- Clothing, Footwear, & Accessories

- U.S. Costume Jewelry Market

U.S. Costume Jewelry Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. Costume Jewelry Market by Product Type (Necklace/Chain, Ring, Bracelet, Earring, Others), Distribution Channel (Online Retail, Specialty Jewelry Stores, Department Stores, Fashion & Lifestyle Stores, Direct‑to‑Consumer (Brand), Misc.), End User (Men, Women) and Regional Analysis for 2026 - 2033

U.S. Costume Jewelry Market Size and Trends Analysis

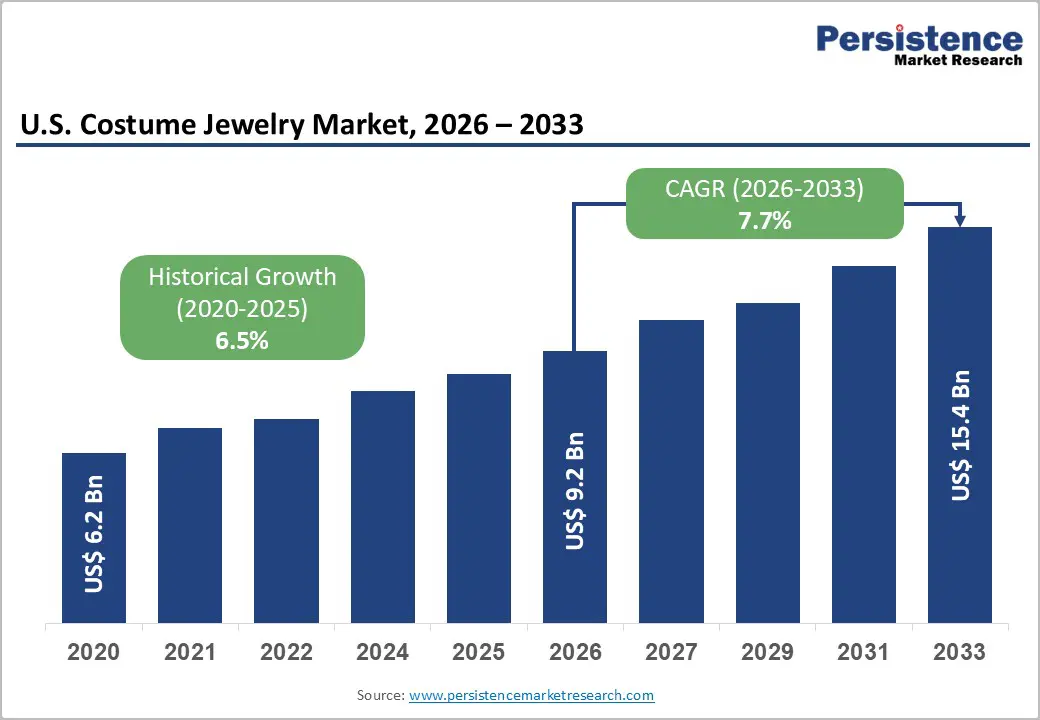

The U.S. Costume Jewelry Market size was valued at US$ 9.2 Billion in 2026 and is projected to reach US$ 15.4 Billion by 2033, growing at a CAGR of 7.7% between 2026 and 2033.Market expansion is driven by accelerating e-commerce channel adoption enabling virtual try-ons and price comparison transparency, Gen Z personalization demand establishing necklace layering and custom initial trends, and sustainable material innovation incorporating recycled metals and eco-friendly alternatives.

Necklace and chain products maintain market leadership through versatility supporting layering trend adoption, while earring segments demonstrate fastest growth driven by social media influencer styling and stackable design variations. The convergence of social commerce integration with TikTok and Instagram trend propagation, direct-to-consumer brand expansion bypassing traditional retail intermediation, and millennial-Gen Z conscious consumerism supporting ethical sourcing practices establishes sustained market momentum throughout the forecast period.

Key Industry Highlights:

- Leading Distribution Channel: Online retail channels command market leadership with 38.8% share, driven by extensive assortment breadth, competitive pricing transparency, and seamless mobile shopping experiences.

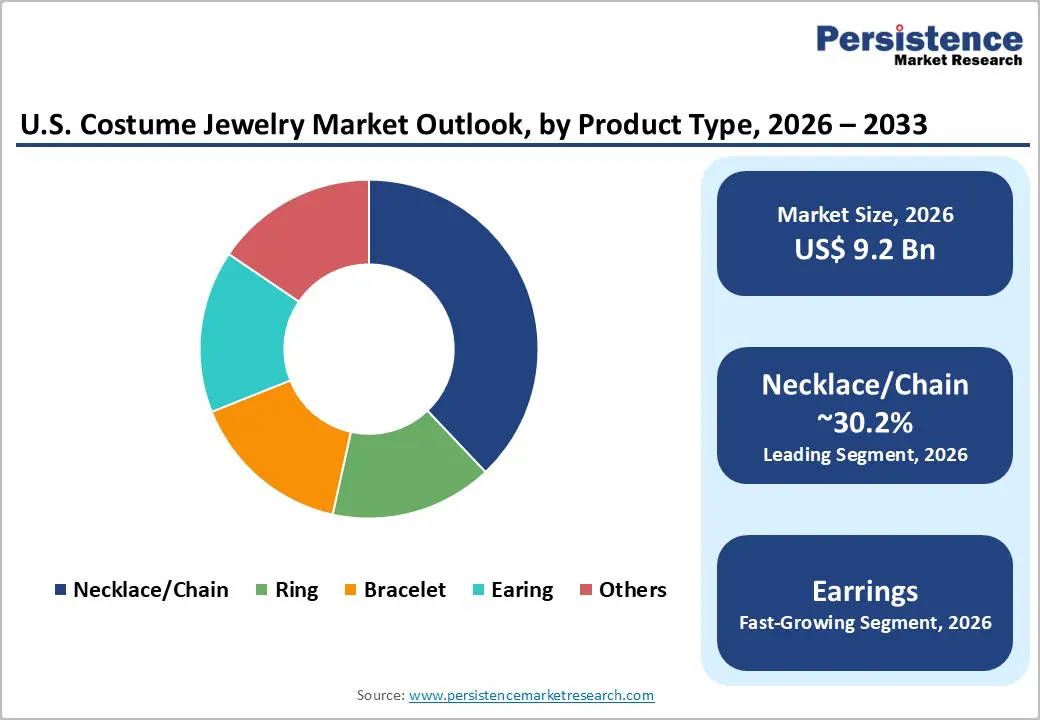

- Dominant Product Category: Necklace & chain products maintain the largest category share at 30.2%, supported by layering trends, personalized pendants, and high styling versatility across casual-to-occasion wear.

- Fastest-Growing Channel: Fashion & lifestyle retail stores represent the fastest-growing segment, enabled by experiential shopping formats, styling assistance, and physical try-on environments.

- Trend-Driven Demand: Market expansion is fueled by social-media-driven trend cycles, influencer styling adoption, and Gen Z personalization behavior supporting frequent non-occasion-based jewelry purchases.

- Emerging Market Opportunities: Sector opportunities are expanding through AR virtual try-on, metaverse commerce, AI personalization, direct-to-consumer models, and influence-owned jewelry lines.

| U.S. Market Attributes | Key Insights |

|---|---|

| U.S. Costume Jewelry Market Size (2026E) | US$ 9.2 Bn |

| Market Value Forecast (2033F) | US$ 15.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.5% |

Market Dynamics

Growth Drivers

E-commerce Channel Penetration and Digital Consumer Commerce Transformation

E-commerce platform maturation establishes fundamental catalyst for costume jewelry market accessibility, enabling consumers to evaluate extensive product selection, compare pricing across retailers, and execute transactions independent of geographic or temporal constraints. Online retail channels exemplify digital commerce channel dominance within costume jewelry distribution infrastructure.

Digital Commerce Applications Market benefits directly from e-commerce accessibility, as virtual try-on functionality and augmented reality capabilities reduce purchase uncertainty and lower cart abandonment rates.

Fashion, hobby, and leisure product categories establishing largest online transaction volumes reflect consumer preference for digital shopping modality. Credit card payment standardization including Mastercard dominance combined with digital wallet adoption including Apple Pay and PayPal establish payment infrastructure reliability supporting transaction completion. Online returns policies and customer ratings infrastructure enabling consumer confidence development supporting repeat purchase behavior. Mobile commerce accessibility enabling smartphone-based jewelry discovery and purchasing supporting shopping convenience.

Social Media Influencer Trend Propagation and Gen Z Personalization Adoption

Social media platforms establishing primary jewelry discovery and styling influence channels for Gen Z and millennial demographics, with viral styling content on TikTok and Instagram demonstrating immediate trend adoption acceleration. Influencer-driven costume jewelry recommendations generating immediate consumer purchasing response establishing commercial viability of social commerce channels. Micro-influencer ecosystem development enabling niche market targeting and authenticity-driven community engagement supporting brand loyalty formation.

The Market benefits directly from social media trend acceleration, with layered necklace and stacked ring styling generating immediate demand surges following influencer content deployment. Personalized jewelry including name necklaces, initial rings, and custom birthstone pieces establishing identity-driven consumer purchasing motivation supporting differentiation from commodity jewelry alternatives.

Gen Z preference for jewelry enabling self-expression rather than occasion-specific wear establishing everyday purchase behavior supporting market volume expansion. Fashion shows and celebrity endorsement influence establishing trend legitimacy with younger demographics. TikTok #jewelrytok hashtag engagement demonstrating community-driven trend discovery and styling education supporting organic market awareness development. Dopamine dressing wave incorporating bright colorful jewelry establishing joyful aesthetic adoption among Gen Z consumers.

Sustainable Material Innovation and Eco-Conscious Consumer Values Alignment

Eco-friendly costume jewelry development incorporating recycled metals, ethically sourced stones, and natural materials addressing Gen Z environmental consciousness and responsible consumption values. Coach Jewels launch featuring recycled material necklaces, earrings, and bracelets exemplifies major brand sustainability commitment supporting market credibility.

BaubleBar sustainability initiative ensuring ethical and sustainable practices across costume jewelry production by 2025 exemplifies industry-wide sustainable practice standardization. The Costume Jewelry Market demonstrates substantial growth opportunity through sustainable product differentiation, as conscious consumerism establishes premium pricing tolerance for environmentally responsible alternatives. Glass and crystal jewelry segments supported by technological advancement in faceting processes replicating natural gemstone properties. Swarovski synthetic-diamond revenue doubling demonstrating market acceptance of laboratory-engineered alternatives to mined gemstones.

H&M and Zara plastic, acrylic, and resin material integration optimizing production cycles while meeting sustainability objectives. Wolf Circus and SOKO recycled wood and bio-based polymer adoption establishing innovative material source supporting environmental credentials. Nickel-free, hypoallergenic material adoption addressing health-conscious consumer preferences establishing material quality differentiation. Circular economy positioning through jewelry recycling programs and upcycled design development establishing sustainability infrastructure development.

Market Restraining Factors

Supply Chain Complexity and Quality Control Standardization

Costume jewelry manufacturing supply chain fragmentation across Asia-Pacific production centers creates logistical complexity and quality consistency challenges affecting brand reputation and consumer satisfaction. Material sourcing variability including inconsistent metal plating durability and stone adhesion reliability establishing product durability concerns limiting repeat purchase propensity. Labor cost pressures in manufacturing centers creating competitive pricing pressure constraining margin expansion opportunity. Intellectual property protection challenges in costume jewelry market addressing design imitation concerns and counterfeit product proliferation.

Regulatory Compliance and Hazardous Material Restrictions

Heavy metal content restrictions including nickel and lead regulations across federal and state jurisdictions establishing compliance complexity and production process modification requirements. Product liability concerns allergic reactions and skin irritation from costume jewelry materials establishing manufacturer risk exposure. Sustainability compliance requirements including packaging waste reduction mandates creating operational cost increases. Environmental regulations restrict certain manufacturing processes and material disposal methodologies complicating production logistics.

Key Market Opportunities

Augmented Reality Virtual Try-On Integration and Technology-Enabled Shopping Experience

Augmented reality virtual fitting technologies enabling consumers to visualize jewelry appearance on personal wearable form factors before purchase, reducing return rates and increasing consumer confidence in online purchasing decisions. Virtual try-on capability deployment across e-commerce platforms enabling real-time personalization and customization visualization supporting purchase conversion rate optimization. The Costume Jewelry Market benefits from technology integration enabling immersive shopping experiences addressing traditional retail touchpoint loss from digital commerce expansion.

Metaverse commerce integration opportunity addressing immersive virtual shopping environment development within gaming and virtual social platforms enabling innovative jewelry merchandise presentation. 3D printing capability enabling limited collection development and rapid design iteration supporting trend responsiveness. AI-based customization systems automating personalization recommendations aligned with individual consumer preferences and historical purchase behavior. Voice-assisted shopping technology deployment supporting accessibility enhancement and emerging interface modality adoption. Blockchain-based authentication establishing counterfeit prevention and supply chain transparency supporting consumer confidence development.

Direct-to-Consumer Brand Model and Influencer-Owned Jewelry Lines

Direct-to-consumer brand strategy implementation enabling costume jewelry manufacturers to bypass traditional retail intermediation supporting margin optimization and consumer relationship establishment. Influencer-owned costume jewelry line development leveraging established social media following enabling rapid market penetration and trendsetting capability. PacSun PS Community Hub shoppable platform integrating social engagement, creator monetization, and immersive commerce exemplifies influencer-led commerce model innovation.

Celebrity and designer collaborations with costume jewelry brands establishing premium positioning and aspirational brand perception supporting premium pricing justification. Subscription-based jewelry delivery models establishing recurring revenue streams and consumer loyalty development through curated monthly selections. Direct brand-to-consumer digital commerce enabling extensive product customization and bespoke jewelry offering supporting millennial and Gen Z consumer demand for personalization. Franchise and licensing model expansion enabling independent retailers to participate in branded costume jewelry distribution supporting geographic market penetration.

Category-wise Analysis

Product Type Insights

Necklace and chain products maintain dominant market share around 30.2% through versatility supporting layering trend adoption enabling multiple concurrent necklaces wearing, gift-giving popularity supporting significant volume of fashion jewelry purchases, and style diversity spanning minimalist chains to statement pendant pieces. Layering necklaces establishing primary styling trend among Gen Z consumers supporting repeated purchase behavior for collection building. Pendant necklace functionality supporting personalization through custom charm and initial attachment enabling identity-driven consumer connection. Chain length variability supporting compatibility with diverse neckline and garment types enabling versatile styling capability.

Costume Jewelry Market dominance reflects consumer preference for necklace category enabling frequent style transformation through accessory substitution. Fashion influencer necklace styling establishing immediate trend adoption acceleration on social platforms.

Earring products demonstrate accelerating adoption momentum driven by stackable and mixed-metal design capability enabling individualized layering expressions, ear-piercing accessibility supporting broader demographic participation than other jewelry categories, and social media trend propagation through close-up styling shots establishing influencer credibility. Ear piercing prevalence among Gen Z and millennial demographics establishing large potential consumer base supporting volume expansion. Multiple ear-piercing accommodation enabling stacked earring configuration supporting statement-making accessory expressions. Statement earring functionality supporting individual personality projection and mood-driven accessory selection. Earring cost accessibility relative to necklace and bracelet alternatives supporting discretionary purchase frequency. Social media close-up photography enabling detailed earring aesthetic showcase supporting influencer trend establishment.

End Use Industry Insights

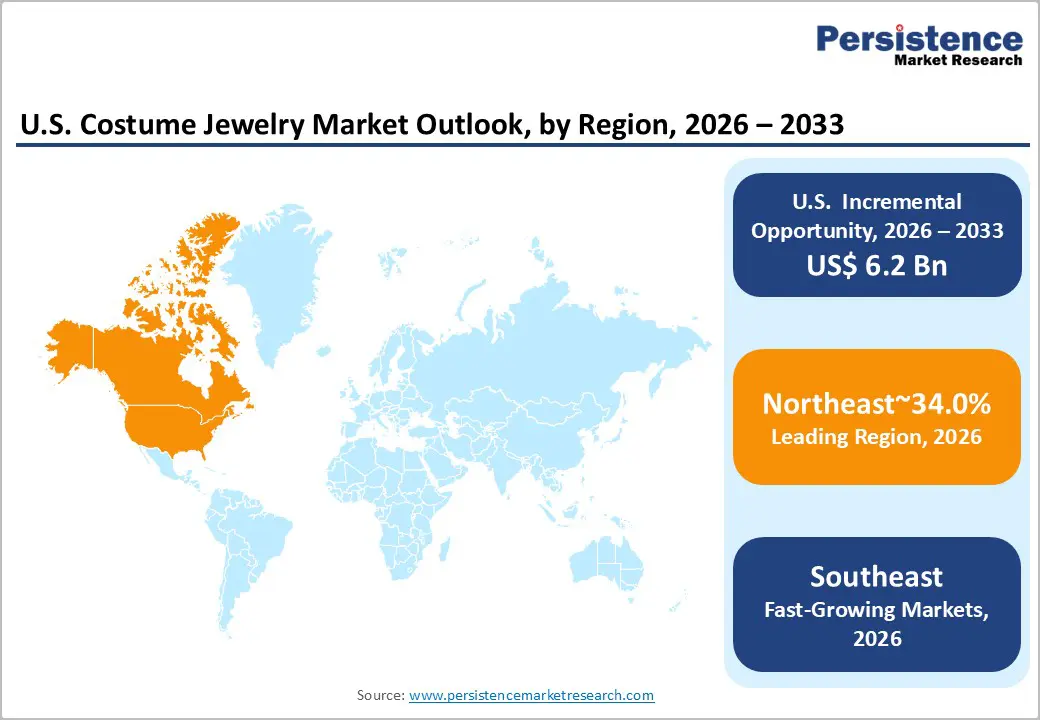

Online retail channels command market leadership through share of 38.8% through extensive product assortment enabling consumer choice maximization, price transparency supporting competitive comparison capability, and delivery convenience enabling home-based shopping accessibility. E-commerce platform standardization reducing merchant technology barriers supporting SME participation in online jewelry retail. Payment flexibility enabling digital wallet, credit card, and installment purchasing options supporting consumer payment convenience. Customer review infrastructure enabling social proof establishment and purchase decision confidence development. Virtual try-on capability reducing purchase uncertainty and supporting higher transaction completion rates. Subscription and membership program integration enabling customer loyalty development and repeat purchase behavior standardization. Mobile commerce optimization supports smartphone-based shopping convenience and impulse purchasing behavior.

Fashion and lifestyle retail establishments demonstrate fastest adoption momentum driven by experiential retail environment enabling hands-on product evaluation and physical try-on capability, fashion brand integrated positioning supporting costume jewelry as core fashion accessory category, and trained sales associate expertise enabling personalized customer styling recommendations.

Competitive Landscape

The U.S. costume jewelry market is fragmented with a consolidated core, where a few leading brands hold significant influence while numerous smaller players compete on design and price. Key players such as Swarovski, Pandora, Guess, Michael Kors, Kate Spade, and BaubleBar dominate through strong brand recognition and extensive retail and e commerce presence. These top brands shape trends and capture premium consumers, while emerging designers and direct to-consumer labels drive innovation and cater to younger, trend-driven buyers. Retail chains like Claire’s face pressure from shifting consumer preferences toward online and influence-driven sales, intensifying competition. While the market has many competitors, the leading brands form a core that impacts pricing, trends, and consumer loyalty.

Key Industry Developments

- On January 9, 2026, Pacsun launched its PS Community Hub, a first-to-market digital platform integrating social engagement, creator collaboration, and shoppable experiences. The platform enables users to co-create fashion and lifestyle products, including costume jewelry, while leveraging AI for personalization, content moderation, and analytics, marking a significant innovation in how jewelry and fashion brands connect with Gen Z and Gen Alpha consumers.

- On December 31, 2024, Swarovski AG reported strong growth in its jewelry category in the United States, with sales of Swarovski Created (lab-grown) Diamonds more than doubling year-over-year. The company introduced its “Eternity” collection globally, highlighting the rising popularity of lab-grown diamonds in fashion and costume jewelry. This performance reflects growing consumer demand for contemporary, accessible luxury jewelry and Swarovski’s success in combining heritage brand appeal with modern, pop-culture collaborations like the “Swarovski x Ariana Grande” capsule collection, strengthening its presence in the U.S. costume jewelry market.

Companies Covered in U.S. Costume Jewelry Market

- Swarovski AG

- Chanel S.A.

- LVMH Moët Hennessy Louis Vuitton SE

- Guess, Inc.

- Gianni Versace S.p.A.

- Pandora A/S

- Alex and Ani, LLC

- Hermès International S.A.

- Hennes & Mauritz AB (H&M)

- Industria de Diseño Textil, S.A. (ZARA)

- Gucci S.p.A. (Kering Group)

- Claire’s Stores, Inc.

- BaubleBar Inc.

- Charming Charlie, Inc.

- Buckley London Ltd.

Frequently Asked Questions

The U.S. Costume Jewelry Market is projected to be valued at US$ 9.2 Bn in 2026.

The Necklace/Chain segment is expected to account for approximately 30.2% of the U.S. Costume Jewelry Market by Product Type in 2026.

The market is expected to witness a CAGR of 7.7% from 2026 to 2033.

The U.S. Costume Jewelry market growth is driven by rising e-commerce penetration, social-media-led trend adoption among Gen Z, and increasing demand for sustainable, affordable, and personalized fashion jewelry.

Key market opportunities in the U.S. Costume Jewelry Market include AR/virtual try-on and tech-enabled shopping, metaverse and AI personalization, direct-to-consumer brand expansion, and influencer/celebrity-driven jewelry lines.

Key players in the U.S. Costume Jewelry Market include Swarovski AG, Pandora A/S, Claire’s Stores, Inc., BaubleBar Inc., Guess, Inc., and Alex and Ani, LLC.