- Automotive

- Vehicle Predictive Maintenance Market

Vehicle Predictive Maintenance Market Size, Share, and Growth Forecast 2026 - 2033

Vehicle Predictive Maintenance Market by Component (Software, Services, Hardware), Application (Predictive Maintenance, Vehicle Telematics, Driver & Behaviour Analytics, Fleet Management, Warranty Analytics, Others), Vehicle Type (Passenger Cars, Commercial Vehicles, Electric Vehicles), End-User (OEMs, Fleet Operators, Insurance Providers, Others), and Regional Analysis for 2026 - 2033

Vehicle Predictive Maintenance Market Size and Trend Analysis

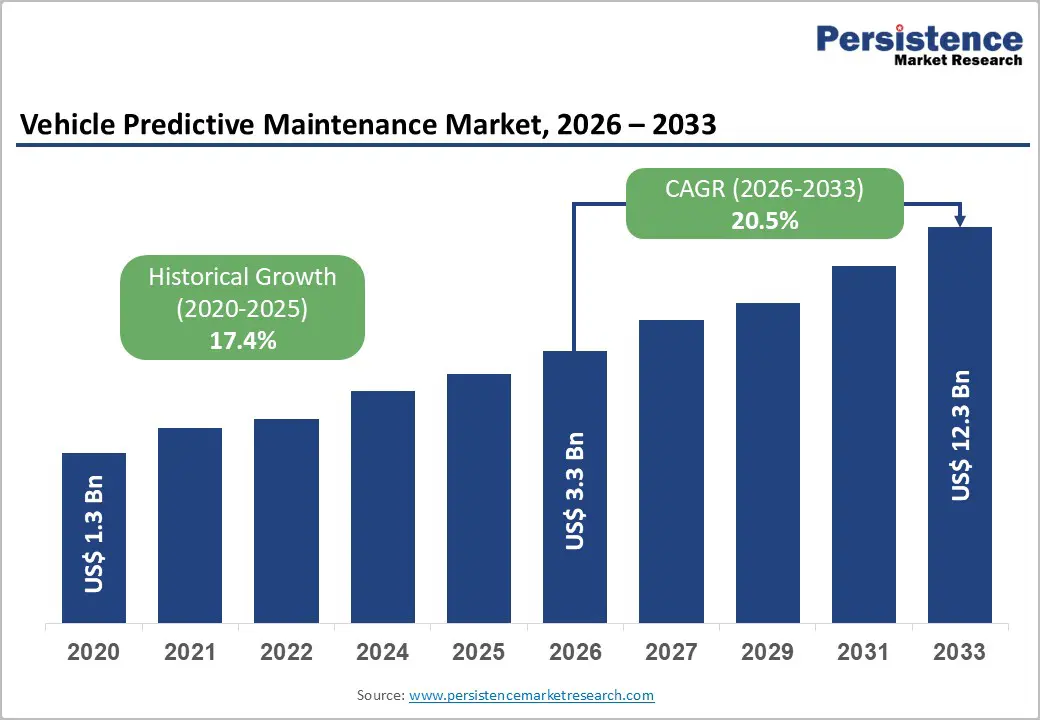

The global vehicle predictive maintenance market is valued at approximately US$ 3.3 billion in 2026 and is projected to reach US$ 12.3 billion by 2033, growing at a CAGR of 20.5% between 2026 and 2033.

This exceptional growth trajectory is driven by the convergence of connected vehicle proliferation, AI-powered analytics maturation, and the escalating operational imperative to eliminate unplanned vehicle downtime across commercial fleets, passenger vehicles, and the rapidly expanding Electric Vehicle (EV) segment. According to the International Energy Agency (IEA), global EV sales surpassed 17 million units in 2024, up 25% year-on-year, massively expanding the addressable market for battery health monitoring and predictive diagnostics.

Key Market Highlights

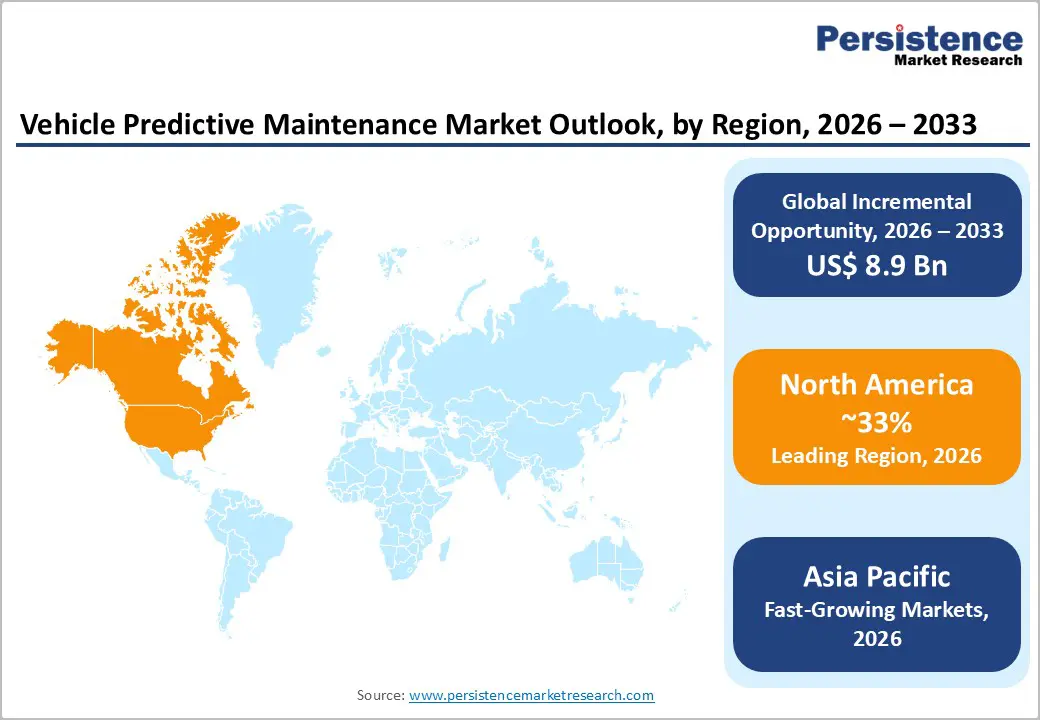

- Leading Region - North America leads the global Vehicle Predictive Maintenance market with approximately 33% revenue share, anchored by the U.S.'s advanced connected-fleet ecosystem, major technology headquarters (IBM, Microsoft, Oracle, PTC), and over 3.2 million EV sales in 2024, expanding battery analytics demand.

- Fastest-Growing Region - Asia Pacific is the fastest-growing region, driven by China's deployment of over 11 million EVs in 2024, Japan's semiconductor-driven edge diagnostics advances, and India's rapid fleet digitization under national EV and commercial vehicle electrification programs.

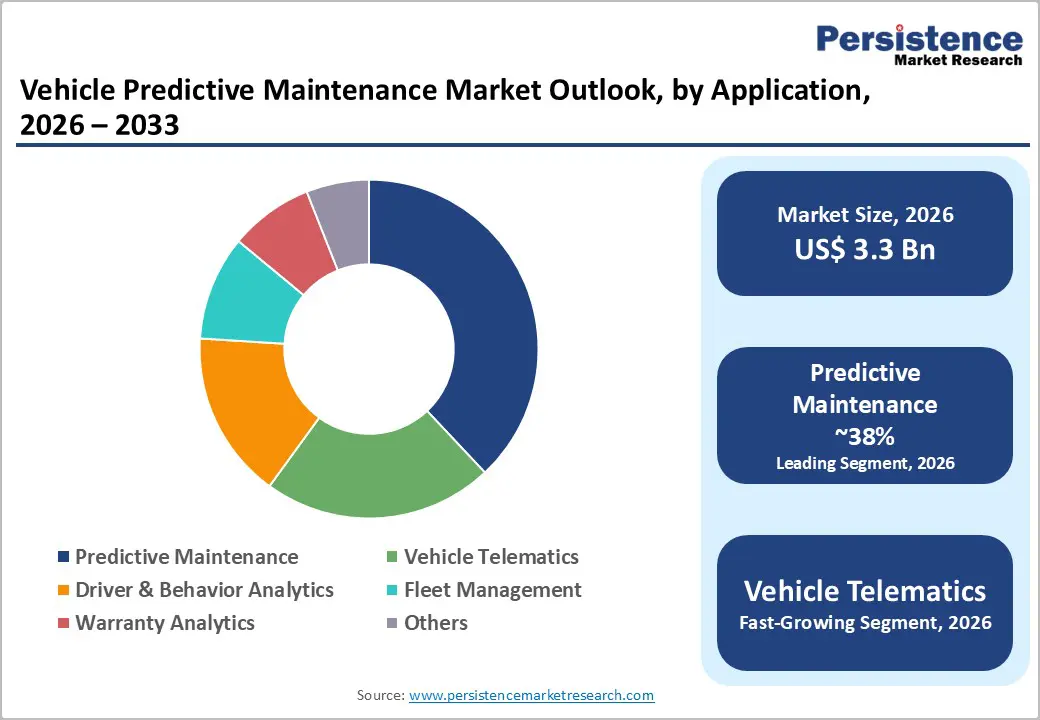

- Dominant Segment - The Software component segment leads with approximately 51% share, driven by AI-powered cloud-native analytics platforms, including IBM MAS 9.0 and Azure IoT services enabling scalable, subscription-based predictive diagnostics for OEMs and fleet operators globally.

- Fastest-Growing Segment - Commercial Vehicles is the fastest-growing vehicle type segment, expanding at over 19% CAGR, as logistics, freight, and transit fleet operators deploy AI-based telematics and predictive platforms to reduce unplanned downtime and optimize total cost of ownership.

- Key Opportunity - The global transition to EVs with sales exceeding 17 million units in 2024 per the IEA is creating high-margin opportunities in battery degradation prediction, remaining-useful-life analytics, and cloud-connected OTA maintenance services for OEMs and fleet operators.

| Key Insights | Details |

|---|---|

| Vehicle Predictive Maintenance Market Size (2026E) | US$ 3.3 Billion |

| Market Value Forecast (2033F) | US$ 12.3 Billion |

| Projected Growth CAGR (2026 - 2033) | 20.5% |

| Historical Market Growth (2020 - 2025) | 17.4% CAGR |

DRO Analysis

Market Growth Drivers

Proliferation of Connected Vehicles and IoT-Enabled Real-Time Diagnostics

The rapid expansion of the connected vehicle ecosystem is the foundational growth driver for the Vehicle Predictive Maintenance market. Modern vehicles are equipped with hundreds of sensors monitoring engine temperature, vibration, tire pressure, battery state-of-health, braking performance, and hundreds of other parameters generating continuous streams of operational data that AI and ML models translate into actionable maintenance predictions.

According to industry data, over 57% of EV buyers now say they are willing to switch vehicle brands to access better connectivity features, according to a McKinsey survey underscoring how central connected diagnostics have become to vehicle ownership expectations. The rise of software-defined vehicles (SDVs) is accelerating this trend, as OTA update architectures enable manufacturers to deploy diagnostic improvements remotely across entire fleets.

Escalating EV Fleet Complexity and Battery Health Monitoring Demand

The explosive growth of Electric Vehicles (EVs) is creating a structurally new and rapidly expanding demand category within the Vehicle Predictive Maintenance market. EV batteries which represent up to 50% of total vehicle costs, require continuous real-time monitoring of state-of-charge (SoC), state-of-health (SoH), temperature cycles, cell balancing, and fault codes to prevent costly failures, thermal incidents, and warranty claims.

The IEA Global EV Outlook 2025 reports that global EV battery production exceeded 1 terawatt-hour (TWh) in 2024 each vehicle requiring sophisticated battery management and predictive analytics systems. LG Energy Solution launched B. once, a battery diagnostic platform capable of identifying key health indicators every 5 minutes, in October 2024. BatteryOK Technologies introduced its AI-enabled EV Doctor across over 1,500 EV service centers globally in January 2025.

Restraints - Data Privacy Concerns and Cybersecurity Vulnerabilities in Connected Vehicles

The Vehicle Predictive Maintenance market faces significant restraints from growing concerns over the privacy and security of vehicle-generated data. Connected predictive maintenance platforms collect and transmit sensitive data, including location, driving behavior, vehicle health metrics, and owner identity, raising regulatory and consumer concerns under frameworks such as GDPR in Europe and emerging data protection mandates in the Asia Pacific.

The proliferation of connected attack surfaces in modern vehicles has prompted the UNECE WP.29 to introduce Regulation No. 155 on cybersecurity management systems for vehicles, creating compliance requirements that increase platform development costs for solution providers.

High Integration Complexity and Legacy Infrastructure Compatibility

Many commercial fleet operators and smaller OEMs face significant barriers in integrating predictive maintenance platforms with existing vehicle electronics, legacy telematics systems, and enterprise IT infrastructure. Diverse ECU architectures, proprietary OBD-II protocols, and fragmented data formats across vehicle manufacturers create interoperability challenges that delay deployment and raise implementation costs.

According to the Deloitte Global Manufacturing Outlook 2024, 82% of companies have experienced at least one unplanned outage yet widespread adoption of predictive maintenance remains hampered by the technical complexity of integrating heterogeneous vehicle data streams into unified analytics platforms.

Opportunities - EV Battery Predictive Analytics and Over-the-Air Maintenance Services

The accelerating transition to Electric Vehicles presents one of the most transformative opportunities for Vehicle Predictive Maintenance market participants, particularly in battery lifecycle management and OTA service delivery. As the IEA reports global EV sales exceeding 17 million units in 2024, the cumulative installed base of EVs requiring battery health analytics is expanding exponentially.

Batteries degrading faster than expected generate warranty claims and customer safety risks creating compelling OEM demand for AI-powered degradation models and remaining-useful-life (RUL) prediction systems. Robert Bosch GmbH announced plans to invest more than €2.5 billion (approximately US$ 2.9 billion) in AI by 2027, with a significant portion targeting automotive predictive analytics and maintenance solutions.

Fleet Management and Insurance Telematics Integration

The convergence of predictive maintenance with fleet management and Usage-Based Insurance (UBI) programs represents a high-growth adjacent opportunity for solution providers in the Vehicle Predictive Maintenance market. Commercial fleet operators, including logistics, last-mile delivery, ride-hailing, and rental companies are adopting predictive platforms that reduce unplanned downtime by 20-25%, per Deloitte analysis of the trucking industry. IBM projects that AI-driven fleet management can improve fuel efficiency by 15-20%.

Insurance providers are leveraging vehicle telematics and driver behavior analytics to offer personalized UBI products that reward safe, well-maintained vehicles with lower premiums creating sustained demand for analytics platforms embedded across OEM, fleet operator, and insurer value chains. COMPREDICT and Renault Group announced a predictive maintenance partnership in September 2024 using virtual sensors to deliver real-time component health data without additional hardware, reducing the total cost of ownership for OEMs and their fleet customers.

Category-wise Analysis

Component Insights

The Software segment leads the global Vehicle Predictive Maintenance market, holding approximately 51% of total revenue in 2026. Software dominance reflects the market's evolution from hardware-centric data collection toward intelligent analytics platforms that generate actionable maintenance predictions, optimize service scheduling, and deliver AI-driven insights to OEMs, fleet operators, and insurers.

Cloud-native predictive maintenance platforms including IBM Maximo Application Suite (MAS) version 9.0 (launched June 2024 with AI-driven predictive maintenance and expanded IoT integration) and Microsoft Azure IoT services, are anchoring enterprise-grade deployments. Subscription-based and SaaS software delivery models are lowering the total cost of entry for mid-market fleet operators and enabling continuous improvement through algorithm updates.

Application Insights

The predictive maintenance application segment leads the global Vehicle Predictive Maintenance market, accounting for approximately 38% of revenue in 2026. The segment's leadership is rooted in its direct economic impact, enabling fleet operators and OEMs to avoid unplanned breakdowns that cost manufacturers an average of US$ 260,000 per hour in downtime costs per the Deloitte Global Manufacturing Outlook 2024.

AI models now achieve 85% precision in predicting component failures weeks or months in advance, translating directly into optimized maintenance scheduling and spare parts procurement. The Fleet Management application is the second-largest segment, driven by rising logistics and last-mile delivery fleet complexity. Vehicle Telematics is the fastest-growing application, propelled by OEM-native connected car platforms and the global expansion of usage-based insurance (UBI) models that rely on real-time vehicle data.

Vehicle Type Insights

Passenger cars lead the global vehicle predictive maintenance market, likely to account for approximately 74% of total revenue in 2026. This dominance reflects the sheer scale of the global passenger vehicle fleet, with over 1.4 billion motor vehicles in operation worldwide according to the International Organization of Motor Vehicle Manufacturers (OICA) and the rapid penetration of connected car technologies across premium and mid-range segments.

Consumers increasingly expect real-time vehicle health monitoring, predictive service alerts, and seamless integration between OEM apps and service centers. Commercial Vehicles represent the second-largest segment but are growing at the fastest pace, projected at over 19% CAGR, driven by logistics, freight, and public transportation operators adopting telematics-based predictive platforms. The Electric Vehicles segment is the fastest-emerging category, with battery health monitoring and RUL prediction becoming critical OEM differentiators.

End-user Insights

OEMs (Original Equipment Manufacturers) are the dominant end-user segment in the global Vehicle Predictive Maintenance market, holding approximately 63% of total revenue in 2026. OEMs are the natural anchor for predictive maintenance deployment, as they own the vehicle data architecture, control OTA update capabilities, and bear warranty liability creating a direct commercial incentive to predict and prevent component failures before warranty claims are triggered.

Robert Bosch GmbH, Continental AG, and ZF Friedrichshafen AG are investing heavily in AI-powered predictive diagnostics integrated with their OEM hardware portfolios. Fleet Operators represent approximately 28% of end-user revenue, and their adoption is accelerating as logistics and transportation companies digitize operations under competitive pressure to reduce total cost of ownership. Insurance Providers represent a fast-growing niche, deploying vehicle telematics data to enable personalized, behavior-adjusted premium models.

Regional Analysis

North America Vehicle Predictive Maintenance Market Trends

North America leads the global Vehicle Predictive Maintenance market, commanding approximately 33% of global revenue in 2026, anchored by the United States' advanced connected-fleet ecosystem, mature IoT infrastructure, and the headquarters presence of market leaders including IBM, Microsoft, Oracle, and PTC. The U.S. market benefits from widespread telematics adoption across commercial logistics, last-mile delivery, ride-hailing, and rental sectors all of which are deploying AI-based predictive platforms as competitive operational tools. U.S. federal standards from the National Highway Traffic Safety Administration (NHTSA) on vehicle safety, combined with state-level EV mandates, reinforce the investment case for advanced diagnostics infrastructure.

AWS expanded its predictive maintenance offerings in March 2024 with new IoT services providing enhanced data collection for automotive applications. IBM unveiled Maximo Application Suite (MAS) 9.0 in June 2024 featuring AI-driven predictive maintenance with expanded IoT integration for real-time vehicle asset monitoring.

Asia Pacific Vehicle Predictive Maintenance Market Trends

Asia Pacific is the fastest-growing region in the global Vehicle Predictive Maintenance market, propelled by the world's largest automotive manufacturing base, the most aggressive EV transition programs, and rapidly expanding logistics and commercial fleet operations. China leads both as the world's largest vehicle producer and the global leader in EV deployment with over 11 million EVs sold domestically in 2024, according to IEA data, generating an immense and growing installed base requiring battery health monitoring, remote diagnostics, and over-the-air service capabilities.

Japan is home to NXP Semiconductors applications and major OEMs, including Toyota, Honda, and Nissan is advancing predictive maintenance through partnerships with semiconductor and software companies, focusing on edge computing for real-time diagnostics. India is a high-growth market, with BatteryOK Technologies deploying its AI-enabled EV Doctor across over 1,500 EV service centers in January 2025 and national fleet operators digitizing maintenance operations under the government's push for electric bus and commercial vehicle adoption. ASEAN markets, particularly Thailand, Indonesia, and Vietnam, are expanding commercial vehicle fleets and attracting OEM manufacturing investment, creating growing demand for predictive maintenance infrastructure.

Europe Vehicle Predictive Maintenance Market Trends

Europe holds a substantial and technologically sophisticated position in the global Vehicle Predictive Maintenance market, driven by the world's most stringent automotive regulatory framework and the headquarters concentration of major OEMs and Tier-1 automotive suppliers. Germany is home to Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, and SAP SE, which is the region's dominant market, with advanced predictive maintenance capabilities embedded throughout its automotive production ecosystem. Robert Bosch announced an investment of over €2.5 billion in AI by 2027, with automotive predictive analytics as a core application.

UK and France are significant markets, with Renault Group's September 2024 partnership with COMPREDICT for virtual sensor-based predictive maintenance illustrating the region's co-innovation dynamics between OEMs and specialized AI software vendors. Spain, Italy, and the Nordic countries are investing in connected fleet infrastructure. The EU's UNECE Regulation No. 155 on cybersecurity management systems, mandatory for type approvals since July 2024, is elevating data security standards across predictive maintenance platforms, shaping investment priorities for software vendors targeting European OEM and fleet operator customers.

Competitive Landscape

The global vehicle predictive maintenance market is moderately consolidated, with technology giants and automotive-domain specialists competing across complementary layers of the value stack. IBM, Microsoft, and SAP SE dominate the enterprise software and AI analytics tier, while Robert Bosch GmbH, Continental AG, and ZF Friedrichshafen AG lead on hardware integration and OEM-embedded diagnostic platforms. PTC and SAS Institute serve specialized industrial and predictive analytics niches. Key differentiators include AI model accuracy, edge-to-cloud data pipeline efficiency, OEM data partnerships, and compliance with automotive cybersecurity standards (UNECE R155/R156).

Key Developments:

- In August 2025, Force Motors introduced iPulse, which is a connected vehicle platform powered by AI-driven fleet intelligence and predictive analytics, as being standard in its commercial vehicles. It provides real time vehicle information developed with Intangles, which improves efficiency and saves expenses.

- In April 2025, PTC and Schaeffler advanced their collaboration by adopting Windchill+, PTC’s cloud-native PLM platform with integrated AI capabilities. This transition enables Schaeffler to speed up predictive maintenance workflows, improve component lifecycle management, and leverage cloud-driven analytics across automotive systems to enhance reliability and development efficiency.

Companies Covered in Vehicle Predictive Maintenance Market

- IBM

- SAP SE

- Cloud Software Group, Inc.

- Continental AG

- Microsoft

- NXP Semiconductors

- Oracle

- PTC

- Robert Bosch GmbH

- SAS Institute Inc.

- ZF Friedrichshafen AG

Frequently Asked Questions

The global Vehicle Predictive Maintenance market is estimated to be valued at US$ 3.3 Billion in 2026 and is projected to reach US$ 12.3 Billion by 2033, registering a CAGR of 20.5% during the forecast period 2026 - 2033.

The primary drivers are the proliferation of connected vehicles and IoT-enabled real-time diagnostics, the explosive growth of EVs requiring battery health monitoring (IEA reports 17+ million EV sales in 2024), and the staggering economic cost of unplanned downtime US$ 260,000 per hour per Deloitte's 2024 data.

The Software component segment leads the global Vehicle Predictive Maintenance market with approximately 51% of revenue share in 2025. Software dominance reflects the market's evolution toward AI-powered cloud-native analytics platforms that translate raw sensor and telematics data into actionable maintenance predictions.

North America leads the global Vehicle Predictive Maintenance market with approximately 33% of revenue share in 2025, driven by the United States' advanced connected-fleet ecosystem, widespread commercial telematics adoption, and the headquarters concentration of leading technology companies including IBM, Microsoft, Oracle, and PTC.

The leading companies in the global Vehicle Predictive Maintenance market include Robert Bosch GmbH, IBM Corporation, Microsoft Corporation, Continental AG, SAP SE, NXP Semiconductors, Oracle, PTC Inc., SAS Institute Inc., and ZF Friedrichshafen AG. Robert Bosch leads in hardware-integrated automotive AI solutions, IBM leads in enterprise asset management and fleet predictive analytics through Maximo, and Microsoft anchors the cloud and IoT infrastructure tier.