

- Indra Sistemas

- Leonardo S.p.A.

Frequently Asked Questions

The global C4ISR Market is projected to be valued at US$142.9 billion in 2026 and is expected to reach US$201.1 billion by 2033, driven by multi-domain integration requirements, advanced real-time tactical data processing, and rising defense modernization initiatives.

Modern military doctrines demand seamless interoperability across land, air, naval, and space platforms. Unified operational pictures and standardized communication protocols enable rapid decision-making in contested environments, prompting continuous procurement of integrated command, control, communication, computers, intelligence, surveillance, and reconnaissance systems.

The C4ISR Market is forecast to grow at a CAGR of 5.0% from 2026 to 2033, reflecting steady expansion fueled by AI-enabled predictive analytics, cloud-based tactical networks, and advanced sensor-data fusion capabilities.

North America is projected to lead with approximately 38% share in 2026 due to robust defense budgets and established procurement pipelines, while Asia Pacific is expected to grow fastest, driven by military modernization programs, border security initiatives, and indigenous defense manufacturing.

The C4ISR Market is highly consolidated, dominated by tier-one defense contractors and aerospace integrators, including Lockheed Martin, Raytheon Technologies, Northrop Grumman, BAE Systems, Bharat Electronics, L3Harris Technologies, Thales Group, Leonardo, and Rheinmetall, competing through advanced platform integration, software innovation, and secure multi-domain solutions.