- Hardware & Software IT Services

- Building Management System Market

Building Management System Market Size, Share, and Growth Forecast 2026 - 2033

Building Management System Market by System Type (HVAC Control Systems, Lighting Control Systems, Energy Management Systems, Security & Access Control Systems, Fire & Life Safety Systems, Elevator & Escalator Management, Water & Waste Management Systems), End-user (New Construction, Retrofit), Application (Residential Buildings, Commercial Buildings, Industrial Facilities, Institutional Buildings, Government & Public Infrastructure), by Regional Analysis, 2026 - 2033

Building Management System Market Size and Trend Analysis

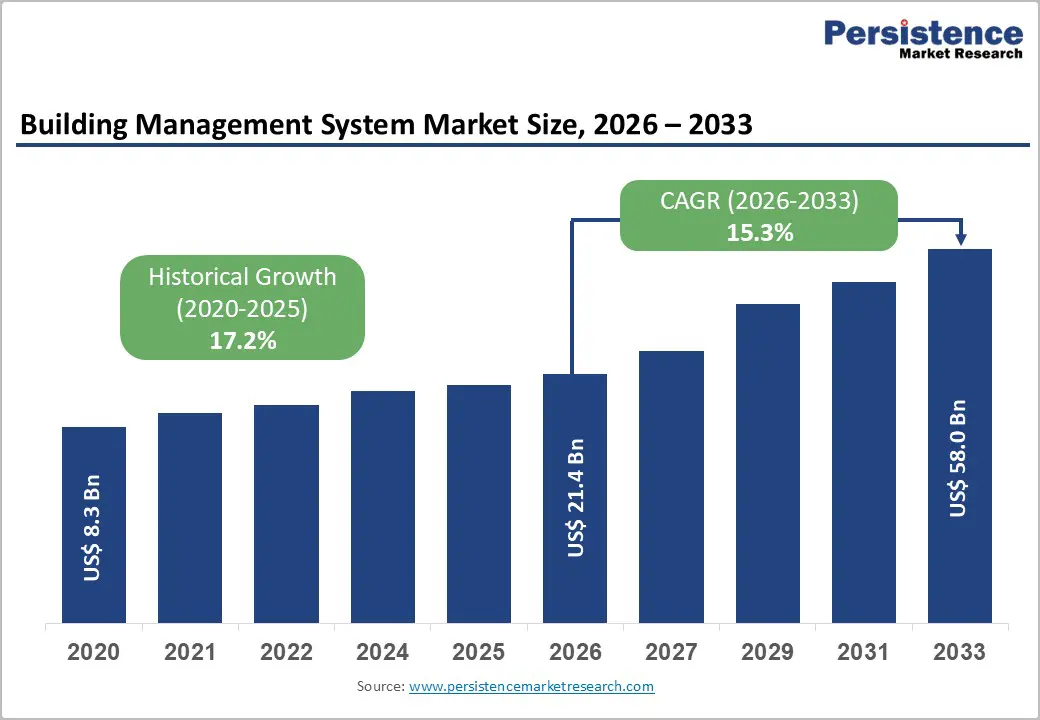

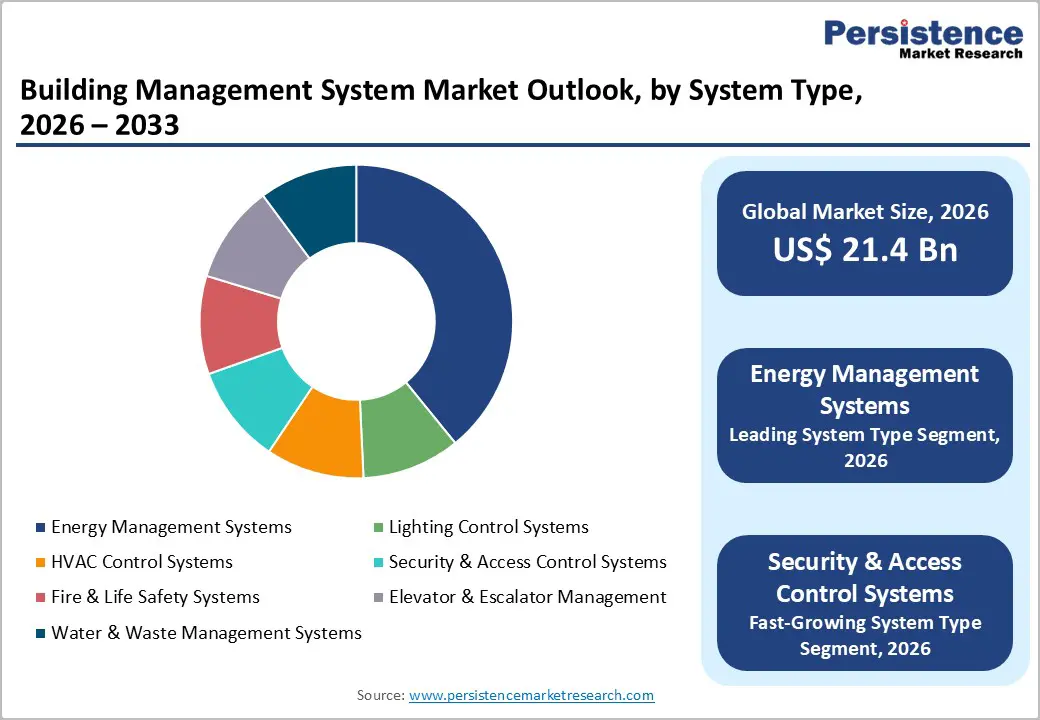

The global building management system market size is expected to be valued at US$ 21.4 billion in 2026 and projected to reach US$ 58.0 billion by 2033, growing at a CAGR of 15.3% between 2026 and 2033.

This robust expansion is primarily driven by escalating global energy efficiency mandates, the rapid proliferation of smart building and IoT-enabled technologies, and rising urbanization across emerging and developed economies. Governments worldwide are instituting stringent building energy codes, including ASHRAE 90.1 in the United States and the EU's Energy Performance of Buildings Directive (EPBD), compelling facility managers to adopt integrated BMS platforms. The convergence of cloud computing, artificial intelligence, and sensor-driven automation is enhancing operational efficiencies, reducing carbon footprints, and lowering lifecycle costs for commercial and industrial building operators.

Key Industry Highlights

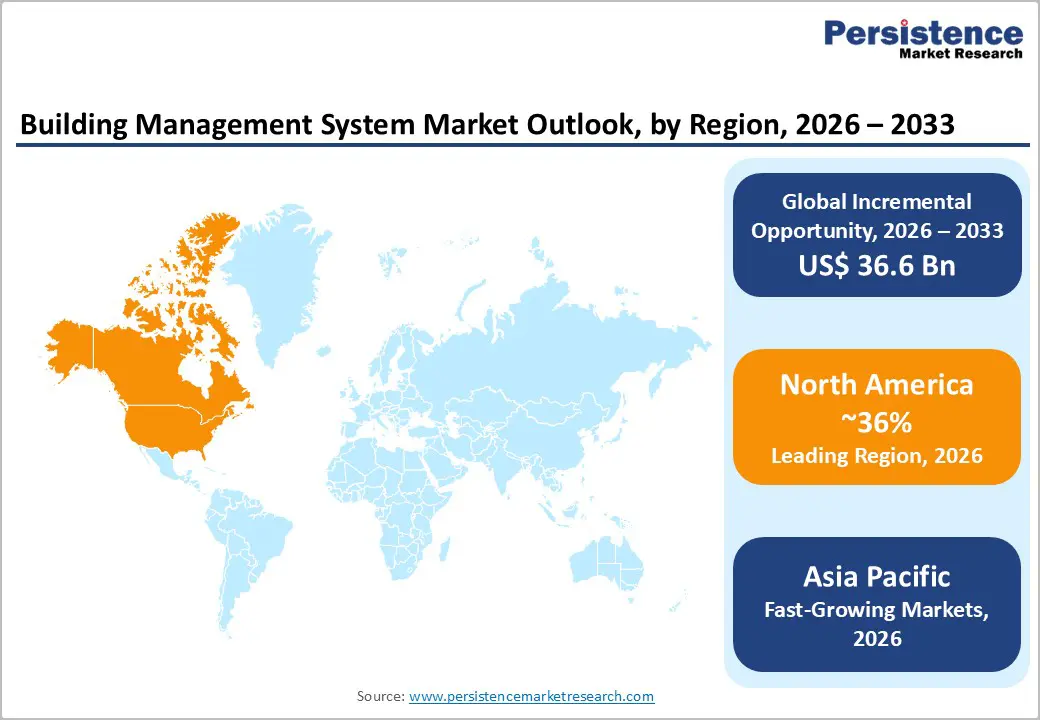

- Leading Region: North America dominated the global BMS market in 2025 with approximately 36% revenue share, supported by stringent ASHRAE standards, EPA's ENERGY STAR program, and high commercial real estate technology adoption rates across the U.S. and Canada.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional BMS market, driven by China's green building mandates under the 14th Five-Year Plan, India's Smart Cities Mission, and rapid commercial construction activity across ASEAN nations through 2033.

- Dominant Segment: Commercial Buildings led the application segment with approximately 43% market share in 2025, driven by energy-intensive mechanical systems, LEED certification incentives, and rising demand for integrated smart office environments.

- Fastest Growing Segment: The Security & Access Control Systems segment is the fastest-growing system type, reflecting heightened enterprise focus on integrated physical security, cybersecurity convergence, and evolving post-pandemic access management requirements globally.

- Key Market Opportunity: The global building retrofit market presents a significant long-term opportunity, as approximately 80% of 2050's building stock already exists, with ESG mandates and IEA energy efficiency targets compelling widespread legacy system upgrades worldwide.

| Key Insights | Details |

|---|---|

| Building Management System Market Size (2026E) | US$ 21.4 Billion |

| Market Value Forecast (2033F) | US$ 58.0 Billion |

| Projected Growth CAGR (2026 - 2033) | 15.3% |

| Historical Market Growth (2020 - 2025) | 17.2% |

Market Dynamics

Drivers - Stringent Energy Efficiency Regulations and Net-Zero Building Mandates

Buildings account for approximately 40% of total global energy consumption and nearly 33% of global greenhouse gas (GHG) emissions, according to the International Energy Agency (IEA). Regulatory bodies across the globe are setting ambitious net-zero energy building (NZEB) targets to curb these figures. In the United States, the Department of Energy's (DOE) Better Buildings Initiative has partnered with over 900 organizations to improve energy efficiency by at least 20%, while the EU's revised Energy Performance of Buildings Directive (EPBD 2024) mandates that all new buildings be zero-emission by 2030. Building Management Systems serve as the central nervous system for achieving these regulatory targets by optimizing HVAC, lighting, and energy consumption across building portfolios. The growing regulatory pressure is compelling both commercial real estate developers and institutional building operators to invest in comprehensive BMS platforms, directly fueling market demand and reinforcing long-term growth trajectories.

Rapid Adoption of IoT and Smart Building Technologies

The integration of the Internet of Things (IoT) with building automation has fundamentally transformed how facilities are monitored and managed. According to the International Telecommunication Union (ITU), there were approximately 15.9 billion active IoT devices worldwide in 2023, with projections indicating this figure could exceed 29 billion by 2030. Smart building platforms leverage real-time sensor data to enable predictive maintenance, occupancy-based climate control, and automated energy load balancing, reducing operational costs by up to 30%, according to the World Green Building Council. IoT-enabled BMS solutions eliminate manual intervention, reducing human error and enabling facility managers to remotely oversee multi-site building portfolios. The combination of declining sensor costs, improved wireless connectivity (5G), and AI-driven analytics is accelerating the adoption of next-generation BMS platforms across commercial, industrial, and residential segments worldwide.

Restraints - High Initial Capital Investment and System Integration Complexity

Despite evident long-term cost benefits, the high upfront capital expenditure required to deploy comprehensive building management systems remains a significant barrier, particularly for small and medium-sized enterprises (SMEs) and developing economies. A full-scale BMS installation encompassing HVAC, energy, security, and fire safety subsystems can require substantial investment per square foot, often discouraging building owners from adopting holistic platforms. Integrating disparate legacy systems, many of which operate on proprietary protocols, with modern IP-based BMS infrastructure adds further complexity and cost. Issues related to interoperability between older HVAC controllers, fire panels, and new cloud-based BMS software are frequently cited by facility managers as major implementation challenges, significantly slowing market penetration, especially in retrofit applications across emerging economies.

Cybersecurity Vulnerabilities in Connected Building Infrastructure

As Building Management Systems become increasingly networked and internet-connected, they are simultaneously becoming high-value targets for cybercriminals. The U.S. Cybersecurity and Infrastructure Security Agency (CISA) has issued multiple advisories warning of vulnerabilities in building automation system (BAS) protocols, including BACnet and Modbus, which are widely deployed in commercial facilities. A notable 2021 incident involving a water treatment facility in Florida demonstrated how compromised building automation infrastructure can lead to potentially life-threatening scenarios. Inadequate cybersecurity measures can expose critical building operations to unauthorized access, ransomware attacks, and data breaches, prompting enterprises to factor additional security investments into BMS deployment budgets, thereby increasing the total cost of ownership and potentially delaying purchasing decisions across enterprise segments.

Opportunities - Smart City Infrastructure Development and Government-Led Building Modernization Programs

The global proliferation of smart city initiatives represents a transformative growth opportunity for BMS market participants. Governments across the Asia Pacific, the Middle East, and Europe are channeling significant public investment into intelligent urban infrastructure. India's Smart Cities Mission, which targets the development of 100 smart cities with modernized civic infrastructure, and the UAE's National Smart Cities Program exemplify government-led initiatives generating substantial demand for integrated Building Management Systems. Additionally, the U.S. Bipartisan Infrastructure Law allocates over US$ 550 billion for national infrastructure upgrades, a portion of which is dedicated to public building modernization. BMS vendors that align their product roadmaps with public-sector procurement priorities, offering scalable, interoperable, and cybersecure platforms, are well positioned to capture significant long-term revenue from government and institutional building portfolios, which collectively encompass billions of square feet of usable floor space globally.

Retrofit Market Expansion Driven by Aging Building Stock and ESG Commitments

The global building stock presents an enormous retrofit opportunity for BMS solution providers. The International Energy Agency (IEA) estimates that approximately 80% of the buildings that will exist in 2050 have already been constructed, with a significant proportion operating on outdated, inefficient building automation infrastructure. Corporate sustainability commitments and Environmental, Social, and Governance (ESG) reporting requirements are compelling building owners and occupiers to upgrade legacy systems. Major institutional investors and Real Estate Investment Trusts (REITs) are increasingly integrating building energy performance metrics into portfolio assessments. Modular, cloud-native BMS retrofit solutions that offer fast deployment timelines, minimal operational disruption, and immediate ROI are gaining strong traction. Vendors offering AI-powered energy analytics overlays that integrate with existing building infrastructure, without requiring full system replacement, are particularly well-positioned to capitalize on this multi-billion-dollar global retrofit opportunity.

Category-wise Analysis

System Type Insights

Energy Management Systems (EMS) commanded the dominant share in the Building Management System market by system type, accounting for approximately 34% of total revenues in 2025. This leadership position is underpinned by the intensifying global mandate for energy conservation and operational cost reduction across commercial and industrial buildings. The U.S. Energy Information Administration (EIA) notes that commercial buildings consume approximately 18% of total U.S. energy, creating acute demand for intelligent EMS platforms. Energy Management Systems enable real-time monitoring of energy flows, automated load shedding, demand response participation, and integration with renewable energy sources, resulting in measurable utility cost savings. The proliferation of smart meters, ISO 50001 energy management certifications, and corporate net-zero pledges has further accelerated EMS deployment across multi-site commercial real estate portfolios, reinforcing its leadership position within the broader BMS ecosystem. The Security & Access Control Systems segment is identified as the fastest-growing system type over the forecast period.

End-user Insights

The new construction segment accounted for approximately 62% of the Building Management System market share in 2025, maintaining a clear leadership position driven by the global surge in commercial real estate development and smart building-by-design standards. As architectural and engineering firms increasingly integrate BMS specifications into the design stage, new buildings are delivered with factory-integrated, protocol-unified BMS infrastructure from the outset. Global construction output is expected to reach US$ 15.2 trillion by 2030, according to Oxford Economics, with a significant proportion of commercial and institutional projects incorporating intelligent building technologies. Green building certification programs such as LEED and BREEAM explicitly incentivize BMS integration, reinforcing adoption in new construction projects. Developers find that BMS-equipped buildings command higher rental premiums and improved occupancy rates in competitive real estate markets. The Retrofit segment is projected as the fastest-growing end-use category over the 2026-2033 forecast period.

Application Insights

Commercial buildings represented the largest application segment in the Building Management System market, contributing approximately 43% of global market revenues in 2025. The segment's dominance is attributable to the high concentration of energy-intensive mechanical and electrical systems within office complexes, retail malls, data centers, and hospitality facilities, all of which require centralized management for operational efficiency. According to the U.S. Green Building Council (USGBC), LEED-certified commercial buildings consume 25% less energy than conventional counterparts, with BMS integration being a key enabler of this performance advantage. The increasing density of commercial real estate in emerging markets, particularly across China, India, and Southeast Asia, coupled with growing demand for smart office environments post-pandemic, has materially strengthened commercial building BMS adoption rates. Residential Buildings are projected as the fastest-growing application segment over the forecast period, driven by the rapid proliferation of smart home technologies.

Regional Insights

North America Building Management System Market Trends and Insights

North America held the largest share of the global building management system market in 2025, accounting for approximately 36% of total revenues, underpinned by the region's mature commercial real estate sector, strong regulatory framework, and high technology adoption rate. The United States leads regional demand, driven by stringent energy codes including ASHRAE 90.1, the ENERGY STAR program administered by the U.S. Environmental Protection Agency (EPA), and federal mandates under the Energy Independence and Security Act (EISA). The Department of Energy's (DOE) Building Technologies Office continues to invest in next-generation building automation research and deployment, providing a supportive ecosystem for BMS innovation.

Canada is emerging as a complementary growth market, with the Pan-Canadian Framework on Clean Growth and Climate Change driving retrofits of federal and provincial building portfolios. The North American BMS landscape is characterized by significant vendor consolidation, with key players such as Johnson Controls, Honeywell International Inc., and Siemens maintaining strong regional footprints. The increasing adoption of AI-powered analytics, digital twins, and predictive maintenance capabilities in U.S. commercial buildings is expected to sustain the region's leadership position throughout the forecast period, with the enterprise and government building segments remaining the primary demand anchors.

Europe Building Management System Market Trends and Insights

Europe is the second-largest regional market for Building Management Systems, with regulatory harmonization under the EU's Energy Performance of Buildings Directive (EPBD) as the primary driver of demand. The revised EPBD, adopted in 2024, mandates that all new buildings in EU member states achieve zero-emission standards by 2030, while existing public buildings must undergo significant energy performance upgrades by 2027. Germany and the United Kingdom are the dominant national markets within Europe, collectively accounting for a significant portion of regional BMS revenues. Germany's Buildings Energy Act (GEG) and the UK's Net Zero Building Strategy are accelerating BMS procurement across both public and private building sectors.

France and Spain are demonstrating accelerating adoption rates, particularly in the commercial and government building segments, supported by national energy renovation programs. The Smart Readiness Indicator (SRI) framework, an EU-wide rating system for buildings' smart technology readiness, is expected to become a key market driver by incentivizing property owners to upgrade BMS capabilities. Cross-border interoperability standards under EN 15232 are further harmonizing BMS deployment practices across European markets, reducing integration complexity and total cost of ownership for multi-jurisdiction real estate portfolios managed by large pan-European property companies and institutional investors.

Asia Pacific Building Management System Market Trends and Insights

Asia Pacific is the fastest-growing regional market for building management systems over the forecast period, driven by unprecedented urbanization, large-scale construction activity, and supportive government smart city policies. China remains the dominant national market in the region, with the Chinese government's 14th Five-Year Plan emphasizing green buildings and energy efficiency standards for new and existing construction. China's Ministry of Housing and Urban-Rural Development (MOHURD) has established mandatory energy-efficiency standards for large public buildings, directly stimulating BMS demand in the institutional and commercial segments.

India represents a high-growth frontier market, supported by the Smart Cities Mission and the Bureau of Energy Efficiency's (BEE) Energy Conservation Building Code (ECBC), which mandates energy performance standards for commercial buildings. Japan continues to drive the adoption of advanced BMS technologies in earthquake-resilient smart buildings. The ASEAN region, including Singapore, Indonesia, and Malaysia, is experiencing rapid commercial construction activity, with Singapore's Building and Construction Authority (BCA) Green Mark scheme serving as a benchmark for sustainable BMS integration. The combination of large construction volumes, rising energy costs, and government green building mandates makes the Asia Pacific the most dynamic regional market for BMS over the forecast period.

Competitive Landscape

The global building management system market exhibits a moderately consolidated structure, with a few multinational technology providers holding a significant share, complemented by regional specialists and emerging start-ups. Large players leverage integrated portfolios, global distribution networks, and long-term service contracts to maintain competitive advantage across commercial and institutional infrastructure segments.

Strategically, the market is witnessing a strong shift toward cloud-native platforms, AI-driven analytics, and open-protocol architectures such as BACnet and KNX, enabling interoperability and scalability across building systems. Vendors are increasingly focusing on digital transformation through software-centric offerings and lifecycle services. Mergers and acquisitions remain a key strategy to enhance technological capabilities and expand geographic presence. Additionally, evolving business models such as subscription-based platforms, BMS-as-a-Service, and performance-linked contracts are reducing upfront costs for clients while driving recurring revenue streams and long-term customer engagement.

Key Developments:

- March 2026: Johnson Controls launched major upgrades to its intrusion portfolio with the introduction of DSC PowerSeries Neo 5 and IQ Panel 5, enhancing security capabilities through hybrid wired-wireless systems, AI-enabled features, improved scalability, and simplified installation for residential and commercial users.

- June 2025: Honeywell unveiled its AI-powered Connected Solutions platform for building management, integrating software, systems, and devices into a single interface to enable real-time monitoring, predictive maintenance, and energy optimization, with early adoption by Verizon and Vanderbilt University.

Companies Covered in Building Management System Market

- Schneider Electric SE

- Azbil Corporation

- Delta Electronics, Inc.

- Emerson Electric Co.

- Hubbell Incorporated

- Cisco Systems, Inc.

- Siemens AG

- Johnson Controls International plc

- Airedale International Air Conditioning Ltd.

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Honeywell International Inc.

- Trane Technologies plc

- Virtusa Corporation

- Beckhoff Automation GmbH & Co. KG

- Mitsubishi Electric Corporation

- ABB Ltd.

- Bosch Building Technologies

- Legrand SA

- Carrier Global Corporation (UTC Fire & Security)

- Robert Bosch GmbH

Frequently Asked Questions

The market is estimated at US$ 21.4 billion in 2026 and is projected to reach US$ 58.0 billion by 2033, growing at a CAGR of 15.3%.

Growth is driven by energy efficiency regulations, IoT and AI integration, net-zero building targets, and smart city initiatives.

North America leads the market with around 36% share, supported by strong regulations and advanced building infrastructure.

The retrofit segment offers major opportunities due to aging infrastructure and rising demand for energy-efficient upgrades.

Key players include Honeywell, Siemens, Johnson Controls, Schneider Electric, Mitsubishi Electric, and other global technology providers.