- Automotive Components & Materials

- Automotive Brake Actuation Systems Market

Automotive Brake Actuation Systems Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Brake Actuation Systems Market by Product Type (Disc Brakes, Drum Brakes, Regenerative Braking Modules), Technology (Anti-lock Braking System (ABS), Electronic Stability Control (ESC), Traction Control System (TCS), Electronic Brake-force Distribution (EBD)), Actuation Mechanism (Hydraulic, Pneumatic, Electromagnetic/Brake-by-Wire, Mechanical (Cable)), Component (Brake Pads and Shoes, Calliper’s, Rotors and Drums, Brake Boosters and Master Cylinders, Electronic Control Units and Actuators), and Regional Analysis for 2026 - 2033

Automotive Brake Actuation Systems Market Size and Trend Analysis

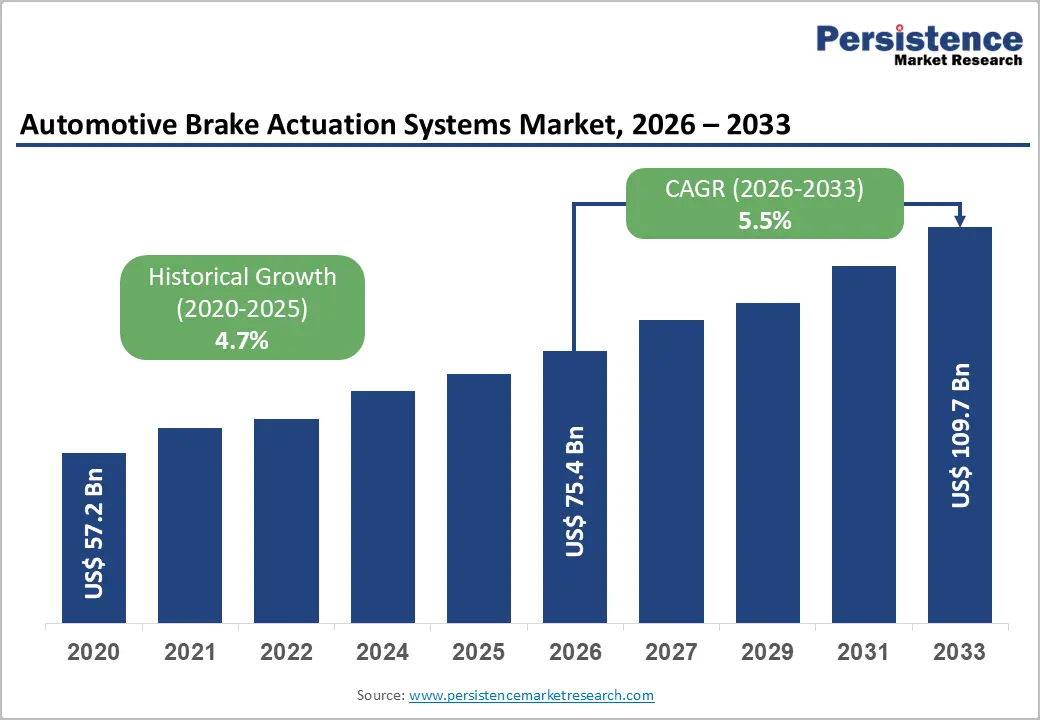

The global automotive brake actuation systems market is valued at US$ 75.4 billion in 2026 and is projected to reach US$ 109.7 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033. This robust trajectory is primarily driven by accelerating global vehicle electrification, the rapid integration of Advanced Driver Assistance Systems (ADAS), and tightening governmental safety mandates requiring anti-lock braking, electronic stability control, and automatic emergency braking across all new vehicle categories.

The global shift toward software-defined vehicle architectures where braking functions are increasingly managed by electronic control units rather than mechanical linkages, is compelling Tier-1 suppliers to invest heavily in brake-by-wire, electro-hydraulic, and regenerative braking modules, fundamentally expanding the per-vehicle content value of actuation systems across all vehicle segments.

Key Highlights

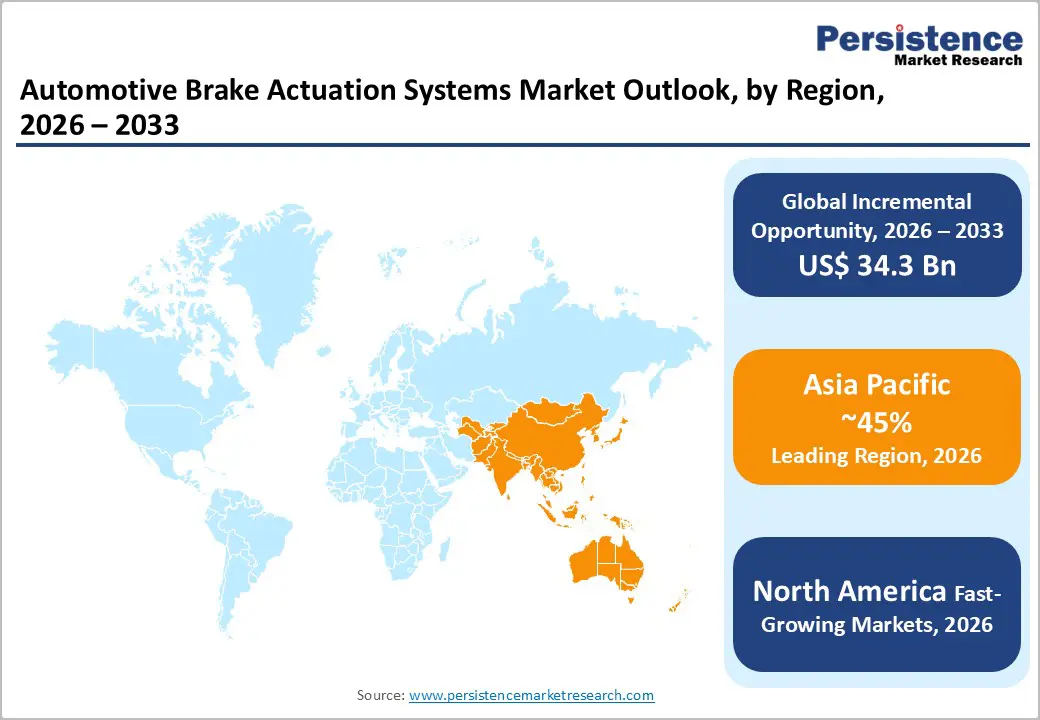

- Leading Region - Asia Pacific dominates global Automotive Brake Actuation Systems demand with over 45% revenue share, led by China's EV manufacturing scale, Japan's Tier-1 supplier ecosystem, and India's rapid ABS mandate expansion and EV adoption growth.

- Fastest Growing Region - North America is the fastest-growing region, driven by accelerating EV fleet electrification from Tesla, Rivian, and GM, rising ADAS content per vehicle, and the early commercial rollout of brake-by-wire systems by Bosch and ZF targeting the region.

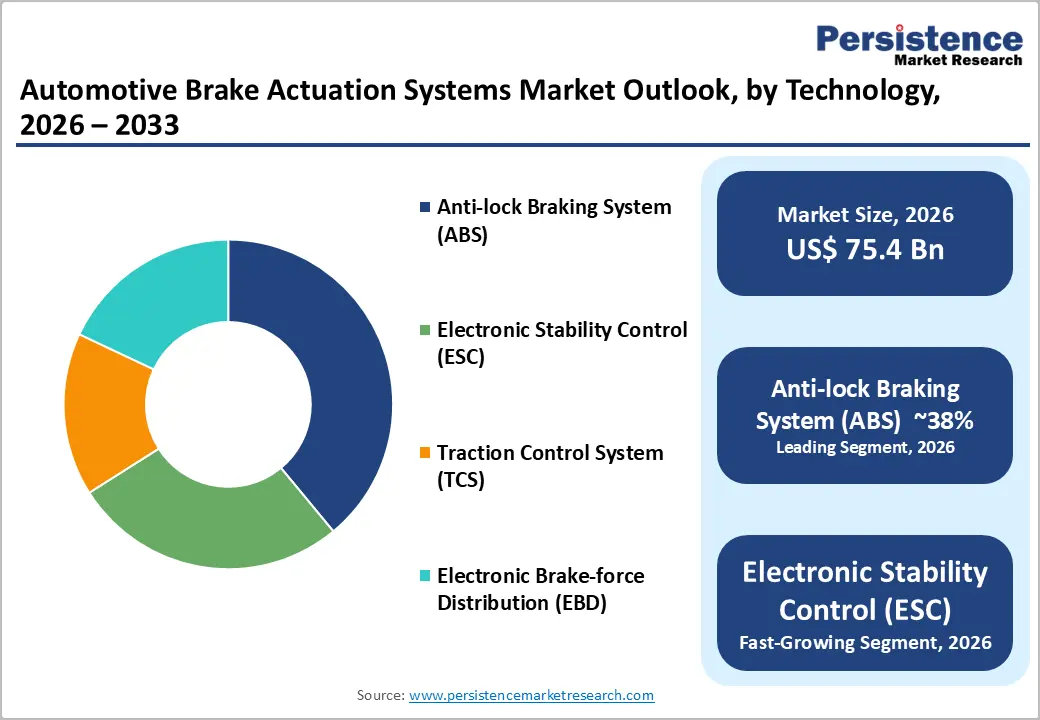

- Dominant Segment - Anti-lock Braking System (ABS) is the dominant technology segment with approximately 38% share, legally mandated across the EU, U.S., Japan, and over 100 nations, and standard in over 90% of new European vehicles in 2024.

- Fastest Growing Segment - The Brake-by-Wire segment is growing at approximately 6.95% CAGR, driven by EV integration, ADAS requirements, and landmark supply contracts by ZF (5 million vehicles) and Bosch's volume production launch in 2025.

- Key Market Opportunity - Euro 7's 7 mg/km brake-dust threshold from mid-2025 is compelling a comprehensive redesign of brake pads, callipers, and disc materials, creating a major material innovation and supply chain opportunity for specialized low-emission brake actuation component manufacturers globally.

| Key Insights | Details |

|---|---|

| Automotive Brake Actuation Systems Market Size (2026E) | US$ 75.4 Bn |

| Market Value Forecast (2033F) | US$ 109.7 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.5% |

| Historical Market Growth (2020 - 2025) | 4.7% CAGR |

DRO Analysis

Drivers - Stringent Global Safety Mandates Accelerating Advanced Braking Adoption

Regulatory requirements are one of the most powerful structural drivers underpinning demand for advanced brake actuation technologies. The European Union made Automatic Emergency Braking (AEB) mandatory for all new vehicle models from May 2022, with compliance extended to all new vehicle registrations by May 2024. The United Nations Economic Commission for Europe (UNECE) further strengthened its AEB provisions for trucks and coaches from February 2023, while Japan mandated AEB for new passenger cars from November 2021, with full fleet compliance required by December 2025.

In the United States, the National Highway Traffic Safety Administration (NHTSA) has found that electronic braking systems can reduce stopping distances by up to 20% compared with conventional systems, providing a strong policy rationale for continued mandates for ABS, ESC, and EBD.

Rapid Electrification of Vehicle Fleets Driving Demand for Regenerative and Brake-by-Wire Systems

The electrification of global automotive fleets is fundamentally restructuring the brake actuation landscape, creating strong incremental demand for regenerative braking modules and brake-by-wire architectures. Electric and hybrid vehicles require sophisticated blended braking systems that coordinate friction brakes with regenerative energy recovery to optimize range and minimize brake wear.

According to the India Brand Equity Foundation (IBEF), more than 50% of three-wheelers and approximately 5% of two-wheelers and 2% of passenger cars sold in India in 2024 were electric, underscoring the breadth of the EV transition even in emerging markets. Robert Bosch GmbH projects that more than 5.5 million vehicles globally will be equipped with brake-by-wire systems by 2030, having already received production orders from multiple OEMs and planning its hydraulic brake-by-wire market launch in fall 2025.

Restraints - High Development Costs and Technical Integration Complexity of Advanced Electronic Systems

The transition from conventional hydraulic brake systems to advanced electronic and brake-by-wire architectures imposes high cost and complexity burdens on vehicle manufacturers and Tier-1 suppliers. Continental AG's brake-by-wire systems reportedly require specialized manufacturing processes that increase production costs by approximately 40% compared to conventional equivalents, while also requiring advanced diagnostic equipment and specially trained technicians for maintenance.

Comprehensive brake system maintenance costs in the U.S. range from US$ 750 to US$ 1,000 per vehicle, while ABS sensor replacement alone runs US$ 150 to US$ 400. These elevated cost structures restrict adoption in price-sensitive developing markets and complicate the business case for fleet operators managing large, heterogeneous vehicle pools.

Cybersecurity Vulnerabilities and System Reliability Risks in Software-Defined Braking

As braking systems become increasingly software-defined and connected, they are exposed to new risks, including cybersecurity vulnerabilities and electronic component failures. In September 2024, BMW issued a major recall affecting over 76,000 vehicles, including 5 Series and 7 Series models, due to faulty welding on brake-by-wire systems supplied by Continental AG.

In January 2025, Chevrolet recalled approximately 3,000 units of the 2025 Equinox EV over an adaptive cruise and braking software defect. These incidents underscore the regulatory and reputational exposure associated with increasingly complex electronic braking architectures, reinforcing OEM caution around rapid deployment timelines.

Opportunities - Brake-by-Wire and Electro-Mechanical Actuation as the Platform for Autonomous Vehicle Integration

Brake-by-wire technology represents the highest-value growth opportunity within the Automotive Brake Actuation Systems market, driven by its essential role in enabling ADAS and autonomous driving functions. Unlike hydraulic systems, brake-by-wire transmits braking intent as a purely electrical signal, eliminating the mechanical pedal-to-system linkage and enabling real-time software-controlled braking profiles, over-the-air updates, and seamless integration with autonomous emergency braking algorithms.

ZF Friedrichshafen AG secured brake-by-wire contracts covering nearly 5 million light vehicles in January 2025 and presented its "Chassis 2.0" holistic by-wire chassis concept at IAA Mobility 2025. Brembo's Sensify smart braking system, developed in partnership with Michelin and scheduled for production in 2026, uses real-time data and electric actuation to optimize braking at each wheel.

Euro 7 Compliance and Low-Emission Braking: Creating New Material and Design Opportunity

The European Union's Euro 7 emission regulation, with its 7 mg/km brake-dust threshold effective from mid-2025, is compelling a comprehensive redesign of brake pad formulations, caliper geometries, and disc materials across the European supply chain. This regulatory shift creates a significant material and engineering opportunity for suppliers capable of delivering copper-free, low-emission brake solutions and lightweight caliper designs.

General Motors' ACDelco Gold pads have already adopted copper-free formulas to comply with 2025 U.S. particulate limits, demonstrating that this regulatory transition is global in scope. In April 2025, Federal-Mogul Motor Parts (Tenneco) marked 30 years of operations in China by opening a GTR-compliant brake-emissions lab and launching a new low-emission brake system aligned with Euro 7 targets, signaling that the regulatory transition is driving tangible product-investment on the product roadmap among market participants globally.

Category-wise Analysis

Product Type Insights

Among the three principal product types, Disc Brakes, Drum Brakes, and Regenerative Braking Modules Disc Brakes hold the dominant position in the Automotive Brake Actuation Systems market, accounting for approximately 60% of market revenue. Disc brakes are the standard specification for front-axle applications globally, with adoption rapidly expanding to rear axles as safety mandates tighten. In 2025, disc brake systems were confirmed as standard in front-axle applications across virtually all new passenger vehicle programs, with growing rear-axle adoption driven by ABS and ESC integration.

Their thermal management advantages, shorter stopping distances, and compatibility with regenerative braking systems in electric vehicles make disc brakes the preferred actuation format for both passenger cars and commercial vehicles.

Technology Insights

Among the four technology categories ABS, ESC, TCS, and EBD Anti-lock Braking System (ABS) is the dominant technology segment, holding approximately 38% share of the technology landscape. ABS has achieved near-universal penetration in developed markets following legislative mandates from the EU, U.S., Japan, and numerous emerging economies. In Europe, over 90% of new vehicles were equipped with ABS in 2024, reflecting the technology's status as a foundational safety standard.

ABS is typically bundled with Electronic Brake-force Distribution (EBD) and Traction Control Systems (TCS), reinforcing its position as the anchor of the broader electronic safety suite. However, Electronic Stability Control (ESC) is the fastest-growing technology sub-segment, as mandates for ESC expand into emerging markets and its life-saving potential in preventing rollover accidents gains wider regulatory recognition globally.

Actuation Mechanism Insights

The Hydraulic actuation mechanism is the dominant segment in the Actuation Mechanism category, accounting for approximately 55% of the Automotive Brake Actuation Systems market. Hydraulic systems have been the industry standard for decades owing to their high force transmission efficiency, reliability across extreme operating temperatures, and established supply chain depth.

Modernized hydraulic architectures, such as ZF Friedrichshafen AG's Integrated Brake Control (IBC) platform announced in May 2024, combine hydraulic actuation with digital ESC, ABS, and regenerative coordination in a compact, OTA-updatable module, demonstrating that hydraulic systems are evolving rather than being entirely replaced. However, the Electromagnetic / Brake-by-Wire segment is growing at the fastest rate within this category, as EV platform requirements, ADAS integration needs, and autonomous driving readiness create compelling technical and commercial arguments for fully electronic actuation.

Component Insights

Among the five defined component categories, Brake Pads and Shoes represent the leading segment, accounting for approximately 32% of market revenue in 2024, driven by their essential consumable nature and high-frequency replacement cycles across the global fleet of over 1.5 billion motor vehicles on the road. The segment's aftermarket volume is structural and recurring, providing a stable revenue base even during vehicle production downturns.

Akebono Brake Industry Co., Ltd. launched a new EURO and Severe Duty Ultra-Premium Disc Brake Pad product line in October 2024, reinforcing active product investment in this segment. Meanwhile, the Electronic Control Units and Actuators sub-segment is the fastest-growing within components, climbing at a CAGR of approximately 10.3% as vehicle value migrates toward software-centric braking modules, with Renesas' 3-nm R-Car X5H processor specifically dedicating hardware isolation for brake-by-wire safety domains.

Regional Insights

Asia Pacific Automotive Brake Actuation Systems Market Share

Asia Pacific is the dominant manufacturing and consumption region in the global Automotive Brake Actuation Systems market, accounting for over 45% of global revenue. China drives this position through its world-leading EV production volumes and an extensive domestic automotive manufacturing base, while Japan's engineering ecosystem anchored by Aisin Corporation, ADVICS Co. Ltd., Akebono Brake Industry, and Hitachi Astemo supplies precision braking components globally. Continental AG alone produced more than 1 million electronic brake systems in India during 2024, with local joint ventures such as Brakes India-ADVICS reinforcing indigenous technology capability.

India's rapidly expanding automotive sector with EV penetration rising across all vehicle categories and government-mandated ABS adoption for two-wheelers driving structural demand makes it an increasingly important growth market. ASEAN nations including Thailand, Indonesia, and Vietnam are building automotive assembly capacity with evolving brake safety standards tracking global norms. China's "Made in China 2025" initiative continues to incentivize domestic production of advanced brake-by-wire and electronic actuation components, reducing reliance on imports.

North America Automotive Brake Actuation Systems Market Share

North America is a technology leadership hub in the global Automotive Brake Actuation Systems market, with the United States commanding approximately 85% of regional revenue in 2024. The U.S. market benefits from a large vehicle fleet, robust regulatory frameworks enforced by the National Highway Traffic Safety Administration (NHTSA), and a strong OEM innovation ecosystem.

In April 2024, General Motors rolled out enhanced regenerative braking systems across its Ultium-based electric SUVs, integrating one-pedal driving and upgraded ABS tuning. ZF Friedrichshafen AG also announced development of a modular Integrated Brake Control (IBC) platform for EVs and SUVs in May 2024, targeting scalable architectures with OTA update support.

Europe Automotive Brake Actuation Systems Market Share

Europe is a highly regulated and technologically mature market for Automotive Brake Actuation Systems. Over 90% of new vehicles registered in Europe were equipped with ABS in 2024, reflecting the region's comprehensive safety legislation. Germany is the market's industrial engine, housing the global headquarters of Robert Bosch GmbH, Continental AG, and ZF Friedrichshafen AG, collectively setting R&D direction for the global brake systems industry. The Euro 7 brake-dust threshold of 7 mg/km, effective mid-2025, is fundamentally accelerating material innovation across the European supply chain, requiring copper-free pad formulations and low-drag caliper designs.

The U.K., France, and Spain represent significant demand centers, with European OEMs transitioning mainstream models to four-wheel disc configurations. Regulatory harmonization under UNECE regulations and EU General Safety Regulation 2019/2144 continues to drive standardization of ESC, AEB, and EBD across all new vehicle types.

Competitive Landscape

The global Automotive Brake Actuation Systems market exhibits a moderately concentrated structure, with the top five suppliers Continental AG, Robert Bosch GmbH, ZF Friedrichshafen AG, Brembo S.p.A, and Aisin Corporation collectively controlling a substantial portion of global revenue. Technology leadership, rather than scale alone, increasingly dictates competitive positioning, as the industry pivots from commoditized hydraulic components toward software-centric brake-by-wire and electro-hydraulic platforms.

Key differentiators include proprietary ECU architectures, OEM co-development partnerships, OTA software update capabilities, and patent portfolios spanning over 3,366 filings for Brembo alone.

Key Market Developments

- In April 2025, Nexteer Automotive launched an electro-mechanical brake-by-wire system designed for modular, software-defined chassis integration.

- In March 2025, Brembo unveiled an electro-mechanical caliper, targeting series production in 2026.

- In January 2025, ZF agreed on a high-volume brake-by-wire supply for a North American model line, pairing electro-mechanical rear brakes with integrated front hydraulics.

Companies Covered in Automotive Brake Actuation Systems Market

- Continental AG

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Brembo S.p.A

- Akebono Brake Industry Co. Ltd

- Aisin Corporation

- ADVICS Co. Ltd

- Knorr-Bremse AG

- Hyundai Mobis Co. Ltd

- Mando Corporation

- Federal-Mogul Motorparts (Tenneco)

- Hitachi Astemo, Ltd.

Frequently Asked Questions

The global Automotive Brake Actuation Systems market is valued at US$ 75.4 Bn in 2026 and is projected to reach US$ 109.7 Bn by 2033, growing at a CAGR of 5.5% over the forecast period.

The key demand drivers are the global expansion of mandatory AEB, ABS, and ESC regulations across major automotive markets (EU, U.S., Japan), rapid vehicle electrification creating demand for regenerative braking and brake-by-wire systems, and the growing integration of braking with ADAS platforms.

The Anti-lock Braking System (ABS) segment leads the technology category with approximately 38% market share, legally mandated across over 100 countries and installed in over 90% of new European vehicles in 2024. It serves as the foundational platform on which ESC, TCS, and EBD functions are layered, making it the anchor technology in all modern electronic braking architectures.

Asia Pacific dominates the global Automotive Brake Actuation Systems market, accounting for over 45% of revenue, driven by China's massive EV production volumes, Japan's advanced braking supplier ecosystem, and India's rapidly expanding vehicle base with rising safety content. Continental AG produced over 1 million electronic brake systems in India alone during 2024, illustrating the region's manufacturing depth.

The leading companies include Robert Bosch GmbH, ZF Friedrichshafen AG, Continental AG, Brembo S.p.A., Aisin Corporation, Knorr-Bremse AG, Akebono Brake Industry Co. Ltd., ADVICS Co. Ltd., Hyundai Mobis Co. Ltd., Mando Corporation, Federal-Mogul Motor parts (Tenneco), and Hitachi Astemo, Ltd.