- Technology

- Audio Codec Market

Audio Codec Market Size, Share, and Growth Forecast, 2026 - 2033

Audio Codec Market by Product Type (Lossy Codecs, Lossless Codecs, Others), Component (Hardware Codecs, Software Codecs, Others), Application, and Regional Analysis for 2026 - 2033

Audio Codec Market Size and Trends Analysis

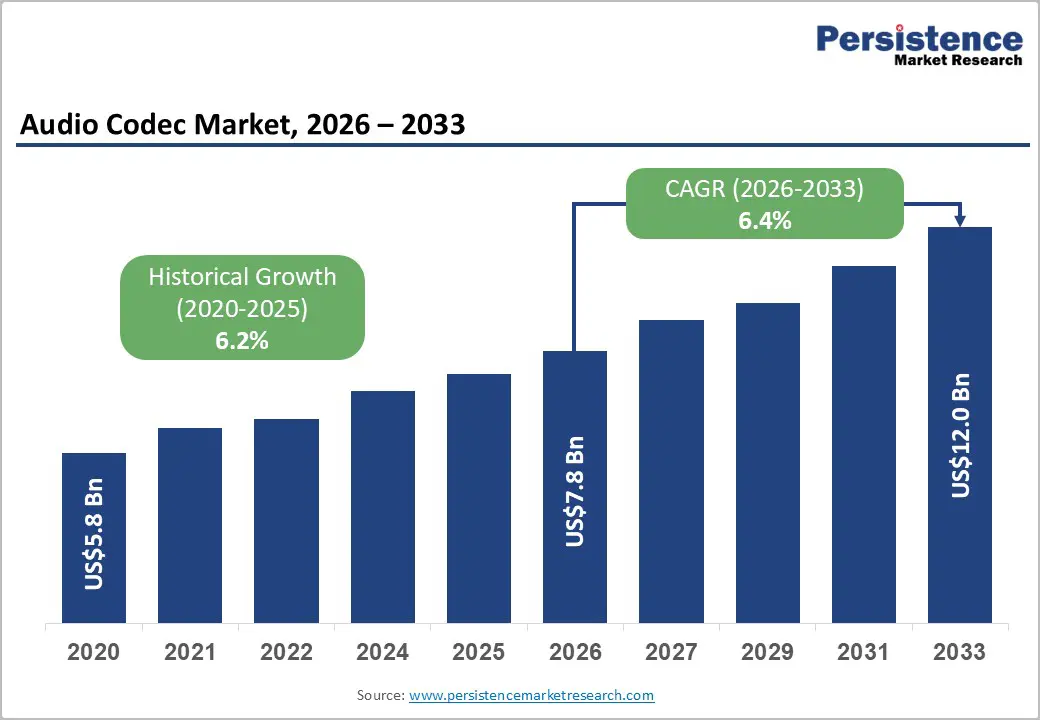

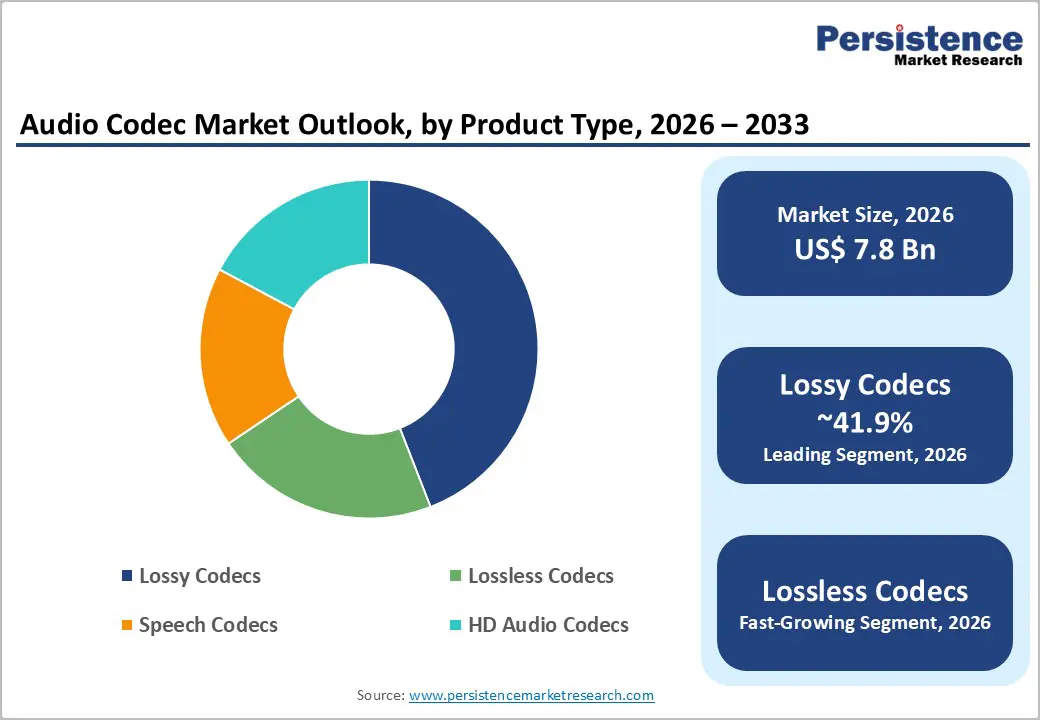

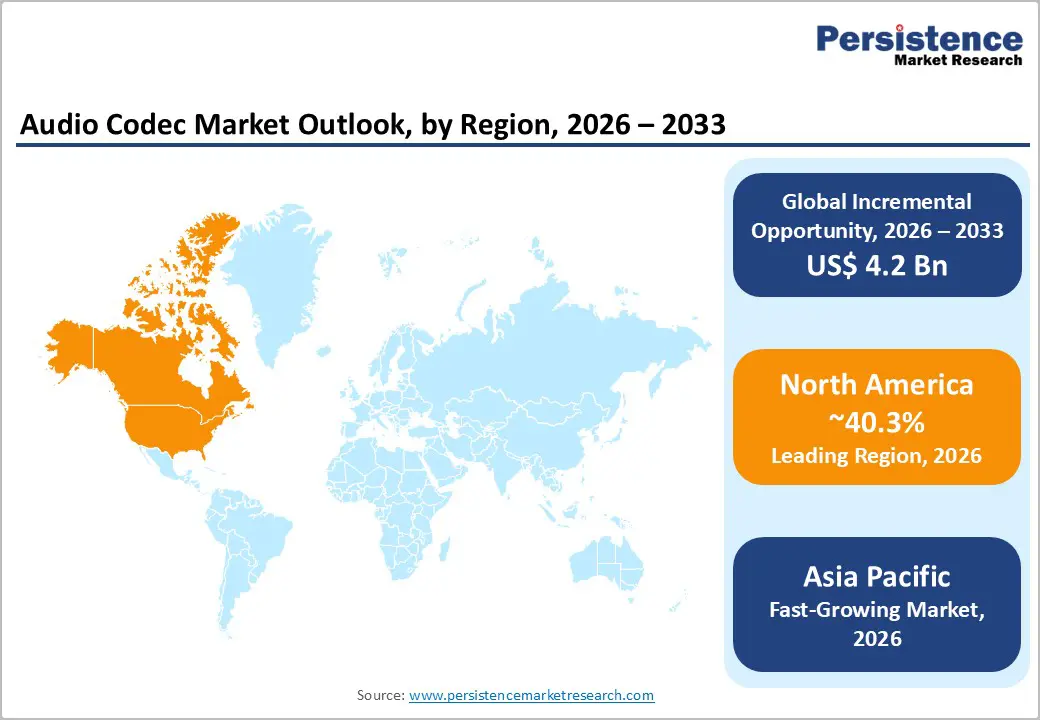

The global audio codec market size is likely to be valued at US$7.8 billion in 2026 and is expected to reach US$12.0 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033, driven by increasing adoption of 5G-enabled devices, the proliferation of wireless audio ecosystems, and advancements in low-power and high-efficiency codec technologies.

Growth is further supported by rising demand for high-resolution streaming, immersive voice communication, and integration of audio solutions across automotive and smart consumer devices. The industry is transitioning from a hardware-centric model focused on smartphones to a broader, software-defined ecosystem spanning connected vehicles, wearables, streaming platforms, and telecommunications infrastructure. Standardization efforts and technological convergence are accelerating adoption while enabling scalable, high-quality audio delivery across diverse applications.

Key Industry Highlights:

- Leading Region: North America is projected to account for approximately 40.3% of the market share, driven by strong adoption of advanced audio technologies, high 5G penetration, and the presence of leading semiconductor and audio technology companies.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, supported by rapid smartphone adoption, expanding 5G infrastructure, and strong manufacturing capabilities across China, India, and Southeast Asia.

- Investment Plans: Industry investments are increasingly focused on software-defined audio, low-power wireless technologies, and automotive infotainment systems, with a significant portion of R&D budgets allocated toward Bluetooth LE Audio, immersive codecs, and AI-driven audio enhancements.

- Dominant Product Type: Lossy Codecs dominate, anticipated to account for approximately 41.9% of the market share, driven by their widespread use in streaming, telecommunications, and consumer electronics due to efficient compression and low bandwidth requirements.

- Dominant Component: Hardware codecs dominate, with an anticipated market share of 59.5%, owing to their critical role in delivering low-latency, power-efficient audio processing in embedded and consumer devices.

| Key Insights | Details |

|---|---|

| Audio Codec Market Size (2026E) | US$7.8 Bn |

| Market Value Forecast (2033F) | US$12.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.2% |

DRO Analysis

Driver Analysis - Rising Connectivity Density and Streaming Consumption

The rapid expansion of global internet penetration and mobile connectivity is a primary driver of the audio codec market. With billions of users accessing digital platforms and a growing share of the global population connected via high-speed networks, demand for efficient audio compression technologies continues to rise. Audio codecs are embedded in nearly every digital interaction, including streaming services, voice calls, and messaging applications. As network bandwidth improves and user expectations increase, there is a shift toward higher-quality audio formats with reduced latency and improved clarity. This trend drives both volume growth in codec deployment and increased value per implementation, particularly in premium devices and services.

Bluetooth LE Audio and Low-Power Wireless Adoption

The introduction of Bluetooth LE Audio has significantly reshaped the wireless audio landscape. The LC3 codec enables superior sound quality at lower bit rates while reducing power consumption, making it ideal for battery-operated devices such as earbuds, wearables, and hearing aids. This advancement supports longer battery life and smaller device form factors without compromising performance. Multi-stream audio capabilities and broadcast audio features further enhance user experience and expand application scenarios. As wireless audio devices become more ubiquitous, the demand for efficient, low-power codec solutions is expected to grow substantially, reinforcing this segment’s importance in the overall market.

Expansion of Immersive Audio in Telecommunications and Automotive

Audio codecs are increasingly integral to next-generation communication systems and in-vehicle infotainment platforms. The emergence of immersive voice technologies and advanced speech codecs is transforming traditional telephony into high-definition, spatial communication experiences. In parallel, the automotive industry is integrating sophisticated audio systems to enhance in-cabin entertainment and connectivity. Automakers are adopting advanced codec technologies to support streaming services, voice assistants, and personalized audio environments. This convergence of communication and entertainment use cases is creating new revenue streams and accelerating innovation in codec design and deployment.

Restraint Analysis - Codec Fragmentation and Licensing Complexity

The coexistence of multiple codec standards, including proprietary and open-source formats, presents a significant challenge for market participants. Each codec is associated with distinct licensing requirements, intellectual property constraints, and compatibility considerations. This fragmentation increases integration complexity for device manufacturers and software developers, particularly when products must operate across multiple platforms and ecosystems. Licensing costs and compliance requirements can also impact profit margins and delay time-to-market, limiting adoption in cost-sensitive segments.

Power, Latency, and Cost Constraints

Despite technological advancements, audio codec implementation remains constrained by the need to balance performance with power efficiency and cost. Device manufacturers must optimize audio quality while minimizing energy consumption and hardware footprint, particularly in portable and wearable devices. These trade-offs can restrict the adoption of advanced codecs in mid-range and entry-level products. Additionally, maintaining low latency for real-time applications such as gaming and voice communication adds further complexity to codec design, potentially slowing innovation in certain segments.

Opportunity Analysis - Growth of Connected Vehicles and In-Cabin Audio Systems

The automotive sector represents a major growth opportunity for audio codec vendors as vehicles increasingly transform into connected, software-defined digital environments. Demand for high-quality audio systems is rising alongside the integration of infotainment, voice assistants, and real-time streaming services within vehicles. Advanced codecs play a critical role in enabling immersive surround sound, low-latency voice interaction, and efficient bandwidth utilization, ensuring seamless audio experiences even in variable network conditions. Automakers are investing heavily in differentiated infotainment ecosystems, including multi-speaker spatial audio systems and personalized in-cabin sound zones. This trend is encouraging collaborations between OEMs and technology providers, creating opportunities for codec vendors to expand through strategic partnerships, embedded solutions, and long-term licensing models, particularly in electric and autonomous vehicle platforms.

Expansion of Accessibility and Assistive Audio Technologies

The development of assistive listening technologies and accessibility-focused audio solutions is unlocking new growth avenues for the audio codec market. Modern codec standards now support advanced capabilities such as broadcast audio, real-time audio sharing, and enhanced compatibility with hearing aids and assistive devices, enabling broader deployment across public infrastructure. These solutions are increasingly being implemented in airports, public transport systems, educational institutions, and healthcare facilities, where clear and inclusive audio communication is essential. Regulatory emphasis on accessibility and inclusivity is driving long-term investments in this segment, ensuring sustained demand. Companies that innovate in low-power, high-clarity codecs tailored for assistive applications can benefit from stable revenue streams and strong institutional adoption, while also contributing to improved user experiences for individuals with hearing impairments.

Emerging Market Adoption and 5G-Driven Services

Rapid smartphone adoption and 5G network expansion in emerging economies are creating significant growth opportunities for audio codecs. As consumers upgrade to advanced devices and access richer digital services, demand for high-quality audio experiences increases. Enhanced messaging platforms, streaming services, and immersive communication applications are driving codec adoption in these regions. The combination of large user bases, improving infrastructure, and rising disposable incomes positions emerging markets as a key growth engine for the industry.

Category-wise Analysis

Product Type Insights

Lossy codecs are expected to dominate the market, accounting for an anticipated 41.9% share in 2026. Their leadership is driven by widespread use in streaming, telecommunications, and consumer electronics, where efficient data compression is essential. These codecs significantly reduce bandwidth and storage requirements while maintaining acceptable audio quality, making them highly suitable for mass-market applications. Formats such as MP3, AAC, and Opus are commonly deployed across platforms such as music streaming services, video platforms, and VoIP applications. Smartphones, wireless earbuds, and streaming ecosystems rely heavily on lossy codecs to deliver scalable and cost-effective audio solutions, particularly in bandwidth-constrained environments. Their ability to balance performance, latency, and efficiency ensures continued dominance in high-volume deployments.

Lossless codecs are likely to represent the fastest-growing segment, driven by the rising demand for high-resolution audio and premium listening experiences. As network infrastructure improves and data costs decline, consumers are increasingly opting for higher-fidelity formats such as FLAC, ALAC, and WAV, especially in premium streaming tiers and professional audio production. Gaming platforms and studio environments also leverage lossless codecs for accurate sound reproduction and immersive experiences. Growth is further supported by advancements in compression efficiency and increasing availability of high-quality audio hardware. Speech codecs and HD audio codecs benefit from this shift as well, particularly in enterprise communications and broadcasting, where clarity and precision are critical performance parameters.

Component Insights

Hardware codecs are expected to lead the market, with an anticipated share of 59.5% in 2026. Their dominance is attributed to their ability to deliver consistent, low-latency audio processing in embedded and real-time environments. Hardware-based solutions are widely integrated into smartphones, automotive infotainment systems, smart TVs, and wearable devices due to their efficiency and reliability. Leading semiconductor companies embed codec functionality directly into system-on-chip (SoC) architectures, enabling optimized power consumption and compact device design. For example, integrated audio codec chips in mobile processors ensure seamless playback, voice processing, and noise cancellation without significantly impacting battery performance. This makes hardware codecs indispensable for high-performance and resource-constrained applications.

Software codecs are likely to be the fastest-growing segment, fueled by the shift toward cloud-based services and software-defined audio architectures. These codecs provide flexibility by allowing updates, feature enhancements, and optimization without requiring hardware modifications. They are extensively used in streaming platforms, video conferencing tools, gaming engines, and over-the-top (OTT) applications. Examples include software-based implementations of Opus in real-time communication platforms and AAC in streaming services. The distinction between DSP-enabled and non-DSP implementations highlights the increasing adoption of hybrid models, where hardware acceleration is combined with software flexibility. This trend supports dynamic audio processing, adaptive bitrate streaming, and real-time enhancements, making software codecs essential for next-generation digital audio ecosystems.

Regional Insights

North America Audio Codec Market Trends - 5G-Driven Premium Audio Innovation and Immersive Streaming Ecosystem

North America is projected to lead the market, accounting for approximately 40.3% of market share in 2026, supported by a mature technology ecosystem, high consumer spending, and early adoption of advanced audio solutions. Strong penetration of 5G networks and connected devices continues to accelerate the use of high-quality audio applications, including streaming, gaming, and real-time communication. The presence of major technology companies such as Qualcomm, Dolby Laboratories, and Cirrus Logic strengthens innovation in codec design, particularly in low-power and high-fidelity audio processing. For example, Qualcomm’s Snapdragon Sound platform has enhanced wireless audio quality and latency performance, influencing adoption across premium smartphones and earbuds.

The U.S. serves as the primary growth engine within North America, driven by continuous investment in R&D and a robust digital infrastructure. The rapid rollout of immersive audio technologies, including Dolby Atmos integration in streaming platforms such as Netflix and Apple Music, has elevated consumer expectations for spatial and high-definition sound. Canada also contributes to market growth through increasing adoption of connected devices and smart home ecosystems, supported by expanding broadband coverage.

Key growth drivers include the expansion of OTT streaming platforms, rising demand for premium audio experiences, and the integration of advanced audio systems in automotive and consumer electronics. For instance, automakers such as Tesla and Ford Motor Company are incorporating immersive audio systems powered by advanced codecs to enhance in-car entertainment. Regulatory frameworks in the region support innovation while ensuring interoperability standards. Investment trends indicate a strong focus on software-defined audio, AI-based sound optimization, and next-generation wireless technologies, creating sustained growth opportunities.

Europe Audio Codec Market Trends - Standards-Led Codec Development and Automotive-Driven High-Fidelity Adoption

Europe represents a significant market for audio codecs, characterized by high connectivity levels, strong industrial capabilities, and a well-defined regulatory environment. The region’s emphasis on standardization and interoperability supports the adoption of advanced audio technologies across multiple sectors. Countries such as Germany, the U.K., France, and Spain are key contributors, supported by strong consumer electronics demand and automotive manufacturing leadership. Companies such as STMicroelectronics and Fraunhofer IIS play a central role in codec innovation and standard development, particularly in formats such as xHE-AAC and MPEG-H. The region’s growth is supported by increasing 5G adoption, expansion of streaming platforms, and rising demand for high-quality audio in both consumer and professional applications. European broadcasters and streaming services have been early adopters of advanced audio standards; for example, public broadcasters in Germany and the U.K. have explored MPEG-H and next-generation audio formats for immersive broadcasting. Europe also places strong emphasis on accessibility, driving adoption of assistive listening technologies and broadcast audio solutions aligned with Bluetooth LE Audio capabilities. This creates opportunities for codec providers to develop solutions tailored to regulatory and inclusivity requirements.

Investment trends highlight a shift toward software-based codec solutions and scalable licensing models. Automotive manufacturers such as BMW and Mercedes-Benz are integrating premium audio systems with advanced codec support to deliver immersive in-car experiences. The region’s collaborative approach, combining regulatory alignment, academic research, and industrial partnerships, ensures steady growth and long-term market stability.

Asia Pacific Audio Codec Market Trends - Smartphone-Led Scale Expansion and Cost-Optimized Codec Integration

Asia Pacific is expected to be the fastest-growing region in the audio codec market, driven by rapid digital transformation, large-scale smartphone adoption, and strong electronics manufacturing capabilities. The region benefits from a vast consumer base and increasing penetration of high-speed mobile networks, particularly 5G. Countries such as China, Japan, India, and members of ASEAN are central to this growth trajectory, contributing both demand and supply-side advantages.

China leads in scale and production capacity, with major smartphone manufacturers such as Xiaomi, Huawei, and OPPO integrating advanced audio codecs into devices to support high-quality streaming and wireless audio. Japan contributes through technological innovation, with companies such as Sony Group Corporation driving high-resolution audio adoption across consumer and professional segments. India and Southeast Asia are witnessing rapid growth in smartphone usage and digital content consumption, supported by affordable data plans and expanding OTT platforms such as Hotstar and regional music services.

Key growth drivers include rising disposable incomes, increasing consumption of digital media, and expansion of automotive and consumer electronics industries. For example, automotive manufacturers in the region are increasingly adopting advanced infotainment systems with immersive audio capabilities, particularly in China’s electric vehicle segment. Additionally, semiconductor companies such as MediaTek are enabling cost-effective codec integration in mid-range and budget devices, accelerating market penetration. Investment in infrastructure, local manufacturing, and technology partnerships continues to drive regional growth. Asia Pacific offers significant opportunities for companies to scale production, establish strategic collaborations, and capture emerging demand for advanced, low-power, and high-fidelity audio technologies across diverse applications.

Competitive Landscape

The global audio codec market is moderately fragmented, with several leading players competing across hardware, software, and licensing segments. While certain companies hold significant market share in specific applications such as smartphones, the broader market remains competitive due to the presence of multiple technology providers. Companies differentiate themselves through innovation, integration capabilities, and strategic partnerships. The competitive landscape is shaped by continuous advancements in audio technology and evolving consumer expectations.

Market leaders are prioritizing innovation, ecosystem partnerships, and software-driven solutions to maintain competitive advantage. Strategies focus on improving audio quality, reducing power consumption, and expanding into new application areas such as automotive and immersive communication. Companies are also adopting flexible licensing models and investing in research and development to address evolving market demands.

Key Industry Developments:

- In January 2025, Samsung and Google introduced Eclipsa Audio, a next-generation immersive audio format based on open standards, aimed at enabling 3D spatial audio experiences across TVs, streaming platforms, and connected devices while reducing reliance on licensed codecs.

- In June 2025, Apple unveiled a new Apple Spatial Audio Format (ASAF) with its positional audio codec (APAC), designed to enhance immersive audio experiences across Apple devices and ecosystems, particularly for mixed reality and streaming applications.

Companies Covered in Audio Codec Market

- Qualcomm

- Cirrus Logic

- MediaTek

- Realtek Semiconductor

- Texas Instruments

- Analog Devices

- STMicroelectronics

- NXP Semiconductors

- Renesas Electronics

- ROHM Semiconductor

- Sony Group Corporation

- Dolby Laboratories

- Synopsys

- Fraunhofer IIS

- Broadcom

- Apple

Frequently Asked Questions

The global audio codec market is estimated to be valued at US$ 7.8 billion in 2026.

The audio codec market is projected to reach US$ 12.0 billion by 2033.

Key trends include the adoption of Bluetooth LE Audio and LC3 codecs, growing demand for high-resolution and lossless audio, increasing integration of audio codecs in automotive infotainment systems, and the shift toward software-defined and cloud-based audio processing solutions.

The smartphones and tablets segment is the leading application category, accounting for approximately 29.51% of the market share, driven by widespread device usage and streaming consumption.

The audio codec market is expected to grow at a CAGR of 6.4% between 2026 and 2033.

Major players with strong product portfolios include Qualcomm, Cirrus Logic, MediaTek, Realtek Semiconductor, and Dolby Laboratories.