- Oil & Gas

- Crude Oil Assay Testing Services Market

Crude Oil Assay Testing Services Market Size, Share, and Growth Forecast 2026 - 2033

Crude Oil Assay Testing Services Market by Service Type (Total Distillation, Physical Property Testing, Chemical Composition Testing, Product Yield & Fraction Analysis, Blending & Compatibility Analysis, Contaminant / Impurity Analysis), Industry (Oil & Gas, Research & Development), and Regional Analysis, 2026 - 2033

Crude Oil Assay Testing Services Market Size and Trend Analysis

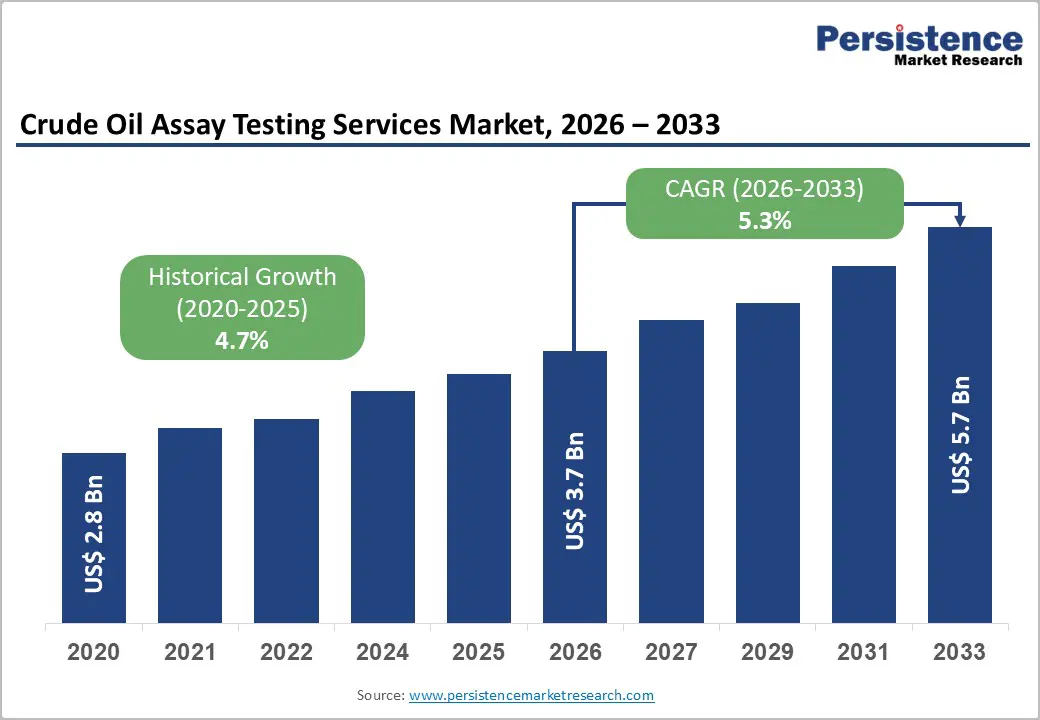

The global crude oil assay testing services market size is likely to be valued at US$ 3.7 billion in 2026 and is projected to reach US$ 5.7 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

Primary growth is driven by the accelerating complexity of global crude slates, tightening environmental and product quality regulations, and the critical role of detailed assay data in optimizing refinery configurations.

According to the International Energy Agency (IEA), global oil demand is expected to plateau near 106 million barrels per day (mb/d) by 2030, with demand growth concentrated entirely in emerging Asian economies, particularly China and India. This geographic concentration intensifies the demand for region-specific crude characterisation, as Asian refiners process an increasingly diverse range of crude types sourced from the Atlantic Basin, Middle East, and non-OPEC producers.

The IEA projects that non-crude products, including natural gas liquids and condensates, will account for 45% of new production capacity additions globally, requiring specialised assay methodologies beyond conventional crude oil testing. These structural forces collectively sustain robust long-term demand for assay testing services.

Key Industry Highlights:

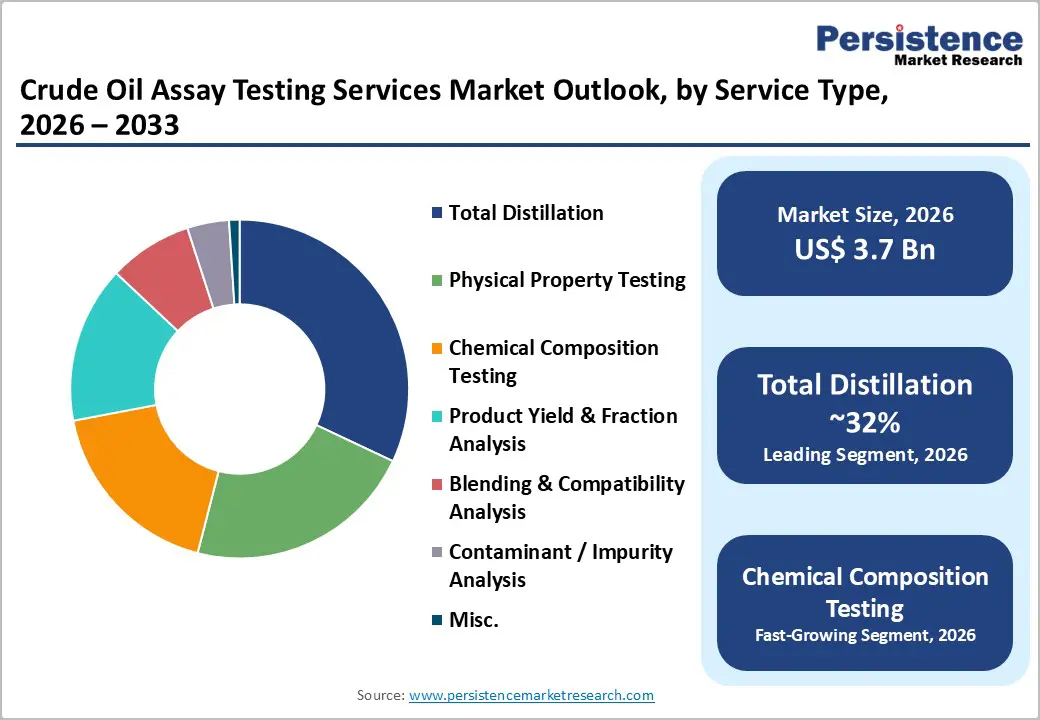

- Leading Service Segment: Total distillation is likely to lead the service type with a 32.0% share in 2026, driven by its universal application in crude yield curve generation across all refinery and trading use cases.

- Fastest-Growing Service Segment: Chemical Composition Testing is the fastest-growing service type, accelerated by IMO 2020 sulfur compliance requirements, proliferation of NGL streams representing 45% of new production capacity additions, and petrochemical integration in Asian refineries.

- Dominant End-user: The oil and gas segment, covering refining, trading, and production support, is likely to account for 78% demand in 2026, anchored by structural refinery feed evaluation and crude procurement workflows.

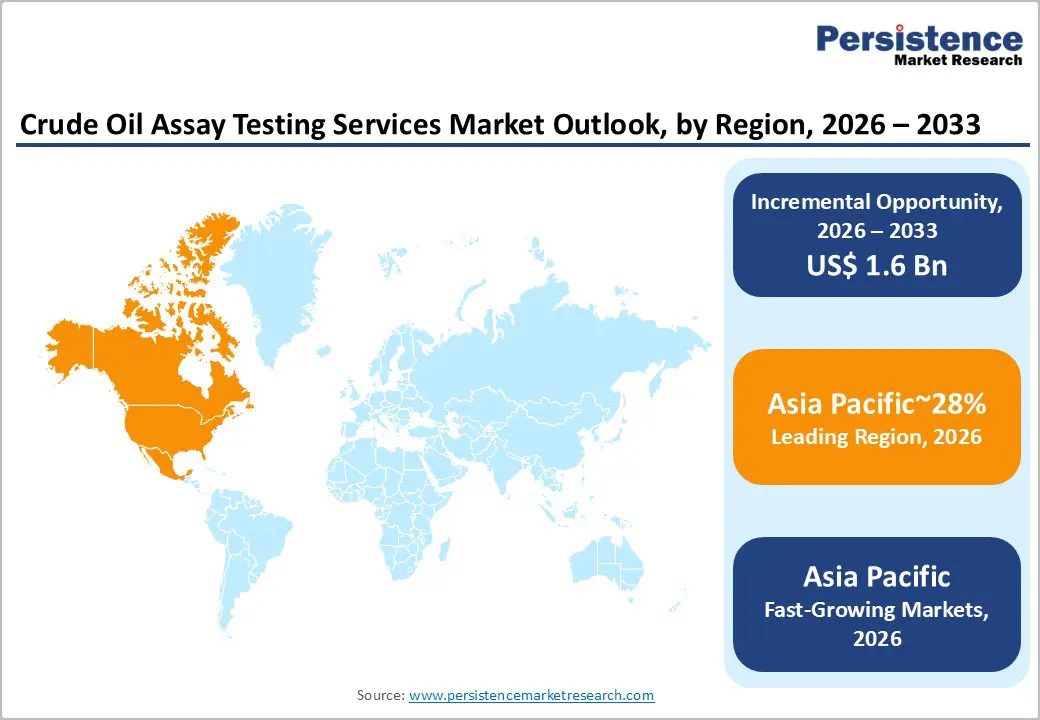

- Regional Leadership: North America commands 28.0% of the global market (US holding US$ 0.8 Bn), followed by Asia Pacific at 26.0%, and MEA.

- Opportunity: IEA data confirms global oil demand plateauing near 106 mb/d by 2030, with demand concentrated in emerging Asian economies, reinforcing Asia Pacific's structural role as the primary long-term growth market for crude oil assay testing services

DRO Analysis

Driver - Diversification of Global Crude Supply and Refinery Feed Complexity

The structural diversification of globally sourced crude blends is compelling refiners to commission far more detailed and frequent crude oil characterisation work, directly stimulating the crude oil assay testing services market. As non-OPEC producers, particularly the United States, Brazil, Guyana, Canada, and Argentina, collectively contribute 4.6 mb/d of net production capacity increases through 2030 per IEA data, refineries are processing crudes with vastly different density, sulfur, metallic contaminant, and distillation profiles. This heterogeneity cannot be managed without rigorous assay data.

The IEA further confirms that global trade flows are shifting eastward, with US light sweet crude, Canadian heavy crude via the Trans-Mountain pipeline, and Middle Eastern grades all increasingly directed toward Asian markets. Asian refiners operating complex hydrocracking and fluid catalytic cracking configurations depend on high-resolution total distillation and physical property testing data to optimise unit performance and meet stringent product specifications. The compounding effect of new crude origins, evolving trade patterns, and refinery configuration upgrades underscores the indispensable role of assay testing in modern refinery economics.

Regulatory Tightening of Fuel Quality and Environmental Compliance Standards

Increasingly stringent fuel quality regulations globally redefine the compliance in the crude oil assay testing services market. Regulatory agencies across the European Union, the United States Environmental Protection Agency, and the International Maritime Organisation have tightened limits on sulfur content in transportation fuels and bunker oil, with the IMO 2020 regulation capping marine fuel sulfur at 0.5% globally. Compliance with these standards requires refiners to conduct detailed chemical composition testing and contaminant analysis to ensure that crude feedstocks and refined products conform to mandated specifications.

The IEA's medium-term outlook notes that while global refining capacity is projected to rise by 3.3 mb/d through 2030, distillate consumption trends are diverging across geographies, placing differential quality demands on refinery output. Regions including Europe and North America face selective shortfalls in diesel and jet fuel, intensifying the importance of product yield and fraction analysis to maximise middle distillate recovery. The intersection of tightening regulatory frameworks with evolving product demand structures is creating a sustained compliance-driven requirement for comprehensive assay testing services across the refining value chain.

Restraints - High Capital and Operational Cost of Advanced Assay Testing Infrastructure

The deployment and maintenance of sophisticated analytical instrumentation required for comprehensive crude oil assay testing, including gas chromatography, mass spectrometry, and high-temperature distillation apparatus, entails significant capital expenditure that constrains market participation to well-capitalized laboratories and service providers. Smaller independent refiners and trading entities in developing markets often find the cost of outsourced assay services prohibitive, limiting addressable demand in price-sensitive geographies.

Operational costs related to sample handling, reagent consumption, equipment calibration, and skilled analyst remuneration further compound financial barriers, particularly for contaminant and impurity analysis workflows that demand advanced analytical precision and regulatory-grade methodology.

Opportunities - Expansion of Assay Testing Demand from Non-Crude Liquid Streams and NGL Characterisation

The IEA projects that non-crude products, particularly natural gas liquids and condensates, will represent 45% of new global production capacity through 2030, with countries such as Saudi Arabia strategically prioritising NGL production over conventional crude expansion. This shift creates a substantial and largely underpenetrated opportunity within the crude oil assay testing services market for service providers to extend their analytical capabilities to condensates, ethane, LPG, and naphtha streams that require customized assay methodologies distinct from conventional crude testing protocols.

Service providers that invest in developing specialised assay frameworks for NGL characterisation, including vapour pressure measurement, compositional analysis by extended gas chromatography, and corrosivity testing, stand to capture incremental revenue from upstream producers and midstream processors managing these new stream categories. As petrochemical feedstock demand is projected to add 3.7 mb/d to global liquids requirements, the precision characterisation of naphtha and ethane feedstocks becomes critical for cracker unit optimisation in integrated refinery-petrochemical complexes. This represents a high-value service adjacency for established assay testing organisations.

Digitalisation of Assay Data Management and Predictive Crude Blending Platforms

The convergence of digital laboratory information management systems, artificial intelligence, and cloud-based crude library platforms is creating a transformative opportunity to deliver value beyond discrete analytical testing. Refinery operations increasingly require integrated digital assay data environments that enable real-time crude selection, blend optimisation, and margin simulation. Service providers that develop or partner with technology firms to offer assay-data-as-a-service platforms can significantly expand their revenue per client and deepen customer stickiness.

The IEA has highlighted that escalating geopolitical risks and fragmented energy markets, including nearly 200 restrictive trade measures introduced since 2020, are compelling refiners to diversify crude sourcing strategies dynamically. Digital assay platforms that maintain live crude libraries updated with fresh physical property and distillation data across multiple origins directly address this strategic need. Partnerships between assay testing laboratories and refinery planning software vendors represent a commercially viable path to developing subscription-based data services that command premium pricing relative to traditional per-sample testing contracts.

Category-wise Analysis

Service Type Insights

Total distillation commands 32.0% of the crude oil assay testing services market, establishing it as the foundational analytical service within the crude oil assay workflow. Distillation testing, encompassing atmospheric and vacuum distillation techniques conducted under standardized ASTM D-86 and D-1160 protocols, provides the fundamental yield curve data that refiners use to configure processing units, establish crude pricing premiums or discounts, and project product slate economics.

As global crude trade flows eastward and refiners process increasingly diverse feedstocks from the Atlantic Basin, Middle East, and non-OPEC producers, the demand for precise distillation characterization across each new crude origin.

Chemical composition testing is the fastest-growing service type within the crude oil assay testing services market, propelled by regulatory compliance requirements, the proliferation of complex crude types, and the expanding use of detailed molecular characterisation in refinery planning. Analysis of sulfur speciation, nitrogen compounds, metallic contaminants such as nickel and vanadium, naphthenic acids, and trace heteroatom content is increasingly required to satisfy environmental regulations, including IMO 2020 sulfur caps and regional low-sulfur fuel standards, as well as to protect refinery catalyst systems from deactivation by metal-bearing crudes.

Industry Insights

The oil and gas end-user segment, including refining, trading, and production support subsectors, commands approximately 78% of the crude oil assay testing services market in 2026, reflecting the sector's foundational reliance on assay data for commercial and operational decision-making. Refinery operators require comprehensive assay data across the full suite of testing categories, from total distillation and physical property measurement to contaminant analysis, to configure processing units, manage crude blending economics, and maintain regulatory compliance.

The IEA projects that global refining capacity will expand by 3.3 mb/d through 2030, with growth concentrated in Asian markets, sustaining robust institutional demand for assay services.

The research and development end-user segment, encompassing commercial laboratories, method development organisations, and academic and energy R&D programs, is the fastest-growing category within the crude oil assay testing services market.

The IEA reports that annual global clean energy investment is approaching USD 2 trillion, and that more than 560 GW of renewable capacity was added in 2023, driving institutional research spending on novel feedstock characterisation, biofuel co-processing compatibility, and low-carbon product certification methodologies. Academic institutions and national energy laboratories are actively commissioning assay testing as part of funded research programs exploring synthetic crude, bio-crude, and waste-derived liquid feedstocks.

Regional Insights

North America Crude Oil Assay Testing Services Market Trends and Insights

North America accounts for an estimated US$ 800 million in 2026, driven by state-of-the-art, technically advanced refining and crude production infrastructure. The region benefits from sustained US tight oil production momentum, with the IEA identifying the United States as one of five non-OPEC producers collectively contributing 4.6 mb/d of net capacity additions through 2030, continuously introducing new crude slates requiring assay characterisation for commercial valuation, refinery feed evaluation, and pipeline scheduling.

U.S. Crude Oil Assay Testing Services Market Size

The United States holds a substantial share in 2026, anchored by its position as the world's top crude oil producer and home to the most extensive network of independent testing laboratories operating under ASTM, EPA, and API-certified protocols. US demand is structurally reinforced by the shale and tight oil production boom, where the continuous introduction of new and highly variable crude slates from the Permian Basin, Eagle Ford, and Bakken formations requires ongoing assay characterization for refinery feed compatibility, blend scheduling, and regulatory product quality compliance.

Asia Pacific Crude Oil Assay Testing Services Market Trends and Insights

Asia Pacific accounts for 26.0% of the global crude oil assay testing services market, the second-largest regional contributor, driven by the combined momentum of refining and petrochemical expansion in China, India, South Korea, Japan, and Southeast Asia. The competitive regional landscape is fragmented, with global testing multinationals competing against local accredited laboratories and captive refinery laboratory operations creating a dual-speed market where pricing pressure from local players coexists with growing premium demand for internationally accredited, high-throughput assay services tied to complex imported crude slate management.

China Crude Oil Assay Testing Services Market Size

China holds an estimated US$ 330 million in crude oil assay testing services market value, the largest national market within Asia Pacific, driven by the country's position as the world's largest petroleum refiner and its simultaneous pursuit of large-scale petrochemical feedstock integration. China accounted for 60% of global new renewable energy capacity additions in 2023 while sustaining intensive petroleum refining investment to meet growing naphtha, LPG, and ethane petrochemical demand, contributing to the projected 3.7 mb/d global increase in petrochemical feedstock requirements through 2030 that is creating systematic demand for precise distillation and chemical composition testing across refinery-petrochemical integrated complexes.

India Crude Oil Assay Testing Services Market Size

India, with an estimated US$ 210 million market value in 2026, is driven by its reliance on imported crude and expanding refinery configurations by IOC, HPCL, and BPCL. The shift toward processing discounted Russian Urals alongside Middle Eastern and U.S. WTI grades has increased crude variability, necessitating more frequent and complex assay characterisation to optimise feedstocks and inform procurement decisions.

Middle East & Africa Crude Oil Assay Testing Services Market Trends and Insights

Middle East & Africa commands 21.0% of the global Crude Oil Assay Testing Services market, underpinned by the region's dual role as the world's largest crude export origin and an increasingly active downstream integration hub where assay testing is simultaneously demanded for export cargo valuation, refinery feed characterisation, and NGL/condensate fraction analysis across a structurally diversifying hydrocarbon product slate.

GCC Countries Crude Oil Assay Testing Services Market Outlook

The GCC constitutes the highest-density concentration of crude oil assay testing demand globally, with Saudi Aramco's structural pivot toward NGL-over-crude production introducing a qualitatively new analytical demand segment centred on gas condensates, C2–C5 NGL fractions, and associated liquids carrying distinct distillation curves, vapour pressure profiles, and chemical composition signatures that require expanded protocols well beyond conventional TBP distillation suites.

The UAE's ADNOC-driven downstream integration, anchored by the active international trading of Murban and Das crude grades under the Abu Dhabi Crude Oil Pipeline system, embeds continuous export valuation and refinery feed assay requirements directly into cargo transfer and joint venture operating agreements. Iraq's government-backed refinery rehabilitation programs at Baiji, Basra, and Karbala complexes, combined with African national oil company modernisation investments in Nigeria, Angola, and South Africa, are collectively expanding the MEA assay testing addressable market across both upstream production support and export-grade crude quality certification functions.

Competitive Landscape

The global crude oil assay testing services market exhibits a fragmented competitive structure, characterised by the coexistence of large multinational testing, inspection, and certification organisations commanding significant share through global laboratory networks, and a diverse ecosystem of regional and specialised providers serving geographically or technically defined niches.

The top five to six players, namely SGS SA, Bureau Veritas, Intertek Group, Core Laboratories, Eurofins Scientific, and MISTRAS Group, collectively anchor the competitive upper tier through laboratory scale, accreditation breadth, and client relationship depth, but no single player commands sufficient share to constitute a consolidated or oligopolistic market structure.

Key Developments:

- April 2026, SGS opened a new crude oil testing laboratory in Bahía Blanca, Argentina, enhancing localised assay capabilities near the Vaca Muerta production hub. The facility enables faster sulfur, density, and contaminant analysis, improving cargo planning, blending decisions, and export quality compliance.

- In 2026, AmSpec Group launched crude assay testing services at its Rio de Janeiro laboratory, deploying advanced PETRODIST distillation systems compliant with ASTM D2892 and D5236 standards. The development strengthens Brazil’s mandatory assay-based pricing and custody transfer framework, enhancing refinery optimisation and trading accuracy.

Companies Covered in Crude Oil Assay Testing Services Market

- SGS SA

- Bureau Veritas

- Intertek Group

- Core Laboratories

- Eurofins Scientific

- MISTRAS Group

- ALS Limited

- TestAmerica (Eurofins)

- Saybolt (Core Lab)

- Exova (Element Materials)

- SOCOTEC Group

- TUV Rheinland

- Petrotechnics

- CESI (RSK Group)

- NABL-Accredited Petroleum Labs

Frequently Asked Questions

The global crude oil assay testing services market is projected to be valued at US$ 3.7 Bn in 2026.

Total distillation leads the crude oil assay testing services market, accounting for approximately 32% share in 2026.

Oil & gas accounts for the largest share of the global crude oil assay testing services market.

The market is expected to witness a CAGR of 5.7% from 2026 to 2033.

Structural diversification of global crude slates combined with tightening fuel quality and environmental regulations is driving continuous demand for advanced crude assay characterisation and compliance testing across refinery operations.

Expansion of assay testing into NGLs and non-crude streams, along with digital assay data platforms enabling real-time crude blending and optimization, represents the key market opportunity.

Key players in the Crude Oil Assay Testing Services Market include SGS SA, Bureau Veritas, Intertek Group, Core Laboratories, Eurofins Scientific, and MISTRAS Group.