- Mining & Services

- Tungsten Carbide Powder Market

Tungsten Carbide Powder Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Tungsten Carbide Powder Market by Application (Mining Tools, Cutting Tools, Dies & Punching, Abrasives, and Others), End use Industry (Building & Construction, Oil & Gas, Transportation, Mining, Aerospace & Defense, and Others), and Regional Analysis for 2026 - 2033

Tungsten Carbide Powder Market Size and Share Analysis

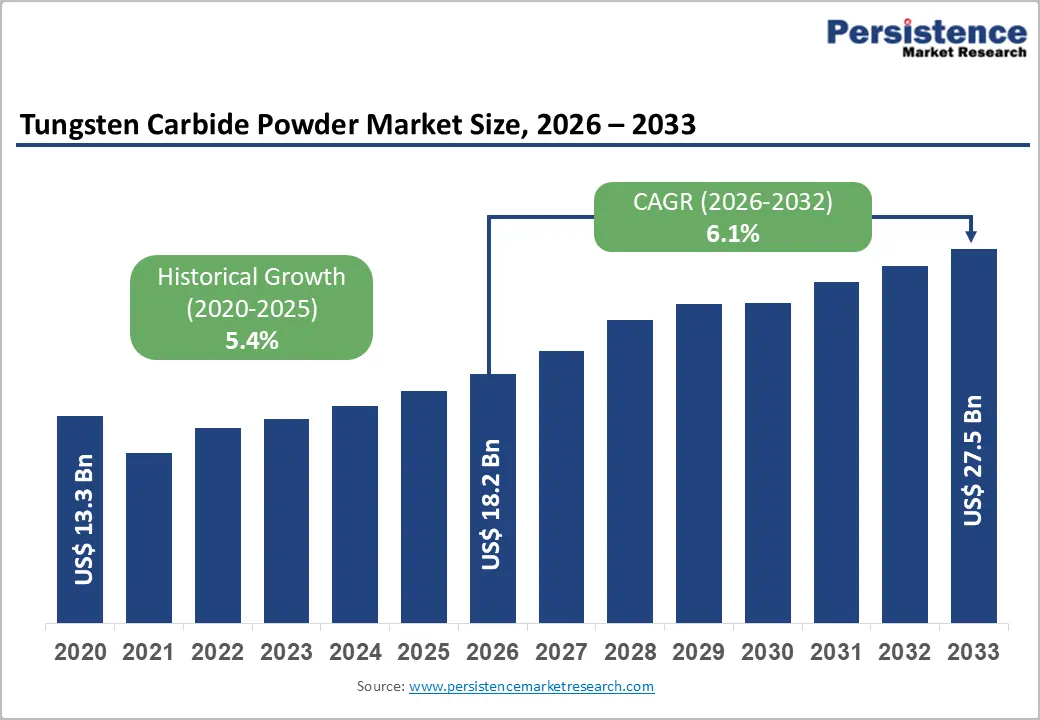

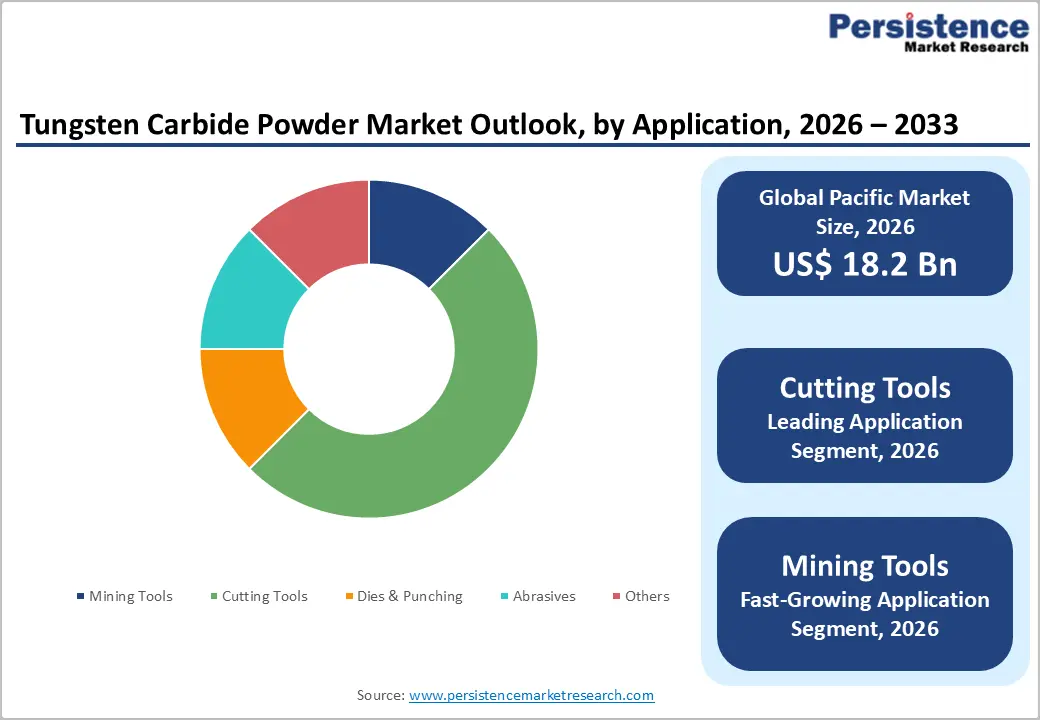

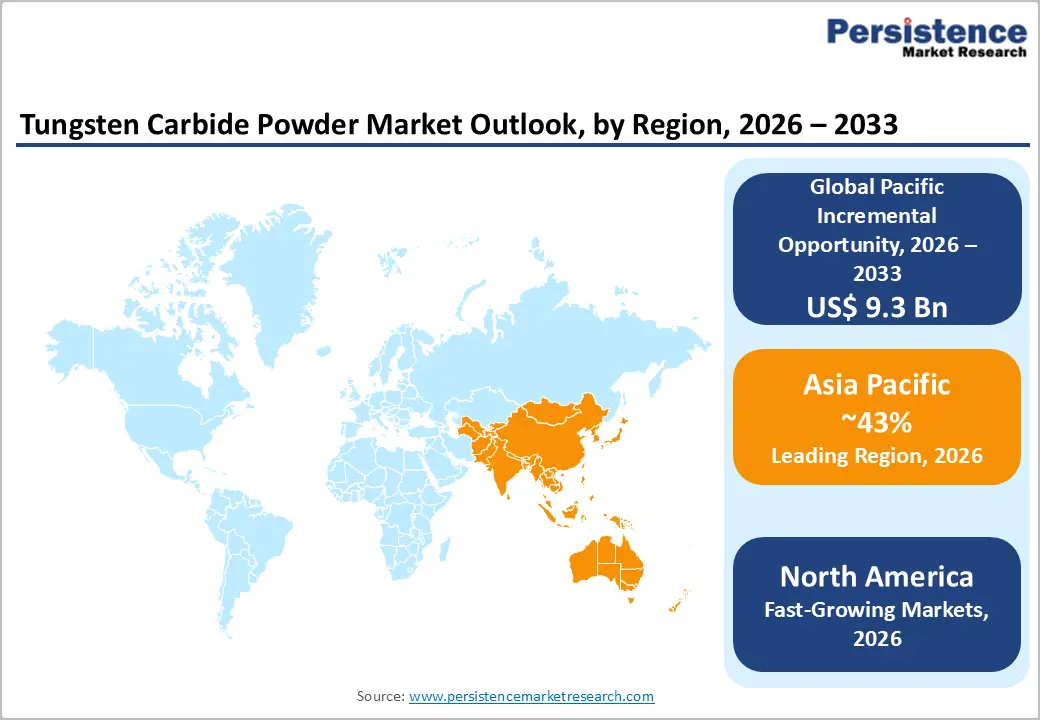

The global tungsten carbide powder market size is likely to be valued at US$ 18.2 billion in 2026 and is projected to reach US$ 27.5 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033. The market expansion is driven by robust demand from high-performance industrial applications, particularly in aerospace, mining, and oil & gas sectors, technological advancements in manufacturing processes, coupled with rapid infrastructure development across emerging economies in Asia Pacific and Latin America, are propelling sustained market growth.

Key Market Highlights:

- Leading Region: Asia Pacific dominates the global tungsten carbide powder market with commanding 43% market share, driven by rapid industrial expansion, infrastructure development across emerging economies, and established manufacturing ecosystems in China, India, and Southeast Asia.

- Fastest Growing Country: India emerges as the fastest-growing regional market within Asia Pacific, experiencing 7.2% CAGR through 2033, propelled by government-sponsored infrastructure investment programs, "Make in India" manufacturing initiatives, defense modernization spending, and accelerating urbanization driving construction and mining equipment demand.

- Dominant Application: Cutting tools command market leadership as the dominant application segment, accounting for 46% market share depending on geographic region classification, reflecting their essential role across precision manufacturing operations in automotive, aerospace, and general industrial sectors globally.

- Growing Application: Mining tools represent the fastest-growing application segment across multiple geographic regions, including Europe and Asia Pacific, driven by escalating mining activities, infrastructure development projects, and emerging economy demand for mineral resource extraction equipment requiring specialized wear-resistant components.

- Key Market Opportunity: Electric vehicle manufacturing and battery technology development represent exceptional growth opportunities, with each EV requiring approximately 2 kilograms of tungsten for battery components and semiconductor systems.

| Key Insights | Details |

|---|---|

|

Global Tungsten Carbide Powder Market Size (2026E) |

US$ 18.2 Bn |

|

Market Value Forecast (2033F) |

US$ 27.5 Bn |

|

Projected Growth CAGR(2026-2033) |

6.1% |

|

Historical Market Growth (2020-2025) |

5.4% |

Market Dynamics

Drivers - Rise in Demand from Aerospace and Defense Sectors

The aerospace and defense industries are major consumers of tungsten carbide powder, driving sustained market growth through increasing demand for precision-engineered components that withstand extreme operational conditions. Tungsten carbide penetrators are extensively used in armor-piercing ammunition systems, where the material's ability to maintain structural integrity under extreme impact forces exceeding 1,700 m/s makes it superior to traditional materials.

Defense modernization initiatives globally, driven by geopolitical tensions and territorial disputes, have accelerated procurement of advanced equipment and systems that incorporate tungsten carbide components. The U.S. military's reliance on tungsten-based armor-piercing ammunition underscores the critical nature of this application segment. Missile guidance systems, aircraft counterweights, and heat-resistant turbine components for military aviation all require tungsten carbide's unique combination of density, thermal stability, and radiation-blocking properties, creating consistent demand momentum in this high-value segment.

Manufacturing Automation and Precision Machining Expansion

Industrial automation and the proliferation of advanced manufacturing technologies are driving unprecedented demand for high-performance cutting tools and wear-resistant components manufactured from tungsten carbide powder. The automotive, aerospace, and general manufacturing sectors require precision machining capabilities at higher speeds and with greater dimensional accuracy than ever before, necessitating tools with superior wear resistance and thermal stability. Sandvik's PowerCarbide® range exemplifies cutting-edge material innovations in rock drilling applications, demonstrating the industry's commitment to advanced cemented carbide button development.

The shift toward Industry 4.0 and smart manufacturing implementations worldwide is accelerating adoption of tungsten carbide-based solutions that maintain consistent performance while reducing downtime. Manufacturing equipment suppliers are expanding production capabilities to address growing demand for specialized tungsten carbide grades in precision machining applications, with India experiencing particularly robust growth through infrastructure development and the "Make in India" manufacturing initiative, encouraging local production of advanced tungsten carbide tools.

Restraints - Geopolitical Supply Chain Vulnerabilities and Export Restrictions

The tungsten carbide market faces significant headwinds from concentrated global supply dynamics, with China controlling approximately 80% of global tungsten production, creating vulnerability to geopolitical disruptions and supply manipulation. Recent policy developments underscore this risk: China's Ministry of Commerce announced new export regulations for 2026-2027 requiring export permits for tungsten shipments, with eligibility restricted to entities meeting specific credit thresholds and demonstrating substantial prior export volumes between 2022-2024. This directive effectively implements state-level supply control, limiting access primarily to China's largest and most compliant traders.

Data reveals concerning trends, with Chinese tungsten exports declining 13.7% year-over-year during January-September 2025 compared to the same period in 2024, despite stable global demand. This deliberate supply manipulation demonstrates Beijing's strategic use of critical mineral controls as geopolitical leverage, forcing Western manufacturers to maintain higher inventory levels, develop alternative sourcing relationships, and absorb supply chain inefficiencies that increase production costs and operational uncertainty across the carbide-dependent industrial ecosystem.

Environmental Compliance and Recycling Infrastructure Challenges

Tungsten carbide powder manufacturers face escalating environmental compliance requirements and regulatory pressures that mandate sustainable production practices and closed-loop recycling systems. While recycling initiatives represent opportunities, transitioning to a comprehensive recycling infrastructure requires substantial capital investments in specialized equipment and processes. The hydrometallurgical and molten salt electrolysis technologies capable of recovering up to 99% of tungsten from scrap involve complex processing methods, high energy consumption, and technical expertise that create implementation barriers, particularly for smaller manufacturers lacking scale economies.

The International Tungsten Industry Association reports approximately 68% of tungsten scrap is currently recycled, indicating that nearly one-third remains unrecovered, representing both environmental liabilities and missed resource recovery opportunities. Regulatory harmonization across regions, including EU Conflict Minerals Regulation compliance and OECD Due Diligence Guidance requirements, increases operational complexity and compliance costs, disproportionately affecting manufacturers without established sustainability infrastructure, thereby constraining market participation and consolidating the competitive landscape.

Opportunity - Electric Vehicle and Renewable Energy Infrastructure Expansion

Electric vehicle manufacturing presents an exceptional growth opportunity for tungsten carbide market participants, driven by the material's critical role in EV battery technology and power electronics. Approximately 2 kilograms of tungsten is incorporated into each electric vehicle, deployed in battery anodes and cathodes, as well as in semiconductor wiring looms, with approximately 2,000 such looms present in every modern vehicle. Tungsten's exceptional electrical conductivity enables rapid battery charging capabilities and facilitates increased nickel integration, extending battery charge retention duration significantly. Hybrid vehicles consume even greater quantities of tungsten, approximately 2.5-3 kilograms per unit, due to the material's critical role in transmission systems and gearing mechanisms that repeatedly transition between electric and internal combustion engine operation.

Global EV production forecasts project continued expansion despite recent market softening, with long-term industry momentum supported by environmental regulations, government incentives, and declining battery costs. The renewable energy sector similarly drives tungsten carbide demand through wind turbine component manufacturing, where wear-resistant bearings and structural elements must endure prolonged operational stresses. Additionally, fusion energy research facilities currently consume approximately 500 metric tons of tungsten annually for plasma-facing components, with demand projected to reach 2,000 metric tons annually by 2035 as demonstration reactors progress toward commercialization. The International Thermonuclear Experimental Reactor (ITER) project alone will utilize over 300 metric tons of tungsten in divertor components, representing the largest single tungsten application in fusion research infrastructure.

Advanced Manufacturing Technologies and Additive Manufacturing Integration

Additive manufacturing and powder metallurgy innovations are creating significant opportunities for tungsten carbide powder suppliers to penetrate emerging applications and market segments with enhanced material properties and manufacturing precision. 3D printing technologies utilizing tungsten carbide powder enable the production of complex geometries previously impossible through conventional sintering methods, unlocking applications in aerospace components, medical devices, and specialized industrial tooling where traditional manufacturing approaches present dimensional or performance constraints. Advanced sintering processes, including low-pressure sintering and nanocrystalline processing techniques, enhance material properties while reducing manufacturing costs, improving cost-performance ratios that expand addressable market segments.

Research and development activities focused on developing cermet powders infused with smart sensors and AI-enabled predictive process monitoring solutions represent emerging business model innovations that optimize manufacturing workflows, reduce downtime, and enable remote equipment monitoring. These technologies transform production floors through increased automation, reduced scrap rates, and enhanced operational efficiency. The convergence of material science advancements with digital manufacturing platforms creates opportunities for innovative startups and established manufacturers alike to differentiate offerings and capture market share through technology-enabled solutions that address specific end-user requirements in aerospace, defense, automotive, and semiconductor manufacturing sectors.

Category-wise Analysis

Application Insights

Cutting tools represent the dominant application segment in the tungsten carbide powder market, commanding approximately 46% market share depending on geographic region and segment classification methodologies. The segment's leadership position reflects cutting tools' essential role across virtually all precision manufacturing operations in automotive, aerospace, and general manufacturing industries. Manufacturers increasingly recognize the superior performance and cost-effectiveness of tungsten carbide inserts compared to solid carbide tools and traditional high-speed steel alternatives. The ability to replace worn inserts without replacing complete tool bodies, combined with extended tool life and higher cutting speeds, drives sustained demand for this product category.

Major market participants including Sandvik, Kennametal, Ceratizit, and Federal Carbide Company have developed comprehensive cutting tool portfolios specifically engineered for demanding applications in automotive component machining, aerospace engine part production, and precision metalworking. The segment's dominance is reinforced by technology leadership investments in cutting-edge tool geometries, coating innovations, and material compositions that enhance performance in high-speed, high-temperature machining applications characteristic of modern manufacturing environments.

Industry Insights

The oil and gas industry emerges as the leading end-use sector for tungsten carbide products, leveraging the material's exceptional hardness, compressive strength, and corrosion resistance to address extreme operational conditions encountered in drilling, extraction, and production operations. Drill bit inserts represent the most critical oil & gas application, where tungsten carbide components withstand extreme impact forces, abrasive rock particles, high downhole temperatures, and corrosive fluid environments while maintaining dimensional precision and cutting efficiency throughout extended drilling campaigns. Approximately 35-40% of oil and gas tungsten carbide consumption derives from drill bit applications, with roller cone and PDC drill bits incorporating tungsten carbide button inserts as wear-resistant cutting elements.

Beyond drilling equipment, tungsten carbide delivers value across critical completion and production systems: valve seats and sleeves in high-pressure pipeline systems maintain reliable sealing under extreme conditions; choke beans and nozzles in flow control manifolds endure high-speed abrasive fluid flows without degradation; pump plungers and liners handle abrasive slurries in high-pressure production systems; and fracturing tools in hydraulic fracturing equipment create controllable rock fractures enabling hydrocarbon extraction. The segment's robustness reflects fundamental economics where tungsten carbide's extended service life dramatically reduces operational downtime, decreases maintenance costs, and improves drilling efficiency sufficiently to justify premium material costs.

Regional Insights

North America Tungsten Carbide Powder Market Trends

North America commands a significant position within the global tungsten carbide market, accounting for 27% of global market share in 2026. The United States represents the regional growth engine, capturing approximately 84% of North American market value, driven by substantial aerospace sector demand, advanced automotive manufacturing capabilities, and robust defense spending supporting military equipment modernization. Kennametal Inc., headquartered in Pittsburgh, Pennsylvania, exemplifies U.S. market leadership, leveraging over 80 years of tungsten carbide manufacturing and processing innovation to develop cutting-edge solutions for aerospace and automotive applications. Precision farming advancements and renewable energy technology development are expanding tungsten carbide adoption across emerging application segments.

The increasing adoption of electric vehicles within North American markets drives new demand patterns, as EV manufacturers require tungsten carbide components in powertrain systems, precision machining of critical components, and wear-resistant elements exposed to high-performance operating conditions. Regulatory pressures supporting clean energy transitions and defense modernization initiatives create structural demand drivers supporting sustained market expansion. Supply chain localization efforts, stimulated by geopolitical tensions and Chinese export controls, are encouraging North American manufacturers to invest in domestic tungsten carbide production capacity, reduce supply chain dependencies, and establish resilient sourcing relationships.

Europe Tungsten Carbide Powder Market Trends

Europe holds 21% of global market share and demonstrating significant regional economic importance to precision manufacturing ecosystems across the continent. Germany maintains leadership positioning within European markets, driving regional innovation initiatives and sustainability leadership. The German manufacturing sector's tradition of precision engineering, combined with strong automotive and aerospace industrial bases, generates consistent demand for high-performance tungsten carbide cutting tools and components. Sandvik's 2023 innovation initiative introducing a new range of high-performance cutting tools designed with recycled tungsten carbide demonstrates sector commitment to compliance with EU environmental regulations while achieving enhanced durability and efficiency improvements that reduce industrial waste and energy consumption.

The broader European market, encompassing UK, France, and Spain, exhibits similar dynamics with cutting tools commanding 39.7% market segment share in 2026 while mining tools emerge as the fastest-growing application segment at accelerated growth rates. Regional growth at 5.8% CAGR through 2033 reflects steady market expansion supported by manufacturing resilience, industrial modernization, and supply chain localization efforts reducing dependencies on Asian suppliers. Regulatory harmonization around OECD Due Diligence Guidance and EU Conflict Minerals Regulations creates compliance requirements that support market consolidation around larger, more sophisticated suppliers capable of navigating complex regulatory environments while maintaining supply chain transparency and responsible sourcing practices.

Asia Pacific Tungsten Carbide Powder Market Trends

Asia Pacific represents the fastest-growing regional market with dominant global positioning, commanding approximately 43% global market share. China serves as the regional production epicenter, leveraging dominant tungsten ore reserves representing approximately 80% of global reserves, advanced processing capabilities, and established manufacturing ecosystems that support both domestic consumption and global export operations. China's strategic implementation of new export controls for the 2026-2027 period creates supply uncertainty for Western manufacturers, stimulating alternative sourcing strategies and investment in non-Chinese supply sources including India's emerging mining capabilities.

India exhibits exceptional growth potential, experiencing 7.2% CAGR through 2033 driven by aggressive infrastructure expansion, defense modernization initiatives, and the government's "Make in India" manufacturing promotion strategy encouraging local tungsten carbide product development. Infrastructure development programs supporting smart city projects, high-speed rail expansion, and transportation network modernization are accelerating construction and mining equipment demand, directly translating into higher tungsten carbide tool consumption across the Indian economy. Japan and South Korea maintain steady demand through precision manufacturing clusters specializing in electronics, semiconductors, and aerospace component production, with South Korea benefiting from Almonty Industries' Sangdong Tungsten Mine reopening, providing stable high-grade tungsten supplies reducing dependency on Chinese sources.

Competitive Landscape

The tungsten carbide powder market exhibits moderately consolidated competitive structure characterized by presence of global diversified material suppliers, specialized tungsten carbide manufacturers, and regional producers competing on differentiation dimensions including product quality, technical service, sustainability practices, and supply chain resilience. Sandvik AB commands market leadership with approximately 10% market share, leveraging integrated operations spanning tungsten mining through Wolfram Bergbau und Hütten AG subsidiary based in Austria, advanced manufacturing facilities, recycling operations across multiple continents, and comprehensive customer support systems. The company's strategic integration from ore extraction through finished product delivery and scrap recycling provides competitive advantages in supply chain control, quality assurance, and sustainability performance, differentiating it from competitors’ dependent on external raw material sourcing.

Kennametal Inc. and Ceratizit S.A. represent major global competitors offering comprehensive product portfolios serving multiple end-use industries. Sumitomo Electric Industries emphasizes advanced cutting technology customization and global market presence. H.C. Starck GmbH focuses on specialized high-performance tungsten carbide grades and advanced material compositions, maintaining premium positioning through technological differentiation. Federal Carbide Company and China Tungsten Online serve regional markets with competitive cost positioning and supply chain advantages. Emerging startups developing cermet powder innovations with integrated smart sensors and advanced recycling technologies represent potential disruptive threats to established competitors, creating innovation pressures across the industry.

Key Market Developments

- In December 2024, Wall Colmonoy Corporation announced the launch of its WallCarb™ HVOF Tungsten Carbide Powders. WallCarb™ HVOF Carbide Powders is designed for thermal spray applications, and provide dense, hard coatings with exceptional wear and corrosion resistance.

- In October 2023, Sandvik completed the acquisition of Buffalo Tungsten, Inc. (BTI), a leading U.S.-based producer of tungsten metal powder and tungsten carbide powder with primary operations in North America. Following the transaction, BTI will be integrated and reported under Sandvik’s Machining Solutions (SMS) business area.

Companies Covered in Tungsten Carbide Powder Market

- Ceratizit S.A.

- China Tungsten Online (Xiamen) Manu. & Sales Corp.

- Chongyi ZhangYuan Tungsten Co., Ltd

- Extramet

- Federal Carbide Company

- Guangdong Xianglu Tungsten Co., Ltd.

- H.C. Starck GmbH

- Japan New Metal Co., Ltd

- Kennametal Inc.

- Sandvik AB

- Nanchang Cemented Carbide Co., Ltd

- Reade International Corp.

- Jiangxi Yaosheng Tungsten Co., Ltd.

- Umicore

- Wall Colmonoy

Frequently Asked Questions

The global tungsten carbide powder market is projected to reach US$ 27.5 billion by 2033, growing at a 6.1% CAGR from 2026 through 2033, driven by sustained demand from aerospace, oil & gas, mining, and emerging electric vehicle manufacturing sectors requiring high-performance carbide components.

Market demand growth is driven by multiple converging factors including escalating demand from aerospace and defense sectors for precision-engineered components; expanding manufacturing automation requiring advanced cutting tools; rapid infrastructure development across emerging economies; electric vehicle manufacturing expansion incorporating tungsten carbide battery components.

Cutting tools represent the dominant application segment commanding 40% market share depending on geographic region, reflecting their essential role across automotive, aerospace, and general manufacturing operations requiring precision machining capabilities with superior wear resistance and thermal stability properties.

Asia Pacific commands market leadership with 43% global market share, driven by industrial expansion, manufacturing capabilities, established tungsten ore reserves representing 80% of global supply, and infrastructure development across China, India, Japan, and Southeast Asia creating sustained demand momentum.

Major market opportunities include electric vehicle and hybrid vehicle manufacturing requiring 2+ kilograms of tungsten per vehicle for battery and semiconductor systems; renewable energy infrastructure development particularly wind turbine component manufacturing.