- Technology

- Workflow Automation Market

Workflow Automation Market Size, Share, and Growth Forecast, 2026 - 2033

Workflow Automation Market by Solution (Software, Services, Others), Deployment (Cloud, Hybrid, Others), Organization Size, End-user Industry, and Regional Analysis for 2026 - 2033

Workflow Automation Market Size and Trends Analysis

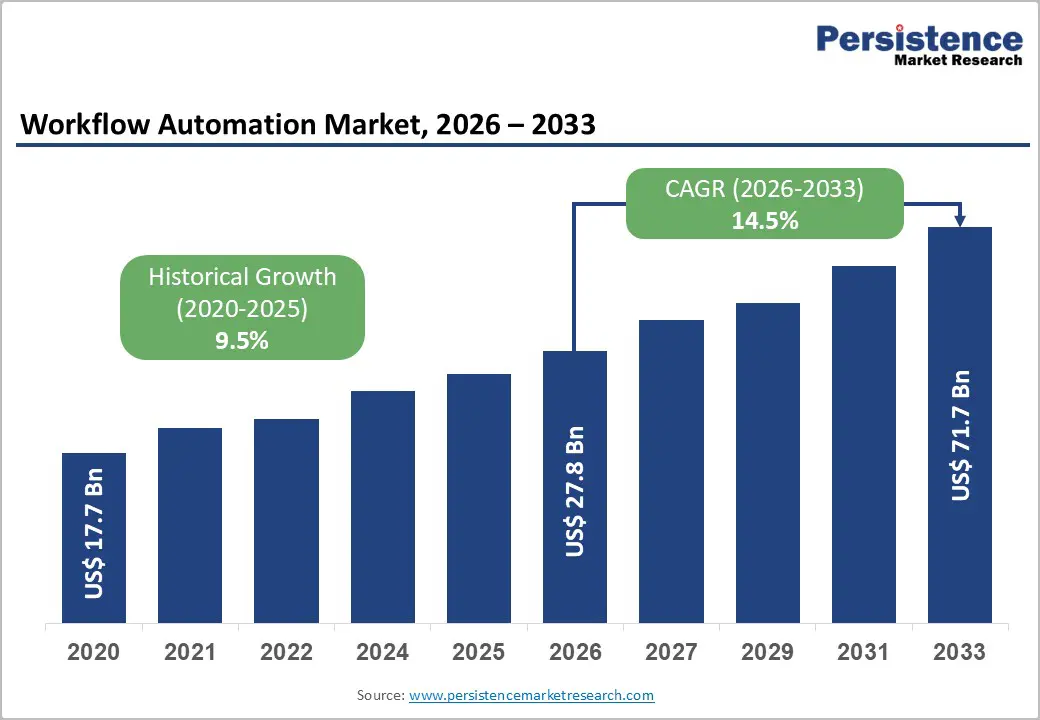

The global workflow automation market size is likely to be valued at US$27.8 billion in 2026 and is expected to reach US$71.7 billion by 2033, growing at a CAGR of 14.5% between 2026 and 2033, driven by enterprise-wide digital transformation, increasing adoption of AI-enabled automation, and rising demand for operational efficiency across industries.

Organizations are prioritizing workflow orchestration to reduce manual intervention, improve compliance, and accelerate decision-making. The shift toward cloud-native platforms and low-code technologies is enabling faster deployment and scalability, reinforcing sustained market expansion.

Key Industry Highlights:

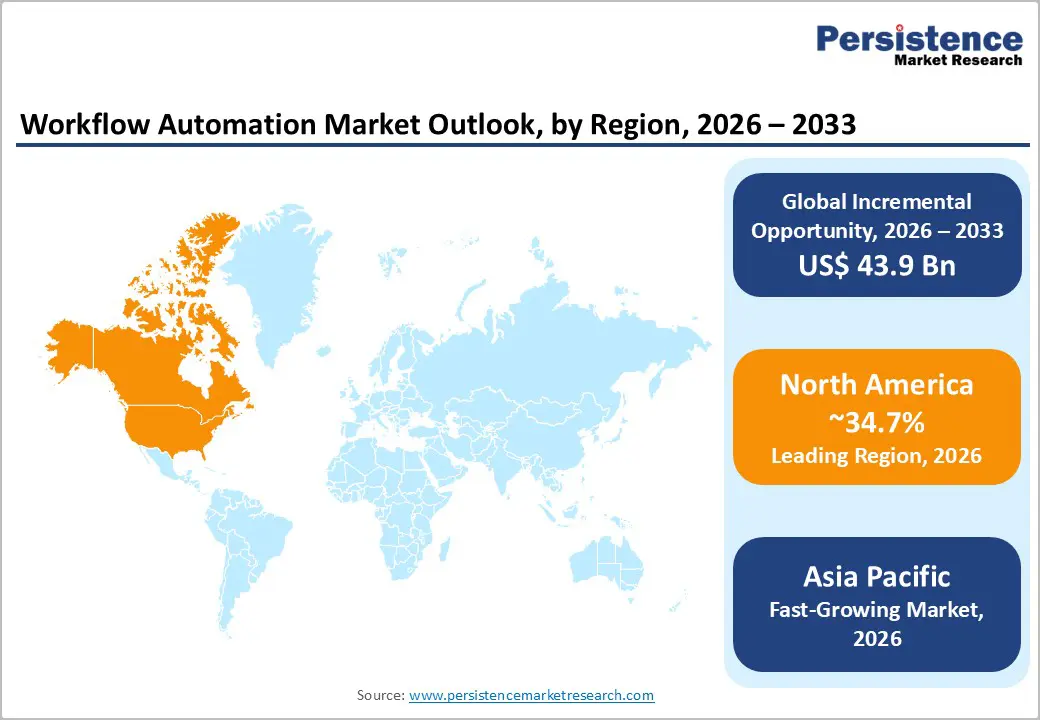

- Leading Region: North America is projected to account for 34.7% of revenue share in 2026, driven by strong enterprise IT spending, early adoption of AI-enabled automation, and the presence of major technology providers.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing region, supported by rapid digitalization across SMEs and manufacturing sectors in countries such as China, India, and Japan.

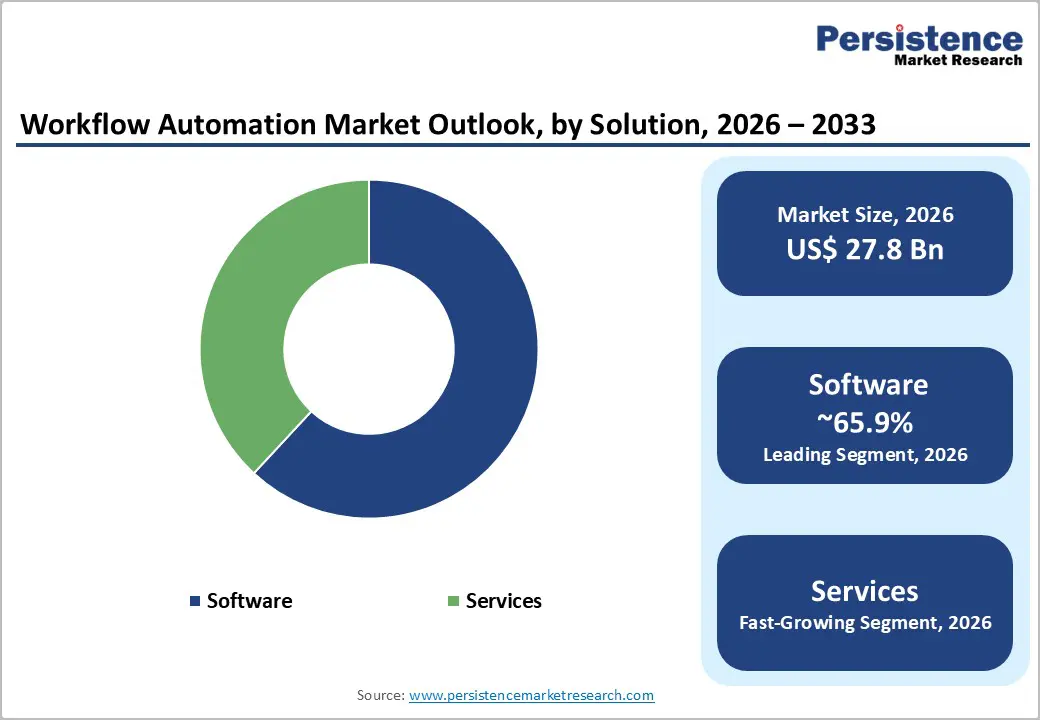

- Dominant Solution: The software segment is expected to dominate, holding an anticipated 65.9% market share in 2026, as organizations prioritize integrated platforms for workflow orchestration, analytics, and AI-driven automation.

- Leading Deployment: Cloud deployment is expected to lead the market, capturing an anticipated 61.4% share in 2026, driven by demand for scalability, cost efficiency, and seamless integration with existing enterprise applications.

DRO Analysis

Driver - AI-Driven Transformation from Task Automation to Intelligent Workflow Orchestration

Artificial intelligence is fundamentally reshaping workflow automation by moving enterprises beyond rule-based task execution toward intelligent, context-aware orchestration. Modern platforms integrate workflow engines, robotic process automation (RPA), and low-code development with AI capabilities such as natural language processing, predictive analytics, and autonomous agents. This convergence allows organizations to automate complex, multi-step processes across departments, including finance, HR, customer service, and healthcare operations.

Enterprises are increasingly deploying AI to identify inefficiencies, predict bottlenecks, and trigger automated actions without manual oversight. The transition typically begins with high-volume, repetitive tasks and expands into enterprise-wide process transformation. This evolution is increasing automation coverage across business functions while improving accuracy and responsiveness.

AI integration is driving higher contract values, deeper platform adoption, and stronger vendor lock-in, as enterprises prefer unified systems capable of managing workflows, data, and intelligent agents within a single ecosystem.

Expanding Demand from SMEs and Regulated Industries Accelerating Adoption

The growing need for digitalization among small and medium-sized enterprises (SMEs) and highly regulated sectors is significantly expanding the addressable market. SMEs are adopting workflow automation to streamline internal processes such as finance, HR, and customer management without large-scale IT investments. Cloud-based deployment models and subscription pricing are making advanced automation accessible to smaller organizations.

Industries such as banking, healthcare, insurance, and government are also implementing workflow automation to meet stringent compliance, reporting, and audit requirements. These sectors benefit from automation’s ability to standardize processes, reduce errors, and maintain traceability across operations. The customer base is diversifying beyond large enterprises, creating new revenue streams through SaaS subscriptions, bundled services, and scalable deployment models. This trend supports long-term market expansion and increases recurring revenue potential for vendors.

Restraint - Integration, Complexity, and Regulatory Compliance Challenges

Despite strong adoption momentum, workflow automation implementation faces significant challenges related to system integration, data security, and regulatory compliance. Enterprises often operate across multiple legacy systems, including ERP, CRM, HR platforms, and document management systems, making seamless integration complex and resource-intensive.

Regulatory frameworks governing data protection, cybersecurity, and AI usage require organizations to ensure transparency, auditability, and human oversight in automated processes. Compliance obligations increase implementation costs and extend deployment timelines, particularly in regulated industries.

The shortage of skilled professionals capable of managing automation frameworks and governance structures further complicates adoption. These factors can delay project execution, increase the total cost of ownership, and reduce return on investment in the short term.

Opportunity - Vertical-Specific Automation Solutions for Regulated Industries

Regulated industries present a high-value opportunity for workflow automation vendors due to their reliance on structured, document-intensive processes. Banking, healthcare, insurance, and public-sector organizations require automation solutions that ensure compliance, auditability, and data security while improving operational efficiency.

Vendors are increasingly developing industry-specific solutions with pre-configured workflows, compliance frameworks, and reporting capabilities tailored to sector requirements. These offerings reduce implementation time and lower adoption barriers for enterprises. Companies that deliver verticalized platforms with built-in governance and regulatory compliance features can capture larger contracts, improve customer retention, and differentiate themselves in a competitive market.

Rapid Expansion in Asia Pacific Driven by SME and Industrial Automation

Asia Pacific represents the most significant growth opportunity, driven by rapid digitalization across manufacturing, services, and SME sectors. Businesses in countries such as China, India, Japan, and Southeast Asia are increasingly adopting workflow automation to enhance productivity, reduce operational costs, and remain competitive in global markets.

Automation is particularly impactful in areas such as supply chain management, procurement, finance operations, and customer service, where process efficiency directly influences business performance. Governments across the region are also promoting digital adoption through infrastructure investments and policy initiatives. Vendors offering scalable, cost-effective, and localized solutions with multilingual support and industry-specific templates are well-positioned to capture market share in this high-growth region.

Category-wise Analysis

Solution Insights

Software is expected to lead, accounting for an anticipated 65.9% of market share in 2026, driven by strong demand for integrated platforms that combine workflow design, orchestration, analytics, and AI capabilities. Enterprises prefer software solutions that enable end-to-end automation across business processes while providing visibility, control, and scalability. These platforms serve as the backbone of digital transformation initiatives, allowing organizations to streamline operations and improve efficiency.

For example, platforms such as Microsoft Power Platform and ServiceNow workflows are widely used to automate HR onboarding, IT service management, and finance approvals. Similarly, SAP and Oracle embed workflow automation within ERP systems to optimize procurement and supply chain processes.

Services are likely to be the fastest-growing segment, supported by increasing demand for consulting, implementation, and integration services. As automation initiatives expand from pilot projects to enterprise-wide deployments, organizations require expertise in process optimization, change management, and system integration. This trend is particularly prominent in regulated industries and among mid-sized enterprises that lack internal automation capabilities.

For instance, banks deploying automation through UiPath often rely on third-party consulting partners for compliance workflow design, while healthcare providers implementing solutions from IBM require integration services to connect clinical and administrative systems. This growing reliance on external expertise is accelerating service revenue growth alongside software adoption.

Deployment Insights

Cloud deployment is expected to lead the market with an anticipated 61.4% share in 2026, reflecting the shift toward cloud-first enterprise strategies. Cloud-based workflow automation enables rapid deployment, lower infrastructure costs, and seamless integration with existing SaaS applications. It also supports scalability and continuous updates, making it the preferred choice for organizations seeking agility and efficiency.

For example, Salesforce Flow and Workato are widely used by enterprises to automate customer service workflows, marketing campaigns, and cross-application integrations in real time. These solutions allow organizations to deploy automation without significant upfront infrastructure investment, accelerating time-to-value.

Hybrid deployment is expected to be the fastest-growing segment, as enterprises seek to balance cloud scalability with on-premise control over sensitive data and critical systems. Hybrid models are particularly relevant in industries with strict regulatory and data residency requirements. They provide a flexible transition path for organizations modernizing legacy systems while maintaining operational continuity.

For instance, financial institutions often use hybrid deployments combining on-premise systems with automation tools from Automation Anywhere to ensure data security while benefiting from cloud-based orchestration. Similarly, manufacturing firms leverage hybrid models with platforms such as Appian to integrate factory-floor systems with enterprise-level workflow automation, enabling real-time decision-making without compromising operational control.

Regional Insights

North America Workflow Automation Market Trends

North America is projected to lead the market, accounting for 34.7% of revenue share in 2026, with the U.S. contributing over 72% of the regional market. The region’s leadership is driven by strong technology infrastructure, high enterprise IT spending, and early adoption of advanced automation solutions.

U.S. Workflow Automation Market Trends

The U.S. dominates the regional landscape due to the presence of major technology providers such as Microsoft, ServiceNow, UiPath, and Salesforce. Recent developments include Microsoft’s expansion of AI copilots within Power Platform and ServiceNow’s launch of AI-driven workflow governance tools, which are enabling enterprises to automate complex, cross-functional processes. These innovations are accelerating enterprise adoption of intelligent workflows in sectors such as BFSI and healthcare.

Enterprises across finance, healthcare, and technology sectors are investing heavily in AI-driven automation to improve operational efficiency and customer experience. For example, large U.S. banks are deploying workflow automation platforms integrated with AI for fraud detection, loan processing, and compliance reporting, significantly reducing processing time and operational risk.

Canada Workflow Automation Market Trends

Canada is emerging as a strong contributor, supported by government-backed digital transformation initiatives and increasing cloud adoption. Companies such as IBM and Appian are expanding their presence in the region through partnerships and enterprise deployments, particularly in the public sector and financial services. This is strengthening the adoption of workflow automation in regulated environments.

Regulatory frameworks across North America emphasize data security and compliance, encouraging organizations to adopt automation solutions with robust governance capabilities. The region also benefits from a skilled workforce and strong venture capital investment, which accelerates product development and market expansion.

Investment trends indicate a shift toward integrated platforms that combine workflow automation, AI, and analytics, enabling organizations to achieve end-to-end process transformation.

Europe Workflow Automation Market Trends

Europe represents a significant market for workflow automation, characterized by strong regulatory oversight and increasing demand for compliant automation solutions. Countries such as Germany, the United Kingdom, France, and Spain are leading adopters, driven by digital transformation initiatives across industries.

Germany Workflow Automation Market Trends

Germany’s leadership is rooted in its strong manufacturing base and Industry 4.0 initiatives. Companies such as SAP are embedding workflow automation into enterprise resource planning systems, enabling manufacturers to automate supply chain operations, procurement, and production workflows. This is improving operational efficiency and reducing downtime across industrial processes.

U.K. Workflow Automation Market Trends

The U.K. is a key market driven by financial services and public sector digitalization. Organizations are increasingly adopting automation platforms from providers such as Automation Anywhere and UiPath to streamline compliance, customer onboarding, and back-office operations. Government initiatives supporting SME digital adoption are further accelerating market growth, particularly among mid-sized enterprises.

Regulatory requirements related to data protection, cybersecurity, and AI governance are shaping the adoption of workflow automation technologies. Organizations are prioritizing solutions that provide transparency, auditability, and control over automated processes.

The region’s industrial base, particularly in manufacturing, is also contributing to market growth through the adoption of automation for process optimization and efficiency improvement. SMEs are increasingly adopting digital tools supported by government initiatives promoting innovation and competitiveness.

Investment trends focus on compliance-driven automation, particularly in regulated industries such as banking, healthcare, and public services, where process standardization and risk management are critical.

Asia Pacific Workflow Automation Market Trends

Asia Pacific is the fastest-growing region, with a CAGR of 9.8%, driven by rapid digitalization across industries and increasing adoption of automation technologies. Key markets include China, Japan, India, and Southeast Asia, where businesses are investing in workflow automation to enhance productivity and reduce operational costs.

China Workflow Automation Market Trends

China is a major contributor, driven by large-scale industrial automation and digital transformation initiatives. Enterprises are integrating workflow automation into manufacturing and logistics operations to optimize supply chains and production efficiency. Companies leveraging platforms from Oracle and SAP are automating procurement, inventory management, and distribution processes, improving operational agility.

Japan Workflow Automation Market Trends

Japan’s market growth is supported by its focus on robotics and process efficiency. Organizations are adopting workflow automation solutions from providers such as IBM to streamline administrative processes and address labor shortages. Automation is widely used in finance, manufacturing, and healthcare to improve accuracy and reduce manual workloads.

India Workflow Automation Market Trends

India is emerging as a high-growth market driven by rapid SME digitalization and expanding IT services. Companies are increasingly adopting platforms like Zoho and Kissflow to automate HR, finance, and customer workflows. The rise of digital-native businesses and government-led digital initiatives is accelerating adoption across sectors.

The region’s strong manufacturing base and growing SME sector are major drivers of demand. Automation is widely used in supply chain management, procurement, finance operations, and customer service to improve efficiency and competitiveness.

Government initiatives promoting digital transformation and infrastructure development are further supporting market growth. The adoption of cloud computing, AI, and IoT technologies is accelerating the deployment of workflow automation solutions across industries.

Investment trends highlight the importance of localized solutions tailored to regional needs, including language support, industry-specific templates, and cost-effective deployment models.

Competitive Landscape

The global workflow automation market is moderately fragmented, with a mix of large enterprise software providers and specialized automation vendors. Leading players hold significant market share due to their comprehensive platforms, global presence, and strong customer relationships. However, numerous niche providers compete by offering specialized solutions targeting specific industries or use cases.

Competition is increasingly centered on platform capabilities, AI integration, and ecosystem strength rather than standalone features. Vendors are focusing on delivering end-to-end solutions that combine workflow automation, integration, analytics, and governance.

Key players are focusing on AI integration, platform consolidation, and vertical specialization to strengthen their market position. Strategic priorities include expanding cloud capabilities, enhancing low-code development tools, and building partner ecosystems. Vendors are also adopting subscription-based pricing and usage models to attract a broader customer base and drive recurring revenue growth.

Key Industry Developments:

- In March 2025, ServiceNow announced the acquisition of AI startup Moveworks in a deal valued at approximately $2.85 billion, marking its largest acquisition to date. The move strengthens ServiceNow’s capabilities in autonomous AI and conversational workflow automation, enabling enterprises to automate complex, multi-step business processes more efficiently.

- In November 2025, UiPath launched its 2025.10 platform release, introducing a unified development environment for building AI agents, robots, and API-based workflows, along with prebuilt templates and governance features. This development improves developer productivity and supports enterprise-scale deployment of agentic automation.

Companies Covered in Workflow Automation Market

- Microsoft

- ServiceNow

- UiPath

- IBM

- SAP

- Oracle

- Salesforce

- Pegasystems

- Appian

- Automation Anywhere

- Workato

- Nintex

- Kissflow

- Zoho

- Bizagi

- Pipefy

Frequently Asked Questions

The global workflow automation market is valued at US$27.8 billion in 2026.

The workflow automation market is projected to reach US$71.7 billion by 2033.

Key trends include AI-driven workflow orchestration, low-code/no-code platform adoption, cloud-first deployment strategies, and increasing integration of RPA with enterprise applications.

The software segment is the leading category, accounting for 65.9% market share, as enterprises prioritize integrated platforms that offer end-to-end workflow automation, analytics, and AI capabilities.

The workflow automation market is expected to grow at a CAGR of 14.5% from 2026 to 2033.

Major players include Microsoft, ServiceNow, UiPath, IBM, and SAP.