- Food Ingredients & Additives

- Oats Market

Oats Market Size, Share, and Growth Forecast, 2026 - 2033

Oats Market by Product Type (Whole Oats, Rolled Oats, Steel Cut Oats, Instant Oats, Oat Flour, Others), Form (Granules, Flakes, Powder, Coarse), Application (Food & Beverages, Animal Feed, Personal Care & Cosmetics, Others), and Regional Analysis for 2026 - 2033

Oats Market Share and Trends Analysis

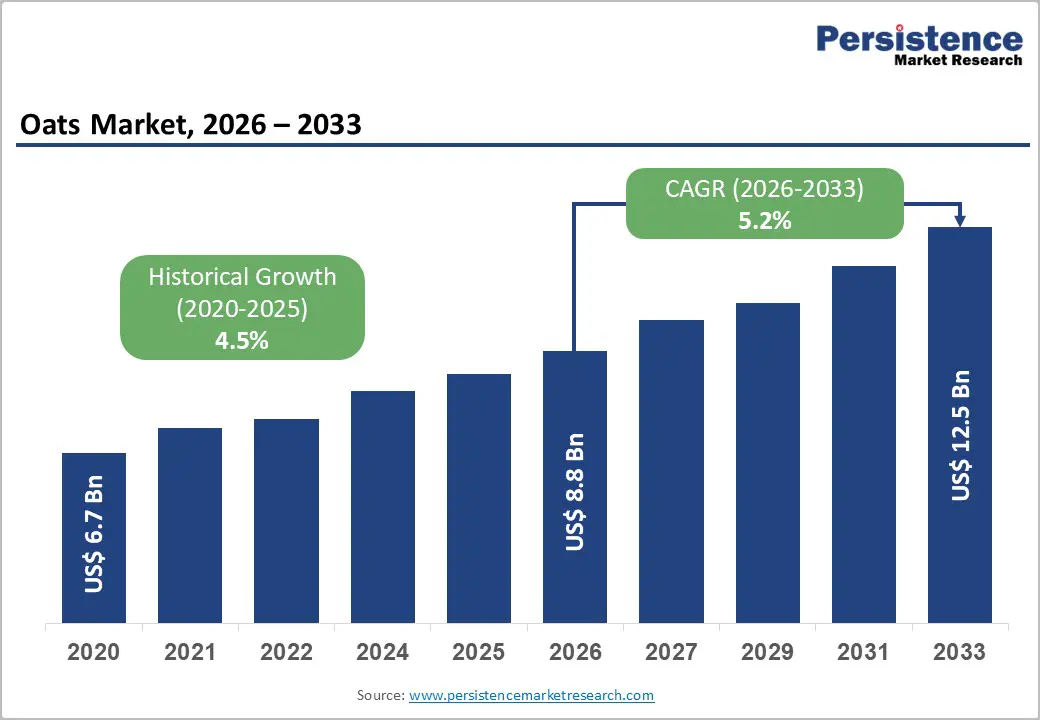

The global oats market size is likely to be valued at US$ 8.8 billion in 2026 and is estimated to reach US$ 12.5 billion by 2033, growing at a CAGR of 5.2% during the forecast period 2026 - 2033.

Growth trajectory reflects a sustained shift toward health-oriented diets and functional nutrition. Rising incidence of metabolic and cardiovascular conditions drives demand for fiber-rich, cholesterol-lowering foods, positioning oats within preventive nutrition. Guidance from global health authorities supports whole grain consumption, reinforcing demand. Urbanization and dual-income lifestyles increase preference for convenient oat-based formats, including instant oats and beverages, while retail and e-commerce expansion improves accessibility.

Advancements in processing enable value-added products such as oat protein, oat milk, and gluten-free variants. Clinical validation of beta-glucan benefits supports dietary inclusion, strengthening adoption across diverse consumer groups and age segments globally.

Key Industry Highlights

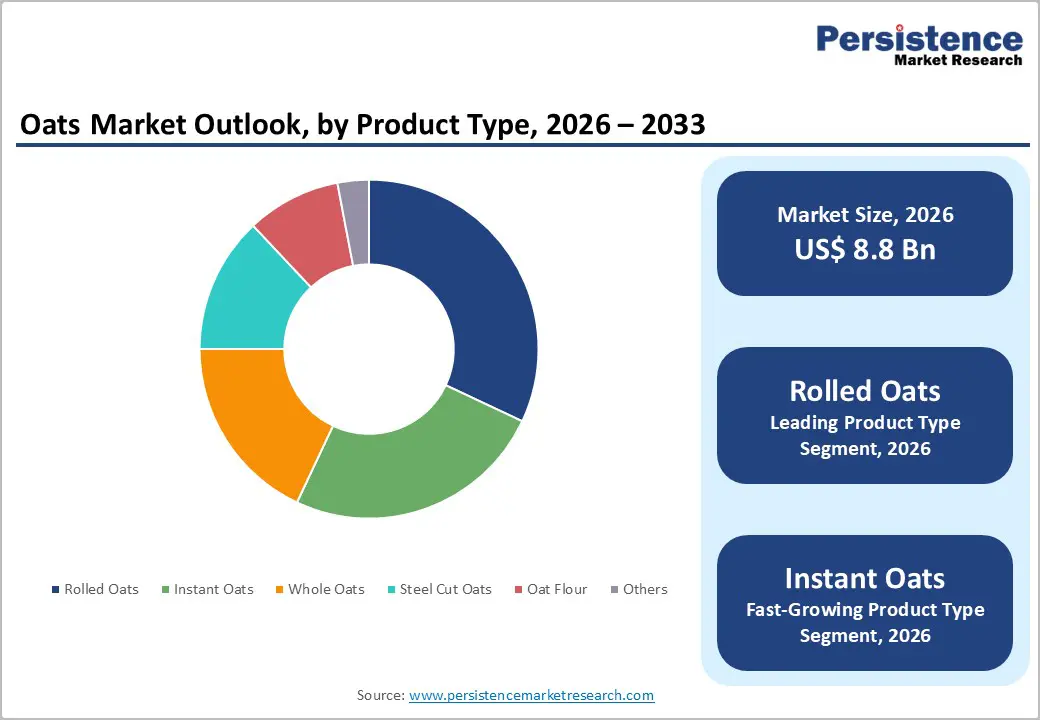

- Leading Product Type: Rolled oats are set to hold around 32% market share in 2026 due to balanced processing, nutritional retention, and widespread application across breakfast and snack categories.

- Fastest-Growing Product Type: Instant oats are likely to record the fastest growth, driven by convenience demand and urban lifestyles.

- Leading Form: Flakes are anticipated to command around 38% share in 2026, powered by consumer familiarity and strong retail presence.

- Fastest-Growing Form: Powder is expected to be the fastest-growing segment from 2026 to 2033, supported by technological enhancements in solubility and nutrient retention.

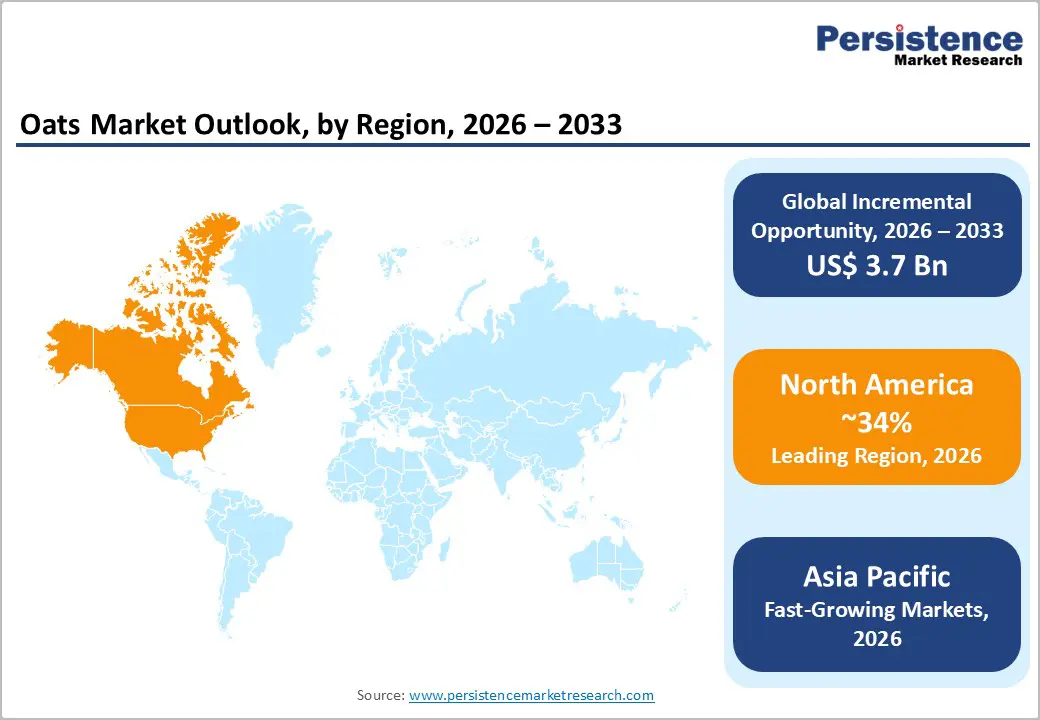

- Regional Leadership: North America is projected to capture nearly 34% share in 2026, while Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, stimulated by health awareness and retail modernization.

- Competitive Environment: Market features moderate fragmentation with global leaders including PepsiCo, General Mills, and Kellogg; competition focuses on innovation, brand trust, and retail penetration.

- Innovation Trends: Expansion in plant-based and functional oat products, including beverages, fortified cereals, and personal care applications, drives differentiation and long-term growth.

| Key Insights | Details |

|---|---|

| Oats Market Size (2026E) | US$ 8.8 Bn |

| Market Value Forecast (2033F) | US$ 12.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

DRO Analysis

Driver - Rising Health Awareness and Preventive Nutrition Adoption

Heightened public concern for chronic disease risk and personal wellness is reshaping dietary behavior toward foods that deliver measurable nutritional value, driving sustained demand for oats as a staple whole grain source. Epidemiological evidence linking fiber-rich diets with reduced cholesterol, improved glycemic control, and lower incidence of type-2 diabetes strengthens consumer preference for oat products over refined alternatives, creating persistent demand expansion on the retail and foodservice sides. Increased awareness of nutrition quality encourages household-level adoption of breakfast cereals, snacks, and ready-to-drink beverages containing oats, translating into higher per capita consumption and consistent growth for manufacturers and distributors across diverse geographic regions.

Parallel growth in preventive nutrition adoption among healthcare professionals and insurers embeds oat inclusion into formal dietary guidance and clinical practice, elevating its role from sporadic food choice to a strategic component of risk-reduction protocols. As dietitians and medical providers emphasize foods that modulate lipid profiles and support metabolic health, institutional procurement at hospitals, workplaces, and schools adjusts purchasing toward oats, expanding operational demand beyond individual consumers to organizational buyers. Retail assortment planners respond with broader oat product lines, reinforcing positive feedback between perceived health benefits and unit sales growth in grocery, e-commerce, and foodservice channels.

Expansion of Plant-Based and Functional Food Ecosystem

Rising consumer adoption of plant-based and functional foods has structurally expanded demand for oats by aligning with federal nutritional priorities. The 2025 U.S. Dietary Guidelines recommend 2-4 servings of whole grains daily, signaling support for fiber-rich ingredients central to plant-based diets. Retailers respond with expanded shelf space for oat-based beverages and fortified grain products, increasing visibility. Manufacturers incorporate oats into breakfast, bakery, and beverage applications to reduce saturated fat and enhance micronutrient content, creating operational efficiency and stimulating volume growth.

Consumer health priorities and manufacturer innovation strengthen oats’ positioning in the functional ecosystem. Low raw material costs and versatile properties enable high-fiber, low-allergen formulations meeting clean-label and nutrient-dense requirements. Product portfolios include oat-based dairy alternatives, snack bars, and cereals targeting flexitarian and health-conscious segments. Fortification with protein and micronutrients embeds oats in functional products, reinforcing consumption patterns aligned with metabolic health and digestive wellness, driving broader adoption across diverse channels and demographic groups.

Restraint - Price Volatility and Agricultural Dependency

Volatility in pricing undermines long-term investment planning and cost forecasting for producers, processors, and distributors of oats, creating exposure to rapid swings in input costs and retail margins when supply tightness or surpluses occur. Limited regional concentration of production makes availability sensitive to short-term shocks and seasonal fluctuations, directly impacting pricing. Sudden supply reductions trigger sharp cost adjustments that increase procurement expenses, compress operational margins, and reduce demand elasticity. Persistent price fluctuations discourage capacity expansion and long-term contracts, reinforcing cyclical patterns rather than supporting stable cost structures.

Dependence on agronomic conditions restricts yield predictability, limiting supply responsiveness during periods of high demand and amplifying operational risk. Reliance on narrow crop cycles exposes production to weather anomalies, pest incidence, and input cost variations that significantly affect yield quality and tonnage. Operational rigidity passes upstream in supply chains, forcing processors to maintain buffer inventories or accept premium spot purchases when output falls short, compressing margins and constraining downstream affordability. Fixed cultivation areas amplify supply sensitivity relative to consumption trends.

Competition from Alternative Grains and Processed Substitutes

Rising consumer interest in quinoa, barley, millet, and other whole grains creates significant demand diversion from oats. These alternatives offer comparable nutritional benefits, diverse flavors, and versatile applications across breakfast cereals, snacks, and beverages. Retailers allocate shelf space strategically, favoring products with strong consumer traction and higher profit margins, which can limit visibility and uptake of oats. Operationally, supply chains for alternative grains benefit from established distribution networks and lower import or processing constraints in certain regions, reinforcing competitive pressure. Price-sensitive segments may shift to substitutes offering perceived value or affordability, reducing volume growth and slowing penetration of oat-based products.

Processed substitutes such as fortified cereals, ready-to-drink grain beverages, and protein-enriched blends attract consumers seeking convenience and functional nutrition. Product innovation cycles in these categories respond rapidly to emerging dietary trends, shortening adoption time for new offerings. Brand loyalty in alternative grains strengthens through targeted marketing and digital engagement, creating barriers for oats to expand in high-growth segments. Distribution partnerships and promotional strategies of substitutes further reinforce competitive positioning against oats.

Opportunity - Innovation in Functional and Value-Added Oat Products

Development of functional and value-added oat products expands demand through alignment with evolving consumer preferences and dietary priorities. Introduction of oat-based beverages, protein concentrates, fortified snacks, and specialty breakfast items captures demand for nutrient-dense, convenient foods. Products emphasizing fiber, plant protein, and micronutrient enrichment respond to lifestyle-driven consumption patterns while enabling differentiation in crowded food categories. Premium positioning supports higher price points, capturing affluent health-conscious segments. Functional attributes, such as cholesterol management and glycemic control, create tangible health associations that influence purchase decisions. Product diversification also enhances retailer assortment strategies, increasing shelf presence and consumer exposure in both conventional and specialty channels.

Advances in processing technologies drive operational efficiency and product quality in functional oat categories. Techniques including milling optimization, enzymatic extraction, and ingredient fractionation enable higher yields of bioactive compounds while maintaining sensory appeal. Formulation flexibility allows integration of oats into beverages, snacks, and bakery products, expanding addressable consumer segments. Manufacturers benefit from scalable production systems that reduce waste and support multiple product lines from a single input. Retailers capitalize on differentiated SKUs targeting health outcomes, convenience, and taste preferences, stimulating repeat purchases and cross-category adoption. Enhanced product versatility reinforces supply chain efficiency and strengthens brand positioning within functional and wellness-driven food markets.

E-Commerce and Direct-to-Consumer Channels

Online retail and direct-to-consumer distribution represent a key opportunity for the oats market by structurally expanding addressable demand through scalable digital channels that bridge geographic and operational gaps between producers and consumers. Digital platforms enable producers to bypass traditional intermediaries, reducing unit distribution costs and unlocking competitive pricing advantages while capturing margin previously retained by third-party retailers. A growing proportion of U.S. retail transactions now occur online, with e-commerce accounting for about 16.6% of total retail sales in the fourth quarter of 2025, according to the U.S. Census Bureau, illustrating sustained consumer migration toward online purchasing. E-commerce environments also support precision marketing, targeted promotions, and personalized consumer engagement that translate into higher conversion rates and increased repeat purchases relative to conventional retail.

Direct digital engagement deepens consumer insights and accelerates product adoption by enabling granular tracking of preferences, purchase frequency, and demand patterns across segments, facilitating smarter production planning and inventory allocation. Real-time data analytics drive dynamic pricing and tailored bundling, enhancing responsiveness to seasonal or episodic shifts in consumption. Operational efficiencies emerge from streamlined logistics networks that integrate order management with scalable fulfillment and distribution partners, reducing lead times and inventory holding costs. Cross-border digital channels also extend reach into emerging economies where brick-and-mortar distribution is limited, creating new revenue streams and strengthening resilience against localized disruptions in traditional retail infrastructure.

Category-wise Analysis

Product Type Insights

Rolled oats are anticipated to secure around 32% share in 2026, reflecting strong alignment with consumer demand for balanced nutrition and convenience. Minimal processing and consistent texture support widespread use in households and food service, including oatmeal, granola bars, and baked goods such as muffins. Endorsements from the World Health Organization on whole grains reinforce consumption due to fiber and micronutrient retention. Manufacturers incorporate rolled oats into cereals, snack bars, and energy bites, while supermarkets, online platforms, and convenience stores ensure broad availability.

Instant oats are expected to be the fastest-growing segment during the 2026 - 2033 forecast period, propelled by increasing demand for convenience-driven food solutions and time-efficient meal options. Ready-to-prepare products such as flavored oatmeal cups, instant porridge, and breakfast sachets appeal to working professionals and younger consumers. Advanced processing preserves texture, taste, and nutrients, while fortification with protein, vitamins, and minerals enhances nutritional value. E-commerce, subscription grocery services, and portion-controlled packaging improve accessibility and recurring consumption. Innovation in flavors and single-serve packs supports engagement in both developed and emerging markets.

Form Insights

Flakes extracts are poised to dominate with a forecasted market share of over 38% in 2026, powered by widespread consumer familiarity, versatility in applications, and strong retail presence. Oat flakes, used in breakfast cereals, granola, muffins, and snack bars, offer adaptability across Western and emerging market diets. Preference for minimally processed foods, supported by clear labeling and nutritional transparency, reinforces adoption. Regulatory guidance from Food Safety and Standards Authority of India promotes whole grains, while established supply chains ensure cost efficiency and consistent quality.

The powder form is estimated to be the fastest-growing segment from 2026 to 2033, fueled by expanding use in functional foods, beverages, and nutraceutical formulations. Oat powder, incorporated into smoothies, protein shakes, infant formulas, and medical nutrition products, supports diverse health-focused applications. Demand rises for personalized nutrition and fortified dietary solutions, including gluten-free and high-protein variants. E-commerce platforms enable direct-to-consumer access, while fitness and wellness communities drive cultural acceptance. Advanced milling and processing improve solubility, texture, and nutrient retention, enhancing product performance and consumer appeal.

Regional Insights

North America Oats Market Trends

North America is expected to lead with an estimated 34% of the oats market share in 2026, supported by strong consumer preference for health-oriented and functional foods. Widespread awareness of dietary fiber benefits and cholesterol management drives consistent demand for rolled oats, instant oats, and oat-based beverages such as oat milk and flavored oatmeal cups. Well-established retail networks and online platforms ensure broad accessibility, while institutional food services incorporate oats into breakfast menus, snacks, and bakery products like granola bars and muffins. Advanced processing infrastructure enables high-quality production of value-added derivatives such as oat protein, fortified cereals, and gluten-free formulations, reinforcing adoption across diverse demographic segments.

Rising interest in preventive nutrition and plant-based diets further strengthens market dominance. Food manufacturers leverage product innovation, including flavored oatmeal, snack bars, and fortified oat powders, to meet evolving consumer expectations. Regulatory guidance supporting whole grain consumption and nutrient labeling promotes confidence in product benefits. Urbanization and dual-income household structures increase reliance on convenient, ready-to-prepare formats such as instant porridge sachets. Strategic distribution, combined with digital commerce expansion and subscription grocery models, enhances recurring consumption, while sustained investment in supply chain efficiency ensures competitive pricing and consistent quality across all product categories.

Europe Oats Market Trends

Europe demonstrates strong leadership in the oats market, supported by high consumer awareness of health and wellness trends, established food processing infrastructure, and well-developed retail networks. Consumers increasingly demand fiber-rich and functional foods to manage cholesterol, blood sugar, and digestive health, driving the adoption of rolled oats, instant oatmeal, and oat-based beverages. Traditional culinary integration, including breakfast cereals, porridge, and baked goods, reinforces steady consumption across households and institutional food services. Advanced milling and processing capabilities enable value-added products such as oat protein powders, gluten-free formulations, and fortified cereals, strengthening market relevance. Strong presence of multinational manufacturers ensures product quality, consistent supply, and diversified portfolios tailored to diverse consumer needs.

Shifts in lifestyle and dietary preferences further stimulate growth in convenience-oriented segments, including single-serve oatmeal cups, flavored granola bars, and ready-to-drink oat beverages. Urban populations with dual-income households rely on quick and nutritious meal solutions, while digital commerce expansion enhances accessibility and recurring consumption. Food labeling regulations promoting whole grain intake and nutritional transparency reinforce confidence in product benefits. Innovation in flavor profiles, packaging formats, and fortification strategies aligns with health-conscious and functional nutrition trends. Strategic partnerships with retailers, online platforms, and food service providers optimize distribution efficiency, ensuring competitive pricing and widespread market penetration across both mature and emerging consumer segments.

Asia Pacific Oats Market Trends

Asia Pacific is projected to be the fastest-growing market, stimulated by rapid urbanization, rising disposable incomes, and shifting consumer preferences toward health-oriented and plant-based nutrition. In China, demand for rolled oats, instant oatmeal, and fortified cereals rises as urban populations adopt fiber-rich diets to manage cholesterol and blood sugar. In India, dual-income households and time-constrained lifestyles drive consumption of ready-to-prepare oat porridge, flavored oatmeal cups, and granola bars. Expansion of organized retail chains, supermarkets, and digital commerce platforms enhances product accessibility, enabling recurring purchases and deepening market penetration across both metropolitan and semi-urban regions.

In Japan, traditional breakfast patterns shift toward functional foods, increasing the adoption of oat flakes, granola mixes, and fortified snack bars among working adults. South Korea shows rising preference for ready-to-drink oat beverages, protein-enriched powders, and portion-controlled oat snacks aligned with fitness and wellness trends. Flavor innovation, convenient packaging, and single-serve formats appeal to younger consumers. Investment in modern processing technologies ensures nutrient retention, consistent texture, and high-quality finished products, supporting demand across retail, e-commerce, and institutional food service channels.

Competitive Landscape

The global oats market demonstrates a moderately fragmented structure, with global corporations and regional producers competing across price points and product types. Key players, including PepsiCo, General Mills, and The Kellogg Company, maintain strong market presence through diversified product portfolios, extensive retail networks, and established brand recognition. Innovation in product formats, such as oat-based beverages, granola bars, and fortified cereals, strengthens competitive positioning and supports consistent consumer engagement across developed markets.

Quaker Oats Company, Oatly Group AB, and Bob’s Red Mill Natural Foods emphasize specialized offerings, including organic, plant-based, and functional oat products. These players leverage regional expertise, targeted marketing, and localized distribution strategies to capture emerging demand segments. Focus on cost-efficient production, flavor innovation, and convenience-driven formats enables penetration in price-sensitive and health-conscious consumer groups. Strategic collaborations and product differentiation maintain competitiveness and expand adoption in both retail and e-commerce channels.

Key Industry Developments:

- In March 2026, Oatly expanded its Barista Edition oat drinks with three new flavored varieties — coconut, vanilla, and caramel designed for creamy foamed coffees, matcha, smoothies, and other hot or cold beverages at major UK retailers.

- In January 2026, Kodiak launched a new line of protein-packed overnight oats in three flavors, offering 20 g of protein per serving with whole-grain oats, chia, flax, and quinoa for convenient, ready-ahead breakfast options at major retailers.

- In January 2026, Honey Bunches of Oats expanded its portfolio with a protein-focused cereal offering about 9 g of protein per serving in Cinnamon and Honey & Almond flavors, rolling out online and in stores to meet growing consumer demand for higher-protein oat-based breakfast options.

- In June 2025, Country Delight introduced a plant-based, lactose-free oats beverage made from Australian oats with no added sugar, preservatives, soy, or nuts to appeal to health-conscious and lactose-intolerant consumers via its app-based distribution.

Companies Covered in Oats Market

- PepsiCo Inc.

- General Mills Inc.

- The Kellogg Company

- Quaker Oats Company

- Oatly Group AB

- Bob’s Red Mill Natural Foods

- Weetabix Limited

- Archer Daniels Midland Company

- Nestlé S.A.

- Danone S.A.

- Vitasoy International Holdings

- Bob’s Red Mill Canada

- SunOpta Inc.

- Roland Foods

- Bob’s Red Mill Australia

Frequently Asked Questions

The oats market is projected to reach US$ 8.8 billion in 2026.

Rising health awareness, demand for fiber-rich and plant-based foods, and convenience-driven consumption drive the oats market.

The oats market is poised to witness a CAGR of 5.2% from 2026 to 2033.

Expansion in emerging economies, value-added product innovation, integration into functional and clinical nutrition, and e-commerce distribution present key market opportunities.

The key market players include PepsiCo, General Mills, The Kellogg Company, Quaker Oats Company, Oatly Group AB, and Bob’s Red Mill Natural Foods.