- Healthcare Services

- U.S. Assisted Living Facility Market

U.S. Assisted Living Facility Market Size, Share, and Growth Forecast, 2026 – 2033

U.S. Assisted Living Facility Market by Ownership Type (Chain Affiliated, Independent Owned), Age (More than 85, 75–84, 65–74, Less than 65), and Service (Personal Care Assistance, Medical Monitoring, Others), and Zone Analysis for 2026 – 2033

U.S. Assisted Living Facility Market Size and Trends Analysis

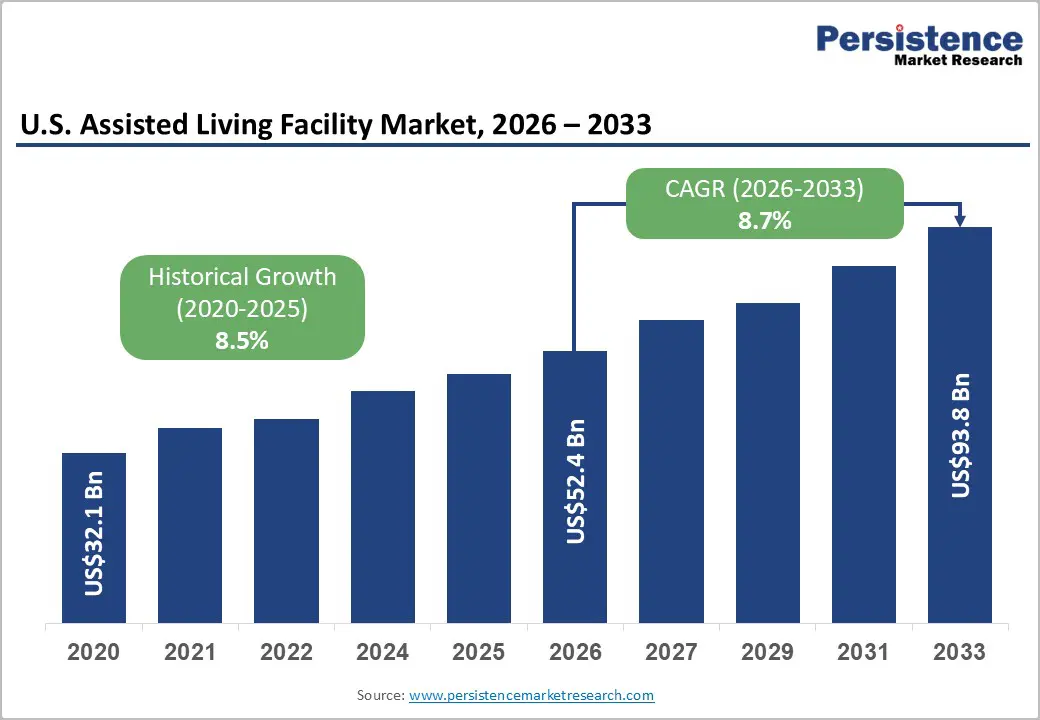

The U.S. assisted living facility market size is likely to be valued at US$52.4 billion in 2026 and is expected to reach US$93.8 billion by 2033, growing at a CAGR of 8.7% during the forecast period from 2026 to 2033, driven by the rapidly aging population and the growing need for long-term supportive care services that allow seniors to maintain independence while receiving assistance with daily activities.

Assisted living communities provide a combination of housing, healthcare support, personal care services, and social engagement programs designed to improve the quality of life for older adults who do not require intensive medical care offered in nursing homes. The increasing prevalence of age-related conditions such as dementia, mobility limitations, cardiovascular disorders, and diabetes has significantly increased the demand for professional caregiving and supervised living environments. Changing family structures, rising life expectancy, and the growing number of elderly individuals living alone have strengthened the demand for structured senior living communities that offer safety, companionship, and healthcare monitoring.

Key Industry Highlights:

- Leading Ownership Type: Chain-affiliated facilities are projected to represent the leading ownership type in 2026, accounting for 56% of the revenue share, driven by their large networks, standardized services, and stronger operational capabilities across multiple assisted living communities.

- Leading Age Type: The more than 85 age group is anticipated to be the leading age type, accounting for over 49% of the revenue share in 2026, supported by high demand for daily living assistance, chronic disease management, and specialized memory and mobility care.

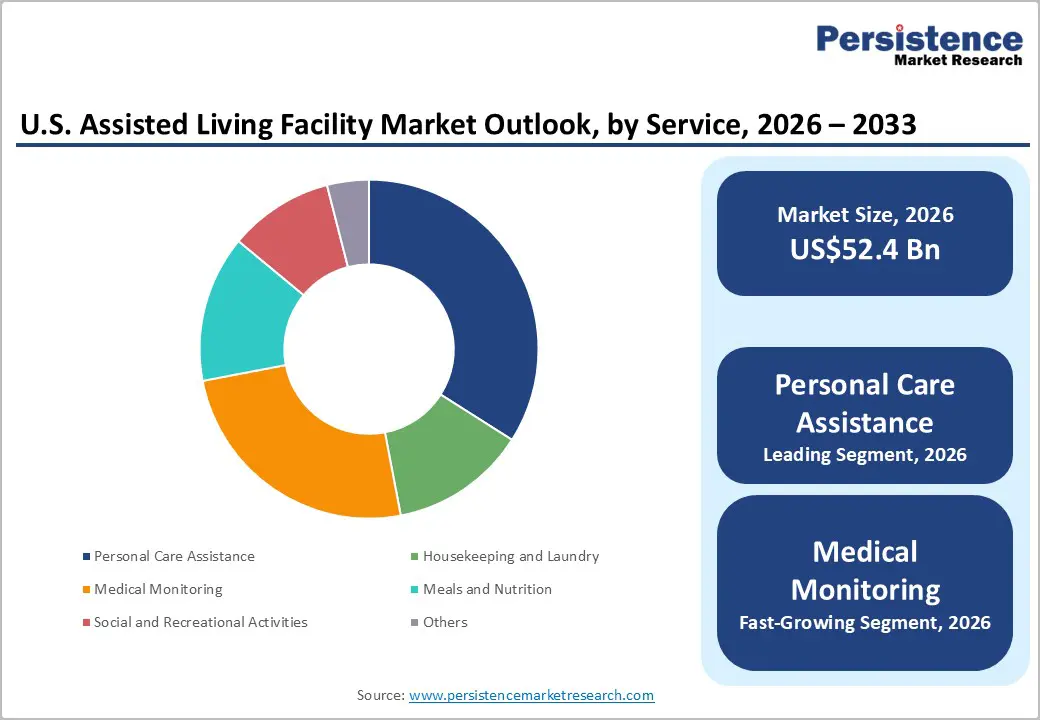

- Leading Service Type: Personal care assistance is estimated to represent the leading service type in 2026, accounting for 35% of the revenue share, driven by the growing need for support with daily living activities such as bathing, dressing, mobility assistance, and medication management among elderly residents in assisted living facilities.

| Key Insights | Details |

|---|---|

| U.S. Assisted Living Facility Market Size (2026E) | US$52.4 Bn |

| Market Value Forecast (2033F) | US$93.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Aging Population and Demographic Shifts

The U.S. assisted living facility market is strongly driven by the rapidly aging population. The number of adults aged 65 and older continues to grow, increasing demand for senior care services that balance independence with support for daily living activities. Aging demographics result in a larger pool of residents requiring medical monitoring, personal care, and social engagement, fueling the expansion of assisted living communities. Facilities are adapting to meet diverse health and mobility needs while offering age-appropriate amenities, including memory care units, mobility assistance, and wellness programs, making demographic shifts a primary driver of market growth.

The demographic trend also encourages investment in senior housing infrastructure, as families increasingly prefer community-based care over institutional nursing homes. With life expectancy rising, seniors are living longer, often with multiple chronic conditions requiring ongoing care. This creates opportunities for facilities to provide integrated services such as rehabilitation, nutrition management, and social activities tailored to elderly residents. Regional variations in aging populations influence market penetration, with high-density elderly areas attracting more facility development.

Value-Based Care and Medicare Advantage Penetration

Assisted living facilities benefit as reimbursement policies increasingly reward preventive care, reduced hospital readmissions, and chronic disease management. Facilities integrate these models to provide comprehensive care plans, including monitoring for chronic illnesses, medication adherence, and early interventions, aligning financial incentives with improved resident health. By participating in value-based programs, operators can enhance care quality while maintaining profitability, promoting adoption of structured care pathways and evidence-based interventions that improve long-term health outcomes for residents.

Value-based care encourages facilities to expand specialized services such as memory care and rehabilitation, improving resident retention. It also drives standardization of operational protocols across multiple facility locations, improving overall efficiency and care consistency.

The penetration of medicare advantage also encourages partnerships between assisted living operators and healthcare providers, facilitating care coordination, data sharing, and remote health monitoring. Facilities can leverage predictive analytics to manage high-risk residents, optimizing resource allocation and enhancing patient satisfaction. With increased reimbursement options, facilities can invest in staff training, technology, and wellness programs, aligning with regulatory requirements and quality metrics. These partnerships support the integration of telehealth services and AI-driven monitoring systems, enabling continuous care for residents with chronic conditions. They also allow facilities to implement proactive population health management strategies, reducing hospital admissions and enhancing long-term operational sustainability.

Barrier Analysis - Workforce Shortages and Staffing Challenges

The high demand for personalized care services is challenging facilities to maintain sufficient staffing levels while ensuring quality and compliance with regulations. Turnover rates are significant due to physically and emotionally demanding work, low wages, and limited career growth opportunities. Staffing gaps can affect resident safety, service delivery, and overall satisfaction, leading to increased operational costs and potential regulatory penalties, making workforce shortages a persistent barrier to sustainable market growth.

Staff shortages can delay the adoption of advanced care technologies such as remote monitoring and AI-driven health analytics. They also hinder the expansion of specialized care units, such as memory care or post-acute rehabilitation, limiting market growth potential.

Facilities are adopting strategies such as recruitment incentives, staff training programs, and partnerships with vocational institutions, but challenges remain. Geographic disparities exacerbate shortages, especially in rural areas where demand is rising but qualified personnel are scarce.

Facilities face challenges in retaining specialized staff for memory care and chronic disease management, critical for high-dependency residents. Staffing issues also limit the ability to expand services, adopt new technologies, and meet increasing occupancy demands. High turnover increases reliance on temporary staffing agencies, raising operational costs and affecting continuity of care. Limited availability of skilled geriatric nurses also impacts facilities’ ability to meet regulatory quality standards and maintain resident satisfaction.

Fragmented Supply Chain for Specialized Equipment

Assisted living facilities often rely on a fragmented supply chain for specialized medical and mobility equipment, creating operational inefficiencies. Procurement of devices such as patient lifts, monitoring systems, mobility aids, and medical beds can be inconsistent, leading to delays and higher costs. Small or independent facilities are particularly affected, as they lack the economies of scale enjoyed by chain-affiliated operators. Equipment shortages can disrupt care delivery, compromise resident safety, and limit the adoption of advanced monitoring or rehabilitation technologies.

Fragmentation also complicates maintenance, technical support, and timely upgrades of essential devices, which are critical for resident care and regulatory compliance. Facilities may face challenges integrating new equipment with existing digital health systems or electronic health records, reducing operational efficiency. Variability in quality and supplier reliability can increase risk, particularly for high-dependency residents needing specialized care. Consolidation or partnerships with trusted suppliers are emerging solutions, but until the supply chain becomes more streamlined, fragmented equipment procurement remains a notable restraint, affecting both service quality and market scalability.

Opportunity Analysis - Integration of AI and Predictive Health Technologies

Facilities can leverage AI-driven monitoring systems, predictive analytics, and wearable devices to anticipate resident health events, manage chronic conditions, and reduce hospitalizations. These tools allow staff to proactively intervene, optimize care plans, and enhance operational efficiency, improving both resident outcomes and satisfaction. Predictive technologies also support resource allocation, helping facilities identify high-risk residents, streamline workflows, and reduce unnecessary costs while maintaining high-quality care standards.

AI-driven insights help in managing occupancy trends and planning capacity for high-dependency units, while assisting in preventive care strategies to reduce emergency interventions. Facilities can also use predictive modeling to forecast staffing needs and optimize scheduling, improving workforce efficiency in high-demand areas.

AI integration enables personalized and adaptive care experiences, aligning services with resident preferences and medical needs. Remote monitoring, telehealth, and AI-enabled alerts facilitate real-time decision-making and reduce response times during emergencies. Facilities can use data insights for strategic planning, compliance reporting, and performance benchmarking. Technology adoption also supports scalability, allowing operators to expand services without proportionally increasing staffing levels.

AI tools help track resident engagement in wellness and recreational programs, enhancing satisfaction and retention. Integration also enables facilities to meet regulatory reporting requirements more efficiently, supporting audits and quality assurance initiatives.

Partnerships with Value-Based Care Providers

Collaborating with hospitals, accountable care organizations, and healthcare networks allows facilities to implement coordinated care models, reduce hospital readmissions, and optimize chronic disease management. Such partnerships facilitate the sharing of medical data, joint care planning, and early interventions, ensuring that residents receive comprehensive, outcomes-focused services while aligning with reimbursement incentives under Medicare and other value-based programs. These partnerships enable assisted living facilities to integrate preventive care programs and chronic condition management protocols, improving overall resident health outcomes.

These collaborations also support the expansion of specialized services such as rehabilitation, telehealth, and memory care programs. By aligning with healthcare providers, facilities can access additional resources, training, and technology, improving staff capabilities and resident satisfaction. Partnerships also help operators differentiate their offerings, attract new residents, and enhance community reputation. Such collaborations enable facilities to adopt population health management strategies, monitor health trends across residents, and implement data-driven care plans. They also improve regulatory compliance by ensuring quality reporting standards are met and assist in optimizing operational efficiency across multiple facility locations.

Category-wise Analysis

Ownership Type Insights

Chain-affiliated assisted living facilities are expected to lead, accounting for approximately 56% of revenue in 2026, owing to their strong presence and standardized operations across multiple sites. These facilities benefit from economies of scale, centralized procurement, and consistent branding, which allow them to maintain higher occupancy rates than independent operators. For example, Brookdale Senior Living operates numerous chain-affiliated facilities nationwide, providing standardized healthcare, wellness programs, and social engagement services to residents. Their scale allows investment in staff training, technology adoption, and memory care units, giving them a competitive edge.

Independent-owned facilities are likely to represent the fastest-growing segment, supported by flexibility, local customization, and niche services, allowing them to cater to underserved markets. Many independent operators focus on specialized offerings such as LGBTQ+ inclusive care, culturally specific programs, or unique wellness services, increasing resident satisfaction and engagement. For example, Sonida Senior Living has successfully expanded independent facilities offering personalized care models and smaller community environments, appealing to families seeking a more home-like setting.

Franchising models allow independents to access technology, marketing, and operational tools without full consolidation, enhancing competitiveness.

Age Type Insights

The more than 85 age group is projected to lead the market, capturing around 49% of the revenue share in 2026, supported by residents in this cohort requiring higher levels of care, including assistance with daily living, memory care, and mobility support. Facilities prioritize specialized units to meet these needs, ensuring 24/7 supervision and tailored healthcare services. For example, Atria Senior Living offers dedicated memory care and high-dependency units, supporting residents with chronic conditions while providing structured social and recreational programs.

The demand stems from increased prevalence of multiple chronic diseases, cognitive decline, and mobility limitations in this age group, necessitating extensive healthcare support.

The less than 65 age group is likely to be the fastest-growing age type, driven by the increasing prevalence of early-onset disabilities and chronic conditions requiring assisted living services. Transitional care needs post-hospitalization and rehabilitation programs for younger residents contribute to the rising demand. For example, Integral Senior Living provides adaptive care environments for residents under 65, offering physical therapy, occupational therapy, and social support tailored to younger adults with neurological or mobility challenges.

Policy shifts toward community-based services and individualized care options support the adoption of these facilities, while families seek flexible, home-like environments that allow independence alongside medical assistance.

Service Type Insights

Personal care assistance is estimated to lead the U.S. assisted living facility market, accounting for approximately 35% of revenue in 2026, due to the core service for residents needing help with activities of daily living (ADLs) such as bathing, dressing, mobility, and medication management. Facilities ensure compliance with state mandates while providing structured and consistent support. For example, Five Star Senior Living integrates personal care assistance with wellness programs, meals, and recreational activities, helping residents maintain dignity and independence while meeting healthcare needs.

The high demand for this service is driven by chronic mobility issues, cognitive impairment, and the aging population’s reliance on daily support. Bundled service offerings increase resident retention, satisfaction, and overall operational efficiency, highlighting why personal care assistance maintains the leading market position.

Medical monitoring is likely to represent the fastest-growing segment in 2026, driven by the adoption of digital health technologies and remote patient monitoring to manage chronic conditions effectively. Facilities increasingly use wearable devices, AI-driven monitoring systems, and electronic health record integration to track resident health in real-time. For example, Kindred Healthcare incorporates telehealth and predictive analytics to reduce hospitalizations, optimize care plans, and ensure timely intervention for high-risk residents.

The growth of medical monitoring is also driven by rising chronic disease prevalence, the need for personalized care, and regulatory support for preventive healthcare models. As assisted living operators expand these services, they enhance resident safety, improve operational efficiency, and reduce healthcare costs, positioning medical monitoring as a critical growth segment for the market.

Competitive Landscape

The U.S. assisted living facility market exhibits a moderately fragmented structure, driven by the presence of numerous national, regional, and local operators that compete for residents across diverse geographic areas. Major national chains leverage large multi state portfolios and strong brand recognition to secure market share, while independent and regional providers retain significant influence by offering personalized, community centered services. Market competition is intensified by demographic trends, increasing care demand, and rising consumer expectations for quality, technology integration, and specialized programs.

With key leaders including Brookdale Senior Living, Atria Senior Living, Sunrise Senior Living, Five Star Senior Living, and Sonida Senior Living, the competitive environment is marked by expansion strategies, mergers, and service innovation. These companies compete through differentiation of care models, the adoption of advanced health technologies, and the expansion of facility networks to capture growing demand in both urban and underserved regions. Facilities also emphasize enhanced wellness programs, resident engagement initiatives, and integrated medical services to strengthen market appeal and foster long term occupancy, with technology adoption and partnerships emerging as key competitive levers.

Key Industry Developments:

- In March 2026, Pegasus Senior Living announced a major expansion of its senior living footprint in the Greater Houston area by planning six new communities across Sugar Land, Webster, Clear Lake, West University, and Memorial City, significantly increasing local assisted living, independent living, and memory care options for elderly residents. The Dallas based operator, which already has a substantial presence with approximately 2,000 units statewide, stated the expansion is aimed at strengthening access to integrated care and support services for seniors and their families, including social engagement and wellness programs.

- In September 2025, the global consulting firm SJ Group launched dedicated Healthcare Advisory Services to support senior living and care industry leaders in strategic planning, capital allocation, and operational resilience tailored to assisted living, memory care, and related residential care facilities. The new advisory arm is designed to help operators make data driven decisions, optimize facility planning, and adapt to evolving industry challenges such as aging populations and shifting care models, strengthening the competitive positioning of assisted living providers.

Companies Covered in U.S. Assisted Living Facility Market

- Kindred Healthcare

- Brookdale Senior Living

- Sunrise Senior Living

- Sonida Senior Living

- Atria Senior Living, Inc

- Five Star Senior Living (AlerisLife)

- Merrill Gardens

- Centers for Dialysis Care

- Integral Senior Living (ISL)

- Belmont Village, L.P.

- Centre for Neuro Skills

- Mary Lee Foundation

Frequently Asked Questions

The U.S. assisted living facility market is projected to reach US$52.4 billion in 2026.

The U.S. assisted living facility market is driven by the rapidly aging population and increasing demand for personalized senior care services.

The U.S. assisted living facility market is expected to grow at a CAGR of 8.7% from 2026 to 2033.

Key market opportunities in the U.S. assisted living facility market include the integration of AI-driven health technologies and strategic partnerships with value-based care providers.

Kindred Healthcare, Brookdale Senior Living, Sunrise Senior Living, Sonida Senior Living, and Atria Senior Living are the leading players.