- Hardware & Software IT Services

- Unified Endpoint Management Market

Unified Endpoint Management Market Size, Share, and Growth Forecast 2026–2033

Unified Endpoint Management Market by Component (Solutions, Services), by Deployment (Cloud-Based, On-Premises, Hybrid), Organization Size (Large Enterprises, Small & Medium Enterprises (SMEs)), Vertical (BFSI, IT & Telecom, Healthcare, Government & Public Sector, Retail & eCommerce, Manufacturing, Transportation & Logistics, Energy & Utilities, Others), by Regional Analysis, 2026–2033

Global Unified Endpoint Management (UEM) Market Size and Trend Analysis

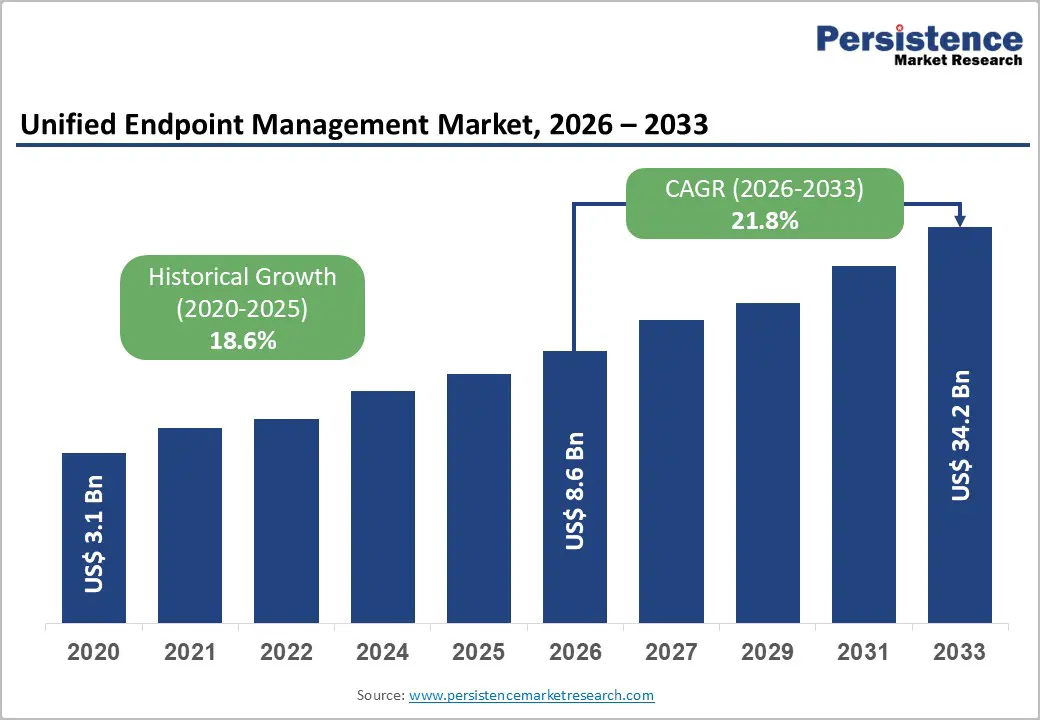

The global unified endpoint management market is expected to be valued at US$ 8.6 billion in 2026 and is projected to reach US$ 34.2 billion, growing at a CAGR of 21.8% between 2026 and 2033, due to the rapid expansion of hybrid workforces and Bring Your Own Device (BYOD) policies is compelling enterprises to adopt unified endpoint management (UEM) platforms capable of securing and managing laptops, smartphones, tablets, rugged devices, and IoT endpoints through a single control layer.

Rising cyber threats, ransomware incidents, and regulatory compliance pressures are further intensifying the need for centralized endpoint visibility, automated patch management, and Zero Trust enforcement across distributed IT environments.

Key Industry Highlights:

- Leading Component: Solutions are likely to dominate with a 68% share in 2026, valued at approximately US$ 5.85 billion, driven by enterprise demand for unified control across device onboarding, policy enforcement, application management, and security compliance.

- Fastest Growing Deployment: Cloud-based deployment is the fast-growing segment, driven by scalability, zero-touch provisioning, and real-time global endpoint visibility across distributed workforces.

- Leading Organization Size: Large enterprises are likely to dominate with over 72% share in 2026, valued at more than US$ 6.19 billion, due to their need to manage highly complex, multi-device, multi-geography endpoint ecosystems with centralized governance and compliance enforcement.

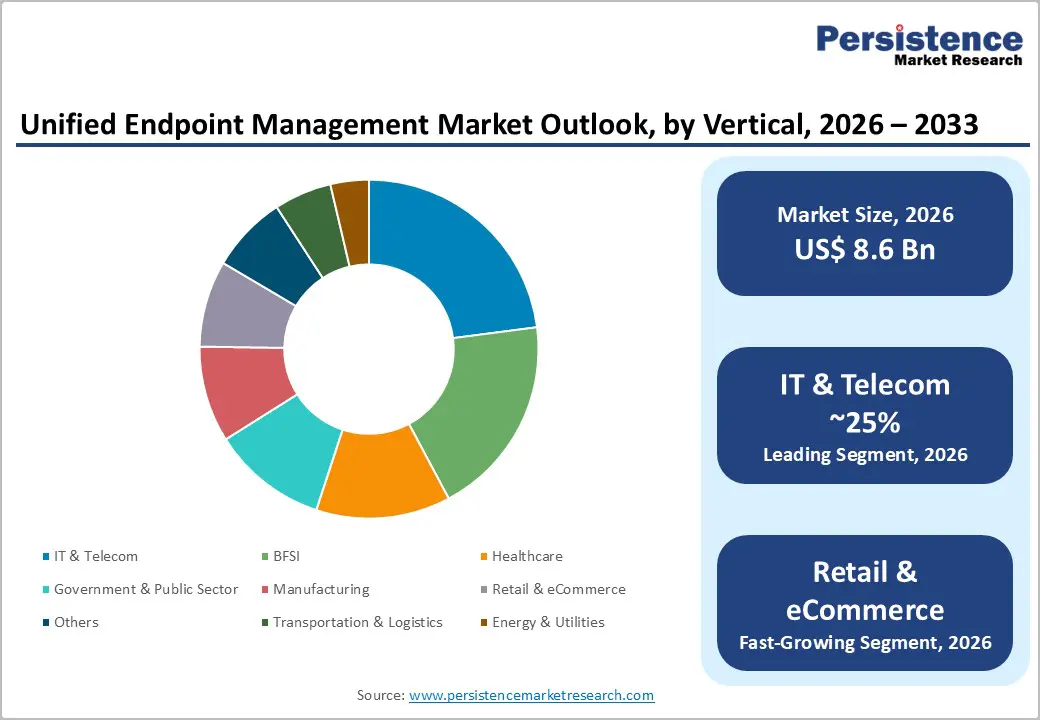

- Leading Vertical: The IT & Telecom vertical is likely to lead with over 25% share in 2026, valued at approximately US$ 2.15 billion, driven by large-scale distributed device environments and high requirements for automation, security, and interoperability.

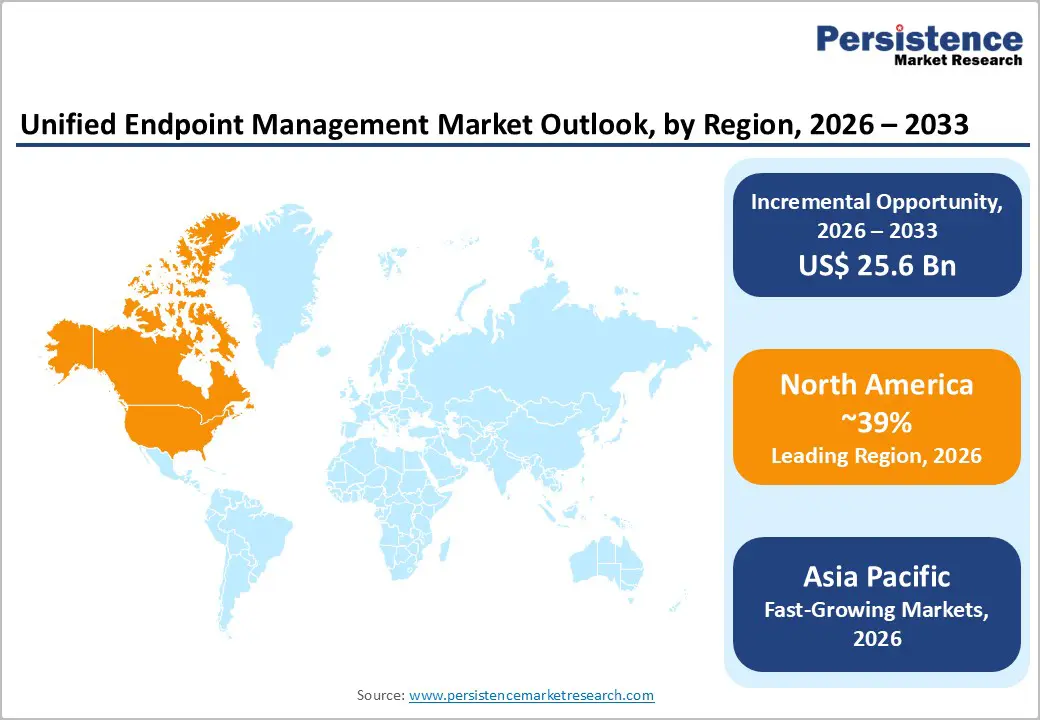

- Leading Region: North America leads the global market with over 39% share in 2026, valued at around US$ 3.35 Billion, supported by strong cybersecurity maturity and mandated Zero Trust adoption across federal and enterprise ecosystems.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, expanding at a CAGR of 26.4%, driven by rapid digital transformation, 5G device proliferation, and tightening national cybersecurity regulations across major economies.

Market Dynamics

Drivers - Zero Trust Architecture Mandates Reshape Enterprise Endpoint Procurement

Enterprise endpoint management is increasingly driven by regulatory compliance rather than discretionary IT spending, making it a critical governance requirement. The U.S. Office of Management and Budget’s M-22-09 memorandum mandates federal agencies to implement Zero Trust architecture, requiring continuous device verification and endpoint visibility. This has effectively made Unified Endpoint Management (UEM) platforms essential infrastructure for compliance enforcement. Vendors such as IBM have strengthened integration between UEM solutions and Zero Trust policy engines to serve federal agencies and contractors. As supply-chain security requirements expand, private enterprises aligned with government ecosystems are adopting similar frameworks. This is significantly broadening the addressable market for compliant endpoint management solutions.

Explosion of IoT and Unmanaged Endpoint Diversity Demands Unified Governance

The rapid proliferation of connected devices across industries is creating unmanaged complexity that legacy endpoint tools cannot handle. With billions of IoT connections globally, enterprises now face a highly fragmented and expanded attack surface across IT, OT, and edge environments.

Traditional mobile device management systems are insufficient for managing rugged devices, sensors, kiosks, and industrial endpoints. This is driving demand for platforms capable of providing centralized visibility, security, and policy enforcement across heterogeneous device types. Vendors like Ivanti are extending UEM capabilities to support IoT and operational technology environments. The need for unified governance is therefore a direct response to escalating operational and cybersecurity risks.

Restraints - Integration Complexity with Legacy IT Infrastructure Suppresses Adoption Velocity

Deploying unified endpoint management across existing enterprise environments frequently requires re-architecting directory services, certificate authorities, and network access control layers a process that routinely extends project timelines by six to eighteen months and inflates total cost of ownership well beyond initial licensing estimates. The National Institute of Standards and Technology (NIST) SP 800-124 revision 2, published in 2023, catalogues the technical prerequisites for mobile device management interoperability with enterprise identity systems, underscoring that integration readiness not platform capability is the primary deployment bottleneck.

Data Residency Regulations Create Multi-Jurisdiction Deployment Friction

Organizations operating across multiple legal jurisdictions face compounding compliance costs when deploying cloud-hosted UEM platforms, as device telemetry and configuration data must often remain within national boundaries under local privacy law. The European Union's General Data Protection Regulation (GDPR), combined with Germany's Federal Data Protection Act (BDSG) amendment, imposes strict restrictions on transferring endpoint management telemetry outside the EU, forcing vendors to maintain regionally isolated cloud infrastructure at material capital expense.

For new market entrants without pre-built regional data centre footprints, this regulatory reality translates to an estimated 20–30% cost premium on EU-compliant cloud UEM deployments compared to single-region architectures, creating a structural barrier that protects established hyperscale-backed vendors.

Opportunities - AI-Driven Autonomous Endpoint Remediation Enables a Premium UEM Tier

AI-native automation is emerging as a high-value differentiation layer within the Unified Endpoint Management market, particularly for mid-to-large enterprises prioritising security efficiency and operational resilience. Vendors that embed machine learning–driven remediation into UEM workflows are enabling automated patch sequencing, policy enforcement, and self-healing endpoints, reducing reliance on manual IT intervention.

Early implementations by players such as CrowdStrike illustrate improving mean-time-to-remediate and stronger endpoint compliance outcomes, reinforcing enterprise appetite for automation-led security operations. This shift is translating into willingness to pay premium subscription pricing for autonomous capabilities versus conventional UEM feature sets. Access to large-scale, heterogeneous endpoint telemetry will become a structural advantage, allowing leading vendors to refine model accuracy and deepen platform stickiness.

Platform Consolidation (Security + UEM Convergence) Creating New Growth Opportunity

Platform consolidation is emerging as a key opportunity as enterprises increasingly replace fragmented endpoint, mobility, and security tools with integrated platforms. The convergence of UEM with endpoint security, identity management, and device compliance functions is reducing operational complexity and lowering the total cost of ownership. This shift is being driven by demand for unified visibility, faster threat response, and centralized policy enforcement across all devices.

Vendors offering combined UEM and security capabilities are securing larger enterprise contracts and higher platform stickiness. This consolidation is expected to reposition UEM as a core layer within broader enterprise security and IT operations ecosystems.

Category-wise Analysis

Component Insights

Solutions segment accounts for 68.0% of the global UEM market in 2026 driven by the need for unified control across device onboarding, policy enforcement, application distribution, and security compliance. Enterprises increasingly require a single platform to eliminate fragmentation caused by multiple endpoint tools and to ensure consistent governance across hybrid work environments. It helps with operational simplicity, reduced security gaps, and faster compliance enforcement at scale. Large organizations prioritize integrated solutions to manage diverse device ecosystems efficiently and maintain continuous visibility.

Services segment is the fast-growing, driven by rising demand for implementation support, integration assistance, and continuous optimization of UEM environments. Enterprises increasingly lack in-house expertise to manage evolving endpoint complexity and AI-driven policy tuning. This creates a strong demand for managed services that ensure ongoing security configuration and performance optimization. Service-based models also support continuous adaptation to new device types and threat landscapes.

Deployment Insights

The on-premises deployment model accounts for over 32% share in 2026, reaching over US$ 2.75 Billion, due to the need for data sovereignty and strict internal control. Highly regulated industries require local infrastructure to ensure sensitive endpoint data does not leave controlled environments. For compliance assurance, air-gapped security, and full administrative control over endpoint telemetry and policy enforcement it is important. Organizations in defense and critical infrastructure sectors continue to rely on on-premises UEM to meet strict regulatory obligations and operational security requirements.

Cloud-based deployment is the fast-growing segment, driven by the need for scalability, rapid provisioning, and simplified global device management. Enterprises increasingly require zero-touch onboarding and centralized policy deployment across distributed workforces. Cloud adoption reduces IT overhead and enables real-time endpoint visibility across geographies. This model also supports faster integration with modern IT ecosystems and hybrid work environments.

Organization Size Insights

Large enterprises hold for over 72% share in 2026, surpassing the value US$ 6.19 billion, since it manages vast and complex endpoint ecosystems. These organizations require centralized governance across thousands of devices spanning multiple operating systems, ownership models, and geographies. It helps in risk reduction through unified compliance enforcement, security standardization, and real-time endpoint monitoring. Large enterprises also prioritize endpoint control to reduce breach exposure and maintain regulatory alignment across global operations.

Small & medium enterprises (SMEs) represent the fast-growing segment, driven by the need for affordable, scalable, and easy-to-deploy endpoint management solutions. SMEs increasingly require cloud-based UEM tools that eliminate heavy infrastructure investment while providing enterprise-grade security. The growth is also supported by rising cyber risk awareness and insurance-driven security requirements.

Vertical Insights

The IT & Telecom vertical accounts for more than 25% of the global unified endpoint management market in 2026, driven by the need to manage highly distributed and heterogeneous endpoint environments. Telecom operators and IT service providers require unified control across network operations, field devices, and enterprise systems. Automation of device lifecycle management, consistent security enforcement, and seamless integration with digital infrastructure drive this vertical. It demands high scalability and interoperability to support large-scale, multi-network operations.

The retail & e-commerce vertical is the fast-growing segment, due to the need to manage large fleets of POS systems, handheld devices, and store-level endpoints. Retailers increasingly require centralized control for kiosk mode enforcement, application whitelisting, and payment security compliance. Operational consistency across thousands of distributed store locations is essential for ensuring smooth retail operations on a scale. The growth is further accelerated by stricter payment security standards and the expansion of digital retail ecosystems.

Regional Insights

North America Unified Endpoint Management Market Trends and Insights

North America accounts for over 39.0% of the global unified endpoint management market in 2026, representing approximately US$ 3.35 Billion, due to deep enterprise cybersecurity maturity and early Zero Trust adoption across both public and private sectors. The region’s growth is structurally reinforced by the U.S. Executive Order 14028 on Improving the Nation’s Cybersecurity (2021), further operationalised through CISA guidance between 2022–2024, which has embedded endpoint visibility and policy enforcement into federal procurement frameworks. Hyperscale cloud penetration and high enterprise security spending across regulated industries continue to accelerate platform adoption.

The United States unified endpoint management market is likely to register over 85% of the North America regional market in 2026, driven by large-scale federal and enterprise modernization initiatives. Compliance frameworks such as the Federal Information Security Modernization Act (FISMA) and funding mechanisms like the Technology Modernization Fund continue to mandate endpoint-level visibility, control, and security enforcement across civilian agencies and defence contractors. Rising cyber insurance compliance requirements and continuous federal contract renewals are reinforcing sustained enterprise investment momentum through the forecast period.

Europe Unified Endpoint Management Market Trends and Insights

Europe unified endpoint management (UEM) market hold over 26% of the global share in 2026, reaching US$ 2.24 billion, due to regulatory enforcement intensity rather than discretionary IT modernization. The enforcement of NIS2 in October 2024 has expanded mandatory cybersecurity compliance across critical infrastructure entities, directly increasing demand for continuous endpoint monitoring, incident response readiness, and supply-chain security controls. The Digital Operational Resilience Act (DORA), effective from January 2025, is reinforcing endpoint resilience validation requirements across the BFSI sector.

Germany unified endpoint management market is expected to exceed the value US$ 0.49 Billion by 2026, supported by its large industrial base and Industry 4.0-driven convergence of IT and operational technology environments. The country’s Mittelstand manufacturers are increasingly deploying unified endpoint governance to secure interconnected production systems and hybrid enterprise networks. Regulatory guidance from the Federal Office for Information Security (BSI), including IT-Grundschutz baselines, is reinforcing standardized UEM adoption in enterprise and industrial deployments. The United Kingdom growth is supported by the National Cyber Strategy 2022 and Cyber Essentials certification requirements that institutionalize endpoint security and patch management across thousands of organizations.

France's UEM market growth is anchored by large-scale public sector digitization under France Relance and sustained cybersecurity modernization across government and healthcare institutions. The ANSSI SecNumCloud framework is reinforcing sovereign cloud requirements for endpoint management platforms used in sensitive environments, shaping procurement preferences toward compliant vendors. The rollout of DORA compliance obligations across major French financial institutions is accelerating enterprise-wide endpoint resilience investments.

Asia Pacific Unified Endpoint Management Market Trends and Insights

The Asia Pacific unified endpoint management (UEM) is expected to reach US$ 1.98 billion and is projected to reach a CAGR of 26.4%, driven by enterprise-wide digital transformation, rapid expansion of 5G-connected endpoints, and tightening national cybersecurity and data protection regulations across major economies. Increasing cloud infrastructure penetration by providers such as AWS, Alibaba Cloud, and Tata Communications is also reducing deployment barriers in emerging Southeast Asian enterprise markets, accelerating UEM adoption at scale.

China holds over 38.0% share of the Asia Pacific UEM market in 2026, reaching US$ 750 million, supported by strict enforcement of the Multi-Level Protection Scheme (MLPS 2.0) mandating continuous endpoint monitoring and compliance for regulated industries. Financial institutions and state-owned enterprises have significantly expanded UEM deployments post-2023 to meet MLPS Level 3 audit requirements, ensuring real-time device posture visibility across critical systems.

Japan unified endpoint management (UEM) market is expected to surpass US$ 0.40 Billion value, due to stricter compliance obligations under the amended APPI and accelerated government and healthcare digitization programs, including AMED-led hospital network security upgrades and national cloud migration initiatives.

India unified endpoint management (UEM) market is expected to grow at a robust rate, supported by the Digital Personal Data Protection Act, which is driving formalized endpoint governance across enterprises handling personal data at scale. Vendors such as Zoho ManageEngine are gaining strong traction by offering cost-efficient, locally compliant UEM platforms tailored for IT services firms and financial institutions.

Competitive Landscape

The global unified endpoint management market is moderately concentrated and competitive, with a small group of leading vendors collectively accounting for nearly half of total market revenue, driven by strong installed base scale, deep enterprise procurement relationships, and tight integration with identity and security ecosystems. Competition is increasingly defined by the depth of AI-driven automation capabilities, the breadth of cross-platform device support, and the ability to function as a credible Zero Trust policy enforcement layer.

Key Developments:

- In December 2025, Microsoft introduced major updates to Microsoft 365 and Microsoft Intune, enhancing cross-platform device management, security policies, and automation capabilities across enterprise endpoints. The updates strengthen Intune’s role in enforcing Zero Trust-based access control and unified endpoint governance across Windows, macOS, iOS, and Android devices.

- In January 2025, Ivanti released Neurons for the UEM platform version 2025.1, introducing AI-powered vulnerability prioritisation that automatically correlates device posture data with real-time threat intelligence feeds to generate ranked remediation queues without human analyst intervention.

Companies Covered in Unified Endpoint Management Market

- Microsoft Corporation

- Omnissa, LLC

- Ivanti, Inc.

- IBM

- Citrix Systems, Inc.

- Zoho Corporation Pvt. Ltd.

- BlackBerry Limited

- Jamf Holding Corp.

- Mitsogo Technologies Private Limited

- SOTI Inc.

- Cisco Systems, Inc.

- Sophos Group plc

- Dell Technologies Inc.

- Matrix42 AG

- Others

Frequently Asked Questions

The global unified endpoint management market is valued at US$ 8.6 billion in 2026 and is projected to reach US$ 34.2 billion by 2033 at a CAGR of 21.8%, driven by the need for unified control of expanding, diverse enterprise device environments under Zero Trust frameworks.

The growth is driven by the need to meet strict cybersecurity compliance requirements like EU NIS2 and to manage increasing endpoint complexity. Enterprises also need faster AI-enabled remediation to reduce security response time and operational risk.

Solutions segment dominates with over 68.0% share in 2026, as enterprises require centralized platforms for managing multiple device types. The need for unified governance and compliance across endpoints creates high switching costs, reinforcing adoption stickiness.

North America leads with a more than 39.0% share in 2026 due to strong cybersecurity spending and strict federal Zero Trust mandates. The region’s enterprises increasingly need scalable endpoint security and compliance across large, distributed IT environments.

A key opportunity lies in AI-driven autonomous endpoint management that reduces manual intervention in security and compliance tasks. Enterprises increasingly require platforms that improve efficiency, reduce risk, and lower operational overhead through automation.

The companies include Microsoft Corporation, Omnissa, LLC, Ivanti, Inc., IBM, Citrix Systems, Inc., Zoho Corporation Pvt. Ltd. and among others.