- Clothing, Footwear, & Accessories

- Shoe Care Market

Shoe Care Market Size, Share, and Growth Forecast 2026 – 2033

Shoe Care Market by Product Type (Shoe Polish, Shoe Cleaners, Shoe Creams & Conditioners, Waterproofing Sprays, Deodorizers & Fresheners, Brushes & Accessories, Shoe Protection Sprays, Others), Material Type (Leather Footwear Care, Suede & Nubuck Footwear Care, Synthetic Footwear Care, Canvas Footwear Care, Sports & Sneaker Care), Application, Distribution Channel, and Regional Analysis for 2026–2033

Shoe Care Market Size and Trend Analysis

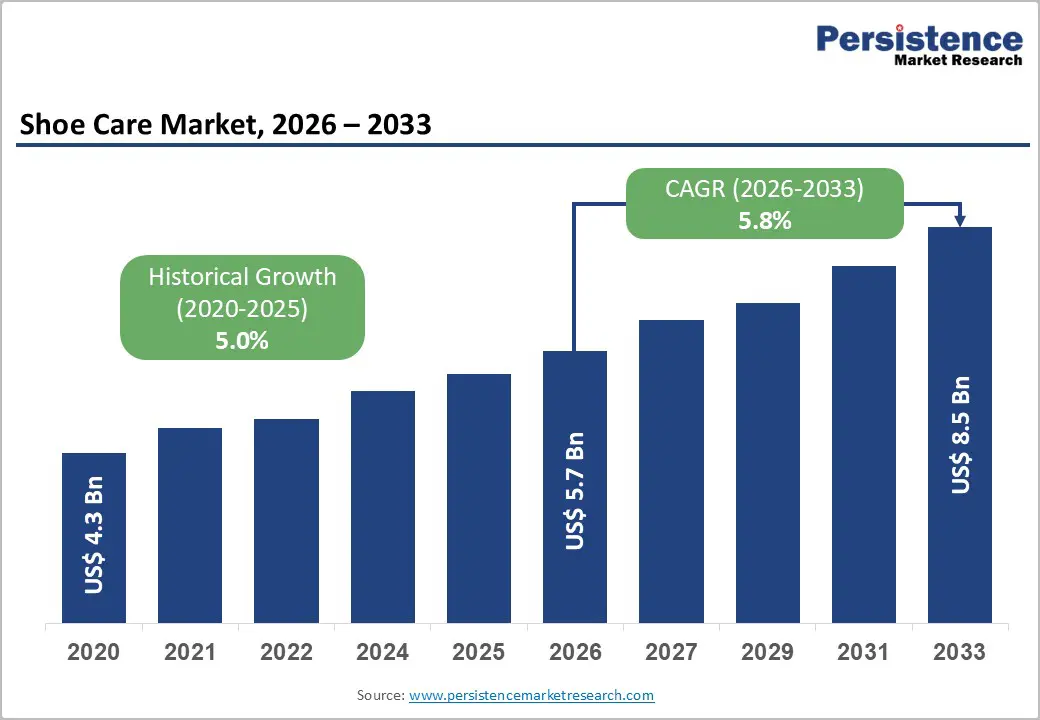

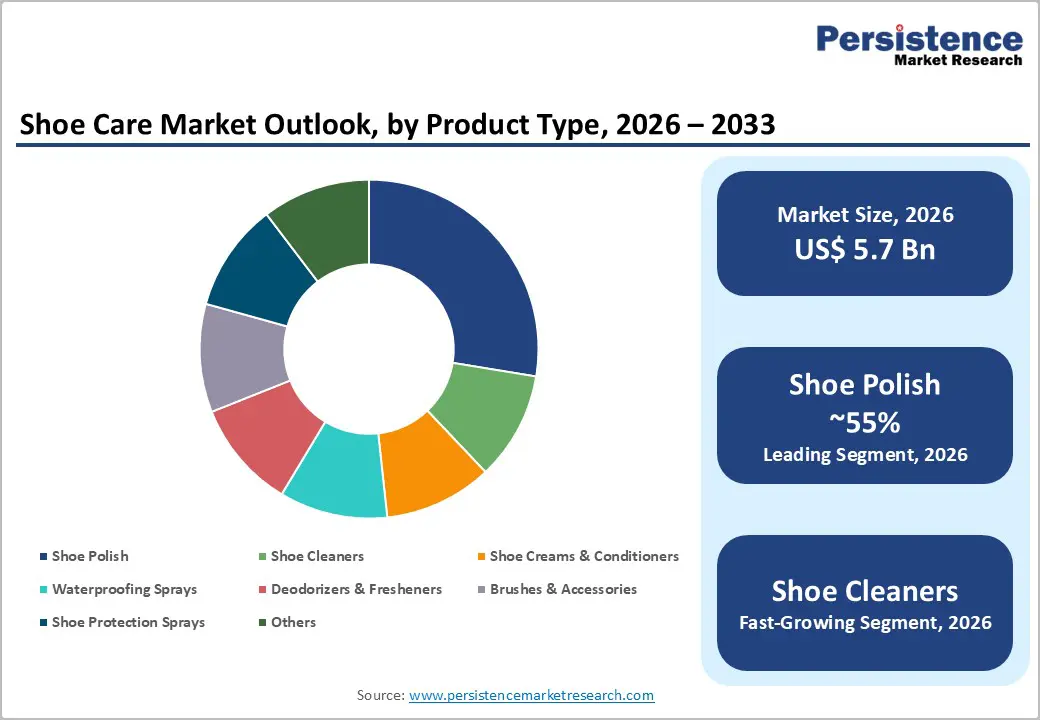

The global shoe care market size is likely to be valued at US$ 5.7 Bn in 2026 and is projected to reach US$ 8.5 Bn by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

This consistent expansion is driven by rising global footwear consumption, premiumization trends in luxury and athleisure footwear categories that require specialized care products, and the rapid growth of sneaker culture, which is compelling consumers to invest in dedicated sneaker cleaning and protection solutions. The World Footwear Yearbook estimates global footwear production exceeds 23 billion pairs annually, creating a structurally large installed base of footwear that requires ongoing care. Simultaneously, growing e-commerce penetration is broadening consumer access to specialty shoe-care brands beyond traditional retail formats, thereby expanding the addressable market globally.

Key Industry Highlights:

- Sneaker Culture Boom: Expanding sneaker resale markets and collector culture are significantly boosting demand for sneaker cleaning kits, protective sprays, and specialty care products, with mint-condition sneakers commanding 30–50% higher resale values globally.

- Luxury Care Demand: Rising luxury footwear purchases across Europe, North America, and the Asia Pacific are accelerating demand for premium leather conditioners, waxes, creams, and waterproofing solutions, benefiting heritage shoe care brands globally.

- Eco-Formulation Opportunity: Sustainable shoe care products, including biodegradable, PFAS-free, and water-based formulations, are emerging as major opportunities due to tightening environmental regulations and increasing consumer preference for eco-friendly products.

- Shoe Polish Leadership: Shoe polish is likely to dominate the product category with approximately 28% share in 2026, driven by military usage, workplace formalwear culture, and consistent household demand across developed economies.

- Sneaker Care Acceleration: Sports and sneaker care products are projected to expand at an estimated 8.5% CAGR supported by growing sneaker ownership, athleisure trends, and footwear resale value protection.

- Leather Care Dominance: Leather footwear care is expected to lead the material segment with approximately 38% share in 2026, driven by premium leather footwear requiring regular polishing, conditioning, waterproofing, and specialized maintenance routines.

- Online Retail Growth: Online retail and e-commerce distribution channels are expected to grow at a 10.2% CAGR, supported by Amazon, Tmall, and direct-to-consumer subscription models expanding global brand accessibility.

- Asia Pacific Momentum: Asia Pacific represents the fastest-growing regional market with an estimated 7.2% CAGR, fueled by rising middle-class footwear consumption, expanding sneaker culture, and strong e-commerce growth across emerging economies.

Market Dynamics

Drivers - Sneaker Culture Explosion and Rising Consumer Investment in Footwear Maintenance

The global sneaker market has grown into a multi-hundred-billion-dollar industry, fundamentally reshaping consumer attitudes toward footwear care. The NPD Group estimates the U.S. athletic footwear market alone exceeds US$ 20 billion in annual retail sales, with limited-edition and collector sneakers often retailing at multiples of their original price. This collector mindset has created a dedicated, high-spend consumer cohort that invests heavily in sneaker cleaning kits, protective sprays, and specialty deodorizers to preserve both the aesthetic and resale value of their footwear.

Stadium Goods and StockX have documented that sneakers in mint condition command 30–50% premiums on the secondary market versus worn pairs, directly incentivizing expenditure on dedicated sneaker care product lines. Brands such as Jason Markk, Crep Protect, and Sneaker Lab have built multi-million-dollar businesses entirely around this high-engagement sneaker care consumer segment.

Premiumization of Luxury Footwear and Growing Demand for Professional-Grade Leather Care

Global luxury footwear sales have expanded consistently, driven by growing high-net-worth populations in Asia Pacific, the Middle East, and North America. Consumers investing US$ 500–5,000+ in luxury leather shoes from Church's, Allen Edmonds, or John Lobb are highly motivated to purchase premium leather care products creams, conditioners, wax polishes, and waterproofing treatments to protect their investment. This premiumization effect is directly driving demand for heritage shoe care brands such as Saphir Médaille d'Or, Collonil, and Burgol, which command significant price premiums over mass-market alternatives and are expanding their direct-to-consumer and specialty retail distribution globally.

Restraints - Availability of Low-Cost Unbranded Substitutes in Price-Sensitive Markets

In price-sensitive emerging markets across South Asia, Southeast Asia, and Sub-Saharan Africa, unbranded and generic shoe care products including loose shoe polish and home-formulated cleaners dominate at price points 70–80% below branded alternatives. The World Footwear Yearbook notes that footwear consumption is highest in these regions by volume, yet average shoe care spend per capita remains extremely low. This structural price sensitivity limits branded shoe care companies' ability to penetrate high-volume but low-value markets without significant downward pricing pressure that compresses margins.

Environmental Regulatory Pressure on Solvent-Based Polishes and Aerosol Sprays

Traditional shoe polishes and waterproofing sprays frequently contain volatile organic compounds (VOCs), petroleum distillates, and fluorocarbon-based repellents that are subject to increasing regulatory restrictions. The European Chemicals Agency (ECHA) and the U.S. Environmental Protection Agency (EPA) have tightened permissible VOC content limits in aerosol consumer products. PFAS-based waterproofing agents widely used in shoe protection sprays are under phased restriction across the EU REACH framework, compelling reformulation investments that increase R&D costs and require re-registration of modified products, acting as a near-term margin and timeline burden for incumbent shoe care manufacturers.

Opportunities - Eco-Friendly and Bio-Based Shoe Care Formulations Addressing Sustainability Demand

Consumer and regulatory demand for sustainable personal care formulations is creating a compelling opportunity for shoe care brands to develop and commercialize bio-based, PFAS-free, and biodegradable product lines. The European Commission's Chemicals Strategy for Sustainability is driving the phase-out of PFAS waterproofing agents by 2025 in many product categories, forcing reformulation while simultaneously rewarding first-movers with eco-credentials that command premium retail pricing.

Brands such as Nikwax whose entire product range is water-based and fluorocarbon-free have demonstrated that sustainability positioning can be a powerful commercial differentiator. As Gen Z and Millennial consumers, who account for over 45% of global footwear purchases per Euromonitor International, increasingly prioritize sustainable product choices, shoe care companies with credible eco-formulation portfolios are positioned to capture disproportionate share in premium retail channels and e-commerce.

E-Commerce Expansion and Direct-to-Consumer Subscription Models for Shoe Care

Online retail is fundamentally changing shoe care product distribution economics, enabling specialist and niche brands to reach global consumers without brick-and-mortar infrastructure. The OECD has documented that global e-commerce penetration for household care products grew from 12% in 2019 to over 22% by 2023.

Platforms including Amazon, Tmall, and Shopee have enabled brands like Jason Markk and Sneaker Lab to grow from domestic to global presences within five years. Emerging subscription box models such as monthly sneaker care kits are generating recurring revenue and improving customer lifetime value for digitally native shoe care brands. The Direct Selling Association (DSA) notes that subscription personal care models retain consumers at 3–4x the rate of single-purchase transaction models, making DTC subscription a strategically attractive growth model for shoe care participants.

Category-wise Insights

Product Type Analysis

Shoe polish holds the dominant position in the product type category, accounting for approximately 28% of the global shoe care market revenue in 2026. Shoe polish's market leadership reflects its century-long utility as the foundational footwear maintenance product used across formal, dress, and leather boots worldwide, combined with the broad price accessibility of mass-market polishes from brands such as Kiwi (SC Johnson) and Lincoln. In mature markets, including the U.K., Germany, and the United States, shoe polish remains a household staple driven by workplace dress code norms and military uniform standards.

The British Army and U.S. Marine Corps, for example, mandate high-gloss leather boot maintenance, creating institutionally consistent demand. Heritage luxury polish brands, including Saphir Médaille d'Or and Tarrago, command premium price points in the specialty footwear care segment, reinforcing the category's revenue leadership.

Sports & Sneaker Care product lines spanning specialist cleaning foams, microfiber applicator kits, and UV whitening solutions represent the fastest-growing product sub-segment, advancing at an estimated CAGR of 8.5% through 2033, well above the market average. The global sneaker resale market's expansion, tracked by StockX and GOAT, is the primary demand catalyst, with collectors investing aggressively in cleaning and preservation to protect resale value.

Material Type Insights

Leather footwear care is likely to be the leading material type segment, commanding approximately 38% of global shoe care revenue in 2026. Leather care's dominant position stems from leather remaining the premium footwear material of choice across formal, luxury, and high-quality casual shoe categories, all of which require regular conditioning, polishing, and waterproofing to maintain appearance and structural integrity. According to the Leather Panel industry group, global leather footwear production accounts for approximately 35–40% of all footwear by value despite constituting a smaller share by volume, reflecting leather's premium pricing. The comprehensive care routine required for leather footwear cleaner, conditioner, polish, and waterproofer generates higher per-unit revenue than synthetic or canvas footwear care, which typically requires only a single cleaning product.

Sports & sneaker care (as a material category encompassing multi-material mesh, knit, and rubber sneakers) is the fastest-growing material segment at an estimated CAGR of 9.0%. The Global Athletic Footwear Market is expanding at mid-single-digit rates annually directly feeds this segment's trajectory, as each new pair of performance or lifestyle sneakers represents an ongoing care product consumption opportunity.

Application Insights

Formal shoes is the leading Application segment, representing approximately 32% of global shoe care market revenue in 2025. Formal footwear care commands the highest per-unit product expenditure, as dress shoe owners invest in comprehensive care routines including welt cleaning, sole conditioning, upper polishing, and storage with cedar shoe trees that involve multiple product SKUs per pair maintained. The persistent global market for men's dress shoes and women's formal pumps sustained by professional workplace norms in financial, legal, and government sectors across North America, Europe, and Asia provides structural demand stability. Corporate return-to-office trends post-pandemic have additionally revived demand for formal shoe care products after a temporary COVID-era dip.

Luxury Footwear care is the fastest-growing application segment, expanding at an estimated CAGR of 7.5% through 2033. Consumers purchasing Hermès, Berluti, and Ferragamo footwear are increasingly purchasing specialist care kits either bundled with the shoe or from premium shoe care retailers, driving above-market revenue growth in this high-margin segment.

Distribution Channel Insights

Supermarkets & hypermarkets hold the leading position in the distribution channel category, accounting for approximately 35% of global sales in 2026. Mass-market retailers, including Walmart, Carrefour, and Tesco provide unrivaled reach for high-volume, everyday shoe care brands such as Kiwi and Meltonian, leveraging high foot traffic and impulse purchase placement near footwear sections or seasonal displays. The channel's dominance is reinforced by private-label shoe care product development by major retailers, who can offer lower-priced alternatives that sustain category volumes while pressuring branded product margins. For mass-market shoe polish, cleaners, and deodorizers, supermarket placement remains the highest-volume path to consumers.

Online retail/e-commerce is the fast-growing distribution channel, expanding at an estimated CAGR of 10.2%, nearly double the overall market CAGR. Amazon, Tmall, and dedicated sneaker care platforms are enabling specialty brands to bypass traditional retail entirely, reaching global consumers with premium and niche shoe care products that would struggle to secure mainstream shelf space.

Regional Insights

North America Shoe Care Market Trends

North America is the second-largest shoe care market, accounting for approximately 28% of global revenue in 2026. The United States drives the vast majority of regional demand, underpinned by a deeply ingrained sneaker culture, high athletic footwear consumption, and growing professional re-entry trends that have revived formal shoe care product demand. The American Apparel & Footwear Association (AAFA) estimates U.S. consumers purchase over 3 billion pairs of footwear annually, creating one of the world's largest installed bases of footwear requiring ongoing care.

The North American market is also a hotbed of sneaker care product innovation, with brands such as Jason Markk (Los Angeles) and Reshoevn8r building significant DTC businesses around digitally native shoe care subscription and kit models. E-commerce penetration for shoe care in the U.S. exceeds 30% of category sales per AAFA estimates, among the highest globally, enabling specialty brands to scale rapidly through Amazon and Shopify storefronts.

U.S. Shoe Care Market: World's Largest Sneaker Culture Driving Premium Care Demand

The United States is the single largest national shoe care market, accounting for approximately 24% of global revenue in 2026 and growing at an estimated CAGR of 5.5% through 2033. The U.S. market's importance stems from its world-leading position in athletic footwear consumption. Americans spend more per capita on shoes than any other major economy, and from the high engagement of U.S. sneaker collectors who invest disproportionately in care products to preserve resale value on limited-edition footwear. Additionally, the U.S. military's strict boot-maintenance requirements across all service branches create a stable, recurring government-adjacent demand channel for shoe polish and leather care products.

Europe Shoe Care Market Trends

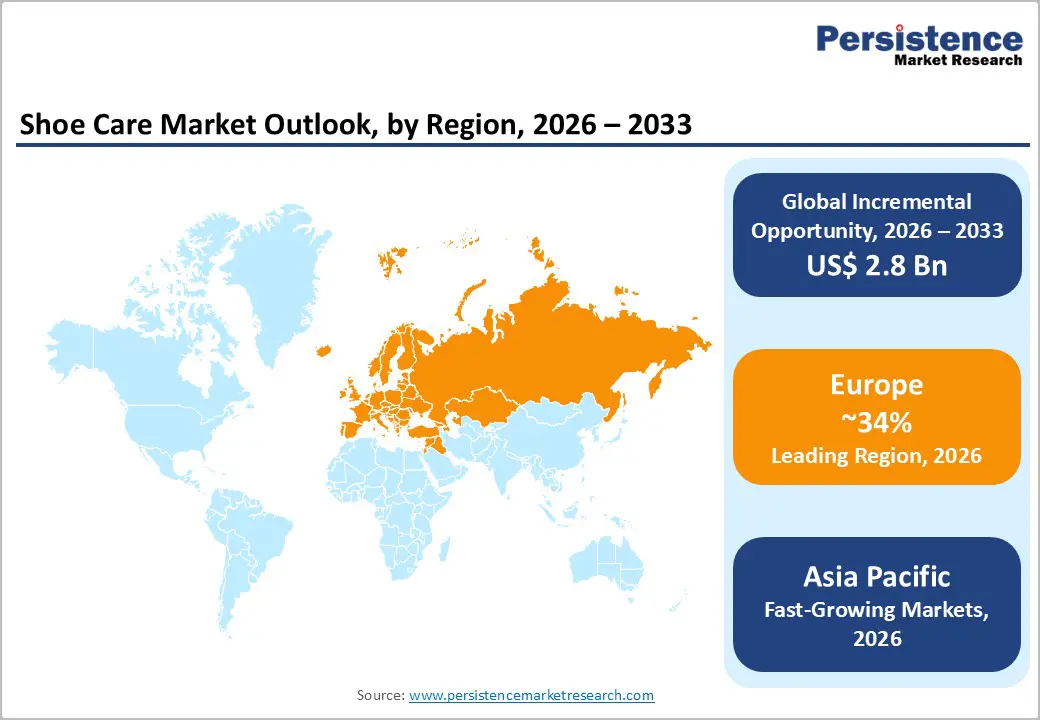

Europe is the world's leading shoe care market, commanding approximately 34% of global revenue in 2026, reflecting the continent's deep heritage in quality leather craftsmanship, high per-capita expenditure on premium footwear, and strong consumer awareness of footwear maintenance. Countries including Germany, Italy, France, and the U.K. are home to the world's most sophisticated shoe care consumers, who regularly invest in specialist polishes, conditioners, and brushes rather than mass-market alternatives.

Regulatory harmonization under EU REACH and the European Commission's Chemicals Strategy for Sustainability is reshaping product formulations across the European shoe care market, phasing out PFAS waterproofing agents and VOC-heavy polishes. This is creating a first-mover advantage for European eco-formulation specialists such as Collonil and Nikwax, whose reformulated water-based ranges are growing rapidly in premium retail channels including Globetrotter and Cotswold Outdoor.

Germany: Leading European Shoe Care Hub with Premium Leather Care Heritage

Germany is the largest shoe care market, accounting for approximately 20% of European market revenue in 2026 and growing at an estimated CAGR of 5.2% through 2033. Germany's dominant position reflects its status as a major leather footwear producer and consumer, with heritage shoe care brands including Collonil and Salzenbrodt headquartered domestically.

The German consumer's well-documented preference for quality and durability expressed through consistent investment in shoe care products to extend footwear lifespan sustains high per-capita shoe care spend. Germany's robust outdoor and hiking footwear culture additionally drives demand for waterproofing sprays and boot conditioners, segments that command premium pricing and above-average margin profiles.

U.K.: Brogue and Boot Culture Sustaining Premium Polish and Conditioner Demand

The United Kingdom accounts for approximately 14% of European shoe care market revenue in 2026, growing at an estimated CAGR of 4.8% through 2033. The U.K.'s shoe care market is characterized by strong demand for traditional leather shoe polish, driven by the country's heritage footwear culture centered on Northampton-made brogues, Oxfords, and Chelsea boots and by military boot-maintenance traditions. Kiwi remains the market-leading mass brand, while Saphir and Burgol serve the premium segment. Growing sneaker culture in U.K. urban centers is driving demand for specialist sneaker care kits, with Crep Protect, a U.K.-founded brand benefiting directly from this trend.

France: Luxury Footwear Capital Powering Premium Shoe Care Product Premiumization

France accounts for approximately 12% of European shoe care revenue in 2026, expanding at an estimated CAGR of 5.0% through 2033. France's market is disproportionately premium home to Saphir Médaille d'Or, the world's most prestigious shoe care brand, manufactured in Toulouse and distributed globally through specialty retailers. French consumer culture prizes chaussures bien entretenues (well-maintained shoes) as an expression of elegance, sustaining elevated per-unit shoe care expenditure relative to European peers. Paris's luxury retail ecosystem, including the Galeries Lafayette and Le Bon Marché department stores serves as a premium distribution channel for specialty shoe care products across the country's affluent consumer base.

Italy: Artisan Leather Footwear Manufacturing Driving Specialist Care Innovation

Italy holds approximately 11% of European shoe care market revenue in 2026, growing at an estimated CAGR of 4.6%. Italy's unique position as the world's premium leather footwear manufacturing capital, with regions including Marche, Tuscany, and Veneto producing footwear for Gucci, Prada, Ferragamo, and Tod's, creates domestic demand for premium leather care formulations. Italian brands, including Tarrago (distributed widely in Italy) and specialty cobblers' product ranges serve a discerning consumer base accustomed to professional-quality shoe care standards.

Asia Pacific Shoe Care Market Trends

Asia Pacific is the fastest-growing shoe care market, expanding at an estimated CAGR of 7.2%, driven by rapidly rising middle-class footwear consumption, the explosive growth of sneaker culture among young urban consumers in China, South Korea, and Japan, and the region's vast manufacturing infrastructure that supports both domestic consumption and export-oriented production. China's role as both the world's largest footwear producer (over 12 billion pairs annually per World Footwear Yearbook) and a rapidly premiumizing consumer market makes it the central growth engine for Asia Pacific shoe care demand.

The ASEAN region, particularly Vietnam, Indonesia, and Thailand is experiencing rapid footwear consumption growth correlated with urbanization and rising disposable incomes, creating new markets for mass to mid-premium shoe care brands entering the region through modern retail and e-commerce channels. Japanese consumers maintain among the world's highest per-capita shoe care expenditure, reflecting the country's culture of meticulously maintained footwear as a social signal.

China: World's Largest Footwear Producer Spawning Massive Shoe Care Consumption

China is the largest shoe care market in Asia Pacific, accounting for approximately 38% of regional revenue in 2026 and growing at an estimated CAGR of 8.0% through 2033. China's dual role as the world's largest footwear manufacturer and its largest national footwear consumer market creates enormous structural shoe care demand. Domestic sneaker culture, particularly among Generation Z consumers in tier-1 cities, has driven rapid adoption of premium sneaker care brands, with platforms including Tmall and Douyin (TikTok China) enabling specialist brands to reach mass audiences through content-driven commerce. International brands, including Crep Protect and Sneaker Lab, have established significant presences in China's online shoe care market, competing with emerging domestic brands offering locally adapted formulations.

India: Fastest-Growing Shoe Care Market Fueled by Rising Footwear Aspirations

India accounts for approximately 10% of the Asia Pacific's shoe care market revenue in 2026, growing at one of the region's fastest rates at an estimated CAGR of 9.5% through 2033. India's shoe care market is at an early stage of organized branded product adoption, historically dominated by unbranded roadside shoe polish services, but is transitioning rapidly as e-commerce penetration (driven by Flipkart and Amazon India) brings premium shoe care products to aspirational middle-class consumers nationwide. Growing youth sneaker culture in metropolitan cities, rising formal office wear adoption post-pandemic, and expanding modern retail formats across tier-2 cities are collectively elevating Indian consumers' awareness of and willingness to pay for branded shoe care solutions.

South Korea: K-Fashion Influence Accelerating Premium Sneaker Care Market Growth

South Korea accounts for approximately 7% of Asia Pacific's shoe care market revenue in 2026. South Korea's outsized cultural influence through K-pop and K-fashion has made footwear aesthetics a high-priority consumer category, with Korean consumers, particularly youth demographics, investing significantly in sneaker cleaning kits, whiteners, and protection sprays. The Korea Shoe Designers Association has noted increasing consumer sophistication in footwear maintenance, with specialty shoe care retailers expanding in Seoul's Hongdae and Gangnam districts. Korean beauty and personal care companies are also entering the shoe care space with differentiated formulations, adding innovation intensity to the domestic market.

Competitive Landscape

The global shoe care market is moderately fragmented, with the top five players including SC Johnson (Kiwi), Reckitt Benckiser, Salamander, Collonil, and Saphir Médaille d'Or collectively accounting for approximately 35–40% of global revenue. Mass-market brands compete on price and retail distribution breadth, while premium brands differentiate through formulation heritage, sustainable credentials, and specialty retailer exclusivity. Emerging business model trends include DTC subscription kits, limited-edition sneaker care collaborations with footwear brands, and refillable eco-formulation formats. The sneaker care segment is the most dynamic and entrepreneurially active, with multiple venture-backed startups competing alongside established household brands.

Key Developments:

- March 2025: Crep Protect launched its Crep Protect Cure Refill System a zero-waste sneaker cleaning solution in concentrated tablet form targeting eco-conscious consumers and expanding into European grocery retail channels as part of its sustainability positioning strategy.

- October 2024: Collonil introduced its 1909 Supreme Cream Bio leather conditioner made from 100% bio-based ingredients, receiving OECD 301 biodegradability certification and launching across premium outdoor and leather goods retailers in Germany, Austria, and Switzerland.

- January 2024: SC Johnson (Kiwi) expanded its Express Shine range into the sports and sneaker care segment with the Kiwi Sport Instant Cleaner formula, leveraging its global retail distribution in over 160 countries to compete directly against specialist sneaker care brands in the high-growth athletic footwear care segment.

Companies Covered in Shoe Care Market

- SC Johnson & Son, Inc. (Kiwi Brand)

- Collonil (Salzenbrodt GmbH & Co. KG)

- Saphir Médaille d'Or (Avel)

- Tarrago Brands International

- Nikwax Ltd.

- Crep Protect

- Jason Markk

- Sneaker Lab

- Reshoevn8r

- Burgol (Schuhpflegemittel GmbH)

- Lincoln Shoe Care (Plasti-Dip International)

- Meltonian Shoe Care

- Salamander GmbH

- Allen Edmonds Shoe Care (Caleres)

- Moneysworth & Best Shoe Care Inc.

- Urge Footwear Care

- Angel Wax Shoe Care

- Bickmore (Bickmore Co.)

Frequently Asked Questions

The global Shoe Care market is valued at US$ 5.7 Bn in 2026 and is projected to reach US$ 8.5 Bn by 2033, growing at a CAGR of 5.8%. Historically, the market grew from US$ 4.3 Bn in 2020 at a CAGR of 5.0%, representing an incremental revenue opportunity of US$ 2.8 Bn over the 2026–2033 forecast period.

The primary drivers are the global sneaker culture explosion with the U.S. sneaker resale market alone exceeding US$ 6 billion annually per Cowen & Company data and the premiumization of luxury footwear consumption compelling owners to invest in professional-grade care products.

Shoe polish is the dominant product type segment with approximately 28% of global shoe care market revenue in 2026.

Europe leads the global shoe care market with approximately 34% of revenue in 2026, anchored by Germany, France, Italy, and the U.K.

The transition to eco-friendly, bio-based, and PFAS-free shoe care formulations is the most significant market opportunity.

Leading companies include SC Johnson (Kiwi brand, present in 160+ countries), Collonil (Germany, Europe's premium leather care leader), Saphir Médaille d'Or (France, world's most prestigious polish brand), Tarrago Brands International, Nikwax Ltd. (U.K., eco-formulation specialist), Crep Protect (U.K., sneaker care leader), Jason Markk (U.S., DTC sneaker care pioneer), and Salamander GmbH, among others.