- Automotive Components & Materials

- Automotive Drum Brake Market

Automotive Drum Brake Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Drum Brake Market by Product Type (Leading Trailing Shoe Brake, Others), Braking Type (Normal Braking, Automatic Self-adjustment, Emergency Braking), Application (Passenger Vehicles, Commercial Vehicles), and Regional Analysis for 2026 – 2033

Automotive Drum Brake Market Size and Trends Analysis

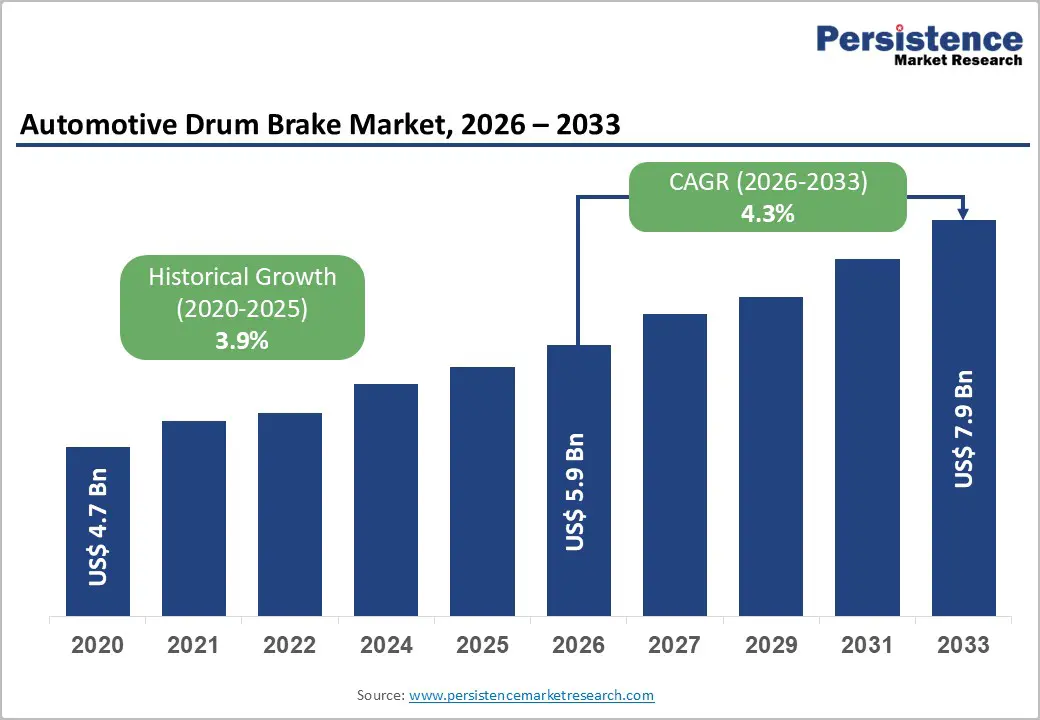

The global automotive drum brake market size is likely to be valued at US$5.9 billion in 2026, and is expected to reach US$7.9 billion by 2033, growing at a CAGR of 4.3% during the forecast period from 2026 to 2033, driven by the increasing prevalence of cost-effective braking systems in emerging economies, rising demand for reliable solutions in commercial vehicles, and advancements in self-adjusting drum brake technologies. The rising demand for durable, low-maintenance automotive drum brakes, particularly in passenger and commercial vehicles, is driving greater adoption across various applications. Innovations in leading trailing shoe brake and servo brake designs are enhancing performance and lifespan, further fueling market growth. The growing recognition of automotive drum brakes as essential for budget vehicles and heavy-duty applications is a key factor in the market's expansion.

Key Industry Highlights:

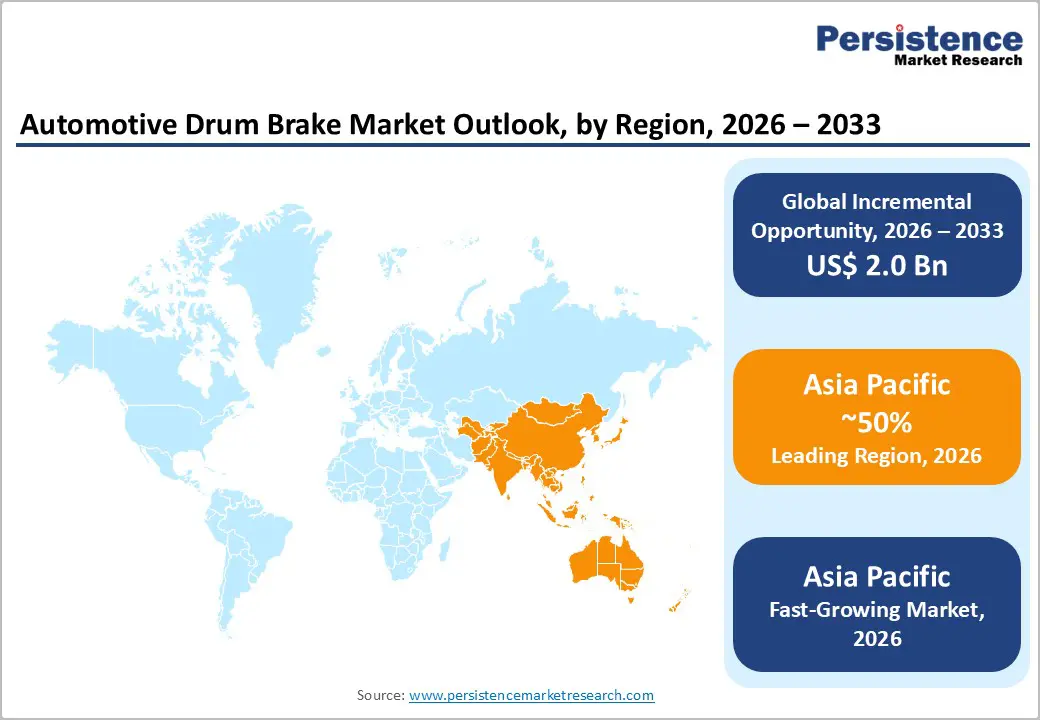

- Leading Region: Asia Pacific, anticipated to account for a 50% market share in 2026, driven by high vehicle production, cost-sensitive markets, and strong demand in India and China.

- Fastest-growing Region: Asia Pacific, fueled by expanding commercial fleet, rising urbanization, and growing investments in affordable braking systems.

- Dominant Product Type: Leading trailing shoe brake, to hold approximately 55% of the revenue share, as it provides simple, effective braking for rear wheels.

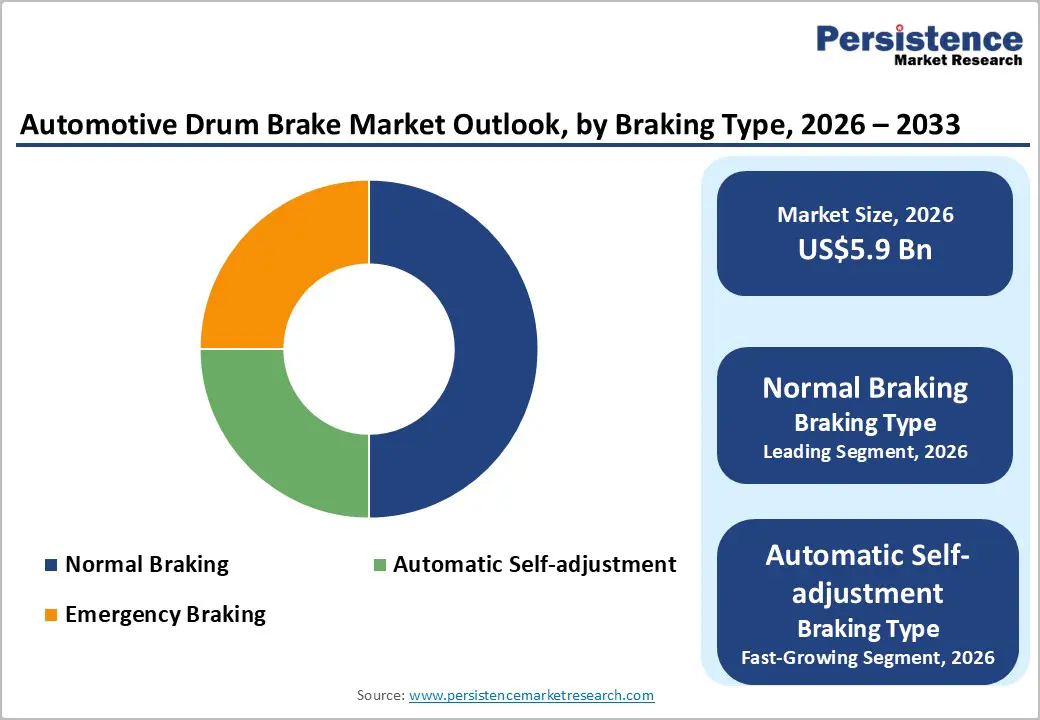

- Leading Braking Type: Normal braking accounts for over 60% of the market revenue, due to standard use in everyday driving.

- Leading Application: Commercial vehicles, contributing nearly 55% of the market revenue, due to their durability in heavy loads.

| Key Insights | Details |

|---|---|

| Automotive Drum Brake Market Size (2026E) | US$5.9 Bn |

| Market Value Forecast (2033F) | US$7.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Cost-Effective Braking Systems in Emerging Economies

The rising demand for cost-effective braking systems in emerging economies is being driven by rapid growth in vehicle ownership, expanding urban populations, and increasing investment in transportation infrastructure. As passenger cars, two-wheelers, and commercial vehicles become more accessible to middle-income consumers, manufacturers are under pressure to offer reliable braking solutions that balance safety, durability, and affordability. Price sensitivity remains high in these markets, encouraging the adoption of braking systems that meet regulatory safety standards while minimizing production and maintenance costs.

Local manufacturing and sourcing of components have played a key role in reducing overall system costs. OEMs and suppliers are increasingly optimizing designs, simplifying system architectures, and using regionally available materials to deliver competitively priced braking solutions. The strong presence of small and medium-scale vehicle manufacturers has accelerated the demand for standardized, easy-to-integrate braking systems that can be deployed across multiple vehicle platforms. The growing aftermarket sector further supports this trend, as fleet operators and individual vehicle owners seek replacement parts that offer consistent performance at lower lifecycle costs.

High Development and Material Costs

High development and material costs present a significant barrier for companies advancing next-generation automotive drum brakes and novel systems. Developing innovative grades, such as automatic self-adjustment, high-heat servo, or lightweight leading and trailing shoes, requires extensive research, specialized friction materials, and advanced casting technologies that are far more expensive than basic designs. Durability is an even greater challenge: many refined variants, heat-resistant lots, and low-noise products are sensitive to wear, fade, and vibration, requiring rigorous optimization to ensure they remain reliable throughout the lifecycle. Achieving long-term performance often involves costly dynamometer trials, sophisticated testing, and the use of high-grade linings, which significantly increase research and development (R&D) expenditures.

Meeting stringent regulatory expectations for stopping distance, noise levels, and batch consistency requires multiple validation studies under various conditions and across several vehicle types. This adds both time and financial burden to development timelines. Scaling up manufacturing requires controlled foundries, specialized assembly lines, and quality-assurance systems, further driving up overall costs. For smaller manufacturers, these challenges can limit innovation or delay commercialization.

Developments in Self-Adjusting and Lightweight Delivery Platforms

Developments in self-adjusting and lightweight automotive drum brake delivery platforms are transforming the global braking landscape by addressing two major challenges, maintenance barriers and weight reduction. Self-adjusting platforms are engineered to achieve automatic clearance, reducing reliance on manual service and enabling longer intervals in commercial vehicles. Innovations, such as ratchet mechanisms, sensor-based controls, hydraulic integration, and wear indicators, significantly improve safety and reduce downtime, lowering operational costs for fleets and consumer campaigns.

Progress in lightweight platforms, such as aluminum drums, composite linings, thin-wall casting, and modular designs, enables more fuel-efficient braking by minimizing unsprung mass, the system’s first line of defense against efficiency loss. These formats eliminate heavy steel, enhance heat dissipation, and allow versatile use without performance trade-offs, making them highly suitable for mass passenger programs. New technologies such as ceramic coatings, bio-adhesive linings, and VLP-based monitoring further enhance durability and response.

Category-wise Analysis

Product Type Insights

The leading trailing shoe brake is expected to dominate the market, accounting for approximately 55% of the revenue share by 2026. Its dominance is driven by simplicity, cost-effectiveness, and reliability, making it preferred for rear-wheel applications. Leading trailing shoe brake provides effective stopping, ensures affordability, and contributes to volume, making it suitable for large-scale vehicle campaigns. Akebono Brake Industry Co., Ltd., a major global brake component supplier, produces leading/trailing shoe-type drum brakes that are widely used by major original equipment manufacturers (OEMs) on the rear axles of passenger cars and light commercial vehicles. These leading/trailing shoe drum brakes are favored in rear-wheel setups as they combine cost-effectiveness, simplicity, and reliable braking performance, exactly the qualities that help OEMs reduce manufacturing costs while meeting safety requirements.

The servo brake represents the fastest-growing segment, due to its amplified force and expanding use in heavy-duty vehicles. Its self-energizing profile makes it ideal for targeted power, reducing pedal effort. Continuous innovations in design are further strengthening its appeal, driving rapid adoption across Asia Pacific and Europe, where demand for commercial braking is accelerating. ZF Wabco (now ZF Commercial Vehicle Solutions), a leading global supplier of braking systems for heavy commercial vehicles such as trucks, buses, and trailers, integrates servo-assisted braking and advanced brake boosters into its platform of servo/Duo-servo drum brakes and brake boosters that amplify pedal force to deliver stronger stopping power with less driver effort.

Braking Type Insights

Normal braking leads, holding approximately 60% of the revenue share in 2026, driven by standard daily use, large volume programs, and strong global demand for basic functionality. Their dominance continues as vehicles expand everyday driving. Rising adoption of automatic self-adjustment and expanded emergency campaigns highlight the growing focus on enhanced safety. For example, companies such as ZF Friedrichshafen AG supply normal braking systems for large-scale cars, stabilizing performance and supporting operational strategies across multiple regions.

Automatic self-adjustment is the fastest-growing segment, due to a strong momentum in low-maintenance and expanding inclusion in modern vehicles. The growing shift toward convenience platforms, along with better longevity, accelerates the adoption. Advancements in mechanisms and the continued progress of sensor integration entering production trials drive market growth. Robert Bosch GmbH, one of the world’s leading automotive technology suppliers, has been a major driver of automatic emergency braking (AEB) systems and sensor-integrated brake control technologies that automatically adjust braking in response to real-time sensor input. Bosch integrates radar, camera, and sensor fusion systems into its AEB solutions, which are then supplied to major vehicle manufacturers around the world.

Application Insights

Commercial vehicles are projected to account for nearly 55% of revenue in 2026, as they continue to serve as the primary sector for heavy-duty braking, large fleet operations, and the management of load-bearing vehicles that demand robust systems. Their strong integration, trained operators, and ability to handle high-volume or demanding blends drive higher consumption. Commercial sectors are leading servo rollouts as well as administering emerging self-adjustment trials. Robert Bosch GmbH, a major global supplier of commercial vehicle braking systems, offers an Advanced Emergency Braking (AEB) system specifically for heavy commercial vehicles. Bosch’s solution uses radar and camera sensors to detect critical proximity to vehicles or obstacles ahead, automatically preparing and applying the brakes to mitigate collisions without driver intervention.

Passenger vehicles represent the fastest-growing segment, driven by their strong economic presence and expanding role in budget cars. They offer convenient, quick, and accessible stopping, attracting buyers who prefer affordable, low-maintenance settings. Increased outreach programs, emerging market focus, and wider availability of routine and premium brakes further accelerate uptake, boosting rapid adoption across both urban and semi-urban areas. Ford Motor Company has expanded its Co-Pilot360 suite of driver-assist technologies, including Pre-Collision Assist with Automatic Emergency Braking (AEB), across a wide range of passenger vehicle models, not just premium cars. This reflects a broader industry push to install advanced braking and safety systems as standard or widely available options even in budget-friendly vehicles, making enhanced braking more accessible to everyday drivers.

Regional Insights

North America Automotive Drum Brake Market Trends

North America's growth is propelled by the region’s established commercial fleet infrastructure, strong research and development capabilities, and high public awareness of cost benefits. Manufacturing systems in the U.S. and Canada provide extensive support for braking programs, ensuring wide accessibility of automotive drum brakes across commercial vehicles and passenger populations. Increasing demand for durable, convenient, and easy-to-maintain forms is further accelerating adoption, as these formats improve reliability and reduce barriers associated with premium systems.

Innovation in automotive drum brake technology, including stable self-adjustment, improved servo delivery, and targeted lightweight enhancement, is attracting significant investment from both public and private sectors. Government initiatives and fleet campaigns continue to promote use against high costs, maintenance issues, and emerging efficiency threats, creating sustained market demand. The growing focus on commercial grades and specialty uses, particularly for trucks and others, is expanding the target applications for automotive drum brakes.

Europe Automotive Drum Brake Market Trends

Europe shows significant growth by increasing awareness of cost benefits, strong commercial systems, and government-led efficiency programs. Countries such as Germany, France, and the U.K. have well-established vehicle frameworks that support routine braking and encourage the adoption of innovative drum delivery methods, including automotive drum brakes. These reliable formulations are particularly appealing for commercial populations, cost-conscious operators, and fleet users, improving longevity and coverage rates.

Technological advancements in automotive drum brake development, such as enhanced self-adjustment, application-targeted delivery, and improved low-noise grades, are further boosting market potential. European authorities are increasingly supporting research and trials for brakes against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, low-maintenance options is aligned with the region’s focus on preventive fleet management and reducing downtime. Public awareness campaigns and transition drives are expanding reach in both urban and rural areas, while suppliers are investing in materials and novel variants to increase efficacy.

Asia Pacific Automotive Drum Brake Market Trends

Asia Pacific is expected to be the leading and fastest-growing, holding approximately 50% market share, supported by rising vehicle production, increasing government initiatives, and expanding application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting brake campaigns to address commercial growth and growing demand for passenger vehicles. Automotive drum brakes are attractive in these regions due to their cost-effectiveness, scalability, and suitability for both urban and rural vehicle fleets.

Technological advancements are supporting the development of stable, effective, and easy-to-maintain automotive drum brakes, which can withstand challenging road conditions and minimize wear dependence. These innovations are critical for reaching remote facilities and improving overall safety coverage. Growing demand for commercial vehicles, passenger cars, and applications is contributing to market expansion. Public-private partnerships, increased auto expenditure, and rising investments in local manufacturing capacity are further accelerating growth. The convenience of drum brake delivery, combined with improved durability and reduced risk of failure, positions automotive drum brakes as a preferred choice.

Competitive Landscape

The global automotive drum brake market features competition between established brake leaders and emerging regional suppliers. In North America and Europe, Continental AG and ZF Friedrichshafen AG lead through strong R&D, distribution networks, and OEM ties, bolstered by innovative grades and performance programs. In Asia Pacific, Aisin Seiki Co., Ltd. advances with localized solutions, enhancing accessibility. Self-adjusting delivery boosts reliability, cuts maintenance risks, and enables mass integrations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Lightweight formulations solve weight issues, aiding penetration in efficiency-focused areas.

Key Industry Developments

- In June 2024, Bendix introduced a new range of brake drums, expanding its product line to include utility vehicles and light passenger cars for the Australian market. This new addition was intended to fill a niche in the company’s parts catalog and was designed to ensure high performance and reliability.

Frequently Asked Questions

The global automotive drum brake market is projected to reach US$5.9 billion in 2026.

The rising prevalence of cost-effective braking systems in emerging economies and the demand for reliable solutions are key drivers.

The automotive drum brake market is poised to witness a CAGR of 4.3% from 2026 to 2033.

Advancements in self-adjusting and lightweight delivery platforms are the key opportunities.

Continental AG, ZF Friedrichshafen AG, Akebono Brake Industry Co., Ltd., Aisin Seiki Co., Ltd., and Bosch Limited are the key players.