- Automotive Components & Materials

- Automotive Aluminium Market

Automotive Aluminium Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Aluminium Market by Application (Body Structure, Powertrain, Suspension, Others), End-Use (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), and Regional Analysis for 2026 - 2033

Automotive Aluminium Market Size and Trend Analysis

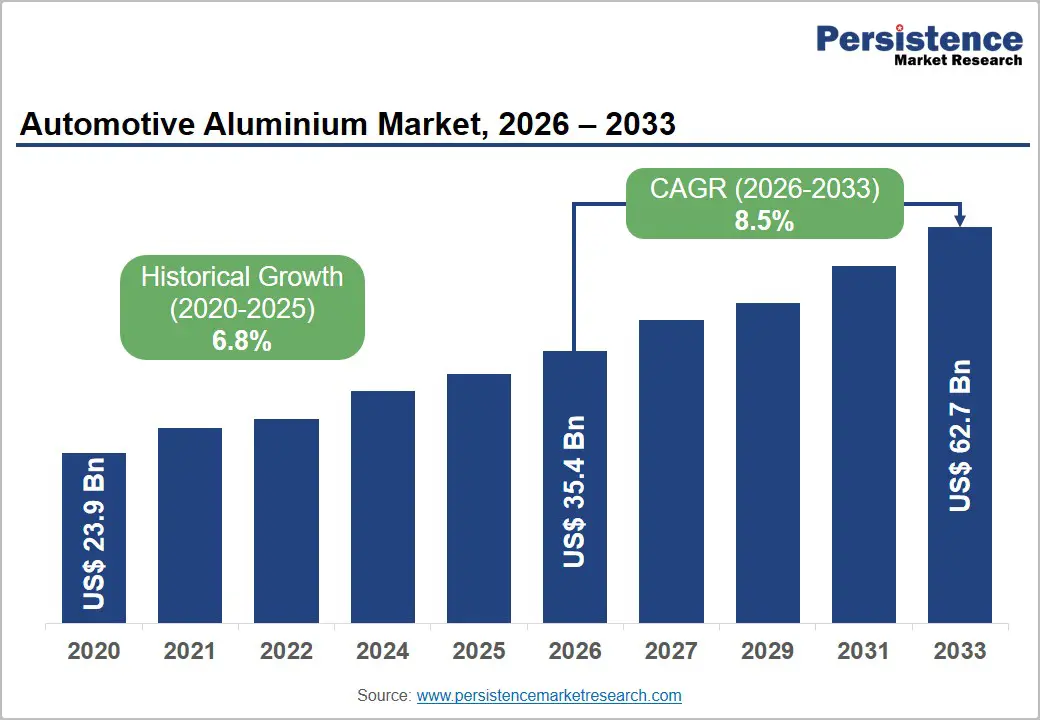

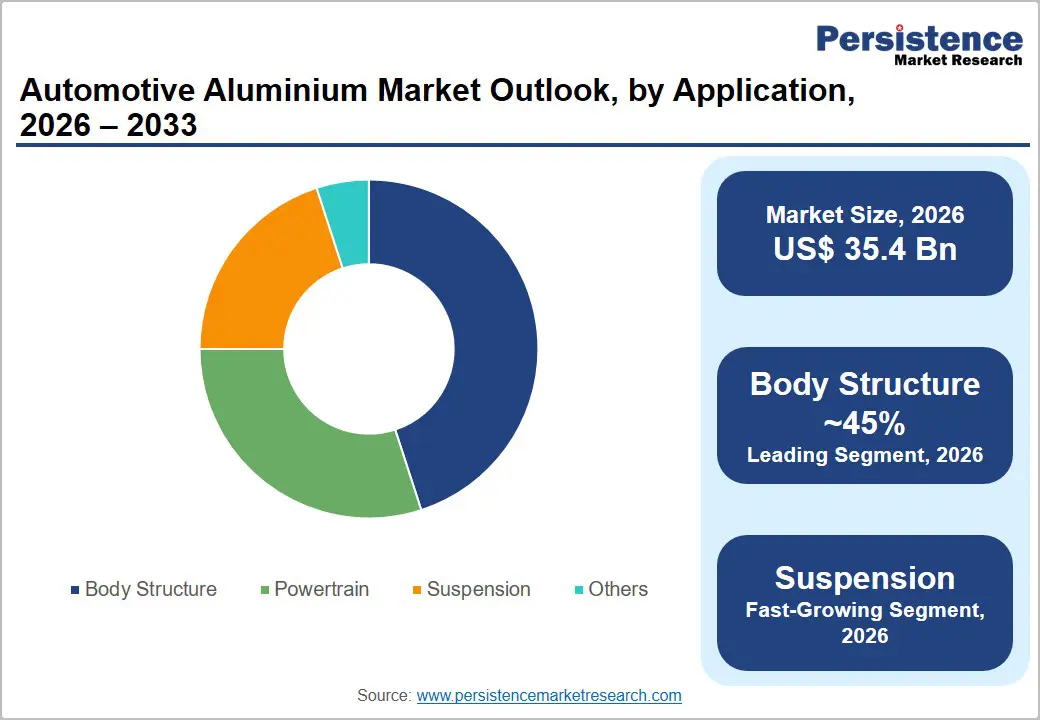

The global automotive aluminium market size is valued at US$ 35.4 Bn in 2026 and is projected to reach US$ 62.7 Bn by 2033, growing at a CAGR of 8.5% between 2026 and 2033.

The market is propelled by the automotive industry’s structural transition toward lightweighting for fuel efficiency and electric vehicle (EV) range optimization, tightening global vehicle emission standards, and rapid EV adoption that requires aluminum-intensive battery enclosures, structural frames, and thermal management systems. The European Union’s CO2 emission standard requiring fleet-average emissions of 95 g CO2/km from passenger cars and the U.S.

Key Industry Highlights:

- Leading Region – Asia Pacific leads the global Automotive Aluminium market with approximately 38% revenue share in 2025, driven by China’s position as the world’s largest EV and vehicle producer operating under strict CAFC emission standards that mandate aluminum-intensive lightweighting across OEM vehicle fleets.

- Fastest Growing Region – Asia Pacific is also the fastest-growing market with India automotive aluminium market reaching a CAGR of approximately 8.7%, driven by CAFE norm compliance, FAME II scheme incentives for EVs, and multinational OEM investment in India as a rapidly growing vehicle manufacturing and export hub.

- Dominant Segment – Body structure leads the application category with approximately 42% market share in 2026, anchored by widespread adoption of aluminum body panels and crash structures across premium and mass-market vehicle platforms globally in response to CO? emission mandates.

- Fast-growing Segment – Electrified vehicle platforms are creating the fastest-growing sub-demand for automotive aluminium particularly battery enclosures and underbody structural components as global EV sales growing at over 35% annually per the IEA drive accelerating per-vehicle aluminum content uplift versus conventional ICE vehicles.

- Key Opportunity – Giga casting technology adoption by Tesla, Volkswagen, Toyota, and BMW represents a transformational opportunity for automotive aluminum die-casting alloy suppliers, as single large-format castings replace 70–100 stamped components, driving new high-volume demand for giga casting-optimized aluminum alloy grades.

Market Dynamics

Drivers - Stringent Global Vehicle Emission Regulations Mandating Lightweighting

Tightening emission standards across major automotive markets are the most powerful structural driver of automotive aluminum demand. The European Union’s Regulation (EU) 2019/631 mandates a fleet-average CO? target of 95 g/km for passenger cars, declining further to 0 g/km effectively by 2035 as the EU phases out new ICE vehicle sales.

The U.S. EPA’s 2024 light-duty vehicle greenhouse gas standards require average fleet emissions of approximately 82 g CO?/mile by 2032 achievable only through significant vehicle weight reduction. Every 10% reduction in vehicle weight achieves approximately a 6–8% improvement in fuel efficiency according to the U.S. Department of Energy (DOE).

Accelerating Electric Vehicle Production Amplifying Per-Vehicle Aluminium Content

The rapid global transition to electric vehicles is creating a multiplier effect on automotive aluminum demand, as EVs require significantly more aluminum per vehicle than conventional ICE counterparts. Battery electric vehicles (BEVs) use aluminum extensively for battery enclosure housings, underbody structural frames, thermal management components, and aluminum-intensive multi-material body structures designed to offset battery weight. The IEA’s Global EV Outlook 2024 reports that global EV sales reached 14 million units in 2023a 35% increase over 2022with EV penetration of new car sales reaching 18% globally.

Restraints - High Processing and Fabrication Costs Relative to Conventional Steel

Despite aluminium’s lightweighting advantages, its higher raw material and processing costs relative to conventional high-strength steel remain a persistent barrier limiting adoption across cost-sensitive vehicle segments. Aluminum costs approximately 3–4 times more per kilogram than advanced high-strength steel (AHSS), and aluminum body manufacturing requires specialized stamping equipment, joining technologies, and surface treatment processes that necessitate significant capital investment.

According to the Centre for Automotive Research (CAR), aluminum-intensive vehicle bodies add approximately US$ 500–1,000 to vehicle manufacturing cost compared to steel equivalents, creating a viability challenge in compact and entry-level vehicle segments where cost-to-consumer sensitivity is high.

Recycling and Supply Chain Infrastructure Constraints

Automotive-grade aluminum recycling while technically efficient, with recycled aluminum requiring only 5% of the energy needed to produce primary aluminum per the Aluminum Association faces supply chain challenges in segregating high-grade automotive alloys from mixed scrap streams.

Achieving closed-loop recycling of multi-alloy automotive aluminum components requires sophisticated sorting, remelting, and alloy correction infrastructure that is nascent in most global markets. Contamination of automotive aluminum scrap can degrade alloy performance, limiting its re-use in structural applications and constraining the circular economy value proposition for automotive aluminum at scale.

Opportunities - Gigacasting and Mega-Casting Technology Revolutionizing Aluminium Structural Integration

The adoption of high-pressure die-casting technologies particularly gigacasting platforms pioneered by Tesla for its Model Y and Cybertruck rear underbody structures represents a transformational manufacturing opportunity that is redefining aluminium’s role in automotive body structures.

Gigacasting replaces assemblies of 70–100 stamped and welded steel components with single large aluminum castings, reducing part counts, assembly time, and factory floor space while improving structural performance and reducing vehicle weight. Volkswagen Group, Toyota, Volvo Cars, and BMW have each announced gigacasting program investments, creating surging demand for large-format aluminum die-casting alloys and high-pressure casting machinery.

Asia Pacific EV Boom and Localised Aluminium Supply Chain Development

The explosive growth of EV production across Asia Pacific particularly in China, which produced over 9.5 million new energy vehicles (NEVs) in 2023 according to the China Association of Automobile Manufacturers (CAAM)is creating vast and concentrated demand for automotive aluminum in one of the world’s most accessible manufacturing geographies.

China’s national policy targets under the New Energy Vehicle Industry Development Plan (2021–2035) call for NEVs to account for 20% of new vehicle sales by 2025 (already achieved) and over 50% by 2035. Companies investing in integrated, localized aluminum production, processing, and delivery capabilities within China and India where vehicle production is growing rapidly are positioned to capture long-term supply contracts from major domestic OEMs and global automotive manufacturers operating regional production facilities.

Category-wise Analysis

Application Insights

The body structure segment leads the automotive aluminium market by application, commanding approximately 42% of total revenue in 2025. Aluminum body structures encompassing hoods, door panels, fenders, trunk lids, roof panels, and structural crash-management components represent the highest-volume and highest-visibility application for automotive aluminum, directly addressable through OEM lightweighting mandates.

The adoption of aluminum-intensive body structures has expanded progressively from premium segment vehicles to mainstream models: Ford’s F-150 pickup truck the world’s best-selling vehicle for over four decades adopted an all-aluminum body in its 2015 redesign, reducing vehicle weight by approximately 700 lbs and demonstrating the commercial viability of mass-market aluminum body structures.

The rapid proliferation of aluminum-dominant multi-material body architectures across global OEM EV platforms ensures that the body structure segment will maintain its leading position through the forecast period.

End-user Insights

The passenger cars dominate the automotive aluminium market by end-use, accounting for approximately 65% of total revenue in 2026. Passenger cars are the primary driver of automotive aluminum consumption due to the segment’s sheer production volume with approximately 70 million passenger cars produced globally each year per International Organization of Motor Vehicle Manufacturers (OICA) data combined with the segment’s leadership in both regulatory compliance pressure and EV transition pace.

Passenger car manufacturers face the most stringent average fleet emission targets across all vehicle categories and have invested most aggressively in aluminum-intensive architectures to meet CO? mandates. Premium passenger car OEMs including BMW, Audi, and Mercedes-Benz have pioneered all-aluminum space frame architectures, while mainstream OEMs are progressively expanding aluminum application across exterior panels, structural components, and powertrain castings within their passenger car portfolios globally.

Regional Analysis

North America Automotive Aluminium Market Trends & Analysis

North America represents a mature and technologically advanced automotive aluminum market, accounting for approximately 22% of global revenue in 2026. The region is characterized by high average aluminum content per vehicle estimated at approximately 208 lbs per vehicle per Ducker Worldwide benchmarks for the North American fleet driven by the widespread adoption of aluminum body structures in popular light trucks and SUVs, which dominate the North American vehicle sales mix.

U.S. Automotive Aluminium Market Size

The United States remains the largest contributor to the North American automotive aluminum market, accounting for approximately 88% of the region's total revenue in 2026. Strong vehicle production, increasing electric vehicle adoption, and stringent fuel efficiency regulations continue to drive aluminum demand across the country.

Europe Automotive Aluminium Market Trends, Drivers, & Insights

Europe is the most regulatory-driven regional automotive aluminum market, with the EU’s 2035 ICE ban effectively mandating an all-electric passenger car fleet transition that is directly accelerating aluminum adoption across OEM vehicle portfolios. The European market is distinguished by its advanced closed-loop aluminum recycling infrastructure.

The European Aluminium Association reports that 95% of aluminum used in European vehicles is recovered and recycled at end-of-life, delivering significant carbon reduction benefits that align with the EU’s Green Deal objectives and reinforce aluminum’s competitive position versus alternative lightweighting materials in the region’s sustainability-conscious automotive procurement environment.

Germany Automotive Aluminium Market Size

Germany leads the European Automotive Aluminium market with approximately 28% of regional revenue in 2025. The German market is valued at approximately US$ 2.5 Bn in 2026 and is projected to reach approximately US$ 4.4 Bn by 2033, growing at a CAGR of approximately 8.4%. Germany is the leading country in the European automotive aluminum market, accounting for approximately 28% of regional revenue in 2025. Its strong automotive manufacturing base, advanced engineering capabilities, and rapid transition toward electric mobility continue to support robust aluminum demand.

U.K. Automotive Aluminium Market Size

The United Kingdom accounts for approximately 14% of European market revenue in 2026. The UK market is valued at approximately US$ 1.2 Bn in 2026 and is projected to reach approximately US$ 2.2 Bn by 2033, growing at a CAGR of approximately 8.8%. The United Kingdom represents approximately 14% of the European automotive aluminum market revenue in 2026, supported by rising electric vehicle production, lightweight vehicle design initiatives, and investments in sustainable automotive manufacturing.

France Automotive Aluminium Market Size

France represents approximately 12% of the European automotive aluminium market in 2026. The French market is valued at approximately US$ 1.1 Bn in 2026 and is projected to reach approximately US$ 1.9 Bn by 2033, growing at a CAGR of approximately 8.2%. France accounts for approximately 12% of the European automotive aluminum market in 2026, supported by the country's strong automotive manufacturing base, increasing electric vehicle production, and emphasis on lightweight, low-emission vehicle technologies.

Asia Pacific Automotive Aluminium Market Drivers & Analysis

Asia Pacific is both the largest and fastest-growing regional market for Automotive Aluminium, accounting for approximately 38% of global revenue in 2025 and growing at a rate exceeding the global average. The region’s leadership is driven by China’s status as the world’s largest vehicle producer and the dominant global EV market, Japan’s advanced automotive manufacturing ecosystem, and India’s rapidly expanding vehicle production base.

Asia Pacific’s aluminum supply chain advantages are significant: China hosts the world’s largest aluminum smelting capacity, producing approximately 41 million tonnes of primary aluminum in 2023 per International Aluminium Institute (IAI) data, while Japan and South Korea maintain world-class aluminum rolling and die-casting industries serving domestic OEMs.

China Automotive Aluminium Market Size

China is by far the largest national market for automotive aluminium globally, accounting for approximately 45% of Asia Pacific regional revenue in 2026. The Chinese market is valued at approximately US$ 6.1 Bn in 2026 and is projected to reach approximately US$ 10.7 Bn by 2033, growing at a CAGR of approximately 8.3%. The country's leadership is driven by its extensive automotive manufacturing capacity, rapid electric vehicle adoption, and strong government support for lightweight, energy-efficient mobility solutions.

India Automotive Aluminium Market Size

India accounts for approximately 12% of Asia Pacific Automotive Aluminium market revenue in 2025. The Indian market size is valued at approximately US$ 1.6 Bn in 2026 and is projected to reach approximately US$ 2.9 Bn, growing at a CAGR of approximately 8.7% by 2033.

Japan Automotive Aluminium Market Size

Japan accounts for approximately 18% of Asia Pacific Automotive Aluminium market revenue in 2026 and is projected to reach approximately US$ 4.3 billion. Japan is home to some of the world’s most aluminum-intensive vehicle manufacturers: Honda’s NSX sports car and Toyota’s GR86 feature extensively aluminum-intensive architectures, while Toyota’s BEV and hybrid platform strategies increasingly deploy aluminum for battery structures and body panels. Japan accounts for approximately 20% of the Asia Pacific automotive brake valve market revenue in 2026, supported by its advanced automotive manufacturing industry, strong presence of leading OEMs, and continuous innovation in vehicle safety and braking technologies. Increasing adoption of advanced driver assistance systems (ADAS) and high-performance braking solutions is expected to sustain steady market growth.

Competitive Landscape

The automotive aluminium market is moderately consolidated, dominated by a handful of large integrated aluminium producers including Novelis (Hindalco), Constellium SE, Norsk Hydro, and Arconic that combine smelting, rolling, and alloy development capabilities with dedicated automotive supply programs.

Market leaders differentiate through proprietary automotive alloy grades, closed-loop recycling programs that reduce customer carbon footprints, just-in-time delivery capabilities proximate to OEM assembly plants, and co-engineering partnerships with OEMs for next-generation platform development.

Emerging trends include investments in gigacasting-compatible alloy formulations, low-carbon and green aluminum product premiums driven by OEM Scope 3 emission reduction commitments, and strategic geographic expansion into high-growth EV production markets in China and India.

Key Developments:

- In March 2025: Novelis Inc. announced the commercial launch of its Novelis Sustain® automotive aluminum product line featuring a minimum 50% recycled content guarantee, enabling OEM customers to significantly reduce supply chain Scope 3 emissions in line with SBTi-aligned carbon reduction targets.

- In November 2024,Constellium SE secured a long-term supply agreement with a leading European electric vehicle manufacturer for aluminum battery enclosure sheets and structural crash management components for a new BEV platform entering production in 2026, reinforcing its EV-focused portfolio growth strategy.

Companies Covered in Automotive Aluminium Market

- Novelis Inc. (Hindalco Industries)

- Constellium SE

- Arconic Corporation

- Norsk Hydro ASA

- Kaiser Aluminum Corporation

- UACJ Corporation

- Aluminum Corporation of China (Chalco)

- Hammerer Aluminium Industries

- Granges AB

- Kobe Steel Ltd. (Kobelco)

Frequently Asked Questions

The global Automotive Aluminium market is valued at US$ 35.4 billion in 2026 and is projected to reach US$ 62.7 billion by 2033, growing at a CAGR of 8.5%.

The primary growth drivers are tightening global vehicle emission regulations including the EU’s 95 g CO₂/km fleet standard and U.S. CAFE standards mandating fuel economy improvements achievable only through lightweighting and the rapid global expansion of EV production.

Body Structure leads the application segment with approximately 42% market share in 2025. Its dominance reflects widespread adoption of aluminum hoods, door panels, trunk lids, fenders, and crash management structures across premium and increasingly mainstream vehicle platforms globally driven by CO₂ fleet targets and EV platform development.

Asia Pacific is the leading region with approximately 38% of global Automotive Aluminium revenue in 2025. China dominates regional demand with approximately 45% of Asia Pacific market share, producing over 30 million vehicles annually including 9.5 million NEVs in 2023under strict CAFC emission standards that mandate fleet-wide lightweighting.

Leading companies include Novelis Inc., Constellium SE, Arconic Corporation, Norsk Hydro ASA, Kaiser Aluminum Corporation, UACJ Corporation, and Kobe Steel Ltd. serving major global automotive OEMs with a comprehensive range of body, structural, and powertrain aluminum products.