- Automotive Components & Materials

- Automotive Brake Valve Market

Automotive Brake Valve Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Brake Valve Market by Function Type (Hydraulic, Pneumatic, Electronic), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), Material Type (Steel, Aluminum, Brass, Composite Materials), Sales Channel (OEM, Aftermarket), and Regional Analysis for 2026 - 2033

Automotive Brake Valve Market Size and Trend Analysis

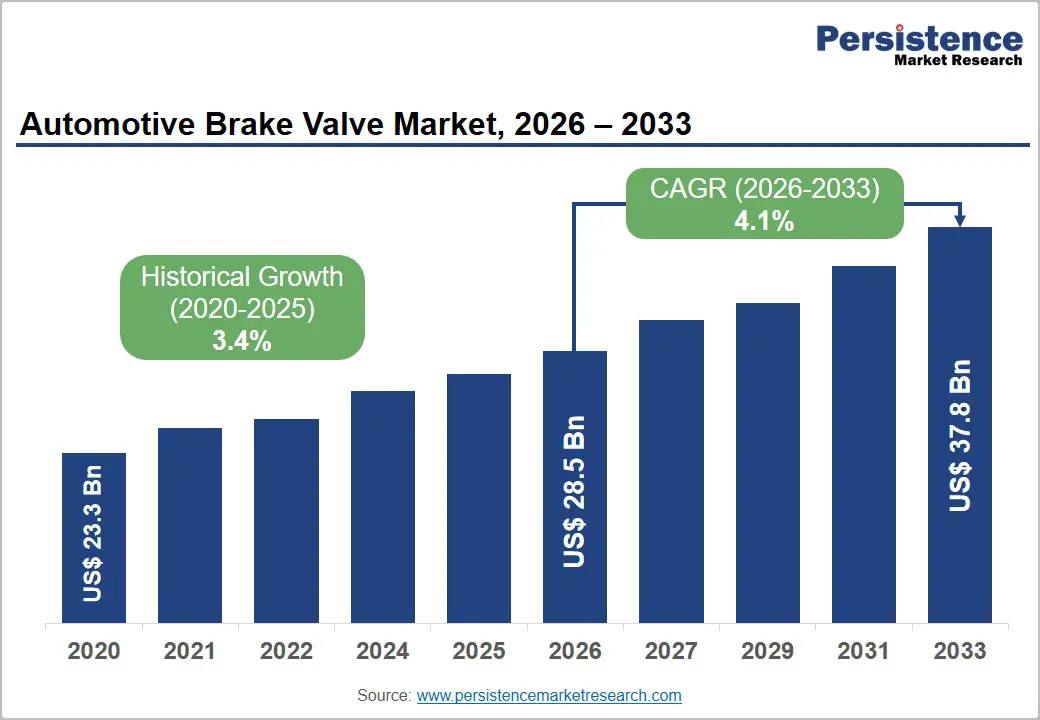

The global Automotive Brake Valve market size is valued at US$ 28.5 Bn in 2026 and is projected to reach US$ 37.8 Bn by 2033, growing at a CAGR of 4.1% between 2026 and 2033.

The market is driven by sustained global vehicle production growth, tightening road safety regulations mandating advanced braking standards across all vehicle categories and accelerating commercial vehicle fleet electrification requiring next-generation electronic and electro-hydraulic brake valve systems.

Key Market Highlights

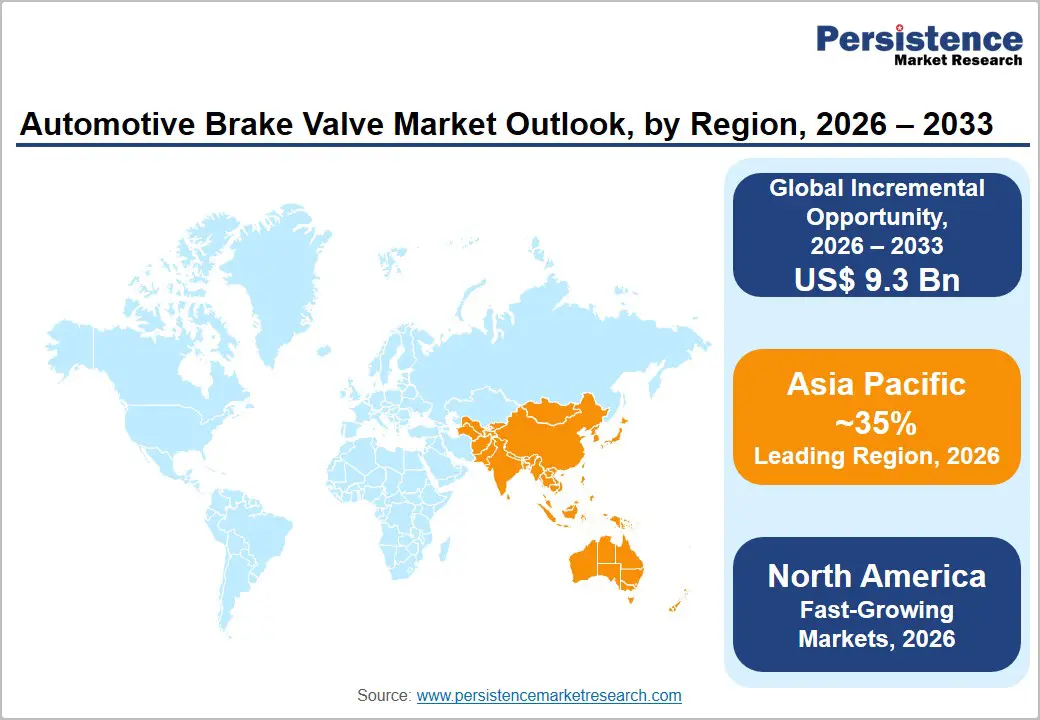

- Leading Region – Asia Pacific leads the global Automotive Brake Valve market with approximately 35% revenue share in 2026, driven by China’s massive vehicle production scale, mandatory ABS and AEBS adoption, and India’s rapidly expanding vehicle parc under progressive braking safety regulatory enforcement.

- Fastest Growing Region – Asia Pacific is also the fast-growing region, with India recording a CAGR of approximately 4.9%, propelled by AIS-145 ABS mandates, BNCAP safety rating incentives, and a rapidly expanding commercial vehicle fleet generating growing OEM and aftermarket brake valve demand.

- Dominant Segment – Hydraulic brake valves lead the function type category with approximately 52% share in 2026, underpinned by their universal adoption across all passenger car platforms globally and proven reliability under ABS, ESC, and increasingly AEBS regulatory mandate requirements.

- Fastest Growing Segment – Electronic Brake Valves are the fastest-growing function type segment, driven by universal AEBS and ESC mandates under EU General Safety Regulation 2019/2144, U.S. NHTSA AEB rules, and EV electro-hydraulic integration requirements creating sustained demand across global OEM production programs.

- Key Opportunity – Electronic brake valve systems for AEBS-compliant commercial vehicles represent the highest-growth opportunity, as UNECE Regulation No. 131 extension and NHTSA mandates for heavy truck AEB drive large-scale OEM adoption of integrated electronic braking valve modules across global commercial vehicle production lines through 2033.

DRO Analysis

Drivers - Tightening Global Road Safety Regulations Mandating Advanced Braking System Integration

Escalating road safety mandates across major automotive markets are the most powerful structural driver of advanced brake valve adoption, compelling OEMs to integrate superior hydraulic and electronic braking components to achieve regulatory compliance.

The EU General Safety Regulation (EU) 2019/2144 requires Advanced Emergency Braking Systems (AEBS) on all new passenger cars and commercial vehicles from July 2024 and July 2022 respectively, directly increasing the demand for precision electronic and electro-hydraulic brake valve assemblies capable of supporting automated braking functions.

The World Health Organization (WHO) reports that approximately 1.35 million people die annually in road traffic crashes globally, maintaining strong political pressure for safety technology mandates.

Growing Commercial Vehicle Fleet and Expanding Vehicle Parc Sustaining Aftermarket Demand

The steady global expansion of the commercial vehicle fleet driven by e-commerce growth, infrastructure investment, and freight demand increases is generating durable structural demand for brake valves across both OEM and aftermarket channels. According to the International Road Transport Union (IRU), global road freight demand is projected to grow by approximately 45% between 2020 and 2050, requiring commensurate expansion of the truck and bus fleet and associated braking system procurement.

The International Organization of Motor Vehicle Manufacturers (OICA) documents a global vehicle parc exceeding 1.4 billion registered vehicles, each requiring periodic brake system inspection, maintenance, and component replacement according to national roadworthiness standards.

Restraints - Transition to Brake-by-Wire Technology Displacing Traditional Valve Architectures

The progressive adoption of brake-by-wire (BBW) and electro-mechanical braking systems in advanced passenger car platforms, eliminating or fundamentally restructuring hydraulic and pneumatic valve architectures, poses a structural displacement risk for conventional brake valve suppliers over the medium term.

Pure electric vehicles using regenerative braking systems reduce hydraulic brake actuation frequency significantly, potentially extending brake component replacement intervals and reducing aftermarket volumes. Continental AG’s MK C1 brake-by-wire system and ZF’s EBB (Electric Brake Booster) represent OEM-level BBW deployments beginning to reshape brake system architectures in premium and EV platforms, requiring traditional brake valve manufacturers to invest in electro-mechanical alternatives to maintain OEM supply relevance.

Raw Material Price Volatility Compressing Component Manufacturer Margins

Brake valve manufacturing is material-intensive, utilizing steel, aluminum, brass, and engineering polymers whose prices exhibit substantial cyclical volatility driven by energy prices, mining output, and geopolitical supply chain disruptions. According to the London Metal Exchange (LME), steel and aluminum prices experienced peak-to-trough swings of over 40–50% between 2020 and 2023 due to pandemic-era supply disruptions and energy market impacts.

For brake valve manufacturers operating on thin contract margins with limited ability to pass through input cost increases under fixed-price OEM supply agreements, raw material price volatility directly compresses operating margins and can challenge capital investment programs required for technology modernization.

Opportunities - Electronic Brake Valve Systems for Commercial Vehicle AEBS and ESC Compliance

The global regulatory mandate for Advanced Emergency Braking Systems (AEBS) and Electronic Stability Control (ESC) on commercial vehicles represents a structurally high-growth opportunity for electronic brake valve system suppliers with certified OEM supply capabilities. The UNECE Regulation No. 131 mandating AEBS on heavy commercial vehicles has been extended to additional vehicle categories, and the European Commission’s roadmap requires ESC on all new coach and bus types. In the United States, the National Highway Traffic Safety Administration (NHTSA) finalized its rule requiring AEB systems on new trucks over 10,000 lbs GVWR in 2024.

Aftermarket Brake Valve Replacement in Asia Pacific and Latin America High-Growth Economies

The expanding vehicle parc in high-growth economies particularly across India, Southeast Asia, Brazil, and Mexico is creating a structurally growing aftermarket brake valve replacement opportunity as aging multi-million-unit commercial and passenger vehicle fleets reach component replacement cycles. India’s vehicle parc exceeded 310 million registered vehicles in 2023 per Ministry of Road Transport and Highways (MoRTH) data, with commercial vehicle fleet age profiles creating substantial recurring brake system maintenance demand.

Brazil and Mexico together accounting for over 5 million annual vehicle sales maintain large, aging commercial vehicle fleets operating under national vehicle inspection regimes that mandate periodic brake system certifications.

Category-wise Analysis

Function Type Insights

The hydraulic segment leads the automotive brake valve market by function type, accounting for approximately 52% of total market revenue in 2026. Hydraulic brake valves encompassing master cylinders, ABS modulator valves, proportioning valves, and brake pressure regulators are the dominant braking technology in passenger cars and light commercial vehicles globally, which collectively constitute the majority of global vehicle production volume.

The widespread, proven adoption of hydraulic braking across all major OEM passenger car platforms from entry-level economy vehicles to premium segment cars reflects the technology’s mature reliability, cost-effectiveness, and performance consistency across a wide range of operating temperatures and load conditions.

Vehicle Type Insights

The passenger cars segment dominates the automotive brake valve market by vehicle type, accounting for approximately 58% of total market revenue in 2026. This segment’s leadership is a direct function of passenger cars’ overwhelming share of global vehicle production with approximately 70 million passenger cars produced annually per OICA statistics combined with the mandatory fitment of ABS, ESC, and increasingly AEBS systems across all new passenger car categories in the European Union, United States, China, and India.

The EU General Safety Regulation (2019/2144) mandating advanced driver assistance systems including AEB on all new passenger cars from July 2024 is increasing brake valve content per vehicle in the passenger car segment globally, reinforcing its market leadership beyond the pure volume advantage conferred by production scale.

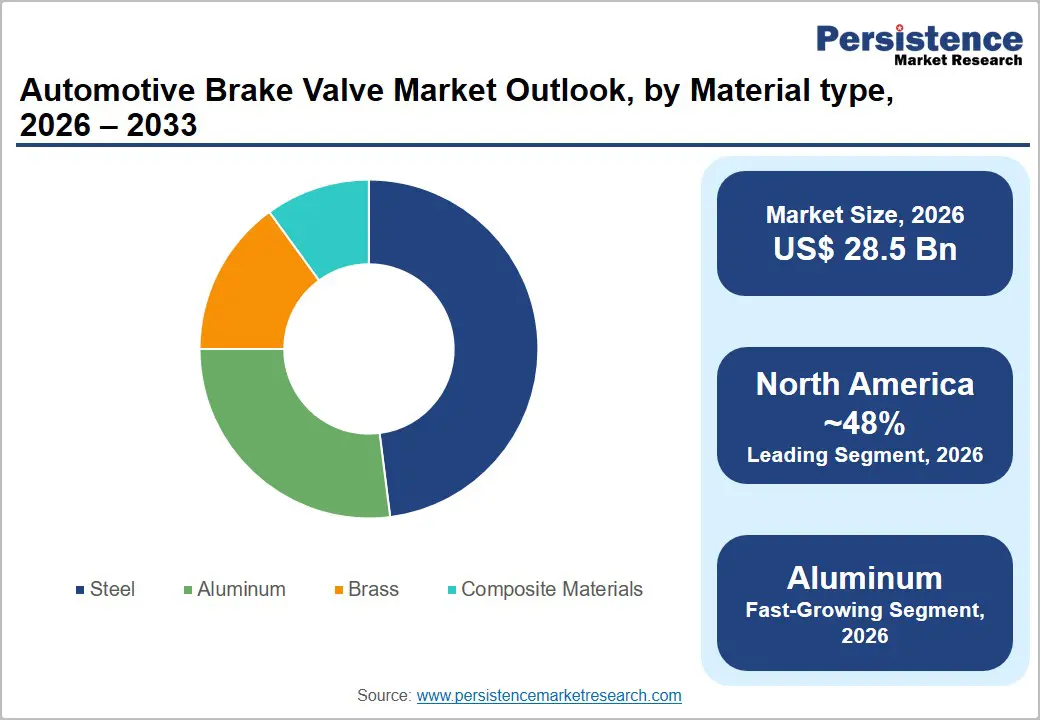

Material Type Insights

The steel segment leads the automotive brake valve market by material type, likely to command approximately 48% of total revenue in 2026. Steel’s dominance reflects its unmatched combination of mechanical strength, fatigue resistance, compatibility with hydraulic and pneumatic pressure requirements, and cost-effectiveness at the production volumes demanded by global automotive OEM supply contracts.

Brake valve bodies, housings, and valve spools fabricated from high-strength carbon and stainless-steel alloys consistently meet the stringent pressure integrity, corrosion resistance, and dimensional stability requirements specified by automotive safety standards including ISO 26262 (functional safety) and UNECE Regulation No. 13.

Sales Channel Insights

The OEM channel leads the automotive brake valve market by sales channel, accounting for approximately 65% of total revenue in 2026. OEM procurement dominance reflects the fundamental requirement of brake valves as safety-critical, mandatory components integrated into every new vehicle at the point of manufacture ensuring a guaranteed, high-volume, recurring revenue stream tied directly to global vehicle production volumes. Tier-1 brake system suppliers including Robert Bosch GmbH, Continental AG, and Knorr-Bremse AG supply integrated brake valve modules directly to OEM assembly lines under multi-year platform supply agreements, capturing substantial forward revenue visibility.

Regional Insights

North America Automotive Brake Valve Market Trends & Analysis

North America represents a mature and regulatory-driven automotive brake valve market, with the United States anchoring regional demand through its combination of world-leading vehicle production volumes, stringent FMVSS braking standards, and a large and aging commercial vehicle fleet generating substantial aftermarket replacement demand.

The North American commercial vehicle segment is an equally important demand driver, with the American Trucking Associations (ATA) reporting a U.S. truck fleet of over 3.5 million Class 6–8 trucks requiring periodic brake system inspection and certification under Federal Motor Carrier Safety Administration (FMCSA) Commercial Vehicle Safety Alliance (CVSA) standards.

U.S. Automotive Brake Valve Market Size

The United States dominates the North American automotive brake valve market, accounting for approximately 85% of regional revenue in 2026. The country's leadership is supported by its large automotive production base, strong commercial vehicle manufacturing sector, and growing adoption of advanced braking and vehicle safety technologies.

Europe Automotive Brake Valve Market Trends, Drivers, & Insights

Europe is the most regulatory-advanced regional automotive brake valve market, characterized by the EU General Safety Regulation (2019/2144) driving comprehensive advanced braking system mandates across vehicle categories, and the presence of global brake valve technology leaders including Robert Bosch GmbH, Continental AG, Knorr-Bremse AG, and ZF Friedrichshafen AG that simultaneously serve as OEM system integrators and Tier-1 suppliers. Germany accounts for the largest share of European brake valve demand, hosting the continent’s highest concentration of automotive OEM headquarters and Tier-1 supplier production facilities.

Germany Automotive Brake Valve Market Size

Germany leads the European Automotive Brake Valve market with approximately 25% of regional revenue in 2026. The German market is valued at approximately US$ 1.9 Bn in 2026 and is projected to reach approximately US$ 2.5 Bn by 2033, reaching an estimated 4% CAGR in the forecast period. The country's strong automotive manufacturing ecosystem, advanced commercial vehicle production, and emphasis on vehicle safety and braking technologies continue to drive market demand.

U.K. Automotive Brake Valve Market Size

The United Kingdom accounts for approximately 14% of the European Automotive Brake Valve market revenue in 2025. The UK market is valued at approximately US$ 1.1 Bn in 2026 and projected to reach approximately US$ 1.4 Bn. The UK’s brake valve market is supported by Jaguar Land Rover’s domestic production deploying advanced hydraulic and electronic brake systems alongside a large commercial vehicle fleet requiring recurring brake system maintenance.

France Automotive Brake Valve Market Size

France accounts for approximately 11% of the European automotive brake valve market in 2026, supported by its established automotive manufacturing industry, growing focus on vehicle safety, and increasing integration of advanced braking systems in passenger and commercial vehicles. The French automotive brake valve market is valued at approximately US$ 0.8 billion in 2026 and is projected to reach nearly US$ 1.1 billion registering a CAGR of approximately 4.2% during the forecast period. Continued investments in automotive innovation and stricter safety standards are expected to sustain market growth.

Asia Pacific Automotive Brake Valve Market Drivers & Analysis

Asia Pacific is the largest regional market for Automotive Brake Valves, accounting for approximately 35% of global revenue in 2025, driven by China’s massive vehicle production scale, Japan’s advanced automotive technology ecosystem, and India’s rapidly expanding vehicle market with accelerating braking safety regulation enforcement. The region is also the fastest-growing market, propelled by rising vehicle parc expansion across ASEAN economies and aggressive adoption of ABS and ESC mandates across China, India, and Southeast Asian markets that are systematically increasing brake valve content per vehicle across domestic OEM production lines.

China Automotive Brake Valve Market Size

China is the dominant national market within Asia Pacific, accounting for approximately 42% of regional revenue in 2025. The Chinese market is valued at approximately US$ 4.2 Bn in 2026 and is projected to reach approximately US$ 5.5 Bn by 2033, growing at a CAGR of approximately 3.9%.

China’s automotive brake valve market is anchored by its production of over 30 million vehicles annually, combined with regulatory mandates requiring ABS on all new passenger vehicles and progressive extension of ESC and AEBS requirements to additional vehicle categories under evolving China Compulsory Certification (CCC) standards.

India Automotive Brake Valve Market Size

India accounts for approximately 15% of the Asia Pacific automotive brake valve market revenue in 2025, driven by expanding automotive production, rising commercial vehicle demand, and increasing adoption of advanced braking systems to meet evolving safety standards. The Indian automotive brake valve market is valued at approximately US$ 1.5 billion in 2026 and is projected to reach nearly US$ 2.1 billion by 2033, registering a CAGR of approximately 4.9% during the forecast period, among the highest growth rates in the Asia Pacific region. Government initiatives supporting domestic vehicle manufacturing and stricter safety regulations are expected to further strengthen market expansion.

Japan Automotive Brake Valve Market Size

Japan accounts for approximately 20% of the Asia Pacific automotive brake valve market revenue in 2025, supported by its advanced automotive manufacturing industry, strong presence of leading OEMs, and continuous innovation in vehicle safety and braking technologies. Increasing adoption of advanced driver assistance systems (ADAS) and high-performance braking solutions is expected to sustain steady market growth.

Competitive Landscape

The automotive brake valve market is moderately consolidated, dominated by global Tier-1 automotive suppliers with significant R&D capabilities, established OEM long-term supply agreements, and broad geographic manufacturing footprints. Market leaders Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG (following WABCO integration), and Knorr-Bremse AG collectively command a substantial global market share through integrated brake system platforms spanning passenger and commercial vehicles. Competitive differentiation centres on systems integration expertise, homologated electronic control software, lightweight material adoption, and closed-loop product development with OEMs.

Key Developments:

- In June 2025, ZF CV Systems Europe BV filed an international PCT application (PCT/EP2024/082346, published as WO/2025/114024) for a method of operating a valve assembly that activates an electropneumatic parking brake at a standstill.

- In October 2024, Cummins Drivetrain and Braking Systems (CDBS), a division of Cummins Inc.’s Components segment, is significantly boosting its production capacity for air disc brakes (ADBs) and rear axles with strategic investments exceeding USD 190 million. This move highlights Cummins’ dedication to addressing the surging demand for sophisticated braking and axle solutions in the commercial vehicle arena.

Companies Covered in Automotive Brake Valve Market

- Robert Bosch GmbH

- Knorr-Bremse AG

- ZF Friedrichshafen AG (WABCO)

- Continental AG

- Haldex AB

- Mando Corporation

- Aisin Corporation

- JTEKT Corporation

- Akebono Brake Industry Co., Ltd.

- BorgWarner Inc.

- Tenneco Inc. (DRiV Motorparts)

- Brembo S.p.A.

Frequently Asked Questions

The global Automotive Brake Valve market is valued at US$ 28.5 billion in 2026 and is projected to reach US$ 37.8 billion by 2033, growing at a CAGR of 4.1% during the forecast period.

Primary demand drivers include tightening global vehicle safety regulations notably the EU General Safety Regulation (2019/2144) mandating AEBS and ESC on all new vehicles from 2022–2024, and the NHTSA AEB rule for U.S. light vehicles by 2029alongside growing commercial vehicle fleets generating aftermarket replacement demand.

Hydraulic Brake Valves hold the largest function type share at approximately 52% of global revenue in 2025. Their dominance is driven by universal adoption across passenger car platforms globally which represent over 80% of new vehicle registrations in major markets combined with regulatory mandates for ABS and ESC systems that are predominantly hydraulic in architecture for passenger vehicle applications.

Asia Pacific is the leading region with approximately 35% of global Automotive Brake Valve revenue in 2025. China dominates with approximately 42% of the regional share, supported by the world’s largest annual vehicle production exceeding 30 million units and regulatory mandates requiring ABS fitment on all new passenger vehicles.

Key companies include Robert Bosch GmbHthe world’s largest automotive supplier with dominant ABS and ESC brake valve market share Knorr-Bremse AG, ZF Friedrichshafen AG following its WABCO acquisition, Continental AG, Aisin Corporation, Mando Corporation, Haldex AB, and Brembo S.p.A..