- Automotive Components & Materials

- Automotive Curtain Airbags Market

Automotive Curtain Airbags Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Curtain Airbags Market by Curtain Airbags Type (Torso Curtain Airbags, Head Curtain Airbags, Combo Curtain Airbags), Vehicle Type (Passenger Cars, Commercial Cars), End Use (OEMs, Aftermarket), and Regional Analysis for 2026 - 2033

Automotive Curtain Airbags Market Size and Trend Analysis

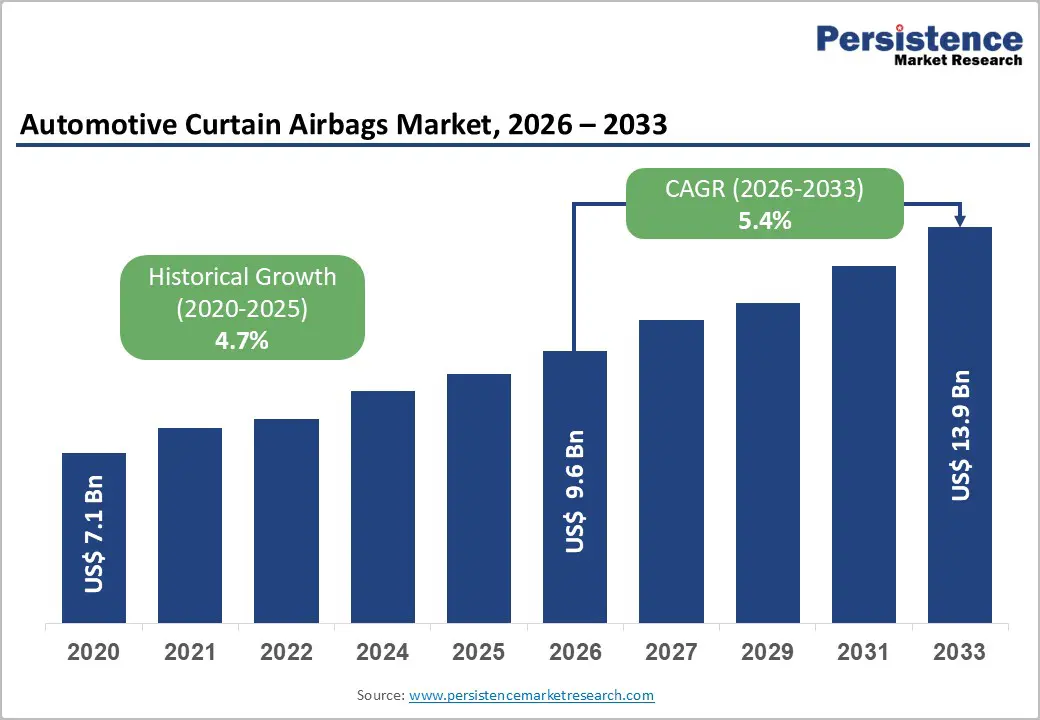

The global automotive curtain airbags market is valued at US$ 9.6 billion in 2026 and is projected to reach US$ 13.9 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

This sustained growth is anchored in increasingly stringent global vehicle safety mandates, the accelerating adoption of advanced passive restraint systems across passenger and commercial vehicles, and rising consumer awareness of occupant protection during side-impact and rollover crash events. feature, directly expanding the addressable fitment rate across vehicle segments globally.

Key Market Highlights

- Leading Region: North America leads the automotive curtain airbags market, driven by NHTSA's FMVSS 226 mandate, high SUV and light truck adoption exceeding 80% of new vehicle sales, and the R&D presence of leading Tier-1 suppliers, including Autoliv and ZF Friedrichshafen AG.

- Fastest growing Region: Asia Pacific is the fastest growing regional market, propelled by China's annual vehicle production of over 30 million units, India's six-airbag mandate effective from October 2023, and progressive C-NCAP and Bharat NCAP safety protocol upgrades elevating curtain airbag fitment requirements.

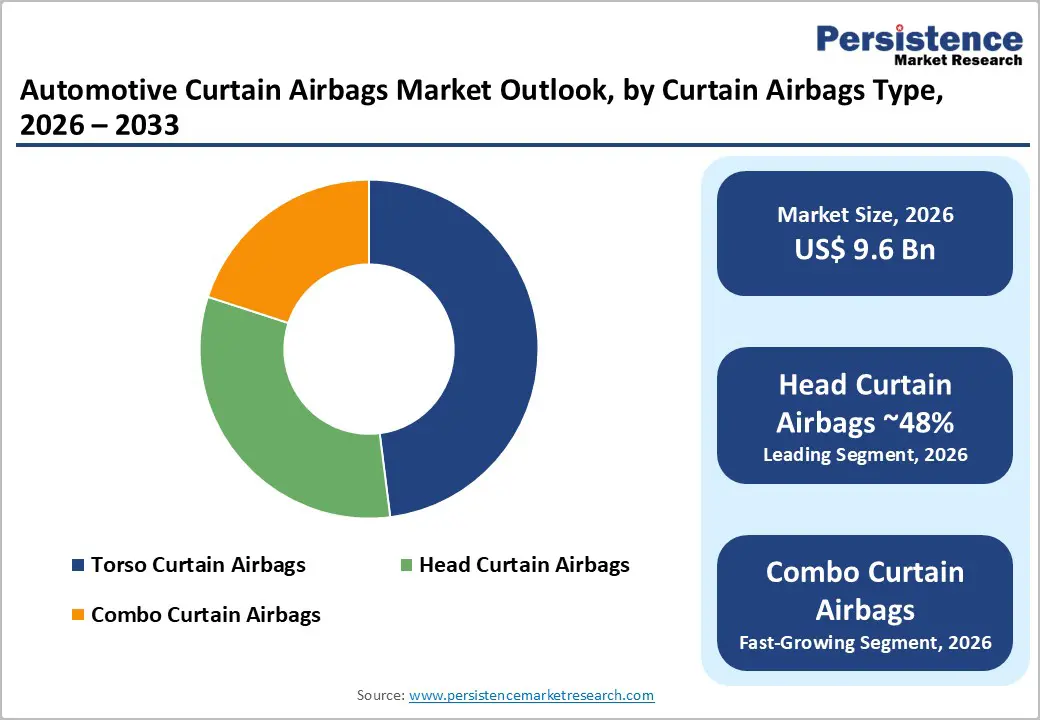

- Leading Segment: Head Curtain Airbags dominate the Curtain Airbags Type category with approximately 48% revenue share in 2026, supported by global regulatory requirements, including FMVSS 226 and Euro NCAP side protection scoring criteria that specifically mandate full-length curtain coverage in passenger vehicles.

- Fastest-Growing Segment: OEMs represent the fastest growing and dominant end-use segment, commanding approximately 88% of market revenue due to factory-fitment mandates, regulatory certification requirements, and platform-level airbag integration that structurally limits aftermarket installation across major markets.

- Opportunities: Electric vehicle platform integration represents the most significant forward opportunity, with global EV stock projected to reach 240 million units by 2030 per IEA, requiring entirely new curtain airbag geometries and deployment architectures tailored to BEV structural configurations, opening a technology-led product development cycle for leading suppliers.

| Key Insights | Details |

|---|---|

| Automotive Curtain Airbags Market Size (2026E) | US$ 9.6 Bn |

| Market Value Forecast (2033F) | US$ 13.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Dynamics

Drivers - Tightening Global Vehicle Safety Regulations Elevating Passive Restraint Requirements

Curtain airbag adoption is fundamentally regulatory-driven, with governments across major automotive markets mandating side and curtain airbag fitment as minimum safety standards. In the United States, the NHTSA's FMVSS 226 standard requires ejection mitigation systems including curtain airbags, across all new light vehicles, while the European Union's General Safety Regulation (GSR) 2019/2144, which came into full effect in 2024, mandates advanced occupant protection systems as standard equipment across all newly type-approved vehicles. The Global New Car Assessment Program (Global NCAP) and its regional affiliates, including Euro NCAP and ASEAN NCAP, have further tightened scoring criteria to reward full curtain coverage and side-impact airbag performance. These converging regulatory vectors are compelling OEMs to standardize curtain airbag fitment across all trim levels, significantly lifting per-vehicle airbag content and supporting the long-term volume and value growth of the Automotive Curtain Airbags Market.

Accelerating Global Vehicle Production and Rising Safety Content Per Vehicle

Global vehicle production volumes directly determine the demand baseline for curtain airbags as a standard-fit safety component. According to the International Organization of Motor Vehicle Manufacturers (OICA), global motor vehicle production recovered to approximately 93.5 million units in 2023 and continued expanding through 2024 and 2025, led by China, the United States, and India. Beyond volume, OEMs are progressively increasing safety content per vehicle, installing multiple airbag modules per unit across front, side, and curtain positions to achieve higher Euro NCAP and NHTSA safety ratings that are increasingly used as key consumer purchase decision criteria. The Insurance Institute for Highway Safety (IIHS) in the United States reports that side curtain airbags reduce the risk of driver death in SUV side-impact crashes by approximately 45%, a statistic widely cited by OEMs in marketing and safety compliance strategies, creating a commercially reinforcing cycle for the expansion of curtain airbag content.

Restraints - High Per-Unit Cost of Advanced Curtain Airbag Systems Constraining Adoption in Price-Sensitive Segments

The incorporation of curtain airbag systems, particularly multi-row combo configurations, adds measurable cost to vehicle build specifications, creating adoption friction in entry-level and economy vehicle segments prevalent across South and Southeast Asian automotive markets. Advanced airbag modules incorporate specially engineered OPW (One-Piece Woven) fabric panels, precision inflator assemblies, and complex ECU integration, all of which carry premium manufacturing costs. In price-sensitive markets such as India, where a significant proportion of passenger vehicles are sold in sub-compact hatchback segments priced below US$ 10,000, OEM pressure on component costs directly constrains the specification of curtain airbags as standard rather than optional equipment, creating a fitment gap that limits total market penetration despite regulatory pressure.

Supply Chain Vulnerabilities in Specialty Textile and Semiconductor Components

Curtain airbag manufacturing depends on a narrowly specialized supply chain encompassing high-tenacity nylon or polyamide airbag-grade fabrics, precision inflation propellant chemistry, and crash detection semiconductor sensors. The global semiconductor shortage of 2021-2023, which reduced global automotive production by an estimated 7.7 million units according to S&P Global Mobility, exposed the acute vulnerability of integrated vehicle safety system supply chains. Ongoing geopolitical trade tensions, raw material concentration risks for nylon feedstocks in Asia, and the limited number of technically qualified inflator propellant manufacturers globally continue to represent structural supply chain risks that can create production delays, cost volatility, and quality compliance challenges for certain airbag manufacturers operating across international supply networks.

Opportunity - Integration of Curtain Airbags in Electric Vehicles and New Vehicle Architectures

The global transition to electric vehicles presents a structurally significant demand opportunity for the Automotive Curtain Airbags Market, driven by the distinct safety architecture requirements of battery electric vehicle (BEV) platforms. EVs exhibit modified crash dynamics compared to internal combustion engine vehicles due to the placement of large battery packs along the underbody, which alters the side-impact energy distribution and underscores the importance of curtain airbag coverage in protecting occupants from battery-related secondary hazards. According to the International Energy Agency (IEA), global electric car stock surpassed 40 million units in 2023 and is on a trajectory to reach 240 million by 2030 across stated policies scenarios. Each new EV platform architected from the ground up offers OEMs the opportunity to redesign curtain airbag geometry, coverage, and deployment logic specifically for EV structural configurations, creating a product innovation cycle.

Emerging Markets and Regulatory Upgrades Driving First-Time Fitment Growth

Regulatory harmonization in rapidly growing automotive markets across South Asia, Southeast Asia, and Latin America is generating a first-time fitment opportunity for curtain airbags that is structurally distinct from the replacement or upgrade cycles prevalent in mature markets. India's Bharat NCAP program, launched by the Ministry of Road Transport and Highways in 2023 and operational for consumer tests from 2024, incentivizes OEMs to achieve five-star ratings, which require comprehensive curtain airbag coverage, across locally manufactured vehicles. Similarly, ASEAN NCAP's 2026-2030 assessment protocol will expand mandatory safety scoring criteria for vehicles sold across the ten-member Association of Southeast Asian Nations bloc. These regulatory upgrades are compelling local and multinational OEMs to retrofit or redesign existing platform specifications to include curtain airbags as standard, creating a multi-year volume step-up in fitment rates across markets where curtain airbag penetration has historically been low relative to developed automotive economies.

Category-wise Analysis

Curtain Airbags Type Insights

The head curtain airbag segment holds the leading position within the curtain airbags type category, accounting for approximately 48% of total market revenue in 2026. Head curtain airbags, also referred to as side curtain airbags, deploy from the roofline along the full side window area to protect occupants' heads during lateral collisions and rollover events. Their dominance is directly attributable to the global regulatory consensus institutionalized through standards such as FMVSS 226 in the United States and UN GTR No. 13 on head restraints under the UNECE framework, which specifically address ejection mitigation and head impact protection in side-impact scenarios. Euro NCAP scoring protocols award significant side protection points for full-curtain head coverage from the A-pillar to the C or D pillar, incentivizing OEMs to standardize head curtain airbag fitment across all rows.

Vehicle Type Analysis

Passenger Cars represent the dominant vehicle type segment in the Automotive Curtain Airbags Market, contributing approximately 78% of total segment revenue in 2026. The passenger car segment's supremacy reflects the combination of the highest global production volumes, the deepest regulatory penetration of curtain airbag fitment mandates, and the highest consumer sensitivity to safety ratings in purchasing decisions. According to OICA, passenger cars accounted for more than 68 million units of global vehicle production in 2023, providing the broadest fitment base for curtain airbag suppliers. Within passenger cars, the SUV and crossover sub-segments are particularly strong demand drivers, as their higher center of gravity relative to sedans creates elevated rollover risk, making comprehensive curtain airbag coverage both a regulatory requirement and a consumer expectation.

End Use Analysis

OEMs constitute the dominant end-use segment for curtain airbags, accounting for approximately 80% of total market revenue in 2026. The OEM channel's dominance reflects the fundamental nature of curtain airbags as a factory-fitted, safety-critical passive restraint component that is integrated into the vehicle's structural and electrical architecture at the point of manufacture, rendering aftermarket installation technically complex, costly, and in many legally constrained jurisdictions. OEM procurement relationships are typically governed by long-term supply agreements spanning vehicle platform lifecycles of four to seven years, creating highly stable, predictable demand pipelines for Tier-1 suppliers. The automotive wheel coating market and other adjacent automotive component markets similarly demonstrate the OEM channel's dominance in safety and structural components.

Regional Insights

North America Automotive Curtain Airbags Trends

North America is the most mature regional market for automotive curtain airbags, shaped by a combination of the world's most established vehicle safety regulatory infrastructure, high consumer safety awareness, and the dominant presence of leading Tier-1 airbag system suppliers. The NHTSA's FMVSS 226 ejection mitigation standards, enforced as a mandatory requirement for all new light vehicles sold in the United States, effectively mandate curtain airbag coverage across virtually all new passenger vehicle registrations.

The United States automotive industry's rapid transition toward SUVs, crossovers, and light trucks, which accounted for over 80% of new vehicle sales in the country in 2024, according to Ward's Automotive, further intensifies regional demand for full-length curtain airbag systems. Companies, including Autoliv and ZF Friedrichshafen AG, maintain significant R&D and manufacturing presence in North America, enabling close collaboration with domestic OEMs on next-generation airbag architectures compatible with EV platforms.

Europe Automotive Curtain Airbags Trends

Europe's curtain airbag market is anchored by the continent's dual role as both a leading vehicle production hub and the originator of the world's most influential consumer vehicle safety assessment program. Euro NCAP, headquartered in Brussels, Belgium, has systematically elevated curtain airbag performance requirements across successive five-year assessment protocols, with its 2026-2030 roadmap further expanding side and curtain protection scoring criteria to cover full occupant rows in longer SUV and MPV body styles.

The European Union's General Safety Regulation (EU GSR) 2019/2144 is fully operative for all new vehicle type approvals from July 2024, mandating advanced occupant safety systems, including side and curtain airbags, as standard equipment. The United Kingdom, following its post-Brexit adoption of UNECE technical regulations through the Vehicle Type Approval framework, maintains harmonized curtain airbag standards aligned with EU requirements.

Asia Pacific Automotive Curtain Airbags Trends

Asia Pacific represents the most dynamic volume growth geography for the Automotive Curtain Airbags Market, driven by the combination of the world's two largest automotive production economies in China and Japan, rapidly accelerating safety regulation mandates in India and ASEAN member states, and the progressive migration of vehicle safety content from premium-only to mainstream segments.

Japan serves as both a major demand market and the headquarters of critical curtain airbag technology innovators, including TOYODA GOSEI Co., Ltd., Ashimori Industry Co., Ltd., and SEIREN Co., Ltd., whose materials and manufacturing technologies underpin global supply chains for OPW airbag fabric and inflator components. In India, the Ministry of Road Transport and Highways notification mandating six airbags as standard in vehicles with up to eight seats implemented from October 2023 has materially elevated curtain airbag fitment requirements for vehicles sold in the country, while the newly launched Bharat NCAP programmed creates consumer incentive structures favoring comprehensive curtain airbag coverage.

Competitive Landscape

The global Automotive Curtain Airbags Market is moderately consolidated, with a small number of technically specialized Tier-1 suppliers commanding many global OEM supply relationships. Autoliv and ZF Friedrichshafen AG jointly account for a substantial portion of global curtain airbag revenues, while TOYODA GOSEI Co., Ltd., Ashimori Industry Co., Ltd., and Yanfeng operate as significant regional and global challengers. Competitive differentiation is driven by proprietary OPW fabric technology, inflator chemistry innovation, multi-sensor crashes detection integration, and the ability to co-develop airbag geometries for new EV platform architectures.

Key Market Developments

- In December 2024, Autoliv and Jiangling Motors entered a strategic partnership to co-develop advanced restraint systems for next-generation EV platforms.

- In November 2024, BMW issued recall 24V-856 after discovering right-side head curtain airbag gas generators were installed 180 degrees out of specification, risking mis-deployment.

- In October 2024, Toyoda Gosei expanded its Neemrana, India airbag plant to meet tightening regional safety mandates and serve Suzuki and Toyota programs.

Companies Covered in Automotive Curtain Airbags Market

- ZF Friedrichshafen AG

- Kolon Industries, Inc.

- Ashimori Industry, Co., Ltd.

- TOYODA GOSEI Co., Ltd.

- Sumitomo Corporation

- SEIREN Co., LTD.

- Yanfeng

- TG Missouri

- Scania Group

- Autoliv

- Other Key Players

Frequently Asked Questions

The global Automotive Curtain Airbags Market is projected to reach US$ 13.9 Bn by 2033, growing from US$ 9.6 Bn in 2026 at a forecast CAGR of 5.4% between 2026 and 2033.

The principal drivers are tightening vehicle safety regulations including NHTSA's FMVSS 226, EU GSR 2019/2144, and Euro NCAP assessment protocols alongside accelerating global vehicle production volumes, growing consumer demand for higher safety-rated vehicles, and the progressive standardization of curtain airbag fitment across all vehicle trim levels.

The Head Curtain Airbag segment leads the Curtain Airbags Type category with approximately 48% of total market revenue in 2026, driven by its mandatory status under FMVSS 226 in the United States and its critical role in achieving high Euro NCAP side-impact and rollover protection scores globally.

North America is the leading regional market, supported by comprehensive NHTSA mandates for ejection mitigation systems, the dominance of SUVs and light trucks exceeding 80% of new vehicle sales, and the headquarters presence of world-leading Tier-1 airbag system suppliers including Autoliv and ZF Friedrichshafen AG.

Leading companies in the Automotive Curtain Airbags Market include Autoliv, ZF Friedrichshafen AG, TOYODA GOSEI Co., Ltd., Ashimori Industry Co., Ltd., Yanfeng, Kolon Industries, Inc., SEIREN Co., Ltd., and TG Missouri, among others.