- Technology

- Merchant Cash Advance Market

Merchant Cash Advance Market Size, Share, and Growth Forecast 2026 - 2033

Merchant Cash Advance Market by Product Type (Traditional Merchant Cash Advance, Revenue-Based Financing, Invoice Factoring, Hybrid MCA Financing), by Repayment Method (Split Percentage, ACH Withdrawal, Lockbox-Based, Fixed Daily/Weekly Payment, Hybrid Repayment), Provider Type, Business Tenure, End-user, and Regional Analysis, 2026 - 2033

Merchant Cash Advance Market Size and Trend Analysis

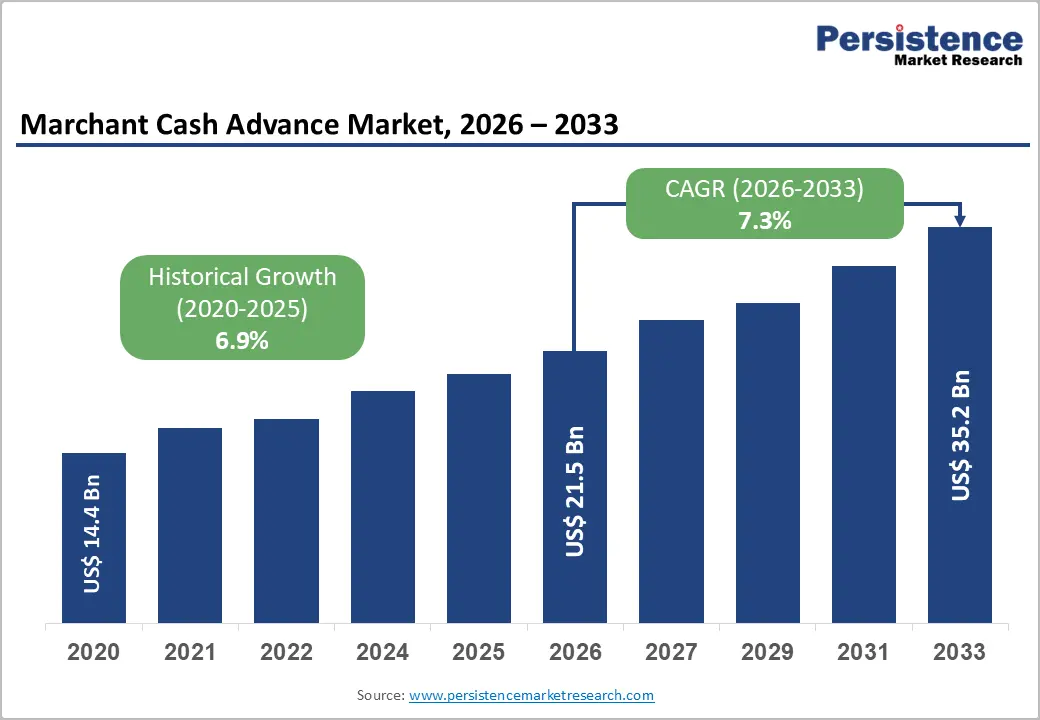

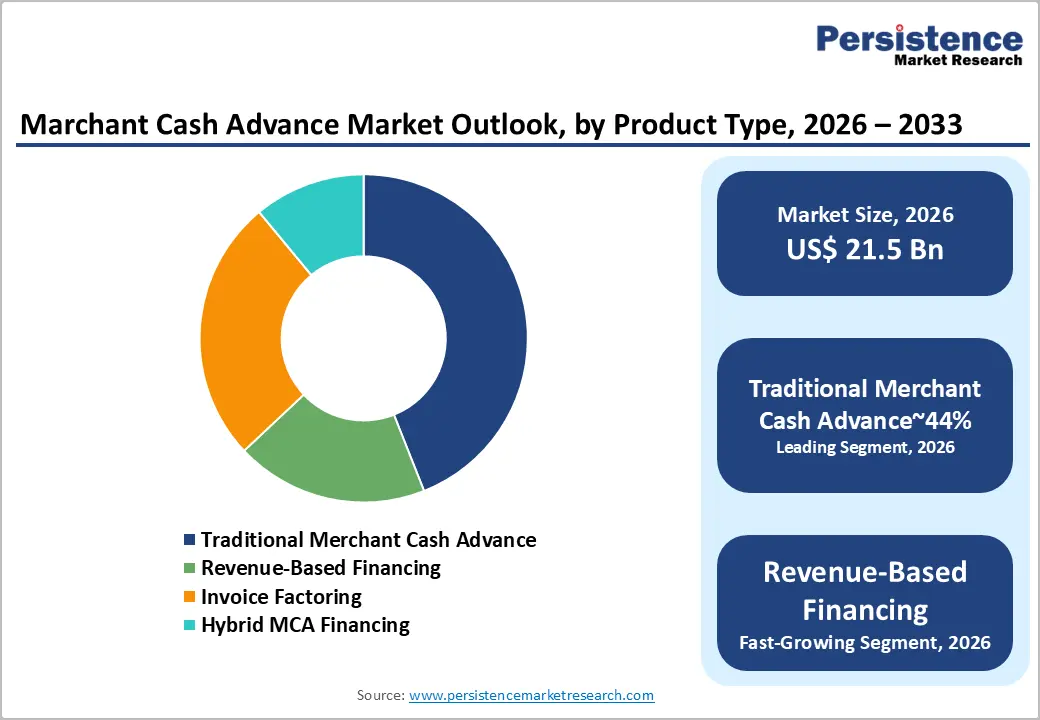

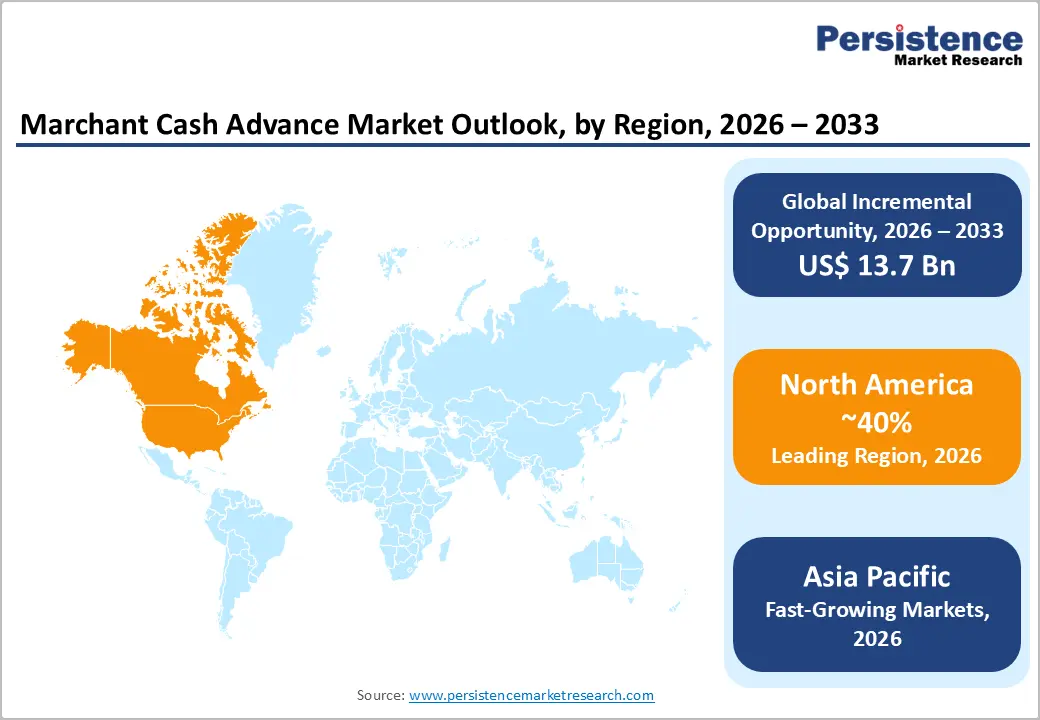

The global merchant cash advance market size is likely to be valued at US$ 21.5 billion in 2026 and is expected to reach US$ 35.2 billion by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 to 2033.

The market's sustained expansion is driven by the persistent financing gap faced by small and medium-sized enterprises (SMEs) globally and the rapid scaling of FinTech lending infrastructure.

Key Industry Highlights:

- Leading Region: North America dominates the global merchant cash advance market, accounting for 40% share, anchored by the U.S.'s 33 million small businesses, mature FinTech lending infrastructure, extensive ISO broker networks, and progressive regulatory frameworks, including California SB 1235, driving industry professionalization.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a rising CAGR of 9.1%, driven by India's 63 million MSMEs, China's digital lending ecosystems, OCEN framework enablement, and ASEAN's mobile payment penetration, creating scalable MCA underwriting data infrastructure across developing markets.

- Dominant Segment: FinTech Lenders lead the provider type segment with approximately 48% market share, leveraging AI-driven underwriting, open banking integrations, and 24-hour funding capabilities that decisively outperform traditional banks in speed, accessibility, and SME borrower experience.

- Fastest Growing Segment: Revenue-Based Financing is the fastest growing product type segment, gaining rapid traction among e-commerce and SaaS businesses seeking flexible repayment structures directly linked to monthly revenue, aligning repayment obligations with business performance cycles.

- Key Opportunity: E-commerce merchant financing represents a high-growth opportunity, with global e-commerce sales exceeding US$ 3.3 trillion annually and platforms like Shopify Capital demonstrating billion-dollar-scale demand for revenue-based advance products tied directly to digital sales proceeds.

Market Dynamics

Drivers - Persistent SME Financing Gap and Rejection Rates at Traditional Banks

A structural, long-standing financing gap between SME capital demand and traditional bank credit supply is the foremost driver of MCA market growth. The U.S. Federal Reserve's Small Business Credit Survey reported that only 51% of small business loan applicants received the full financing they sought from large banks in 2023. Globally, the International Finance Corporation (IFC) estimates the SME financing gap in developing economies alone exceeds US$ 5 trillion annually.

MCA products circumvent traditional credit scoring requirements by evaluating a merchant's daily card sales and transaction history, enabling approvals within 24 to 48 hours, a decisive competitive advantage over bank loan timelines averaging 30 to 90 days. This speed-to-capital advantage remains irreplaceable for SMEs navigating urgent working capital needs, seasonal cash flow gaps, and opportunistic inventory purchases.

Rapid Expansion of FinTech Lending Platforms and Digital Payment Infrastructure

The proliferation of FinTech lending platforms has dramatically expanded the reach, efficiency, and product sophistication of the MCA market. According to the Cambridge Center for Alternative Finance (CCAF), global alternative finance volumes, encompassing MCA, revenue-based financing, and invoice factoring, have grown at double-digit rates annually over the past decade. Cloud-native underwriting platforms leveraging open banking data, real-time payment analytics, and machine learning risk models enable MCA providers to assess creditworthiness with unprecedented precision.

The Consumer Financial Protection Bureau (CFPB) noted that digital small business lending accounted for over 20% of U.S. SME loan originations by value in 2022. This maturation of the digital lending ecosystem, combined with payment processor partnerships that provide direct access to merchant transaction data, is accelerating MCA origination volumes and compressing operational costs for providers.

Restraints - High Effective Cost of Capital and Regulatory Scrutiny

The annualized equivalent cost of MCA financing, often expressed as a factor rate ranging from 1.1x to 1.5x the advance amount, translates into effective annual percentage rates (APRs) that can exceed 100-300% in some cases, drawing significant regulatory scrutiny.

The U.S. Federal Trade Commission (FTC) and multiple state attorneys general have issued enforcement actions against predatory MCA practices. California's SB 1235 and New York's Commercial Finance Disclosure Law now mandate APR disclosures for commercial finance products, including MCAs, increasing compliance costs and limiting aggressive pricing models that have historically driven volume growth.

Debt Stacking and Default Risk Among Over-Extended Borrowers

Debt stacking, the practice of SMEs simultaneously obtaining multiple MCAs from different providers without full disclosure, poses systemic risk to lender portfolios and limits sustainable market growth. The Electronic Transactions Association (ETA) and industry observers have flagged debt stacking as a leading cause of elevated default rates among MCA borrowers.

When multiple daily repayment obligations overlap, a merchant's net daily revenue can turn negative, triggering cascading defaults across multiple MCA providers simultaneously. This credit risk concentration discourages institutional capital from entering the MCA funding stack and contributes to periodic tightening of underwriting criteria, particularly during macroeconomic downturns.

Opportunities - E-Commerce Merchant Segment as a High-Growth Financing Channel

The exponential growth of e-commerce and the unique cash flow patterns of online merchants represent a transformative growth opportunity for MCA providers. According to the United Nations Conference on Trade and Development (UNCTAD), global e-commerce sales reached US$ 3.3 trillion in 2022 and continue to expand robustly. E-commerce merchants on platforms such as Amazon, Shopify, and eBay face frequent inventory financing needs tied to seasonal demand spikes and platform-driven sales events.

MCA products, particularly revenue-based financing structures, are ideally suited to this segment given their direct linkage to digital sales proceeds. Shopify Capital's rapid growth to over US$ one billion in annual merchant financing demonstrates the enormous latent demand. Independent MCA providers offering platform-integrated, API-driven advanced products to e-commerce merchants stand to capture significant incremental market share.

Emerging Market SME Financing via Mobile-First MCA Platforms

Emerging economies in the Asia Pacific, Latin America, and Sub-Saharan Africa present a high-growth frontier for mobile-first MCA platforms targeting underbanked SME populations. The World Bank Global Findex Database 2022 reports that 1.4 billion adults worldwide remain unbanked, with a disproportionate concentration in developing markets with high SME density.

Mobile payment platform data, from providers such as M-Pesa in East Africa and Paytm in India, provides rich transactional datasets enabling alternative credit scoring for merchants lacking formal credit histories. India's Account Aggregator (AA) Framework and the Open Credit Enablement Network (OCEN) infrastructure are specifically designed to unlock data-driven SME lending, creating a structurally favorable environment for the deployment of MCA products at massive scale across the developing world.

Category-wise Analysis

Product Type Insights

Traditional merchant cash advance remains the leading product type segment, accounting for approximately 44% of total market revenues. This product structure, in which a lump-sum advance is provided in exchange for a fixed percentage of future credit and debit card receivables, is deeply embedded in U.S. and global small-business financing ecosystems, having been commercially established since the late 1990s.

Its dominance reflects strong brand recognition among small business owners in sectors such as retail, restaurants, and personal services, where daily card transaction volumes are predictable and high. The Electronic Transactions Association (ETA) notes that the MCA industry facilitated tens of billions in small-business funding annually at its peak, with traditional MCA comprising the bulk of originations by both volume and value.

Repayment Method Insights

ACH Withdrawal is the dominant repayment method, representing approximately 39% of total repayment transactions. This method involves automated fixed daily or weekly debits directly from the merchant's bank account via the Automated Clearing House (ACH) network, providing MCA providers with consistent, predictable cash flow regardless of daily card sales fluctuations.

Its prevalence is underpinned by the near-universal adoption of ACH infrastructure among U.S. businesses. The National Automated Clearing House Association (Nacha) reports that ACH network volume exceeded 30 billion transactions in 2023, reflecting deep institutional entrenchment. ACH-based repayment simplifies reconciliation for both providers and borrowers and enables seamless integration with digital banking and accounting platforms.

Provider Type Insights

FinTech lenders are the dominant provider type segment, commanding approximately 48% of the total market. Their market leadership reflects decisive advantages in speed, technology infrastructure, and borrower experience over traditional banks and NBFCs. FinTech MCA providers leverage proprietary underwriting algorithms, open banking data integrations, and API-based connectivity to payment processors to approve and fund advances within 24 hours, a benchmark that traditional financial institutions cannot replicate.

The Cambridge Center for Alternative Finance (CCAF) documented that U.S. FinTech lenders more than doubled their small business lending market share between 2015 and 2022. Companies including OnDeck, Credibly, and Rapid Finance exemplify this segment's commercial scale and operational sophistication.

Business Tenure Insights

The more than 18-month tenure segment is the leading category, accounting for approximately 52% market share. Merchants with over 18 months of operating history exhibit more stable transaction data, stronger revenue histories, and lower default probabilities, enabling MCA providers to offer larger advance amounts at more competitive factor rates.

The U.S. Bureau of Labor Statistics (BLS) reports that approximately 80% of businesses survive their first year and roughly 55% survive five years, confirming that businesses that have crossed the 18-month threshold represent a meaningful and creditworthy segment. MCA providers prioritize this cohort for repeat advance programs and portfolio growth strategies that aim to increase lifetime customer value.

End-user Insights

Retail is the dominant end-use segment, contributing approximately 26% of total revenue. Retail merchants, encompassing brick-and-mortar stores, specialty retailers, and omnichannel operators, have historically been the archetypal MCA borrower due to their high daily credit card transaction volumes and predictable seasonal revenue patterns.

According to the U.S. Census Bureau, the U.S. retail sector comprises over one million establishments, the vast majority of which are independently owned SMEs with limited access to traditional bank credit. The segment's dominance is reinforced by persistent working capital needs tied to inventory procurement cycles, lease obligations, and staffing costs, all of which MCAs are particularly well-suited to address quickly and efficiently.

Regional Insights

North America Merchant Cash Advance Market Trends & Analysis

North America remains the largest Merchant Cash Advance (MCA) market, driven by the U.S.’s mature alternative lending ecosystem and strong SME demand. The region accounts for an estimated 40% of global MCA volume in 2026. Regulatory frameworks are enhancing transparency, while institutional funding is strengthening long-term market stability.

- U.S. Merchant Cash Advance Market Size

The United States dominates the regional market, contributing approximately USD 10.1 billion in 2026, supported by over 33 million small businesses. High credit gaps, strong fintech penetration, and evolving compliance frameworks (state-level disclosures and federal data rules) are accelerating adoption and formalizing underwriting standards across MCA providers.

Europe Merchant Cash Advance Market Trends, Drivers & Insights

Europe is an emerging MCA market, accounting for roughly 25% of the global share. Growth is fueled by fintech innovation, Open Banking (PSD2), and SME funding diversification initiatives. Increasing regulatory harmonization and reduced bank lending are creating favorable conditions for alternative financing expansion.

- Germany Merchant Cash Advance Market Size

Germany represents a high-potential but underpenetrated MCA market, estimated at USD 1.5 billion in 2026. Its large Mittelstand base drives demand, but conservative financing preferences slow adoption. However, digital lending platforms and increased fintech activity are gradually unlocking growth opportunities in revenue-based financing solutions.

- U.K. Merchant Cash Advance Market Size

U.K. merchant cash advance market leads Europe, with an estimated USD 2.2 billion market size in 2026. London’s advanced fintech ecosystem and strong alternative lending culture support rapid growth. Post-Brexit lending gaps and SME reliance on non-bank finance continue to accelerate MCA penetration and product innovation.

- France Merchant Cash Advance Market Size

France merchant cash advance market is growing steadily, reaching approximately USD 1.1 billion in 2026. Government-backed SME initiatives and increasing fintech adoption are supporting expansion. Regulatory oversight and improved access to financial data are enabling lenders to scale MCA offerings while maintaining responsible lending practices.

Asia Pacific Merchant Cash Advance Market Size

Asia Pacific is the fastest-growing MCA market, projected to capture 30% share with the highest CAGR of ~9.1%. Growth is driven by massive SME populations, digital payment ecosystems, and fintech-led credit models leveraging transaction data for underwriting.

- China Merchant Cash Advance Market Size

China leads the region with an estimated USD 2.5 billion MCA-equivalent market in 2026. Digital lending platforms integrated with e-commerce ecosystems enable real-time credit delivery. Strong fintech infrastructure and data-driven underwriting models are significantly improving access to working capital for SMEs.

- India Merchant Cash Advance Market Size

India’s is rapidly expanding, estimated at USD 1.6 billion in 2026. With over 63 million MSMEs, the credit gap remains substantial. Digital frameworks like Account Aggregator and OCEN are enabling scalable, data-driven lending, making India one of the most promising high-growth MCA markets globally.

- Japan Merchant Cash Advance Market Size

Japan’s market size is valued at approximately USD 900 million in 2026. It is evolving through its established receivables financing ecosystem. SMEs are gradually adopting revenue-based financing models. Stable regulatory systems and strong financial infrastructure support steady but moderate growth compared to emerging Asian markets.

Competitive Landscape

The global Merchant Cash Advance market is highly fragmented, characterized by a mix of large FinTech lenders, specialized funders, ISO networks, and emerging platform-integrated providers. Market leaders such as OnDeck, Credibly, and Rapid Finance differentiate through proprietary underwriting technology, broker network scale, and brand credibility.

Emerging business models include embedded finance partnerships with payment processors and e-commerce platforms, and white-label MCA program offerings for banks seeking to serve SME clients without direct origination capabilities. Strategic acquisitions and ISO channel consolidation are reshaping the competitive hierarchy, while 12% of revenues are being reinvested into AI-driven risk analytics and automated servicing infrastructure.

Key Developments:

- March 2025: Lendio announced the expansion of its marketplace lending platform to include embedded MCA products for small businesses applying through partner banks and credit unions, targeting underserved SME segments with advance amounts from US$ 5,000 to US$ 500,000 with same-day funding commitments.

- October 2024: Credibly launched an AI-powered underwriting engine integrating real-time open banking data and alternative data signals, including social commerce reviews and e-commerce platform performance metrics, to extend MCA approvals to early-stage merchants with limited traditional credit history.

- January 2024: Rapid Finance completed a strategic partnership with a major U.S. payment processor to offer merchant-embedded working capital advances directly within the processor's merchant dashboard, enabling seamless one-click advance applications with automated repayment via daily transaction settlement.

Merchant Cash Advance Market- Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 14.4 Bn |

| Current Market Value (2026) | US$ 12.5 Bn |

| Projected Market Value (2033) | US$ 35.2 Bn |

| CAGR (2026 - 2033) | 7.3% |

| Leading Region | North America, 40% share |

| Dominant Product Type | Traditional Merchant Cash Advance, 44% share |

| Top-ranking Provider Type | FinTech Lenders, 48% |

| Incremental Opportunity | US$ 13.7 Bn |

Companies Covered in Merchant Cash Advance Market

- Forward Financing

- Uplyft Capital

- Giggle Finance

- Fundomate

- Expansion Capital Group

- Byzfunder

- RAN Funding

- Lendio

- Credibly

- Rapid Finance

- CAN Capital

- OnDeck

- National Funding

- Fora Financial

- Libertas Funding

- Bluevine Inc.

- Kabbage

- Fundbox, Inc.

- PayPal Working Capital

- Square Capital

Frequently Asked Questions

The global merchant cash advance market is projected to reach US$ 35.2 Billion by 2033, growing from US$ 21.5 Billion in 2026 at a CAGR of 7.3% over the 2026 - 2033 forecast period, driven by persistent SME financing gaps, FinTech platform expansion, and rising e-commerce merchant financing demand globally.

The primary drivers include the structural SME financing gap, with the IFC estimating a global SME credit deficit exceeding US$ 5 trillion in developing economies, and rapid FinTech lending platform proliferation enabling 24-hour approvals. The expansion of digital payment infrastructure globally also underpins MCA underwriting quality and repayment monitoring capabilities.

FinTech Lenders are the dominant provider type with approximately 48% market share. Their leadership stems from AI-powered underwriting, open banking integrations, and 24-hour funding capabilities. The Cambridge Centre for Alternative Finance confirmed U.S. FinTech lenders more than doubled their small business lending market share between 2015 and 2022.

North America is the leading region, anchored by the U.S. market's 33 million small businesses per SBA data, decades-long MCA industry establishment, extensive ISO broker distribution networks, and progressive regulatory frameworks. California SB 1235 and New York's Commercial Finance Disclosure Law are professionalizing the sector and attracting institutional capital.

Key opportunities include capturing e-commerce merchant financing demand, with global e-commerce sales exceeding US$ 3.3 trillion annually per UNCTAD, and deploying mobile-first MCA platforms in Asia Pacific's underbanked SME markets. India's OCEN framework and Account Aggregator infrastructure enable scalable data-driven MCA underwriting for 63 million MSMEs.

Key market participants include OnDeck, Credibly, Rapid Finance, Lendio, CAN Capital, National Funding, Fora Financial, Forward Financing, Uplyft Capital, Giggle Finance, Fundomate, Expansion Capital Group, Byzfunder, RAN Funding, and Libertas Funding, alongside embedded finance providers such as PayPal Working Capital, Square Capital, and Kabbage.