- Non-food Packaging

- Biofoam Packaging Market

Biofoam Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Biofoam Packaging Market by Material Type (Polylactic Acid, Starch, PHA, Cellulose, Mycelium, Others), Application (Protective & Cushioning, Food Service, Temperature Sensitive Goods, Industrial Packaging, Agricultural Packaging, Others), Packaging Form (Molded Foam Parts, Trays & Clamshells, Loose-fill, Cups & Bowls, Sheets & Boards), Industry, and Regional Analysis for 2026 - 2033

Biofoam Packaging Market Size and Trend Analysis

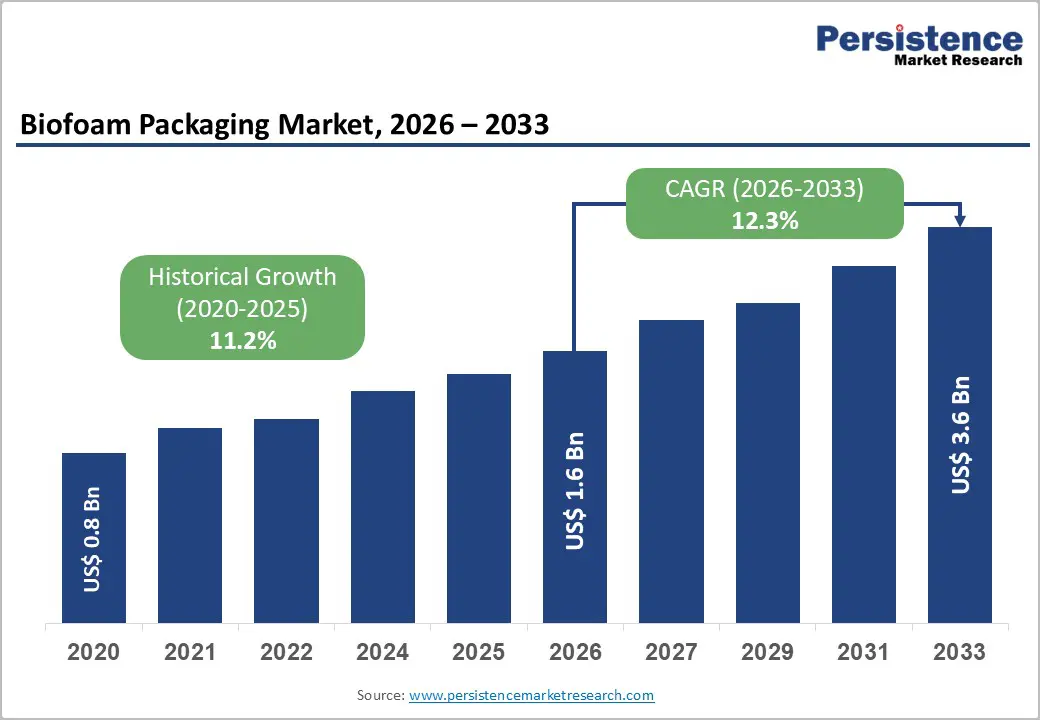

The global biofoam packaging market is valued at US$ 1.6 billion in 2026 and is projected to reach US$ 3.6 billion by 2033, growing at a CAGR of 12.3% between 2026 and 2033.

The market's robust growth trajectory is fundamentally driven by a convergence of regulatory pressure, technological innovation, and shifting consumption patterns. Sweeping legislative mandates across the European Union, United States, and Asia Pacific, including the EU Packaging and Packaging Waste Regulation (PPWR), state-level EPS bans, and single-use plastic restrictions, are compelling packaging manufacturers, foodservice operators, and e-commerce companies to adopt certified biodegradable alternatives.

Key Industry Highlights:

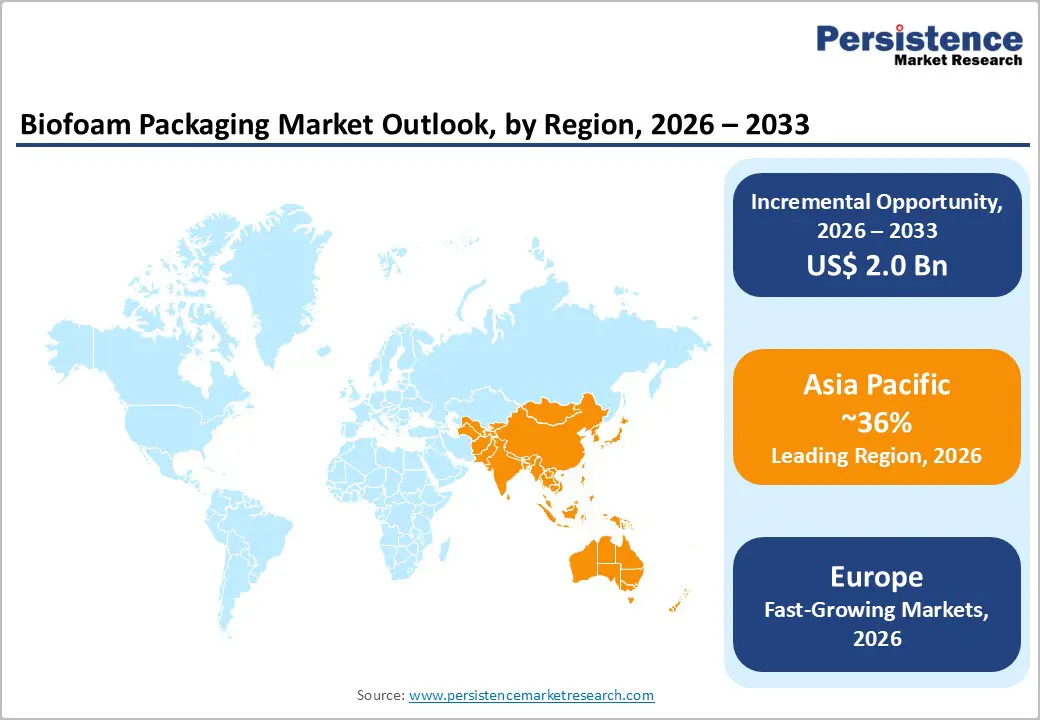

- Leading Region: Asia Pacific leads the global biofoam packaging market, accounting for approximately 36% of total revenue in 2025, driven by China's policy-driven EPS substitution programs, Japan's Plastic Resource Circulation Act (2022), and India's rapidly growing packaged food and e-commerce delivery sectors.

- Fastest Growing Region: Europe is the fastest-growing region with innovation-driven markets for biofoam packaging. Germany leads regional adoption, supported by extensive industrial composting capacity and the stringent Green Dot recovery system.

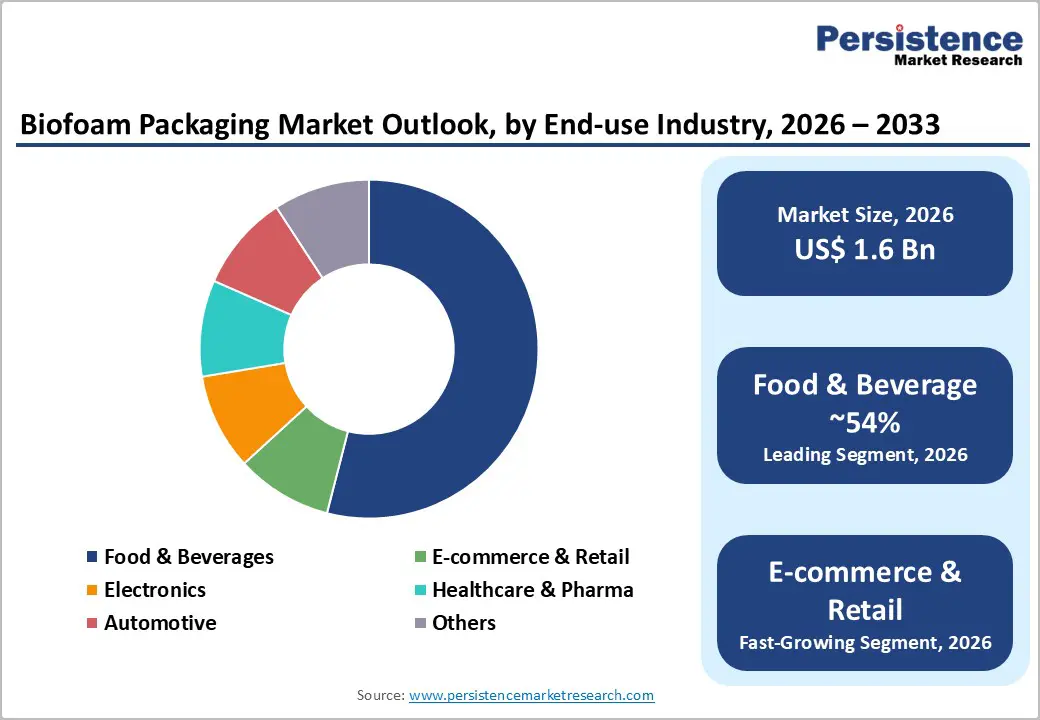

- Dominant Industry: Food & Beverages is the dominant end-use industry, commanding approximately 54% of total biofoam packaging market revenue in 2025, driven by sweeping mandates for compostable trays, clamshells, and insulated containers under the EU PPWR, France's AGEC Law, and global QSR sustainability sourcing policies.

- Fastest Growing Segment: Polyhydroxyalkanoates (PHA)-based biofoam is the fastest-growing material type, driven by its superior marine and home composting biodegradability, regulatory preference under PPWR and ASTM D6400, and expanding commercial production capacity from RWDC Industries, Danimer Scientific, and TotalEnergies Corbion globally.

- Key Market Opportunity: The rapid commercialization of mycelium-based biofoam packaging, pioneered by Ecovative Design LLC, presents a transformative market opportunity as brands seek plastic-free, home-compostable packaging for premium consumer goods, electronics, and the pharmaceutical sectors to meet intensifying ESG commitments and circular-economy regulations.

| Key Insights | Details |

|---|---|

|

Biofoam Packaging Market Size (2026E) |

US$ 1.6 Bn |

|

Market Value Forecast (2033F) |

US$ 3.6 Bn |

|

Projected Growth CAGR (2026-2033) |

12.3% |

|

Historical Market Growth (2020-2025) |

11.2% |

DRO Analysis

Drivers - Regulatory Mandates on Single-Use Plastics Accelerating Biofoam Substitution

Escalating global regulations targeting petroleum-based single-use packaging materials are emerging as the most influential force reshaping the biofoam packaging market. Under the European Union’s Packaging and Packaging Waste Regulation (EU 2025/40), effective from 11 February 2025, all packaging sold within the EU must be recyclable or compostable by 2030, with specific single-use plastic formats prohibited from January 2030. This framework imposes stringent compliance requirements on packaging converters across all 27 Member States.

In the United States, federal procurement policies administered by the EPA and the USDA BioPreferred Program prioritize certified bio-based materials, such as those that meet ASTM D6400 standards. Similarly, France’s AGEC Law mandates compostable or reusable foodservice packaging from 2025, accelerating the displacement of EPS foam. Collectively, these mandates are driving a sustained structural shift toward biofoam adoption through the forecast period.

E-Commerce Expansion Driving Protective Biofoam Packaging Demand

The rapid expansion of global e-commerce represents the second most significant structural driver of demand for biofoam packaging. With business-to-consumer e-commerce sales surpassing US$ 6.5 trillion in 2023 and expected to continue accelerating, the rise in last-mile delivery volumes has intensified the need for lightweight, shock-absorbent, and environmentally responsible cushioning solutions. Biofoam materials derived from PLA, starch blends, and mycelium composites are engineered to meet these performance and sustainability requirements.

Major e-commerce platforms and logistics operators are increasingly adopting molded inserts, loose-fill materials, and customized protective biofoam formats as part of broader ESG and net-zero initiatives. Furthermore, leading online retailers now require supplier compliance with standards such as EN 13432 in Europe and ASTM D6400 in the United States, reinforcing biofoam uptake across the packaging value chain.

Restraints - High Production Costs and Price Premium Over Conventional Foam

A persistent barrier to mainstream adoption of biofoam packaging is the significant price premium relative to conventional expanded polystyrene (EPS) foam. Bio-derived polymers such as PLA and PHA remain substantially more expensive than petroleum-derived polystyrene, due to higher raw material costs, energy-intensive fermentation and polymerization processes, and limited economies of scale. European Bioplastics data indicate that the global bioplastics industry operated at approximately 72% of total production capacity in 2025, suggesting significant underutilization that constrains per-unit cost reductions. Until bio-based feedstock prices decline and manufacturing yields improve, biofoam will remain a premium-priced product, limiting penetration in price-sensitive end markets such as agricultural packaging and lower-value consumer goods.

Inadequate Industrial Composting Infrastructure in Emerging Markets

The environmental value proposition of biofoam packaging is critically dependent on access to appropriate end-of-life management systems, particularly certified industrial composting facilities. Most PLA and starch-based biofoam materials require controlled composting conditions, including temperatures above 55°C, to biodegrade within the EN 13432 or ASTM D6400 certification timeframes. However, industrial composting infrastructure remains sparse in many developing economies, undermining the sustainability proposition in high-growth markets across Southeast Asia, Latin America, and Sub-Saharan Africa. Even within Europe, composting coverage is uneven; Eastern European markets report only approximately 28% municipal composting coverage, limiting the closed-loop end-of-life options that justify biofoam's premium pricing for corporate and institutional buyers.

Opportunities - Commercial Scale-Up of PHA-Based Biofoam Opens New End-Market Channels

Polyhydroxyalkanoates (PHA) represent the most advanced next-generation material opportunity within the biofoam packaging market. Unlike PLA, PHA naturally biodegrades in marine, freshwater, soil, and home-composting environments, offering unmatched end-of-life flexibility without the need for industrial composting systems. Danimer Scientific’s Nodax® PHA, which holds multiple TÜV AUSTRIA certifications for both industrial and home compostability and is approved by the U.S. FDA for food-contact applications, underscores this capability.

Global biobased plastics production is projected to expand from 2.31 million tonnes in 2025 to approximately 4.69 million tonnes by 2030, with PHA among the fastest-growing segments. The commissioning of RWDC Industries’ 10,000-tonne PHA facility in Greece further strengthens supply readiness, positioning PHA-based biofoam to capture significant market share through 2033.

Mycelium Biofoam Commercialization Creating Premium Differentiation Opportunity

Mycelium-based biofoam presents a significant commercial opportunity for packaging manufacturers targeting premium and brand-sensitive sectors. Derived from fungal root structures cultivated on agricultural substrates, these materials are fully biodegradable within weeks under natural conditions and require no industrial composting infrastructure, offering a distinct sustainability advantage.

Ecovative Design LLC, a leading innovator in mycelium biomaterials, utilizes its proprietary AirMycelium™ technology to produce commercial-scale molded packaging with performance comparable to EPS foam. A peer-reviewed study reported a tenfold increase in research on mycelium-based materials between 2016 and 2023, reflecting growing scientific and market interest. With Ecovative opening access to its MycoComposite™ patent and tightening EU PPWR and U.S. EPR regulations, mycelium biofoam offers a compelling, plastic-free solution for premium consumer goods and pharmaceutical applications.

Category-wise Analysis

Material Type Insights

Starch-based biofoam holds the leading position in the material type category, representing roughly 40% of the global biofoam packaging market in 2024. This prominence stems from the widespread availability of starch derived from corn, potato, wheat, rice, and tapioca, as well as its cost advantage over synthetic biopolymers. Starch blends also offer favorable melt-flow characteristics compatible with existing thermoforming equipment, allowing converters to reduce capital investment.

Starch-based biofoam further benefits from EN 13432 certification in Europe and USDA BioPreferred recognition in the U.S. While PLA is the fastest-growing material category, starch-based biofoam is expected to maintain dominance due to its cost efficiency and established supply chains.

Application Insights

The protective & cushioning segment remains the leading application within the global market, accounting for approximately 35% of total market share in 2025. Its dominance reflects the essential role of biofoam in safeguarding fragile products, such as electronics, glassware, medical devices, and premium consumer goods, throughout storage and transportation. The continued expansion of global e-commerce has further elevated demand for lightweight, shock-absorbent, and environmentally responsible packaging materials that support corporate sustainability commitments.

Industry organizations, including the Sustainable Packaging Coalition and the Ellen MacArthur Foundation, actively promote the transition to bio-based protective solutions as part of broader circular-economy objectives. Meanwhile, the Food Service segment represents the fastest-growing application, driven by EU PPWR and France’s AGEC Law, which mandates compostable or reusable foodservice packaging across Western Europe.

Packaging Form Insights

Molded Foam Parts command the leading share of the packaging form market, accounting for approximately 42% of the global biofoam packaging market in 2024. Molded biofoam inserts, end-caps, and formed trays deliver superior fit-and-protection performance for high-value consumer electronics, industrial instruments, and medical devices, making them the default format for premium protective packaging. The precision achievable in standard injection molding and compression molding enables manufacturers to achieve low scrap rates and consistent dimensional quality.

Advancements in PLA-based and starch-based expandable beads for molding processes, alongside the emergence of bio-based expandable alternatives to conventional EPS, are broadening the performance envelope of molded biofoam. The Loose-fill segment is identified as the fastest-growing packaging form, fueled by the explosive growth of e-commerce fulfillment and logistics operations that require scalable, certified compostable void-fill alternatives to conventional polystyrene peanuts for domestic and cross-border parcel distribution.

Industry Insights

The food & beverages sector remains the dominant end-use industry in the global biofoam packaging market, contributing nearly 54% of total market revenue in 2025. This leadership is driven by the widespread use of biofoam trays, clamshells, cups, bowls, and insulated containers across quick-service restaurants, cloud kitchens, supermarkets, fresh produce distributors, and ready-meal manufacturers.

The global food packaging industry is undergoing a structural shift toward compostable and bio-based materials, influenced by France’s AGEC Law, the EU PPWR, and sustainability mandates from major retail organizations such as the Consumer Goods Forum. In 2024, food and beverage applications accounted for approximately 58.95% of the bioplastic packaging market. The E-commerce & Retail sector follows as the second-largest and fastest-growing end-use segment, supported by rising parcel volumes and stricter sustainable packaging requirements.

Regional Insights

North America Biofoam Packaging Trends

North America maintains a significant share of the global biofoam packaging market, with the United States serving as the region’s primary growth anchor. The U.S. benefits from a robust innovation ecosystem that includes biomaterial science startups, established packaging converters, and the world’s largest e-commerce sector. The USDA BioPreferred Program continues to channel substantial institutional procurement toward bio-based packaging certified under ASTM D6400 standards.

Furthermore, state-level bans on EPS foam in California, New York, and Maryland have accelerated the shift toward biofoam alternatives in foodservice and takeaway applications. Canada is advancing similar objectives through Extended Producer Responsibility frameworks, promoting compostable packaging adoption across retail and logistics. Collectively, these factors support a projected CAGR for the North American market of roughly 12.14% through 2033.

Europe Biofoam Packaging Trends

Europe remains one of the most highly regulated and innovation-driven markets for biofoam packaging, guided primarily by the EU Packaging and Packaging Waste Regulation (EU 2025/40), which took effect on 11 February 2025 and becomes fully applicable from 12 August 2026. Germany leads regional adoption, supported by extensive industrial composting capacity and the stringent Green Dot recovery system. France’s AGEC Law, requiring compostable foodservice packaging from 2025, is accelerating the shift away from EPS in the restaurant and catering sectors.

Italy’s network of 360 certified industrial composters provides an efficient closed-loop model increasingly replicated across Northwestern Europe. Spain and the Nordic countries are rapidly aligning regulations with PPWR, while the UK’s Plastic Packaging Tax incentivizes bio-based alternatives. The EU-wide EPR eco-modulation framework, effective from 2030, will further promote compostable and recyclable packaging formats.

Asia Pacific Biofoam Packaging Trends

Asia Pacific remains the leading region in the global biofoam packaging market, accounting for nearly 36% of total revenues in 2025. Growth is primarily driven by China, Japan, India, and the broader ASEAN bloc. China serves as both the largest consumer and a rapidly expanding producer of bioplastics-based packaging, supported by policies under the 14th Five-Year Plan aimed at reducing single-use plastic consumption.

Japan’s Plastic Resource Circulation Act (2022) has further accelerated the transition to biofoam in food retail and electronics packaging. India is emerging as a high-growth market through the Plastic Waste Management Amendment Rules (2022) and the BioE3 Policy launched in 2024. Meanwhile, ASEAN countries are implementing national roadmaps to reduce plastic. Strong agricultural feedstock availability provides a structural cost advantage, reinforcing the region’s role as both the largest market and the lowest-cost manufacturing base globally.

Competitive Landscape

The global biofoam packaging market exhibits a moderately fragmented competitive structure, with market leadership concentrated among a combination of vertically integrated chemical conglomerates, specialized biopolymer producers, packaging converters, and emerging biomaterial startups. Leaders such as BASF SE, NatureWorks LLC, and Novamont S.p.A. leverage proprietary polymer portfolios, Ecovio®, Ingeo™ PLA, and Mater-Bi®, respectively, to maintain strong upstream positions. Packaging manufacturers, including Sealed Air Corporation, BEWi Group, and Pregis LLC compete on converting expertise and customer proximity, while innovators such as Ecovative Design LLC and Synbra Technology BV differentiate on next-generation biomaterial platforms. Key strategic trends include capacity expansions in the Asia Pacific, biopolymer supply licensing and joint ventures, and integration of composting certification tools to support corporate ESG reporting.

Key Developments:

- January 2025: Sealed Air Corporation announced that it has entered into a definitive agreement to be acquired by funds affiliated with CD&R, a leading private investment firm with deep experience in the industrial and packaging industries, in an all-cash transaction with an enterprise value of $10.3 billion.

- December 2025: Stora Enso unveiled a flocked variant of its cellulose-based Papira® biofoam, developed in partnership with Krekelberg Flock Products and Flocktechniek, C&B Innovations. The innovation targets premium packaging in beauty, electronics, and fragile goods, addressing the EU PPWR's ban on non-recyclable protective foam formats.

- August 2025: Stora Enso has invested EUR 1.1 billion in the consumer packaging board production line in Oulu, Finland. The investments have made it possible to convert former paper machines into board lines utilising the latest technology, while the environmental impact has been reduced by cutting fossil carbon dioxide emissions by 90%.

Top Companies in Biofoam Packaging

BASF SE (Ludwigshafen, Germany) is the world's largest chemical company by revenue. Its Ecovio® and Ecoflex® product lines are certified compostable biopolymer solutions widely adopted in biofoam packaging, compostable mulch films, and foodservice ware. With operations spanning more than 90 countries and over 230 production sites globally, BASF leverages its vertically integrated supply chain and global R&D footprint to maintain leadership in both biopolymer resin supply and downstream biofoam packaging application development.

NatureWorks LLC (Plymouth, Minnesota, U.S.) is the world's foremost producer of PLA biopolymers, supplying Ingeo™ PLA resin to biofoam packaging manufacturers worldwide. With an annual production capacity exceeding 150,000 tonnes across facilities in North America and Asia, NatureWorks commands significant influence in setting PLA pricing, quality, and performance benchmarks across the industry. Its Ingeo™ PLA is deployed across protective foam packaging, foodservice trays, cups, and loose-fill cushioning applications in markets regulated by both EN 13432 and ASTM D6400 composting standards.

Novamont S.p.A. (Novara, Italy) is a leading European bioplastics innovator, recognized for its Mater-Bi® starch-based biopolymer range, which is widely deployed in compostable biofoam packaging for food-contact applications across EU markets. Operating within a bioeconomy district model that integrates bioplastics production with regional agricultural feedstock sourcing in Italy, Novamont maintains a competitive advantage in cost and supply chain sustainability. Its materials are certified to EN 13432 and BPI standards, positioning them as fully compliant solutions under the EU PPWR and meeting the growing sustainability mandates of retailers and foodservice operators across Europe.

Companies Covered in Biofoam Packaging Market

- BASF SE

- Sealed Air Corporation

- Stora Enso

- NatureWorks LLC

- Ecovative Design LLC

- Synbra Technology BV

- Novamont S.p.A.

- Danimer Scientific

- BEWi Group

- Good Biopak

- Semepack

- Pregis LLC

- TotalEnergies Corbion

- Cruz Foam

- RWDC Industries

Frequently Asked Questions

The global Biofoam Packaging market is valued at US$ 1.6 Bn in 2026 and is projected to reach US$ 3.6 Bn by 2033, registering a CAGR of 12.3% during the forecast period. Historically, the market grew at a CAGR of 11.2% between 2020 and 2025, reflecting sustained momentum in global demand for certified biodegradable and compostable packaging solutions.

The principal factors driving market demand include increasingly stringent legislative mandates on single‑use plastics, most notably the EU Packaging and Packaging Waste Regulation (PPWR) enacted in February 2025, as well as state‑level prohibitions on EPS foam in California, New York, and Maryland.

Starch-based biofoam leads the material type category, accounting for approximately 40% of total market share in 2025. Its dominance is attributed to low feedstock cost, wide agricultural availability from corn, potato, wheat, and tapioca, and certified compostability under EN 13432 (Europe) and ASTM D6400 (U.S.) standards.

Asia Pacific is the leading regional market, holding approximately 36% of total global revenue in 2025. The region benefits from strong government policy support in China, Japan, and India, a high manufacturing base utilizing low-cost agricultural feedstocks, and rapidly expanding e-commerce and food delivery service sectors that are generating sustained demand for protective and foodservice biofoam packaging solutions across China, India, Indonesia, and Vietnam.

The most significant opportunity lies in the commercialization of next-generation PHA-based and mycelium-based biofoam. Both technologies offer superior end-of-life biodegradability, including marine and home composting environments, without requiring industrial composting infrastructure.

The leading companies in the global Biofoam Packaging market include BASF SE, NatureWorks LLC, Novamont S.p.A., Sealed Air Corporation, Ecovative Design LLC, Danimer Scientific, Synbra Technology BV, Stora Enso, Pregis LLC, and BEWi Group, among others.