- Specialty & Fine Chemicals

- Decyl Oleate Market

Decyl Oleate Market Size, Share, and Growth Forecast, 2025- 2032

Decyl Oleate Market by Source (Plant Based and Animal Based), Application (Personal Care, Pharmaceutical, and Others), and Regional Analysis for 2025 - 2032

Decyl Oleate Market Size and Trends Analysis

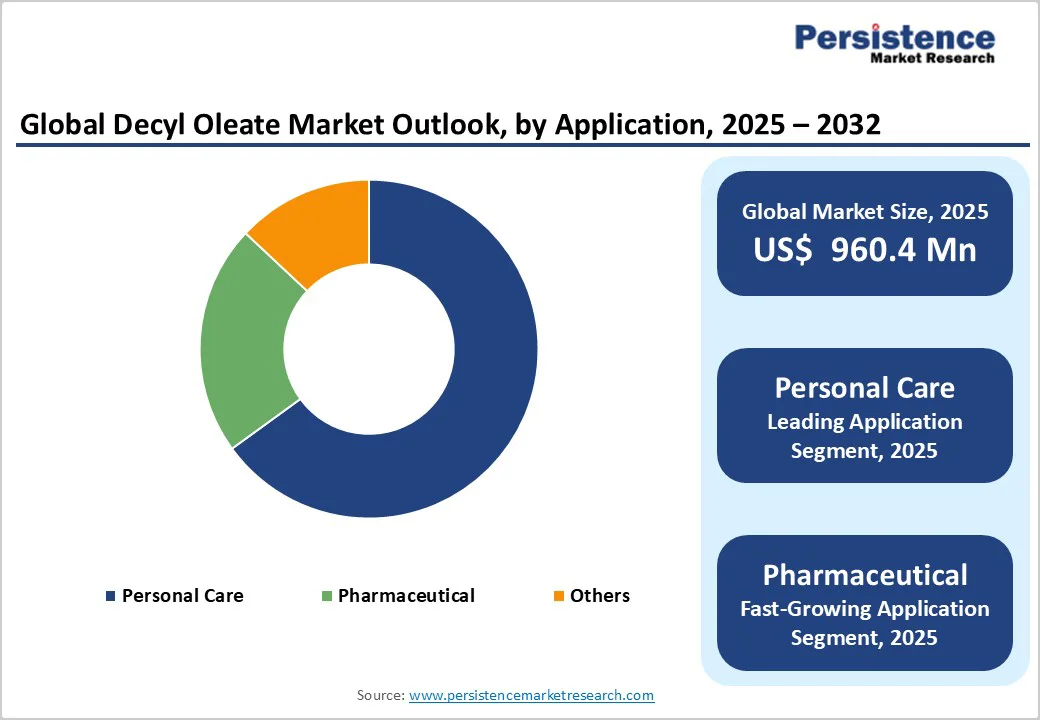

The global decyl oleate market was valued at US$ 960.3 million in 2025 and is expected to reach US$ 1,319.1 million by 2032, reflecting a CAGR of 4.6% during the forecast period. This steady growth outlook is supported by rising demand for bio-based emollients in the personal care industry, as consumers increasingly prefer natural, clean-label, and sustainably sourced ingredients.

Decyl oleate, an ester derived from decanol and oleic acid, features a long hydrocarbon chain that underpins its performance as an effective surfactant and emollient. It is typically produced as a colorless to pale-yellow liquid with a mild odor, aligning well with formulation requirements in cosmetics and skincare applications.

Historically, the market exhibited resilience, recording a CAGR of 2.8% between 2019 and 2025 and reaching US$ 781.2 million in 2019. Growth has been driven by expanding use in cosmetic formulations, increasing pharmaceutical incorporation, and supportive regulatory momentum favoring oleochemical-based alternatives over petrochemical derivatives across key global markets.

Key Industry Highlights:

- Consumer preference for natural, plant-based skincare is boosting decyl oleate demand. Its lightweight, non-greasy emollient profile and strong safety record make it ideal for clean-label moisturizers, creams, and lotions.

- Plant-based decyl oleate dominates with above 65% revenue share, while animal-based variants represent the fastest-growing segment, driven by specialized premium formulation applications.

- Personal care applications command above 75% market share, with the pharmaceutical segment emerging as the fastest-growing category at 3.6% CAGR through 2033, driven by drug delivery innovations.

- North America leads with above 30% global revenue share, supported by premium positioning, clean beauty trends, and 85% U.S. contribution to regional cosmetic ingredient demand.

- Digital B2B platforms enable formulators to source decyl oleate directly from manufacturers. Online procurement improves documentation access, reduces order barriers, and supports small cosmetic brands in emerging markets.

| Key Insights | Details |

|---|---|

| Decyl Oleate Market Size (2025E) | US$ 960.4 Mn |

| Market Value Forecast (2032F) | US$ 1,319.1 Mn |

| Projected Growth (CAGR 2025 to 2032) | 4.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.8% |

Market Dynamics

Drivers - Rising Consumer Demand for Natural and Plant-Based Personal Care Ingredients

Decyl oleate is a widely used cosmetic ingredient known for its excellent emollient and skin-conditioning properties. Its lightweight, fast-absorbing nature makes it a preferred choice in moisturizers, creams, and lotions, where it delivers a smooth, non-greasy finish. As the global personal care industry increasingly shifts toward natural and plant-based formulations, demand for decyl oleate continues to grow.

The market estimates indicate that natural ingredients are rapidly increasing their share, supporting the rise of clean-label esters such as decyl oleate, which is produced by combining oleic acid, primarily derived from palm kernel and other vegetable oils, with decyl alcohol.

Its strong safety profile, characterized by low toxicity and minimal irritation potential even at high concentrations, further enhances its acceptance in cosmetic formulations. Moreover, expanding oleochemical production capacities, particularly in fast-growing markets like India, is strengthening the availability and supply outlook for decyl oleate.

Technological Advancements in Oleochemical Production and Cost Competitiveness

Manufacturing innovation is narrowing the cost gap between bio-based and petrochemical alternatives, enhancing decyl oleate's market competitiveness. Investment in advanced oleochemical processing technology is increasing at a rate of 10% year-on-year, primarily focused on yield optimization and production efficiency.

Life Cycle Assessment (LCA) studies confirm that palm-based fatty alcohols exhibit a carbon footprint 50% to 80% lower than synthetic petrochemical-derived oxo alcohols on a cradle-to-gate basis. This environmental advantage aligns with corporate sustainability commitments, particularly Scope 3 emissions reduction targets mandated by environmental, social, and governance (ESG) frameworks.

The global oleochemicals market is projected to reach above USD 60 billion by 2032, indicating robust infrastructure investment in feedstock production. Southeast Asia's dominance in palm oil production, the primary raw material source ensures supply chain stability and favorable economics for decyl oleate manufacturers.

Restraint - Regulatory Complexity and Compliance Costs Across Multiple Jurisdictions

The decyl oleate market faces increasing regulatory scrutiny as global cosmetic regulations diverge post-Brexit and EU standards intensify. Commission Regulation (EU) 2024/996 and Regulation (EU) 2025/877 introduced stricter bans and restrictions for cosmetic substances, with 21 CMR (carcinogenic, mutagenic, or toxic to reproduction) substances banned effective September 1, 2025.

While decyl oleate itself is not restricted, manufacturers must ensure complete supply chain traceability and documentation to comply with evolving ingredient disclosure requirements under the EU Cosmetics Regulation (EC) No. 1223/2009.

The United Kingdom's divergent regulatory pathway following Brexit adds compliance complexity, with the UK's Product Safety and Metrology SI (Schedule 34) incorporating unique requirements separate from EU standards.

In North America, the FDA's Modernization of Cosmetics Regulation Act (MoCRA) imposes enhanced safety assessment and facility registration obligations, increasing operational costs for ingredient suppliers. These multi-jurisdictional requirements create barriers to entry for smaller manufacturers and increase time-to-market for new formulations.

Opportunity - Expansion into Anti-Aging and Sun Protection Formulations

The rise in aging global population presents substantial growth opportunities for decyl oleate in premium skincare applications. The skincare application segment is anticipated to capture 30.0% of the personal care ingredient market revenue in 2025, driven by anti-aging, hydration, and sun protection demand.

Decyl oleate's occlusive properties prevent moisture loss and enhance skin elasticity, making it particularly valuable in anti-aging formulations targeting mature consumers. Skin care product sales alone surged by 15% in 2025 in urban centers, reflecting heightened investment in personal grooming.

The compound's non-comedogenic profile, meaning it does not clog pores, addresses formulation challenges for acne-prone and sensitive skin types, expanding addressable market segments. Sun protection products represent another high-growth opportunity, as decyl oleate improves sunscreen spreadability and sensory experience while maintaining UV filter stability.

The European market particularly demonstrates strong demand for sun care products due to increasing awareness of skin cancer risks associated with UV exposure.

Digital Commerce and Direct-to-Manufacturer B2B Channels

E-commerce transformation in chemical ingredient procurement is creating new revenue channels for decyl oleate suppliers. Manufacturers concentrated in Southeast Asia are increasingly launching dedicated B2B platforms for direct sales to cosmetic formulators, eliminating traditional distributor markups and improving profit margins.

The rapid expansion of e-commerce in the personal care sector presents significant opportunities, offering convenience and broader market access to previously underserved regions.

Digital platforms enable technical documentation sharing, certificate of analysis (CoA) provision, and regulatory compliance verification in real-time, accelerating procurement cycles. For small and medium-sized cosmetic brands seeking natural ingredient alternatives, online sourcing platforms reduce minimum order quantities and provide formulation support resources.

This channel democratization is particularly impactful in emerging markets across Latin America and Eastern Europe, where traditional chemical distribution infrastructure is less developed. The integration of digital supply chain transparency tools also addresses sustainability verification demands from conscious consumers.

Category-wise Analysis

Product Type Insights

The global decyl oleate market is shaped by two contrasting yet complementary source segments, plant-based and animal-based each contributing to overall demand dynamics. The plant-based segment dominates with over 65% revenue share, supported by strong regulatory alignment, consumer preference for botanical ingredients, and the widespread availability of vegetable oil feedstocks such as palm kernel and coconut oil.

Sustainability mandates across the EU and North America, coupled with clean-label positioning and corporate commitments to natural sourcing, further reinforce its leadership. With natural fatty alcohols expected to capture more than 58% of the global market in 2025, plant-based decyl oleate benefits from robust upstream integration, particularly in Southeast Asia’s well-established palm oil value chain.

Certifications such as RSPO, COSMOS, and NATRUE enable premium market positioning, although the segment continues to face scrutiny over land-use concerns, prompting exploration of algae oils and waste-derived alternatives.

In contrast, the animal-based segment, though smaller, represents the fastest-growing category. Derived mainly from tallow-based oleic acid, it finds niche demand in luxury skincare, dermatological products, and formulations designed for mature skin.

Its growth is tempered by ethical and religious considerations, as well as regional preferences, but remains relevant in markets where circular economy principles and established tallow industries support its use. Regulatory requirements for transparent labeling ensure consumer awareness while preserving the segment’s specialized market role.

Application Insights

The personal care segment dominates decyl oleate consumption, contributing over 75% of total revenue. Within this, cosmetics lead with nearly 78% market share in 2023 and a CAGR of 3.7%, driven by the ester’s ability to disperse pigments uniformly in foundations, blushes, and eye shadows.

Decyl oleate (C20H40O2) is a versatile cosmetic ester valued for its emollient, skin-conditioning, and lipid-layer-enhancing properties, often used as an effective alternative to Mulsifan. Its structure derived from decyl alcohol and oleic acid gives it a lightweight, silky profile that improves product spreadability, absorption, and overall sensory appeal.

This makes decyl oleate a key ingredient across skincare, haircare, and makeup formulations, where it imparts a smooth, luxurious texture.

In haircare, it enhances manageability and softness, while in skincare, projected to reach 30% market share by 2025 it effectively reduces TEWL, supporting barrier repair in moisturizers, serums, and anti-aging products. Ongoing innovation in microencapsulation, emulsion systems, and biomimetic technologies continues to elevate its importance.

The pharmaceutical segment, though smaller, is the fastest growing at a 3.6% CAGR (2023 - 2033), supported by decyl oleate’s role as a penetration enhancer in topical and transdermal drug delivery. Compliance with pharmacopeial standards and rising adoption in dermatology and cosmeceuticals create strong opportunities for medical-grade variants as the personal care chemicals market expands toward US$21.8 billion by 2032.

Regional Insights and Trends

North America strengthens its leadership in the global decyl oleate market through innovation, premiumization, and strong regulatory support

North America leads the global decyl oleate market with over 30% revenue share, supported by a strong cosmetic innovation ecosystem, high consumer spending, and a well-developed regulatory framework that favors safe, established ingredients.

The United States drives nearly 85% of the region’s personal care ingredient demand, supported by a mature beauty industry defined by premiumization, scientific validation, and clear consumer preference for natural, plant-based components.

U.S. cosmetic imports, valued at $7.79 billion in 2024, highlight the region’s active ingredient sourcing and robust industry scale. Regulatory oversight under the FDA’s FD&C Act and MoCRA ensures safety substantiation and transparent labeling, creating a conducive environment for multifunctional emollients like decyl oleate.

Growth in North America is largely shaped by three key drivers: rising demand for premium anti-aging skincare, the widespread adoption of clean beauty standards by major retailers, and expanding domestic manufacturing supported by supply chain resilience initiatives.

Canada further strengthens regional momentum with $1.99 billion in cosmetic imports and strong consumer inclination toward natural, cruelty-free products. Investment trends also reinforce market expansion, with over $1 billion annually flowing into clean beauty start-ups that prioritize natural formulations. Combined with a thriving e-commerce channel capturing more than 25% of beauty sales, the region offers substantial opportunity for decyl oleate suppliers.

Europe’s Harmonized Regulatory Framework Strengthens Demand for High-Purity and Sustainable Decyl Oleate in the Cosmetics Market

Europe remains a highly influential market for cosmetic ingredients like decyl oleate, driven by stringent regulatory harmonization under the EU Cosmetics Regulation (EC) No. 1223/2009.

The region enforces a precautionary, science-based approval framework requiring detailed safety assessments and Product Information Files (PIFs), positioning Europe as a global benchmark in cosmetic safety and standardization. As part of the $74.89 billion global cosmetics industry in 2024, Europe contributes significantly as both a manufacturing hub and major consumer market.

Germany leads regional production, supported by strong dermatological testing standards and major companies such as Beiersdorf, which generate substantial revenue across EU and U.S. markets.

The U.K., operating under post-Brexit Schedule 34 requirements, retains partial alignment with EU norms, while France’s premium brands like L’Oréal and Spain’s expanding natural-ingredient-focused sector further strengthen demand for high-purity and sensory-enhancing ingredients such as decyl oleate.

Regulatory oversight by the SCCS ensures continuous refinement of ingredient standards, exemplified by recent updates like Regulation (EU) 2024/996 and the upcoming prohibition of 21 CMR substances in 2025.

This environment drives manufacturers to prioritize safety, compliance, and sustainable sourcing. European suppliers, led by BASF SE and IOI Oleo GmbH, benefit from rising demand for bio-based, COSMOS- and Ecocert-certified decyl oleate as the EU accelerates its transition toward carbon neutrality by 2050.

Competitive Landscape

The global decyl oleate market shows moderate consolidation, with 30-35% of share held by major multinational oleochemical producers and the rest distributed among regional manufacturers and niche ingredient suppliers.

Its structure reflects the wider oleochemical sector, where vertical integration from feedstock sourcing such as palm plantations to downstream specialty esters creates strong competitive advantages. Leading companies operate large, diversified fatty ester portfolios, with decyl oleate being one of several key products.

The top four producers BASF SE, IOI Oleo GmbH, KLK OLEO, and Wilmar International collectively control around 40-45% of global capacity, reinforcing an oligopolistic environment. Alongside these giants, regional players cater to localized regulatory standards and formulation needs.

Competitive positioning generally falls into three groups: integrated oleochemical leaders with raw material advantages, specialized ester manufacturers offering technical and formulation expertise, and distributors enabling market access and inventory support for smaller formulators.

Key Industry Developments

- In 2024, Arkema's Oleris® oleochemicals product line received the USDA Certified Biobased Product Label in March 2024, indicating 100% renewable carbon content, providing customers with third-party verification of environmental claims supporting corporate sustainability objectives.

Companies Covered in Decyl Oleate Market

- BASF SE

- IOI Oleo GmbH

- Ecogreen Oleochemical (S) Pte. Ltd.

- Ashland LLC.

- KLK Oleo

- Mosselman SA

- Italmatch Chemicals SpA

- Oleon NV

- Zschimmer & Schwarz Holding GmbH & Co KG

- Stearinerie Dubois Fils SA

- Alzo International Inc

- Kumar Organic Products Limited

- CISME Italy s.r.l

- Venus Ethoxyethers Pvt. Ltd.

- Triveni Interchem Pvt. Ltd.

- R & D Laboratories Ltd

- Domus Chemicals S.p.A.

- Phoenix Chemicals Inc.

- Syntechem Co.,Ltd.

- Other Market Players

Frequently Asked Questions

The Decyl Oleate market is estimated to be valued at US$ 960.4 Mn in 2025.

The key demand driver for the Decyl Oleate market is its growing utilisation in the cosmetics and personal-care sector, particularly in skincare and hair-care formulations.

In 2025, the North America region will dominate the market with an exceeding 30% revenue share in the global Decyl Oleate market.

Among applications, personal care has the highest preference, capturing beyond 60% of the market revenue share in 2025, surpassing other applications.

BASF SE, IOI Oleo GmbH, Ecogreen Oleochemical (S) Pte. Ltd., Ashland LLC. KLK Oleo, and Mosselman SA are a few leading players in the Decyl Oleate market.