- Technology

- 3D Printed Jewelry Market

3D Printed Jewelry Market Size, Share, and Growth Forecast 2026 - 2033

3D Printed Jewelry Market by Product Type (Necklace, Ring, Earring, Bracelet, Others), Distribution Channel (Online, Offline), and Regional Analysis for 2026 - 2033

3D Printed Jewelry Market Size and Trend Analysis

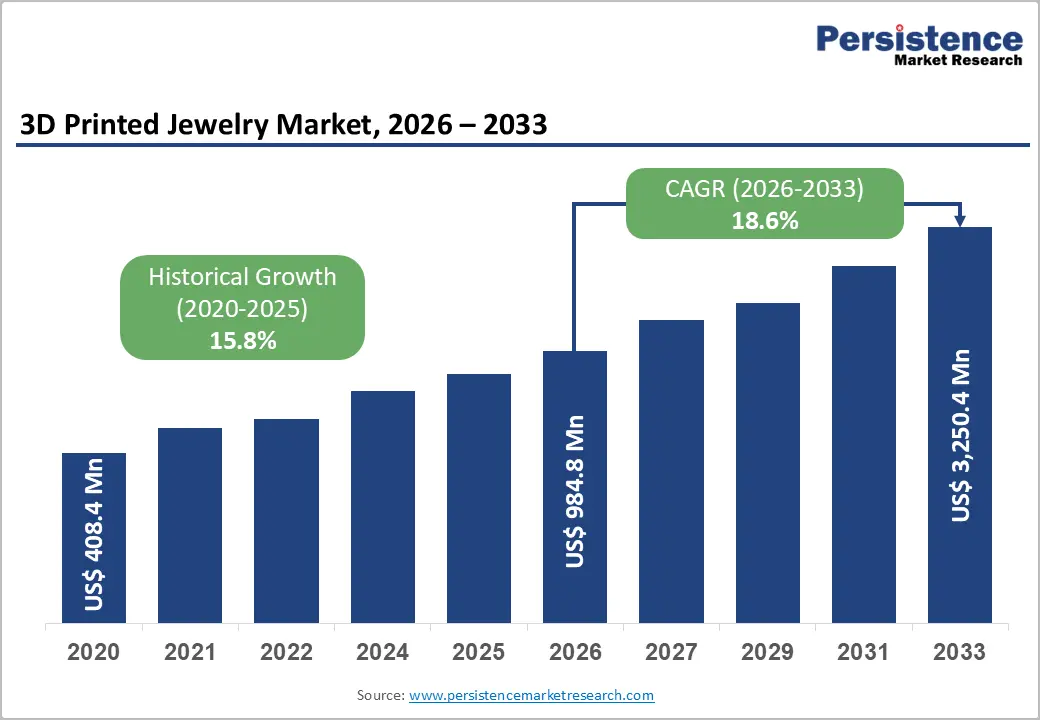

The global 3D Printed Jewelry market size is valued at US$ 984.8 million in 2026 and is projected to reach US$ 3,250.4 million by 2033, growing at a CAGR of 18.6% between 2026 and 2033. Jewelry making is a craft yet time-intensive process. Use of digital designs and 3D printing transforming the jewelry industry. By combining traditional methods with modern digital technologies, jewelers can create more complex designs, improve production efficiency, and offer better customization options to customers. Jewelry 3D printing works alongside the traditional investment casting or lost-wax casting process, while adding the benefits of digital design and manufacturing.

The market is experiencing strong growth driven by accelerating adoption of additive manufacturing technologies in the Jewelry sector, rising consumer demand for customized and personalized adornments, and the expanding accessibility of metal 3D printing and photopolymer resin printing systems. Growing e-commerce penetration enables direct-to-consumer customization on a scale, while declining hardware costs and improvements in selective laser sintering (SLS) and direct metal laser sintering (DMLS) technologies are lowering barriers for independent designers and established brands alike, further stimulating market expansion.

Key Market Highlights

- Personalized Jewelry Demand: Rising consumer preference for customized jewelry is driving market growth, with over 36% of consumers interested in personalized products, especially among millennials and Gen Z buyers.

- Advanced Printing Technologies: Innovations in DMLS, SLA, and specialty materials are improving design precision, enabling complex jewelry production, and reducing precious metal waste by up to 70%.

- Growing Online Sales: Global online jewelry sales surpassed US$58 billion in 2024 and are growing at over 12% annually, creating strong growth opportunities for customized 3D-printed jewelry platforms.

- Sustainable Manufacturing Focus: Additive manufacturing uses only 10% surplus material, encouraging luxury brands such as Cartier and Chopard to adopt sustainable jewelry production practices.

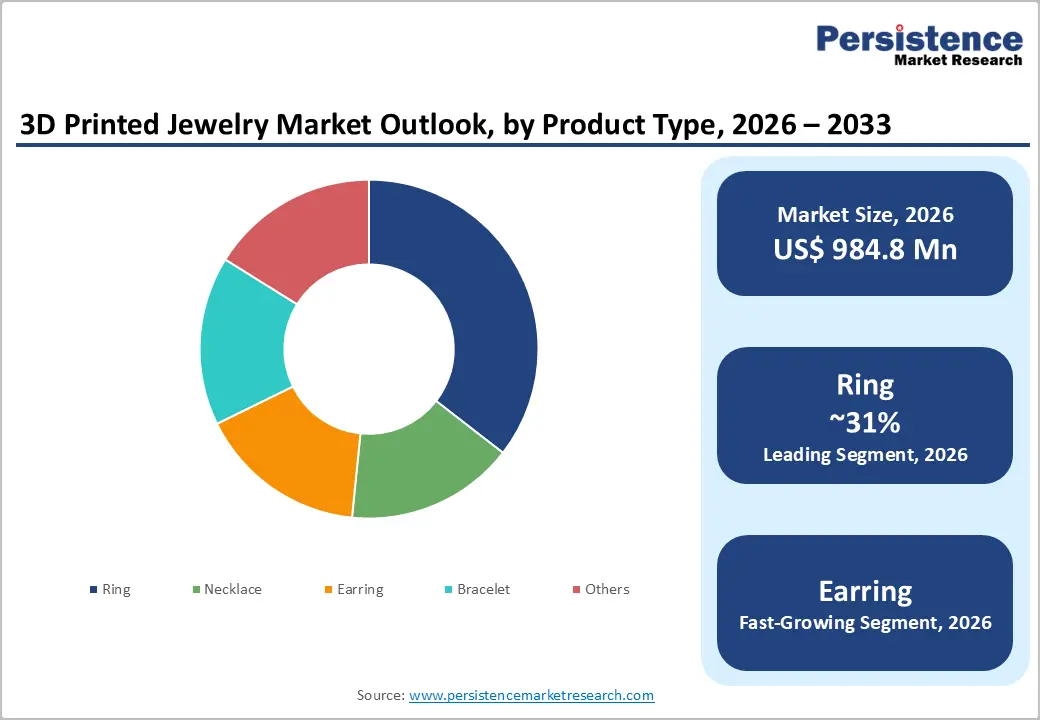

- Dominance of Rings: Rings account for approximately 31% of the total market share in 2025 due to high demand for personalized engagement rings, wedding bands, and fashion jewelry.

- Earrings Fast-Growth: The earrings segment is projected to reach a CAGR of 21.4% due to increasing demand for lightweight and fashion-oriented jewelry designs.

- Online Channel Leadership: Online distribution channels dominate the market with around 58% revenue share in 2025, supported by e-commerce growth, digital configurators, and social commerce platforms.

Market Dynamics

Drivers - Rising Consumer Demand for Personalized and Customized Jewelry

The most prominent driver accelerating the 3D printed Jewelry market is the surge in consumer preference for personalized accessories. According to a Deloitte consumer survey, more than 36% of consumers expressed interest in purchasing personalized products, and Jewelry ranked among the top three categories. Additive manufacturing enables jewelers to craft unique, made-to-order designs with complex geometries that are impossible to achieve using traditional casting or milling techniques.

Digital design tools like CAD (Computer-Aided Design) integrated with 3D printing workflows allow even small studios to offer bespoke engagement rings, monogrammed pendants, and intricately patterned bracelets at competitive costs. This resonates strongly with millennial and Gen Z consumers who prioritize uniqueness and self-expression in fashion, fueling sustained demand growth across online and offline retail channels.

Technological Advancements in Additive Manufacturing and Material Science

Rapid technological advancement in 3D printing hardware and specialty materials is a powerful driver for the Jewelry market. The commercialization of direct metal laser sintering (DMLS) and stereolithography (SLA) systems capable of processing gold, silver, platinum, and titanium alloys has dramatically expanded design possibilities. The World Gold Council reports increasing experimentation with 3D-printed gold Jewelry among luxury brands seeking to optimize material use and reduce waste by up to 70% compared to traditional subtractive fabrication. Additionally, innovations in castable photopolymer resins allow lost-wax casting at finer tolerances, enabling mass customization at lower per-unit costs, attracting mid-market jewelers and independent artisans to adopt these technologies.

Restraints - High Initial Capital Expenditure and Skill Requirements

Despite falling equipment costs, the initial investment in industrial-grade metal 3D printers remains a significant barrier. Professional DMLS or SLM (Selective Laser Melting) systems can cost between US$ 150,000 and US$ 500,000, placing them beyond the reach of small Jewelry studios. Furthermore, operating these machines requires specialized knowledge in CAD/CAM software and materials science. The Jewelers of America estimates that fewer than 12% of independent jewelers in the U.S. have adopted additive manufacturing workflows, underscoring the skills gap constraining broader market penetration.

Regulatory and Hallmarking Compliance Challenges

Jewelry produced via 3D printing must comply with strict national and international hallmarking and precious metals purity standards. In the European Union, directives such as those enforced by the International Hallmarking Convention require rigorous assay testing of all items offered for sale. Additive manufacturing of multi-metal or composite pieces can complicate this assay process. Inconsistent material distributions in printed metal parts may cause finished pieces to fail purity thresholds, leading to rework costs and delays. These regulatory hurdles slow adoption among jewelers in markets with strong hallmarking traditions, including the U.K., Germany, and India.

Opportunities - Expansion of Online Custom Jewelry Platforms and D2C Models

One of the most compelling opportunities in the 3D printed Jewelry market lies in the rapid proliferation of direct-to-consumer (D2C) online platforms that leverage digital customization interfaces paired with on-demand 3D printing fulfillment. As of 2024, global e-commerce Jewelry sales surpassed US$ 58 Bn, according to Statista, and this channel continues to grow at over 12% annually.

Companies such as Nervous System and Shapeways have demonstrated that consumers are willing to pay a premium for algorithm-generated, fully individualized designs. Emerging augmented reality (AR) try-on tools integrated into online stores further reduce purchase hesitation, increasing conversion rates. This shift creates a substantial opportunity for both established brands and startups to capture recurring revenue from design-conscious consumers globally.

Sustainable Manufacturing and Luxury Sector Adoption

Growing emphasis on sustainable production presents a major opportunity for 3D printed Jewelry. Traditional lost-wax casting generates substantial metal waste, whereas additive manufacturing typically uses only 5–10% surplus material, much of which is recyclable. The Responsible Jewelry Council (RJC) has highlighted additive manufacturing as a key enabler of reduced environmental footprint in the fine Jewelry sector.

Luxury brands such as Cartier and Chopard have begun pilot programs integrating 3D printing for prototype development and limited-edition collections, demonstrating high-end market validation. With sustainability increasingly influencing purchasing decisions, especially among consumers aged 18–35, adoption by major luxury houses signals a transformative shift that could unlock premium market tiers and drive significant revenue growth for technology providers.

Category-wise Analysis

Product Type Insights

Among the product categories in the 3D printed jewelry market, rings hold the dominant position, accounting for approximately 31% of the total market share in 2026. This dominance is attributable to the category's high demand for personalization. Engagement rings, wedding bands, and fashion rings are among the most requested custom Jewelry items worldwide. The ability of 3D printing to produce intricate lattice structures, bespoke sizing, and embedded stone settings with millimeter-level precision makes it exceptionally well-suited for ring fabrication.

Rings account for approximately 29% of total U.S. fine Jewelry sales by value, and 3D-printed rings are claiming an increasing share of this segment. Consumer acceptance of technology-fabricated luxury rings has grown substantially, validated by major retailers offering CAD-to-print ring customization services both in-store and online.

The earrings segment is the fast-growing product category within the 3D printed Jewelry market, projected to grow at a CAGR of approximately 21.4% during the forecast period. Earrings lend themselves particularly well to additive manufacturing due to their small size, lightweight design requirements, and strong consumer appetite for fashion-forward geometric forms that push the limits of traditional manufacturing.

Distribution Channel Insights

The online distribution channel dominates the 3D printed Jewelry market, commanding approximately 58% of total market revenue in 2026. The digital-native nature of 3D printed Jewelry where products typically originate as digital design files makes e-commerce an inherently efficient and scalable distribution model. Online platforms enable jewelers to display infinite design variants, offer interactive 3D configurators, and operate globally without the overhead of brick-and-mortar retail.

The growth of social commerce, particularly on platforms such as Instagram and Pinterest has further amplified online sales, with visually distinctive 3D-printed Jewelry designs achieving viral reach. According to Statista, global online Jewelry sales grew by over 15% in 2023 alone, providing a strong tail wind for digitally distributed 3D printed Jewelry. Logistics improvements including same-day local printing fulfillment networks are also reducing delivery times, addressing a historically noted barrier to online fine Jewelry purchases.

The offline distribution channel is the fastest growing segment in this category, anticipated to grow at a CAGR of 20.2% from 2026 to 2033. Physical retail is being reinvented through in-store 3D printing kiosks and digital design consultation services, offering tactile experiences that augment the personalization appeal of 3D printed Jewelry and drive premium purchase decisions.

Regional Insights

North America 3D Printed Jewelry Trends

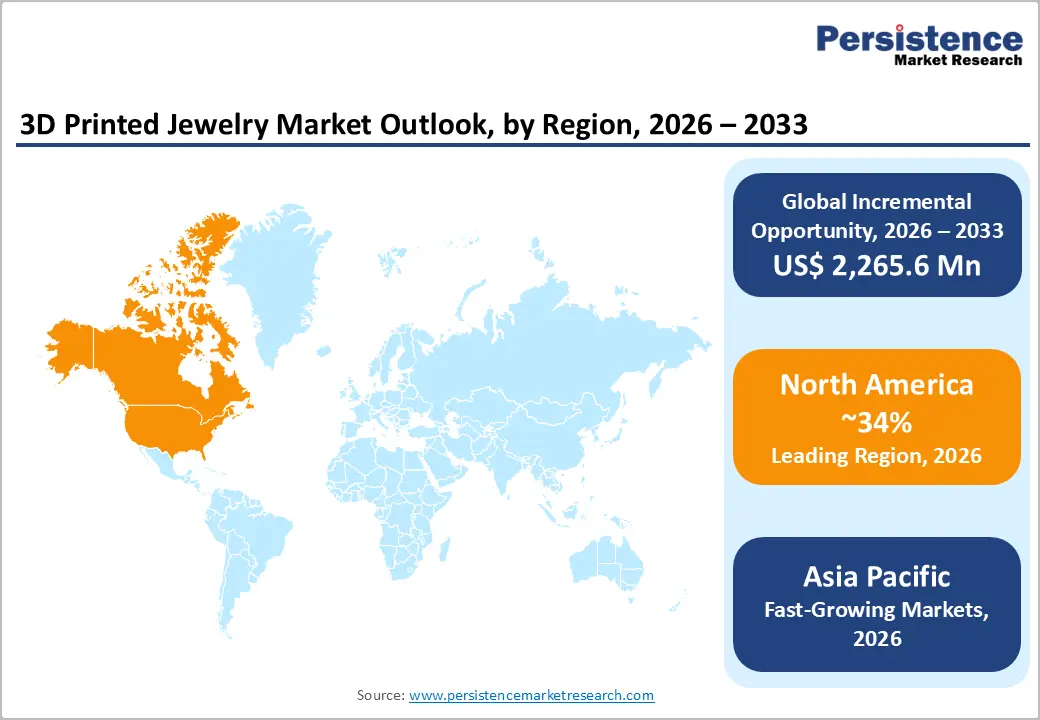

North America is the leading regional market for 3D printed Jewelry, holding approximately 34% of global market share in 2026. The region benefits from strong consumer spending on Jewelry, a mature e-commerce infrastructure, and widespread availability of industrial-grade additive manufacturing technologies. The United States is the primary engine of growth, with its large base of technology-forward consumers and a robust ecosystem of 3D printing service bureaus that support Jewelry brands of all sizes.

Canada is also emerging as a notable market, particularly for sustainable luxury Jewelry. Canadian government initiatives supporting advanced manufacturing through the Strategic Innovation Fund have catalyzed investments in additive manufacturing capabilities. North American trade shows such as JCK Las Vegas increasingly feature 3D-printed Jewelry collections, signaling mainstream industry acceptance.

- U.S.: Largest Market for Customized 3D Printed Fine Jewelry

The United States commands approximately 78% of the North American 3D printed Jewelry market and is poised at an estimated CAGR of 17.9% by 2033. The country's dominance is underpinned by its advanced manufacturing base, including companies such as Shapeways and Nervous System that have pioneered mass-customized 3D printed Jewelry. American consumers rank Jewelry among their top discretionary purchases, spending over US$ 39 Bn annually on fine and fashion Jewelry according to the Jewelers of America. The proliferation of CAD-enabled jewelers, established metal 3D printing service networks, and high consumer tech literacy collectively cement the U.S. as the global bellwether for market adoption.

Europe 3D Printed Jewelry Trends

Europe represents the second-largest regional market, supported by a heritage of fine craftsmanship, strong luxury Jewelry consumption, and growing integration of digital fabrication tools among established Jewelry houses. Key markets include Germany, the U.K., France, and Italy. European jewelers have been early adopters of SLA and wax 3D printing for prototype development, and many are now transitioning toward full production use. Regulatory frameworks under the EU Ecodesign Regulation are encouraging manufacturers to adopt lower-waste production methods, accelerating the shift toward additive manufacturing.

The Responsible Jewelry Council (RJC) has noted increasing European brand commitments to sustainable supply chains, further boosting adoption of 3D printing. Germany's Formnext trade fair the world's leading additive manufacturing exhibition regularly showcases Jewelry-focused 3D printing applications, reflecting the region's central role in technology adoption and dissemination.

- Germany: Engineering Precision Driving 3D Jewelry Innovation

Germany holds approximately 22% of the Europe 3D printed Jewelry market, poised to reach a CAGR of 17.2% through 2033. German engineering excellence translates directly into high adoption of precision DMLS and SLM technologies. Cities like Pforzheim historically known as the 'City of Gold' are hubs for additive manufacturing integration in Jewelry production. German companies such as EOS GmbH have developed metal 3D printing systems widely adopted by European jewelers, cementing Germany's dual role as both a consumer and technology supplier.

- U.K.: Fashion-Forward Market Embracing Bespoke 3D Printed Designs

The United Kingdom accounts for approximately 19% of the Europe with a CAGR of 17.8%. London's is a global fashion capital that drives strong demand for cutting-edge Jewelry design. British institutions such as the Royal College of Art and the British Jewellers' Association actively support 3D printing curriculum development and industry workshops. The Assay Office has developed protocols for hallmarking 3D printed precious metal Jewelry, reducing regulatory friction for market participants.

- France: Luxury Couture Heritage Merging with Digital Jewelry Fabrication

France holds approximately 17% of the Europe 3D printed Jewelry market. France's luxury Jewelry houses, including Van Cleef & Arpels and Boucheron, have incorporated 3D printing into their haute joaillerie prototyping workflows. The Institut Français de la Mode has highlighted digital fabrication as a critical skill for the next generation of French Jewelry designers, supporting an ecosystem of tech-savvy artisans who are pushing the boundaries of the craft.

- Italy: Artisanal Tradition Complemented by Advanced 3D Printing Technology

Italy commands approximately 20% of the European 3D printed Jewelry market and is growing at a leading CAGR. Renowned Jewelry districts such as Vicenza and Valenza are incorporating 3D printing to complement traditional goldsmithing. The Italian Exhibition Group (IEG), organizer of Vicenzaoro the world's premier gold and Jewelry trade show has dedicated significant exhibition space to additive manufacturing in recent editions, reflecting Italy's strategic push to modernize its artisanal Jewelry industry through digital technologies.

Asia Pacific 3D Printed Jewelry Trends

Asia Pacific is the fast-growing market for 3D printed Jewelry, driven by expanding manufacturing capabilities, a vast and aspirational consumer base, and government-led digital manufacturing initiatives. China, India, Japan, and South Korea are leading adoption, each contributing distinct demand profiles. China's dominant role in global 3D printing hardware production creates strong cost advantages, while India's booming Jewelry consumption market second largest in the world by volume is beginning to embrace additive technologies.

Japan's precision manufacturing culture aligns well with the exactness required for fine 3D printed Jewelry, while South Korea's technology-forward consumer market and K-fashion influence are creating new demand vectors for innovative Jewelry forms. ASEAN nations such as Thailand and Vietnam traditionally strong Jewelry manufacturing hubs are also exploring 3D printing integration to enhance design capability and production efficiency.

- China: Global 3D Printing Manufacturing Hub Powering Jewelry Production

China holds approximately 38% of the Asia Pacific 3D printed Jewelry market and is likely to reach a positive CAGR in the forecast period. China is the world's largest producer and exporter of 3D printing equipment, with domestic players such as BLT (Bright Laser Technologies) and Bambu Lab significantly reducing equipment costs globally. The Chinese government's 'Made in China 2025' initiative prioritizes additive manufacturing, supporting direct capital investment in Jewelry-sector applications. The country's massive gold Jewelry consumption accounting for approximately 28% of global demand per the World Gold Council provides an enormous domestic addressable market.

- India: Booming Jewelry Consumption Fueling 3D Printing Technology Uptake

India accounts for approximately 18% of the Asia Pacific market, making it one of the fastest growing market. India is the world's second largest Jewelry consumer and a major manufacturing hub. The Gem & Jewelry Export Promotion Council (GJEPC) has actively promoted 3D printing adoption among Indian manufacturers to improve design competitiveness in export markets. Government programs under Skill India and Make in India are also funding 3D printing training for artisans in key Jewelry manufacturing centers such as Surat, Jaipur, and Mumbai.

- South Korea: K-Fashion Driving Demand for Avant-Garde 3D Printed Jewelry

South Korea represents approximately 12% of the Asia Pacific 3D printed Jewelry market and is growing at a leading CAGR. South Korea's globally influential K-pop and K-fashion culture has created intense demand for fashion-forward, limited-edition Jewelry. Korean consumers are among the most technologically sophisticated globally, and e-commerce adoption for Jewelry in South Korea grew by over 18% in 2023 according to Statistics Korea. The country's advanced semiconductor and electronics manufacturing ecosystem provides strong underlying capabilities for precision 3D printing technology adaptation in Jewelry applications.

Competitive Landscape

The global 3D Printed Jewelry market is moderately fragmented, featuring a blend of large multinational manufacturers and numerous regional specialists. Leading European players such as Warema Renkhoff SE, markilux GmbH + Co. KG, and Schmitz-Werke GmbH command significant shares in the premium segment through product innovation and design excellence. North American players, including SunSetter Products LP and Sunesta LLC, dominate the residential retractable 3D Printed Jewelry category through strong direct-to-consumer and dealer network models. Companies across the board are focusing on smart technology integration, eco-friendly materials, and customization as key differentiators. Strategic alliances, acquisition activity, and regional manufacturing expansion are the primary growth strategies employed to capture emerging opportunities.

Key Industry Developments:

- In June 2025, Platinum Guild International (PGI) introduced the world’s first commercially available 3D-printed platinum jewellery collection. Named “Tùsaire,” a Scottish Gaelic word meaning “pioneer,” the collection represents a major advancement in jewellery manufacturing and design innovation. The launch highlights the growing adoption of additive manufacturing technology in the precious metal jewellery industry, enabling more advanced designs, improved precision, and greater production flexibility.

- In January 2025, Shapeways announced a strategic partnership with a leading European fine Jewelry brand to launch an AI-powered custom ring design platform integrating DMLS gold printing for direct consumer fulfillment, expanding its premium market footprint.

- In March 2024, Nervous System (USA) unveiled its 'Lichen' earring collection, the first fully generative algorithm-designed 3D printed silver Jewelry line to be sold through a major department store chain, marking a milestone for mainstream retail penetration.

- In October 2024, EOS GmbH (Germany) introduced the EOS M 290 1kW metal 3D printer with enhanced gold and platinum alloy compatibility, directly targeting the fine Jewelry manufacturing sector and enabling higher throughput for small luxury producers.

Global 3D Printed Jewelry Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 408.4 Mn |

|

Current Market Value (2026) |

US$ 984.8 Mn |

|

Projected Market Value (2033) |

US$ 3,250.4 Mn |

|

CAGR (2026–2033) |

18.6% |

|

Leading Region |

North America, ~34% share |

|

Dominant Segment |

Rings, ~31% share (2025) |

|

Top-ranking Segment |

Online Distribution, ~58% share |

|

Incremental Opportunity (2026–2033) |

US$ 2,265.6 Mn |

Companies Covered in 3D Printed Jewelry Market

- Shapeways

- Nervous System

- EOS GmbH

- Materialise NV

- i.materialise

- 3D Systems Corporation

- Stratasys Ltd.

- Cookson Precious Metals

- Cooksongold

- Legor Group

- Renishaw plc

- Formlabs Inc.

Frequently Asked Questions

The global 3D printed Jewelry market is projected to reach US$ 3,250.4 Mn by 2033, growing from US$ 984.8 Mn in 2026 at a CAGR of 18.6% during the forecast period.

Key growth drivers include rising consumer demand for personalized and custom Jewelry, rapid advancements in additive manufacturing technologies such as DMLS and SLA, declining equipment costs, and the exponential growth of e-commerce Jewelry platforms that facilitate direct-to-consumer customization at scale.

The rings segment is the dominant product category, accounting for approximately 31% of total market share in 2025. High demand for personalized engagement and wedding rings, enabled by CAD-integrated 3D printing, is the primary driver of this segment's leadership.

North America is the leading regional market, holding approximately 34% of the global market share in 2025. The United States is the dominant country within the region, supported by strong consumer spending, a mature e-commerce infrastructure, and an advanced ecosystem of 3D printing service bureaus.

Key opportunities include the expansion of D2C online customization platforms powered by on-demand 3D printing fulfillment, adoption of sustainable manufacturing practices incentivized by regulations, and entry of luxury Jewelry brands into additive manufacturing for limited editions and bespoke collections.

Leading market players include Shapeways, Nervous System, EOS GmbH, Materialise NV, 3D Systems Corporation, Stratasys Ltd., Formlabs Inc., and Renishaw plc, among others.