- Biotechnology

- Diagnostic Enzymes Market

Diagnostic Enzymes Market Size, Share, and Growth Forecast 2026 - 2033

Diagnostic Enzymes Market by Product Type (Molecular Diagnostic Enzymes, Clinical Diagnostic Enzymes), by Enzyme Type (Oxidoreductases, Hydrolases, Transferases, Others), by Application (Infectious Diseases, Diabetes, Oncology, Cardiology, Others), by End-user (Hospitals & Clinics, Diagnostic Laboratories, Research & Academic Institutes, Biotechnology & Pharmaceutical Companies), by Regional Analysis, 2026 - 2033

Diagnostic Enzymes Market Share and Trends Analysis

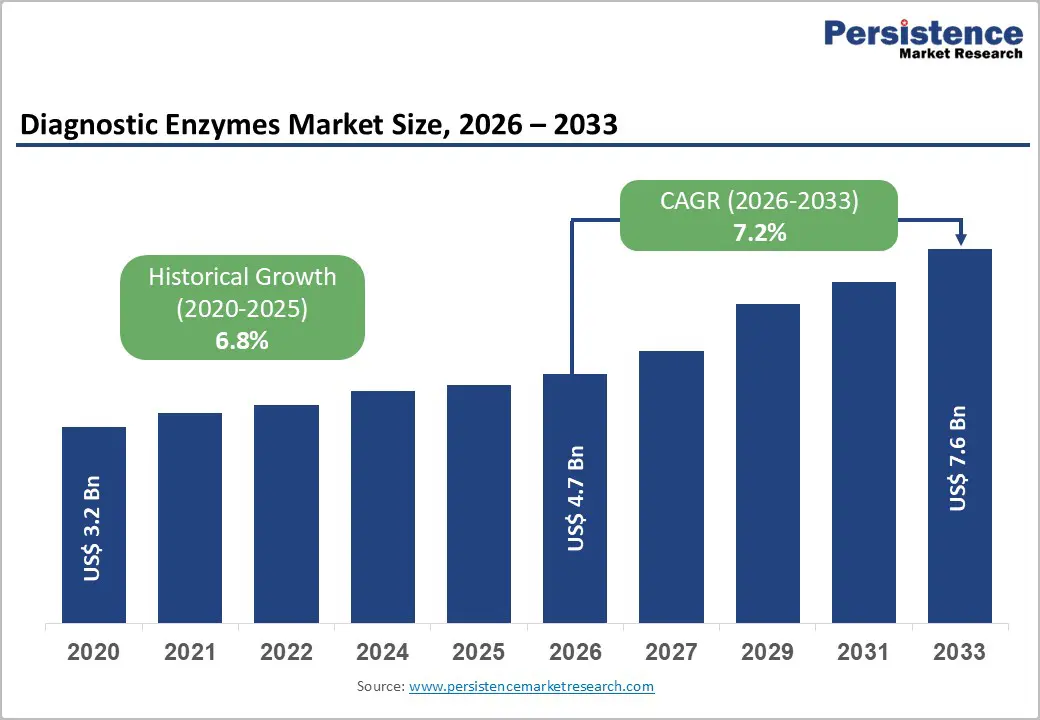

The global diagnostic enzymes market size is expected to be valued at US$ 4.7 billion in 2026 and projected to reach US$ 7.6 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

This growth is driven by the sustained shift toward molecular and high-throughput diagnostics, the rising burden of chronic and infectious diseases, and continuous menu expansion on clinical chemistry and molecular platforms. In vitro diagnostic manufacturers increasingly rely on high-performance enzymes to power polymerase chain reaction (PCR), next-generation sequencing (NGS), point-of-care testing, and routine clinical chemistry assays, which structurally tie enzyme demand to expanding test volumes. The market also benefits from aging populations, higher testing intensity in diabetes, oncology, and cardiology, and growing investments in laboratory automation and centralized reference laboratories worldwide.

Key Industry Highlights:

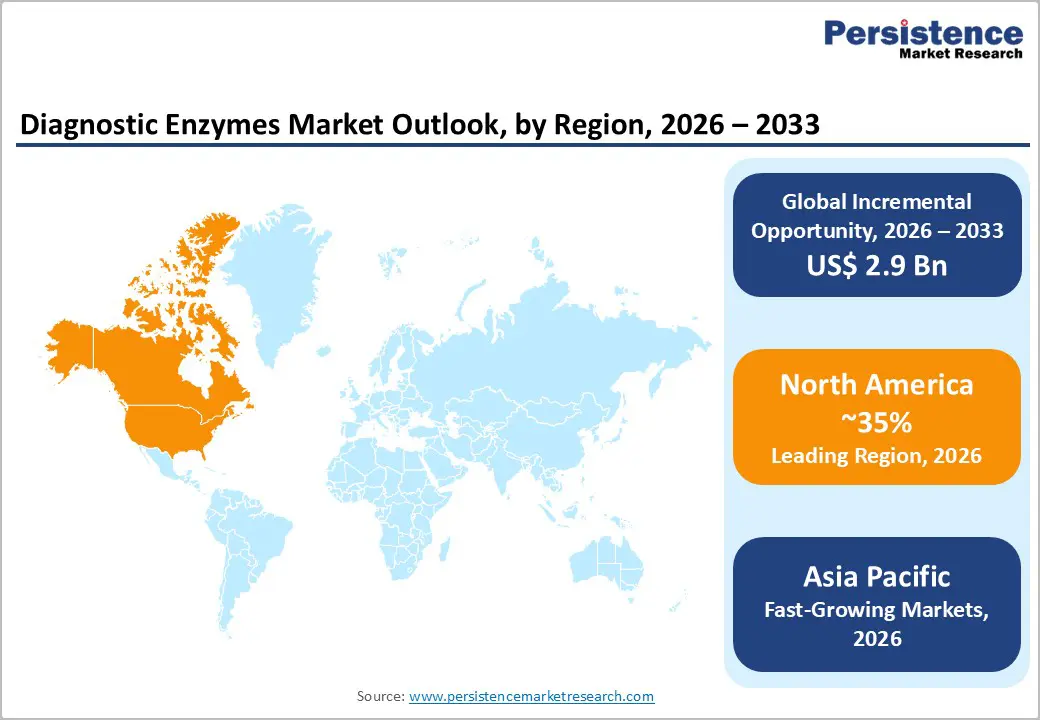

- North America leads the diagnostic enzymes market with about 35% share in 2025, supported by advanced clinical laboratory networks, high diagnostic intensity in chronic and infectious diseases, strong regulatory oversight, and a concentration of major IVD and life science companies.

- Asia Pacific is the fastest-growing region, driven by rising healthcare expenditure, expansion of hospital and reference labs in China and India, increasing adoption of molecular diagnostics and NGS, and local manufacturing advantages for enzyme production and diagnostic kits.

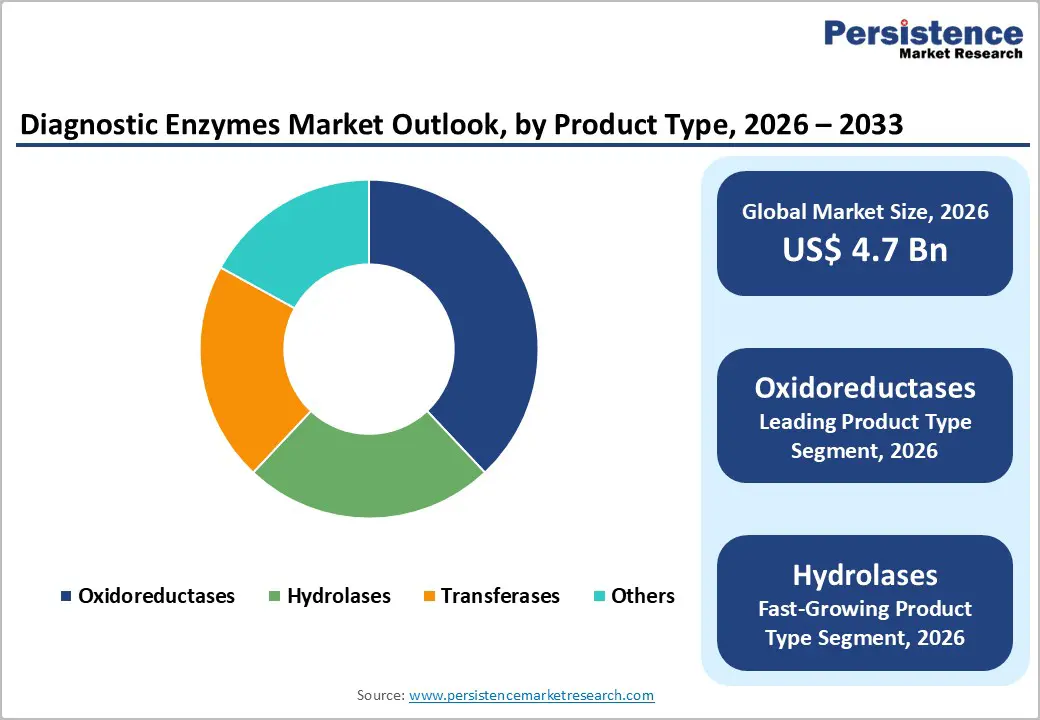

- Among enzyme types, oxidoreductases dominate with around 38% share in 2025, reflecting their critical role in clinical chemistry and biosensor-based assays for glucose, lipids, and cardiac markers, which are among the most frequently ordered diagnostic tests globally.

- Hydrolases represent the fastest-growing enzyme class as advanced immunoassays, molecular workflows, and multiplex platforms increasingly use phosphatases and proteases for signal amplification, sample preparation, and enhanced sensitivity in oncology, cardiology, and infectious disease testing.

| Key Insights | Details |

|---|---|

| Diagnostic Enzymes Market Size (2026E) | US$ 4.7 billion |

| Market Value Forecast (2033F) | US$ 7.6 billion |

| Projected Growth CAGR (2026 - 2033) | 7.2% |

| Historical Market Growth (2020 - 2025) | 6.8% |

Market Dynamics

Drivers - Rising Burden of Chronic and Infectious Diseases and Test Volume Expansion

A key driver for the diagnostic enzymes market is the global rise in chronic diseases such as diabetes, cardiovascular disorders, and cancer, alongside persistent infectious disease threats. Clinical chemistry enzymes such as glucose oxidase, cholesterol esterase, lactate dehydrogenase, and creatine kinase are integral to routine panels used in monitoring metabolic and cardiac health, and test volumes scale directly with disease prevalence and screening intensity. During the COVID-19 pandemic, molecular diagnostic enzymes (notably thermostable polymerases and reverse transcriptases) became critical inputs for RT-PCR assays, creating a structural uplift in manufacturing capacity and supply chains that now supports broader respiratory and infectious disease testing. As laboratories upgrade to higher-sensitivity assays and more comprehensive panels for oncology markers, cardiac biomarkers, and liver and kidney function tests, they require robust enzyme formulations with improved stability, lot-to-lot consistency, and performance under automated conditions. This combination of growing disease burden, guideline-driven screening, and test menu expansion translates into steadily increasing demand for both molecular and clinical diagnostic enzymes across hospitals, diagnostic laboratories, and point-of-care settings.

Acceleration of Molecular Diagnostics, Precision Medicine, and NGS Workflows

Another strong growth driver is the rapid adoption of molecular diagnostics and precision medicine workflows that are fundamentally enzyme-intensive. Techniques such as real-time PCR, digital PCR, isothermal amplification, and next-generation sequencing depend on highly engineered polymerases, ligases, nucleases, and reverse transcriptases optimized for speed, fidelity, and tolerance to inhibitors. As oncology, infectious disease, and genetic disorder testing increasingly shift toward multiplexed panels and NGS-based assays, demand for specialized molecular diagnostic enzymes grows in parallel. Clinical laboratories and reference centers are investing heavily in NGS platforms to support tumor profiling, minimal residual disease monitoring, and hereditary cancer risk assessment, each requiring multiple enzymatic steps from library preparation through amplification and sequencing. At the same time, the rise of syndromic respiratory panels and point-of-care molecular platforms in emergency and urgent care environments is driving demand for enzymes designed for rapid cycling and robust performance with diverse sample matrices. The convergence of precision medicine, companion diagnostics, and decentralized molecular testing thus creates a sustained, technology-driven pull for innovative diagnostic enzyme formulations.

Market Restraints

High Production Complexity, Quality Requirements, and Cost Pressures

Diagnostic enzymes must meet stringent purity, activity, stability, and regulatory requirements, which drives up production complexity and cost. Manufacturing high-performance enzymes typically involves advanced fermentation, purification, and formulation processes, along with detailed quality control to ensure batch-to-batch consistency. For molecular diagnostic enzymes, additional engineering to improve thermostability, fidelity, or resistance to inhibitors further increases development timelines and costs. At the same time, diagnostic laboratories and healthcare systems face strong reimbursement and budget pressures, which limit their willingness to pay premium prices. This combination can compress margins for enzyme manufacturers, particularly smaller producers lacking large-scale fermentation capacity, and can slow adoption of newer, more expensive engineered enzymes even when they offer performance advantages.

Regulatory and Validation Burdens for Diagnostic Enzyme Integration

While diagnostic enzymes are often sold as reagents or components rather than finished tests, they still sit within a tightly regulated in vitro diagnostics (IVD) ecosystem. When IVD manufacturers change enzyme suppliers or upgrade formulations, they may need to perform extensive revalidation and, in some jurisdictions, update regulatory submissions, especially under frameworks such as the U.S. Food and Drug Administration (FDA) requirements or the European Union In Vitro Diagnostic Regulation (IVDR). These validation demands can discourage frequent enzyme switching and make it harder for new suppliers to displace incumbent vendors, even when offering competitive pricing or technical performance. In addition, variability in regulatory expectations across regions increases the complexity for enzyme producers that serve global diagnostic OEMs, potentially slowing global rollout of innovative enzyme technologies and limiting smaller regional players’ ability to scale internationally.

Market Opportunities

Growth of Point-of-Care Testing and Decentralized Diagnostic Platforms

The rapid expansion of point-of-care (POC) and near-patient testing creates a significant opportunity for diagnostic enzymes tailored for rugged, user-friendly platforms. POC tests for infectious diseases, cardiac markers, and metabolic parameters rely on enzymes that perform reliably under ambient conditions, with long shelf life and minimal cold chain requirements. Lateral flow assays, microfluidic cartridges, and integrated lab-on-a-chip systems increasingly incorporate oxidoreductases and hydrolases for signal generation and amplification, often in combination with novel labels and detection chemistries. As health systems implement POC testing in emergency departments, primary care, pharmacies, and home settings, manufacturers of diagnostic enzymes can grow by supplying customized formulations with enhanced stability, one-step reaction profiles, and compatibility with dried or lyophilized formats. Partnerships between enzyme suppliers and POC platform developers, including collaborations with biotechnology and pharmaceutical companies developing companion diagnostics at the point of care, open further opportunities to co-develop assay-specific enzyme blends that underpin differentiated, rapid testing solutions.

Engineered Enzymes for High-Sensitivity, Sustainable, and Automated Diagnostics

Advances in protein engineering, directed evolution, and computational design enable the creation of diagnostic enzymes with improved performance characteristics that align with emerging trends in automation and sustainability. There is a growing need for enzymes that maintain high activity at lower temperatures, tolerate a broad range of pH and buffer conditions, and show resilience to inhibitors present in complex clinical samples, thereby simplifying sample preparation and workflow steps. Engineered oxidoreductases and hydrolases can deliver stronger signals at low analyte concentrations, supporting ultra-sensitive assays for early disease detection in oncology and cardiology. At the same time, improved thermostability and resistance to degradation allow for more efficient shipping, reduced cold chain dependence, and extended reagent on-board stability in automated analyzers, which supports greener, lower-waste laboratory operations. Enzyme suppliers that invest in R&D to develop next-generation biocatalysts with these attributes and that can demonstrate their benefits in automated clinical chemistry and molecular platforms are well placed to capture share in high-growth segments and to participate in co-innovation initiatives with leading IVD manufacturers.

Category wise Analysis

Product Type Insights

Within product type, clinical diagnostic enzymes represent the leading segment, accounting for an estimated 52% market share in 2025, compared with molecular diagnostic enzymes. Clinical diagnostic enzymes are deeply embedded in routine chemistry, immunoassay, and hematology workflows used by hospitals and diagnostic laboratories worldwide to monitor glucose, lipids, liver enzymes, kidney function, and cardiac markers. Because these tests are ordered at high frequency in both inpatient and outpatient settings, the underlying enzyme consumption is substantial and recurring. Enzymes such as glucose oxidase, peroxidase, urease, alkaline phosphatase, and various dehydrogenases are core components of widely adopted automated analyzers from multinational manufacturers, and test volumes scale with chronic disease prevalence and screening guidelines in diabetes, cardiovascular disease, and metabolic syndrome. Molecular diagnostic enzymes, while smaller in absolute share, are growing faster as PCR and NGS assays proliferate, but the entrenched, daily use of clinical chemistry assays keeps clinical diagnostic enzymes in the leading position across the forecast period.

Enzyme Type Analysis

Among enzyme types, oxidoreductases constitute the leading segment with around 38% market share in 2025, reflecting their central role in colorimetric and electrochemical detection systems used in clinical chemistry and point-of-care devices. Oxidoreductases such as glucose oxidase, lactate oxidase, cholesterol oxidase, and various dehydrogenases catalyze redox reactions that can be coupled to chromogenic or amperometric signals, making them ideal for analyzers and biosensors that require robust, measurable outputs. Their dominance is reinforced by the high frequency of tests they power particularly glucose, lipids, and cardiac markers, which are among the most ordered diagnostics globally. Hydrolases represent the fastest-growing enzyme type, supported by expanding use in immunodiagnostics, molecular workflows, and multiplex assay formats. Enzymes like alkaline phosphatase and various proteases are used in signal amplification, substrate conversion, and sample processing, and as immunoassay and nucleic acid technologies evolve toward higher sensitivity and multiplexing, demand for specialized hydrolases with optimized kinetics and stability is accelerating.

Application Insights

In terms of application, infectious diseases form the leading segment with an estimated 34% market share in 2025, reflecting the high test volumes associated with respiratory infections, sexually transmitted infections, bloodstream infections, and hospital-acquired pathogens. Both molecular diagnostic enzymes (for PCR and isothermal amplification) and clinical enzymes (for serology and supporting chemistry tests) play crucial roles in identifying causative organisms, monitoring treatment responses, and implementing infection control measures. The COVID-19 pandemic underscored how quickly infectious disease testing volumes can escalate, driving structural investments into enzyme manufacturing capacity and platform development that now support broader respiratory, gastrointestinal, and vector-borne disease panels. Oncology is one of the fastest-growing application segments, driven by the adoption of molecular assays and NGS for tumor profiling, minimal residual disease detection, and companion diagnostics, all of which rely heavily on polymerases, ligases, nucleases, and other enzymes optimized for high-fidelity amplification and sequencing. Diabetes and cardiology also remain substantial users of diagnostic enzymes due to continuous monitoring requirements and adherence to global clinical guidelines.

Regional Insights

North America Diagnostic Enzymes Market Trends and Insights

North America holds a leading position in the diagnostic enzymes market with approximately 35% share in 2025, driven by a combination of advanced healthcare infrastructure, high per-capita diagnostic spending, and strong presence of multinational IVD manufacturers. The United States accounts for the bulk of regional demand, with a dense network of hospital laboratories and large reference labs that run extensive menus of clinical chemistry, immunoassay, and molecular tests powered by diagnostic enzymes. The region’s high prevalence of chronic diseases, such as diabetes, cardiovascular disease, and cancer, and intensive screening and monitoring practices recommended by organizations like the American Diabetes Association and American Heart Association, translate into consistently high test volumes for enzyme-based assays.

The regulatory environment, overseen by the U.S. Food and Drug Administration (FDA) and Health Canada, supports innovation in diagnostic platforms while requiring robust analytical and clinical validation, which encourages the use of high-quality, well-characterized enzyme reagents. North America also acts as a hub for biotechnology and pharmaceutical R&D, including companies developing novel molecular diagnostics, companion diagnostics, and NGS-based tests, all of which depend on engineered polymerases and other enzymes. Strong venture capital activity in diagnostics and life sciences tools, combined with extensive collaborations between academic medical centers and industry, fosters ongoing demand for cutting-edge enzyme technologies and customized formulations tailored to new assay formats.

Asia Pacific Diagnostic Enzymes Market Trends and Insights

Asia Pacific is the fastest-growing region in the diagnostic enzymes market, supported by rising healthcare expenditure, expanding laboratory infrastructure, and a high burden of infectious and chronic diseases across China, India, Japan, and ASEAN countries. China is rapidly scaling up its hospital and reference laboratory capacity, and has become an important manufacturing base for diagnostic reagents, including enzyme preparations for clinical chemistry and molecular tests. As the country invests in NGS, precision oncology, and large-scale screening programs, demand for high-performance molecular diagnostic enzymes is increasing. Japan, with its advanced healthcare system and aging population, continues to adopt sophisticated automated platforms and molecular diagnostics, creating steady demand for both clinical and molecular enzymes in hospital and commercial labs.

India’s growth is driven by a large population, expanding private diagnostic chains, and government efforts to strengthen laboratory services under national health initiatives, including programs focused on diabetes, cardiovascular disease, tuberculosis, and other infectious diseases. ASEAN countries such as Singapore, Malaysia, Thailand, and Indonesia are building capacity in both public and private sectors, including molecular and point-of-care testing for infectious diseases and non-communicable diseases. The region’s manufacturing advantages and lower production costs also encourage local firms to develop and export diagnostic enzymes and kits, often in partnership with global players. As healthcare access improves and test utilization rises, Asia Pacific is expected to outpace mature markets in growth, particularly in segments like molecular diagnostic enzymes, hydrolases for advanced immunoassays, and enzymes designed for POC platforms tailored to resource-limited settings.

Competitive Landscape

The global diagnostic enzymes market is moderately consolidated with several established players competing on product innovation, enzyme specificity, and supply reliability. Competition centers on developing high-performance, stable, and cost-effective enzymes tailored for clinical chemistry and molecular diagnostics. Firms differentiate through proprietary technologies, enzyme engineering, and broad reagent portfolios that enhance sensitivity and throughput. Strategic partnerships with diagnostic kit manufacturers and expanding distribution networks are common.

Key Developments:

- In October 2025, Proventus Bioscience, a recognized leader in industrial microbial fermentation, launched LifeLore Pathways, a new independent biotech company based in Montreal. Fully focused on early-stage life sciences innovation, LifeLore supported the rapid development of tailor-made microbial solutions across health, nutrition, and environmental applications.

Companies Covered in Diagnostic Enzymes Market

- Thermo Fisher Scientific Inc.

- F. Hoffmann-La Roche Ltd.

- Merck KGaA

- Takara Bio Inc.

- Promega Corporation

- Enzo Life Sciences, Inc.

- Amano Enzyme Inc.

- Codexis, Inc.

- Biocatalysts Ltd.

- Ampliqon A/S

- Sekisui Diagnostics

- BBI Solutions

- New England Biolabs

- QIAGEN N.V.

- Agilent Technologies, Inc.

Frequently Asked Questions

The global diagnostic enzymes market is expected to reach approximately US$ 4.7 billion in 2026, and is projected to grow further to about US$ 7.6 billion by 2033, reflecting a forecast CAGR of around 7.2% over 2026 - 2033.

Demand is driven by the rising prevalence of chronic diseases and infectious diseases, the expansion of routine clinical chemistry and cardiac testing, growth in molecular diagnostics and NGS-based assays, increasing use of point-of-care platforms, and continuous test menu expansion in hospitals and diagnostic laboratories.

North America is the leading region, supported by advanced healthcare infrastructure, high diagnostic spending, extensive hospital and reference laboratory networks, strong regulatory and guideline frameworks, and the presence of major global IVD and life science companies supplying enzyme-powered platforms.

One of the most attractive opportunities lies in engineered enzymes designed for point-of-care and high-sensitivity diagnostics, including thermostable, inhibitor-resistant polymerases and robust oxidoreductases and hydrolases that enable rapid, multiplexed, and decentralized testing in both developed and emerging markets.

Key players include Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd., Merck KGaA, Takara Bio Inc., Promega Corporation, Enzo Life Sciences, Inc., Amano Enzyme Inc., Codexis, Inc., Biocatalysts Ltd., Ampliqon A/S, Sekisui Diagnostics, and BBI Solutions, along with other specialized enzyme and life science reagent companies.