- Automotive Components & Materials

- Automotive Multi-link Suspension Market

Automotive Multi-link Suspension Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Multi-link Suspension Market by Axle Fitment (Rear Multi-Link, Front Multi-Link), by Material of Links (Iron, Steel, Aluminum, Composite), Vehicle Type (Hatchback/Sedan, SUV, LCV, HCV), Component (Control Arms, Bushings, Ball Joints & Spherical Joints, Knuckles / Wheel Carriers, Fasteners & Mounting Hardware), Sales Channel (OEM, Aftermarket), and Regional Analysis, 2026 - 2033

Automotive Multi-link Suspension Market Size and Trend Analysis

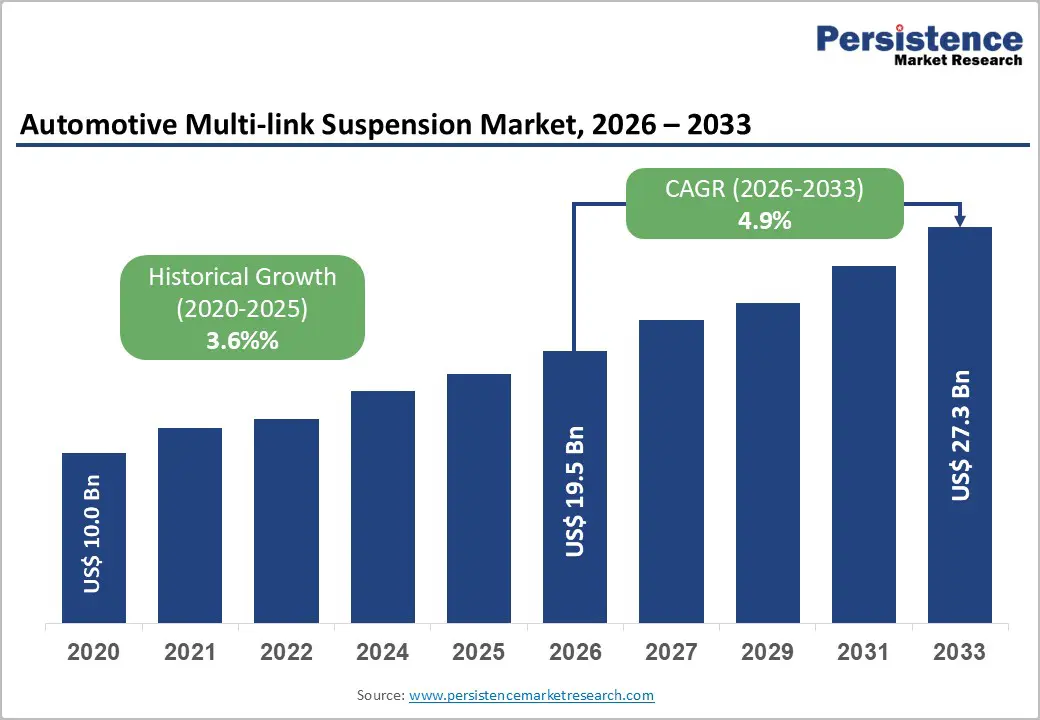

The global automotive multi-link suspension market size is likely to be valued at US$ 19.5 Billion in 2026 and is expected to reach US$ 27.3 Billion by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 to 2033.

Rising global vehicle production, growing consumer preference for premium ride comfort and superior handling dynamics, and rapid expansion of the SUV and electric vehicle segments are the primary forces propelling market growth.

Key Industry Highlights:

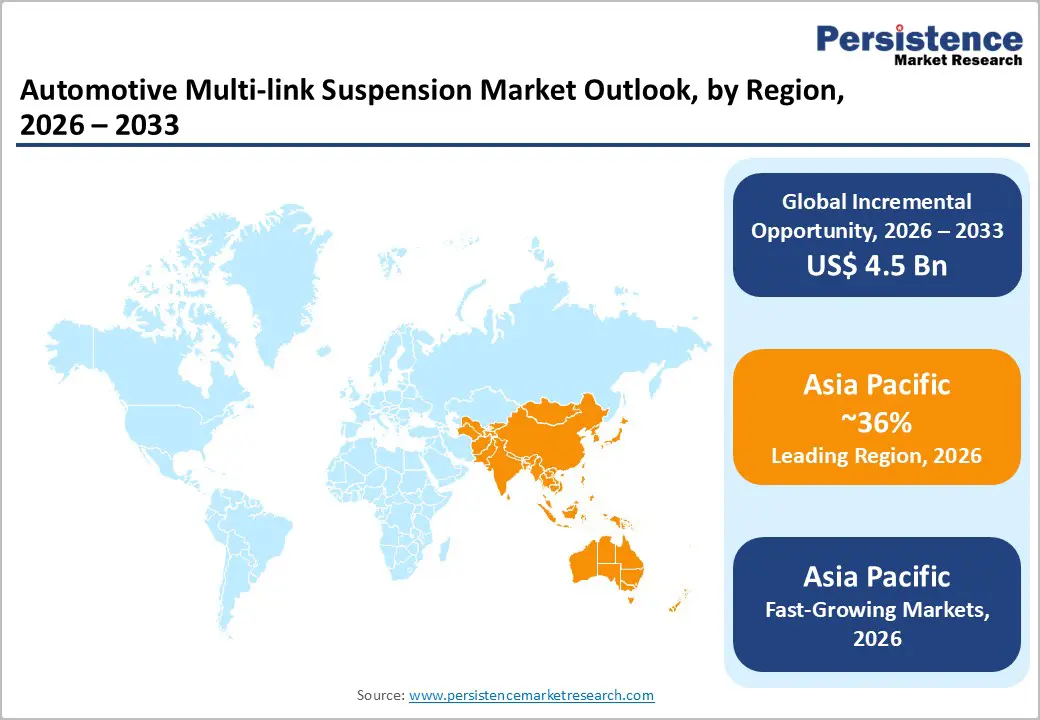

- Leading Region: Asia Pacific leads the global automotive multi-link suspension market, accounting for 36% share, driven by China's massive vehicle production volumes, Japan's engineering leadership, and India's rapidly expanding SUV market, collectively accounting for the largest share of global demand.

- Fastest Growing Region: Asia Pacific is also the fastest growing region with rising CAGR of 6.1%, with India and China's BEV boom and surging mid-premium SUV adoption driving above-average suspension component demand through 2033.

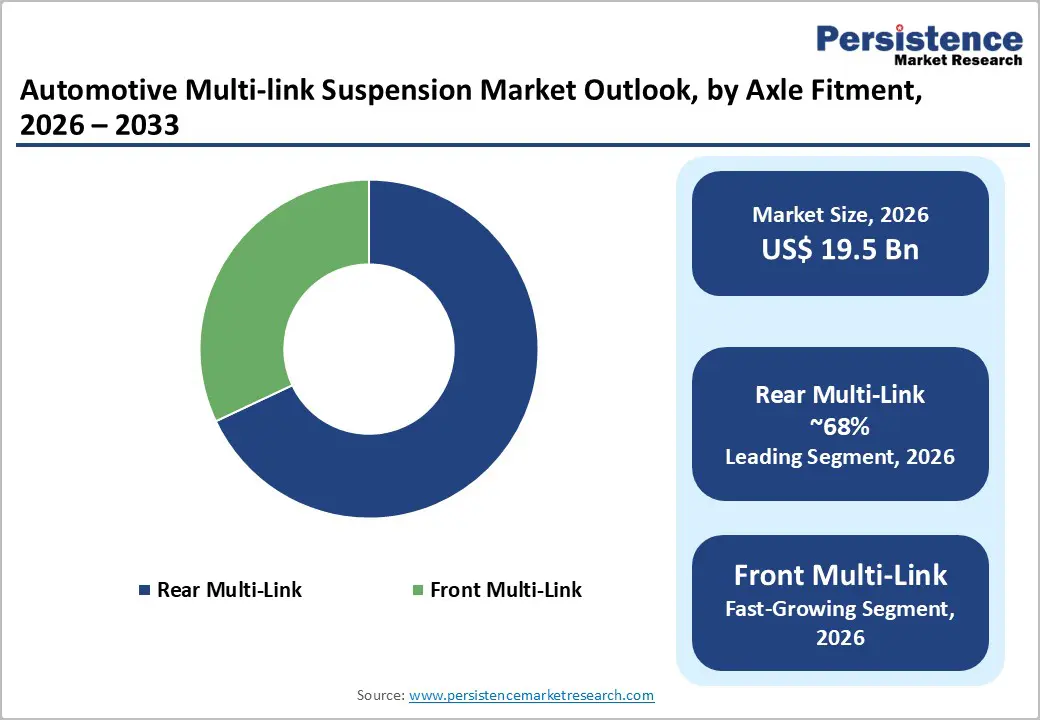

- Dominant Axle Fitment: The rear multi-link axle segment dominates with approximately 68% market share, as it is standard across mid-size and full-size SUVs, crossovers, and premium sedans globally.

- Fastest Growing Material Segment: Aluminum material links represent the fastest growing sub-segment, propelled by EV platform lightweighting mandates and CO2 emission standards driving a shift away from heavier steel links.

- Key Opportunity: Integration of electronically controlled adaptive multi-link suspension with ADAS platforms presents the highest-value growth opportunity, as Euro NCAP and NHTSA safety frameworks increasingly reward advanced dynamic chassis management.

| Key Insights | Details |

|---|---|

| Automotive Multi-link Suspension Market Size (2026E) | US$ 19.5 Billion |

| Market Value Forecast (2033F) | US$ 27.3 Billion |

| Projected Growth CAGR (2026 - 2033) | 4.9% |

| Historical Market Growth (2020 - 2025) | 3.6% CAGR |

DRO Analysis

Drivers - Rising global SUV and crossover demand significantly driving adoption of advanced multi-link suspension systems worldwide

The global sport utility vehicle segment has expanded significantly, with SUVs accounting for nearly 46% of global passenger car sales in 2023, according to the International Energy Agency (IEA). Multi-link suspension systems are widely preferred in SUVs, crossovers, and premium sedans because they allow engineers to fine-tune handling, steering response, and ride comfort independently at each wheel.

As automakers compete to deliver vehicles that combine off-road capability with superior on-road refinement, four- and five-link rear suspension systems have become standard across mid-size and full-size SUV platforms worldwide. This trend is directly increasing both the value of suspension components per vehicle and the overall demand for multi-link systems. As SUV popularity continues to grow across developed and emerging markets, manufacturers are increasingly prioritizing advanced suspension architectures to enhance driving performance and customer experience.

Rapid Electric Vehicle Growth is Amplifying the Need for Stronger, Precisely Engineered Multi-Link Suspension Systems Globally

The rapid shift toward battery-electric vehicles (BEVs) is significantly increasing demand for advanced multi-link suspension systems. Unlike traditional internal combustion engine vehicles, BEVs eliminate components such as driveshafts and transmission tunnels, allowing for flatter and more flexible vehicle architectures that are ideal for multi-link configurations. However, BEVs also carry heavy battery packs, typically adding 200-650 kg compared to conventional vehicles, which increases the demand for stronger and more precisely engineered suspension systems. These systems must effectively manage higher loads while maintaining ride comfort and vehicle stability. According to the International Energy Agency (IEA), global BEV sales exceeded 10 million units in 2022 and continue to grow rapidly. Each new BEV platform requires specially designed multi-link suspension components to handle unique weight distribution and performance needs, creating strong and sustained demand for advanced suspension solutions.

Restraints - High Manufacturing Complexity and Cost Limiting Multi-Link Suspension Adoption In Price-Sensitive Vehicle Segments Worldwide

Multi-link suspension systems are significantly more complex than traditional suspension designs, requiring more precision-engineered components, such as links, ball joints, bushings, and mounting brackets. This added complexity leads to increased material costs, longer assembly times, and higher labor requirements during manufacturing. The greater number of components raises the risk of maintenance issues and warranty claims over the vehicle lifecycle. Compared to simpler systems like MacPherson struts or torsion beam axles, multi-link setups are considerably more expensive. A five-link rear suspension system can cost automakers 2 to 3 times as much as a torsion beam alternative. This cost difference makes it difficult for manufacturers to justify the use of multi-link systems in entry-level and compact vehicle segments, where pricing pressure is high and profit margins are relatively low.

Volatility in Steel and Aluminum Prices Impacting Supplier Margins and Limiting Investment in Innovation

The automotive multi-link suspension supply chain relies heavily on key raw materials such as steel and aluminum, both of which are subject to significant price fluctuations. These variations are influenced by factors such as energy costs, geopolitical tensions, supply chain disruptions, and global trade policies. According to the World Steel Association, steel prices experienced volatility of over 40% between 2021 and 2023. Aluminum prices have also shown sharp fluctuations, impacting the cost structure of suspension components. Since these materials form a major portion of production costs, such volatility puts pressure on Tier-1 and Tier-2 suppliers, reducing their profit margins. As a result, suppliers may face challenges maintaining stable pricing for OEMs while also investing in research and development of advanced materials, such as lightweight aluminum and composite links, which are essential for next-generation vehicle platforms.

Opportunities - Integration of ADAS with Active Suspension Systems Creating High-Value Growth Opportunities for Multi-Link Technologies

The integration of advanced driver assistance systems (ADAS) with active and semi-active suspension technologies presents a major growth opportunity for the automotive multi-link suspension market. Modern multi-link systems equipped with electronically controlled dampers, air suspension, and predictive road-scanning technologies can dynamically adjust wheel movement and ride height in real time. This improves vehicle stability, comfort, and safety, especially during sudden maneuvers or challenging road conditions. Regulatory bodies such as the European New Car Assessment Program (Euro NCAP) are increasingly recognizing and rewarding vehicles equipped with advanced chassis control systems in their safety ratings. This encourages automakers to adopt more sophisticated suspension technologies. Companies that can develop integrated mechatronic suspension systems that seamlessly connect with vehicle control units are well positioned to capture higher value per vehicle and benefit from long-term aftermarket service opportunities.

Lightweight Aluminum and Composite Materials Gaining Traction to Improve Efficiency and Performance in Electric Vehicles

The growing focus on vehicle lightweighting, particularly in electric vehicles, is creating strong opportunities for aluminum and composite suspension components. Reducing vehicle weight is critical for improving energy efficiency, extending battery range, and meeting global emission standards. Aluminum control arms, produced through forging or casting, can reduce weight by 30-40% compared to traditional steel components while maintaining similar strength and durability.

According to the European Automobile Manufacturers' Association (ACEA), a 10% reduction in vehicle weight can improve fuel efficiency or electric range by 7%. In addition to aluminum, advanced materials such as carbon-fiber-reinforced polymers (CFRP) are gaining attention for their superior strength-to-weight ratio. Suppliers investing in these advanced materials and manufacturing technologies are expected to gain a competitive advantage, especially as demand for high-performance electric vehicle platforms continues to grow globally.

Category-wise Analysis

By Axle Fitment Insights

The rear multi-link segment holds a dominant position in the automotive multi-link suspension market, accounting for approximately 68% of total market revenue. This dominance stems mainly from the rear axle's crucial role in managing both traction and braking forces while maintaining optimal wheel alignment under dynamic driving conditions. Multi-link rear suspension systems provide better control over toe and camber angles, improving vehicle stability, comfort, and handling performance.

In many front-wheel-drive vehicles, manufacturers combine a MacPherson strut front suspension with a multi-link rear setup to achieve a balance between cost and performance. For all-wheel-drive and rear-wheel-drive vehicles, especially SUVs and premium sedans, multi-link rear systems are often essential. Leading automakers such as BMW AG, Mercedes-Benz Group AG, and Toyota Motor Corporation widely use multi-link rear axles across their vehicle portfolios, reinforcing this segment’s strong market position.

By Material of Links Insights

Steel-based links continue to dominate the material segment, accounting for around 52% of the market. Steel remains the preferred material due to its high strength, durability, cost-effectiveness, and well-established manufacturing processes such as stamping and forging. It is widely used across mass-market and mid-range vehicles where cost efficiency is critical.

Advancements in high-strength steel (HSS) and advanced high-strength steel (AHSS) are enabling manufacturers to reduce weight while maintaining structural integrity. According to the World Steel Association, the use of AHSS in automotive components has been growing steadily at around 8% annually, with suspension systems being a key application area. However, aluminum is emerging as the fastest-growing material segment, driven by the increasing demand for lightweight components in electric vehicles. As automakers focus more on improving efficiency and performance, the adoption of aluminum and other advanced materials is expected to rise significantly.

By Vehicle Type Insights

The SUV segment leads the automotive multi-link suspension market, contributing approximately 43% of total demand. SUVs require advanced suspension systems to balance off-road capability and on-road comfort, making multi-link designs highly suitable. The growing popularity of SUVs is reflected in their strong share of global vehicle sales, accounting for around 46% of passenger car registrations in 2023, according to the International Energy Agency (IEA).

In addition to higher sales volumes, SUVs also generate greater revenue per vehicle due to their more complex suspension systems. Full-size SUVs often use five-link rear suspension systems and, in some cases, multi-link setups at the front as well. This increases the number of components and overall system value. As consumer preferences continue to shift toward SUVs in both developed and emerging markets, this segment is expected to remain a key driver of growth for multi-link suspension systems.

By Component Insights

Control arms represent the largest component category in the automotive multi-link suspension market, accounting for approximately 34% of total revenue. Each wheel in a multi-link suspension system typically includes multiple control arms, ranging from two to five, making them the most widely used components in the system. These parts play a critical role in connecting the wheel hub to the vehicle frame while allowing controlled movement in multiple directions.

Control arms must withstand complex forces, including vertical loads, lateral forces, and braking stress, requiring high strength, durability, and precise engineering. The growing use of five-link suspension systems in SUVs and premium vehicles has further boosted demand for control arms. Additionally, the shift toward aluminum control arms in electric vehicles is driving higher average selling prices, creating opportunities for suppliers to offer premium, lightweight, and high-performance solutions.

By Sales Channel Insights

The OEM segment dominates the automotive multi-link suspension market, accounting for approximately 74% of total revenue. Multi-link suspension systems are highly complex and require precise integration with vehicle design, making them primarily sourced directly by automakers rather than through the aftermarket. These systems are engineered to match specific vehicle platforms, ensuring optimal performance, safety, and durability.

Major Tier-1 suppliers such as ZF Friedrichshafen AG, Magna International, and KYB Corporation supply complete suspension modules or individual components directly to OEMs under long-term contracts. While the aftermarket segment is smaller, it is gradually growing due to an aging vehicle population and increasing demand for replacement parts and performance upgrades, particularly in regions like North America and Europe, where vehicle ownership cycles are longer.

Regional Insights

North America Automotive Multi-link Suspension Market Trends

North America is a mature and high-value market for automotive multi-link suspension systems, with the United States serving as the key contributor. Strong consumer preference for SUVs, pickup trucks, and crossover vehicles has significantly driven demand for advanced suspension systems, as these vehicle types commonly use multi-link rear suspensions.

According to Wards Intelligence, SUVs and light trucks accounted for over 75% of new-vehicle sales in the U.S. in 2023, underscoring the segment's importance. The presence of major automotive manufacturers such as General Motors, Ford Motor Company, and Stellantis, along with Tesla, Inc.'s growing production, supports strong regional demand. Additionally, regulatory requirements related to safety and fuel efficiency are encouraging the adoption of lightweight and high-performance suspension systems, further boosting market growth.

Europe Automotive Multi-link Suspension Market Trends

Europe remains a global leader in multi-link suspension innovation, with Germany playing a central role in advancing this technology. Leading automakers such as BMW AG, Mercedes-Benz Group AG, Volkswagen Group, and Porsche AG continue to develop and deploy advanced suspension systems across their vehicle portfolios. Strict regulatory frameworks, including Euro 7 emission standards, require manufacturers to improve vehicle efficiency, reduce emissions, and enhance ride quality.

Multi-link suspension systems play a key role in achieving these goals by optimizing tire performance and reducing noise, vibration, and harshness (NVH). Other countries, such as France, Spain, and the United Kingdom, also contribute to the regional market through strong vehicle production capabilities. The ongoing shift toward electric vehicles in Europe is expected to sustain long-term demand for advanced suspension technologies.

Asia Pacific Automotive Multi-link Suspension Market Trends

Asia Pacific is the largest and fastest-growing market for automotive multi-link suspension systems, driven by high vehicle production and increasing adoption of advanced automotive technologies. China leads the region, producing over 30 million vehicles in 2023, according to the China Association of Automobile Manufacturers (CAAM). Domestic automakers such as BYD Company, NIO Inc., and Li Auto Inc. are actively adopting multi-link suspension systems in their electric and hybrid vehicles to enhance performance and compete globally.

Japan also plays a significant role, with companies such as Toyota Motor Corporation, Honda Motor Co., Ltd., and Nissan Motor Co., Ltd., focusing on advanced engineering and global exports. India is emerging as a key growth market, supported by rising SUV demand and increasing vehicle production.

Competitive Landscape

The global automotive multi-link suspension market is moderately consolidated, particularly at the Tier-1 supplier level, where a few large multinational companies hold significant market share. Key players such as ZF Friedrichshafen AG, Continental AG, Magna International, and Tenneco Inc. dominate OEM supply contracts through their advanced technological capabilities and strong relationships with automakers. These companies differentiate themselves by offering lightweight materials, integrated mechatronic systems, and customized engineering solutions.

In contrast, Tier-2 and Tier-3 suppliers are more fragmented, focusing on manufacturing individual components such as links, bushings, and fasteners. To remain competitive, companies are increasingly engaging in strategic partnerships, joint ventures, and acquisitions, particularly in emerging markets. Additionally, continuous investment in research and development is helping suppliers innovate in adaptive suspension technologies and support the growing demand from electric vehicle platforms.

Key Developments:

- In January 2025, ZF Friedrichshafen AG launched its next-generation active multi-link rear axle module tailored for electric vehicles, integrating electronic damper control systems and achieving 15% weight reduction. This enhances ride comfort, vehicle dynamics, and energy efficiency for modern EV platforms.

- In September 2024, Magna International entered a long-term agreement with a leading European BEV manufacturer to supply aluminum multi-link rear suspension subframe assemblies, strengthening its position in lightweight suspension systems and supporting automakers’ goals for improved efficiency and electrification.

- In March 2023, Tenneco, through its DRiV division, expanded its Monroe aftermarket product range to cover over 85% of U.S. vehicles, enhancing the availability of multi-link suspension components and reinforcing its leadership in the automotive aftermarket segment.

Companies Covered in Automotive Multi-link Suspension Market

- ZF Friedrichshafen AG

- Continental AG

- Benteler Automotive

- Magna International

- KYB Corporation

- Mando Corporation

- Thyssenkrupp Automotive

- Bosch

- Tenneco

- Hitachi Astemo

- Schaeffler AG

- Hyundai Mobis Co., Ltd.

- BWI Group

- NHK Spring Co., Ltd.

- Multimatic Inc.

- Gestamp Automocion

- Martinrea International Inc.

- Tower Automotive

- Yorozu Corporation

Frequently Asked Questions

The global Automotive Multi-link Suspension Market is valued at US$ 19.5 Billion in 2026 and is projected to reach US$ 27.3 Billion by 2033, expanding at a CAGR of 4.9% during the forecast period.

The primary growth drivers include surging global SUV and crossover sales, which require multi-link rear suspensions as standard, and the rapid proliferation of battery electric vehicle (BEV) platforms that mandate sophisticated suspension geometries to manage increased battery weight and optimize ride dynamics.

The Rear Multi-Link segment is the dominant axle fitment category, holding approximately 68% of market revenue, owing to its near-universal specification in mid-size and full-size SUVs, all-wheel-drive vehicles, and premium sedans globally.

Asia Pacific is the leading region, anchored by China's position as the world's largest vehicle producer, Japan's advanced suspension engineering ecosystem, and India's rapidly growing SUV market, collectively driving the region's outsized demand for multi-link suspension components.

The most significant opportunity lies in the development and commercialization of electronically controlled adaptive multi-link suspension systems that integrate with ADAS platforms. As safety regulations from Euro NCAP and NHTSA increasingly reward advanced dynamic chassis management, suppliers delivering mechatronic multi-link modules stand to capture premium per-vehicle content value.

The leading companies in the Automotive Multi-link Suspension Market include ZF Friedrichshafen AG, Continental AG, Magna International, Tenneco, KYB Corporation, Hitachi Astemo, Schaeffler AG, Hyundai Mobis Co., Ltd., Bosch, Mando Corporation, and Multimatic Inc., among others.