- Mining & Services

- Mining Automation Market

Mining Automation Market Size, Share, and Growth Forecast 2026 - 2033

Mining Automation Market by Solution (Software Automation, Services, Equipment Automation), Technique (Underground, Surface), Application (Metal Mining, Mineral Mining, Coal Mining), and Regional Analysis, 2026 - 2033

Mining Automation Market Size and Trends Analysis

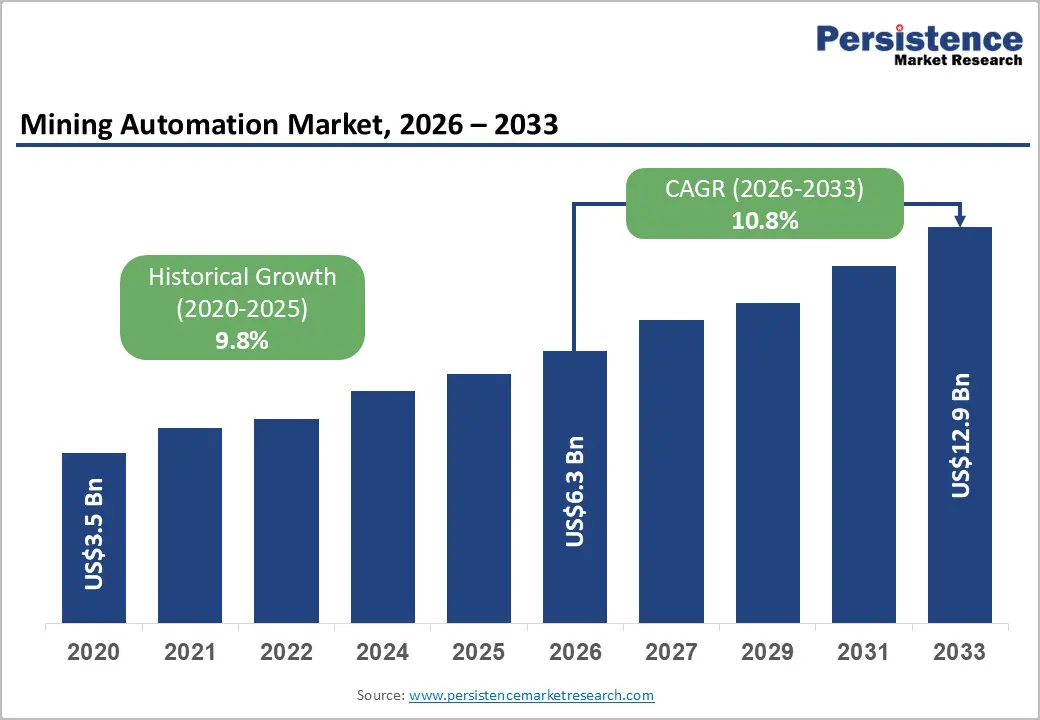

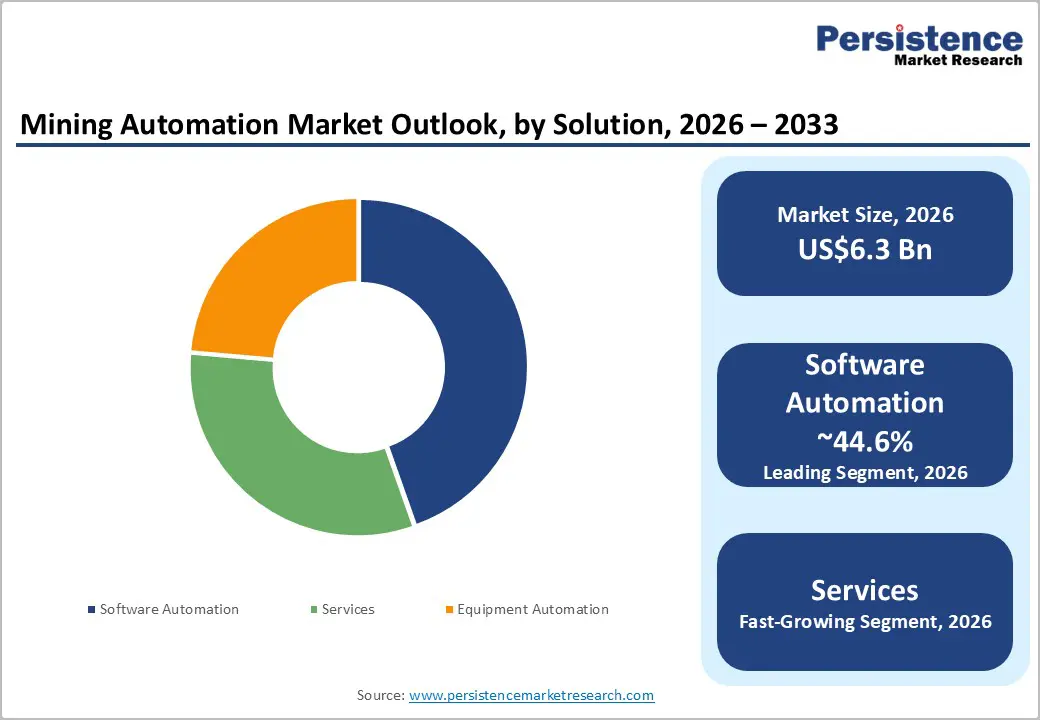

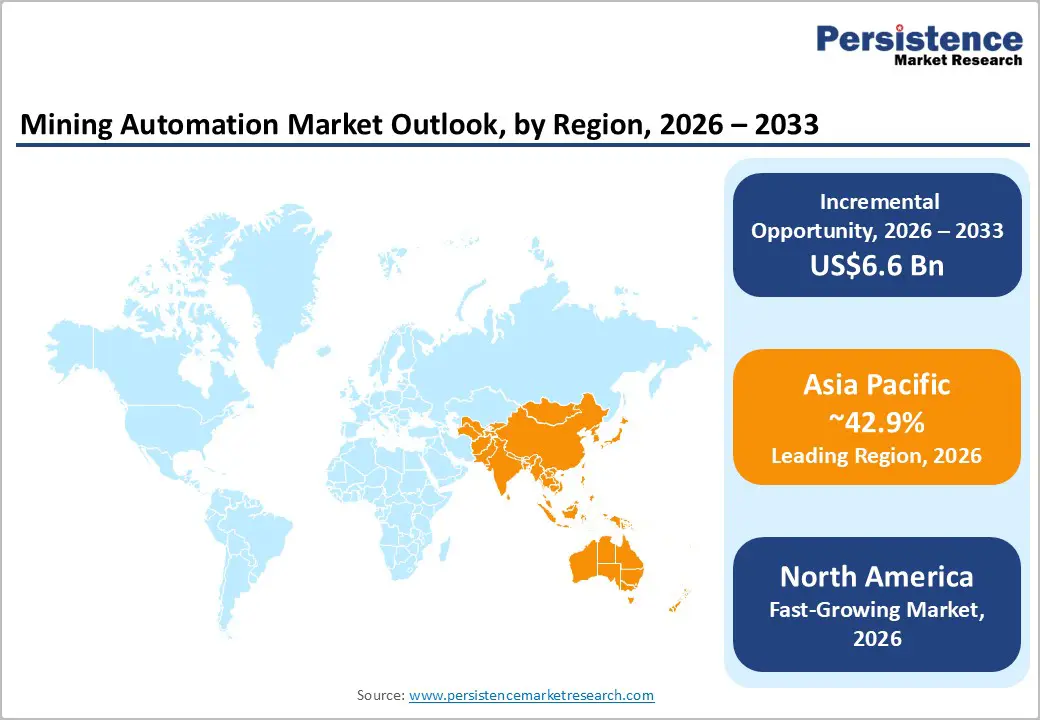

The global mining automation market size is likely to be valued at US$6.3 billion in 2026 and is expected to reach US$12.9 billion by 2033, growing at a CAGR of 10.8% during the forecast period from 2026 to 2033, driven by rising labor shortages in remote mining locations and increasing focus on worker safety through reduced human exposure.

High demand for critical minerals such as lithium and copper, and ongoing adoption of AI-based fleet management systems, are also predicted to boost the market.

Key Industry Highlights:

- Leading Solution: Software automation, approximately 44.6% share in 2026, as it acts as the central control layer that integrates equipment, data analytics, and real-time decision-making across mining operations.

- Dominant Application: Mineral mining, nearly 40.2% in 2026, as large, repetitive, and open-pit operations make it easier to deploy autonomous haulage and drilling systems.

- Leading Region: Asia Pacific, with about a 42.9% share in 2026, owing to large-scale mining operations and extensive government-backed automation programs.

- Fast-growing Region: North America, backed by strict safety norms and investments in advanced technologies by companies such as Caterpillar.

- New Order: In July 2025, Epiroc won a large order from Sociedad Punta del Cobre (Pucobre) for a fleet of Minetruck MT65 S underground haulers, along with a package of digital solutions. The digital solutions ordered include Fleet+ and Fleet+ ShiftGoals, which provide visibility into machine performance and goal tracking.

DRO Analysis

Driver- Increasing Need to Improve Worker Safety

Mining remains one of the most dangerous industries globally. According to the Mine Safety and Health Administration (MSHA), fatal mining accidents rose 25% in 2022, with 38 fatalities recorded by December 2023, up from 30 in 2022. Automation addresses this by relocating workers from the blast zone, underground tunnels, and toxic atmospheres to centralized control rooms. Rio Tinto, for instance, operates 73 driverless trucks across four iron ore mines in Australia specifically to reduce worker exposure to danger.

Next-generation hoisting and belt conveyor systems are replacing haul trucks, which reduces vehicle movements in total and cuts vehicular risks alongside carbon emissions. Key mines report up to a 66% reduction in accident rates per 1,000 workers when transitioning from traditional to automated operations. This measurable safety impact is a powerful business and regulatory case for increased automation adoption.

Demand for Round-the-Clock Operations without Human Constraints

Human-operated mines are constrained by shift rotations, fatigue limits, and safety-mandated breaks. Autonomous equipment removes all of these. Caterpillar's MineStar Command for hauling enables near-continuous operation and claims to improve productivity by 30% while reducing operational costs by 20%. The system has hauled more than 2.5 billion tons since its commercial launch in 2013.

Komatsu's FrontRunner Autonomous Haulage System, first deployed commercially in Chile in 2007 and Australia in 2008, integrates electric-drive haul trucks with fleet management software. It allows loaders, graders, and dozers to interact for optimized operations. Around-the-clock runs also produce predictable cycle times, which improve planning accuracy and reduce yield variability. These are the outcomes that manual operations simply cannot guarantee.

Restraint - Workforce Displacement in Mining-Dependent Regions

Automation in mining doesn't redistribute jobs, but it eliminates them, especially for workers doing manual, repetitive, or physically hazardous tasks. The economic hit falls hardest on communities where mining is the primary employer. A report from the University of Queensland's Center for Social Responsibility in Mining found that while large-scale automation improves efficiency and safety, a reduction in on-site roles is likely to reduce economic activity in local communities. Governments and mining firms face high pressure to develop credible reskilling and transition frameworks, and without those, social license to operate in affected regions remains at risk.

Opportunity - Move toward Fully Integrated and Self-Managing Operations

Mining automation is evolving beyond simple remote control toward self-managing equipment that handles its own power, navigation, and positioning. A key example is Huawei's deployment at Huaneng Group's Yimin open-pit coal mine in Inner Mongolia. The world's first fleet of 100 autonomous electric mining trucks has been officially launched at the Yimin mine. These trucks can monitor their own status, manage charging cycles, and operate with highly precise positioning enabled by advanced geolocation technology.

A fully automated battery-swapping station returns the trucks to operation in minutes when power is low, thereby removing the last human touchpoint in the cycle. After initial trials that hit 87% of human driver efficiency, continuous refinement pushed autonomous operations to 120% of human productivity by 2024. This full-stack autonomy model, where machines sense, decide, refuel, and operate independently, signals where the market is headed.

Emergence of 3D Mapping and Navigation

One of the final frontiers in mining automation has been navigating the complex and three-dimensional geometry of deep underground mines. This barrier is now being broken. Epiroc's Deep Automation platform has introduced true 3D capability for underground operations, enabling orchestration of autonomous truck haulage across complex and multi-level ramps, while improving fleet visualization and traffic coordination.

Developed and tested at Agnico Eagle's Odyssey Mine in Canada, the system now applies to all compatible underground Scooptram loaders as well as the Minetruck MT54 S and MT65 S. These are now automation-ready. Peer-reviewed research published in a journal supported by the National Institutes of Health (NIH) validated the use of 3D LiDAR-based SLAM to produce accurate maps of underground tunnels with significant elevation changes. These developments make truly unmanned deep underground operations a near-term reality.

Category-wise Analysis

Solution Insights

The software automation segment is predicted to lead with a share of approximately 44.6% in 2026, as it has become the core of mining automation due to its ability to connect and control everything in real time. Modern mines run on centralized platforms that manage fleets, monitor equipment health, and optimize routes. Hardware alone cannot deliver these outcomes without intelligent software layers. For example, Caterpillar’s MineStar system integrates haul trucks, drills, and loaders into one control platform. The company reported hundreds of autonomous trucks operating globally under this system, all managed through software-backed decision engines.

Services are estimated to be the fastest-growing segment over the forecast period, as mining companies lack in-house expertise to manage complex automation systems. Deploying automation is not a one-time task. It requires continuous support such as system integration, remote monitoring, and software updates. Several miners now outsource these tasks to OEMs and tech providers. Mining companies are also setting up remote operation centers that require constant technical support. According to the World Economic Forum, remote mining operations require continuous data monitoring and cybersecurity services, which create recurring revenue opportunities for service providers.

Application Insights

The mineral mining segment is expected to account for nearly 40.2% of the market share in 2026, driven by its early and extensive adoption of automation technologies, particularly in large-scale coal and iron ore operations. These mining activities involve repetitive processes, high production volumes, and predictable operating conditions, making them highly suitable for autonomous systems. Autonomous haulage solutions are especially effective in such environments, where fixed routes and continuous material movement enhance operational efficiency. This leadership position is further supported by Australian government mining reports, which indicate that autonomous haulage systems are more widely deployed in iron ore and coal mines than in other mining segments. The prevalence of open-pit mining in these commodities also facilitates easier implementation and scalability of automation technologies.

The metal mining segment is expected to remain in the second position in 2026, backed by rising demand for critical minerals such as copper, lithium, and nickel. These metals are essential for electric vehicles, batteries, and renewable energy systems. Governments worldwide are pushing for increased production of these resources. Unlike mineral mining, metal mining often involves complex underground operations. This creates a high demand for advanced automation such as tele-remote loaders and AI-supported drilling systems.

Regional Insights

Asia Pacific Mining Automation Market Trends

Asia Pacific is anticipated to dominate in 2026 with a share of nearly 42.9%, as it combines large-scale mining activity with fast adoption of automation. Countries such as Australia, China, and India have extensive coal, iron ore, and mineral operations. These mines operate at scale, which makes automation more viable. A key example comes from CSIRO, which has supported multiple autonomous mining trials and digital mine projects. Australia already runs some of the world’s largest autonomous fleets.

China is also deploying automation at speed across coal mines. Asia Pacific benefits from government-backed mining modernization programs, which push digital and autonomous systems across operations.

China Mining Automation Market Trends

In 2026, China is projected to account for a share of around 34.6%, backed by superior government intervention and local technology development. The government has issued multiple policies to build smart mines. These include 5G-enabled underground systems and AI-based monitoring platforms. For example, the country’s National Energy Administration has mandated the development of hundreds of smart coal mines. Many of these mines now use autonomous trucks and remote-controlled drilling systems. Companies such as XCMG and SANY are producing low-cost autonomous equipment at scale.

Australia Mining Automation Market Trends

Australia is surging due to early adoption and strong mining majors. Companies such as Rio Tinto and BHP have invested heavily in autonomous haulage and remote operations. Rio Tinto’s autonomous haulage system is one of the largest in the world. The company has publicly shared that its autonomous trucks have moved billions of tons of material in Pilbara operations. These systems are managed from remote operation centers located hundreds of kilometers away.

Government and research support also play a key role. Agencies such as Geoscience Australia and CSIRO are actively working on digital mining technologies. Australia also faces workforce shortages in remote regions, which pushes automation adoption faster than in many other countries.

North America Mining Automation Market Trends

North America will likely account for a share of approximately 25.6% in 2026, owing to increasing technology integration and safety regulations. Mining companies in the U.S. and Canada are investing in automation to improve safety and meet regulatory standards. For example, the National Institute for Occupational Safety and Health has published research promoting automation to reduce worker exposure to hazardous environments. This has encouraged mining companies to adopt remote-controlled and autonomous systems.

Another factor is the presence of leading automation providers. Companies, including Caterpillar and Hexagon, are actively deploying advanced fleet management and AI-based solutions across mines in North America. Canada, in particular, is seeing increased adoption in underground metal mining.

U.S. Mining Automation Market Trends

The U.S. is expected to see steady growth, backed by critical mineral demand and policy support. The government is pushing domestic production of lithium, copper, and rare earth elements to reduce import dependence. The U.S. Geological Survey has highlighted rising demand for these minerals due to electric vehicles and clean energy. To meet this demand, mining companies are investing in automation to increase efficiency and reduce operational risks. The U.S. Department of Energy (DOE) has further funded projects focused on smart mining and digital operations. These initiatives support the use of AI, robotics, and real-time monitoring systems in mining. This creates a long-term outlook for automation in the country.

Europe Mining Automation Market Trends

A share of approximately 12.4% is anticipated to be registered in Europe in 2026. This growth is spurred by strict environmental and safety regulations. Mining companies are under pressure to reduce emissions and improve worker safety. Automation helps achieve both goals. The European Commission has launched initiatives under the Critical Raw Materials Act to secure the supply of key minerals. This includes encouraging digital and automated mining practices. Unlike Asia Pacific, Europe has fewer large-scale mines, which limits swift expansion.

However, steady investments in sustainable and efficient mining technologies are supporting gradual growth. Several local mines are now focusing on underground automation and battery-electric equipment.

U.K. Mining Automation Market Trends

The U.K. is estimated to see moderate growth, mainly in mining technology and development. The country has limited large-scale mining, but it is investing in critical mineral projects and digital solutions. The British Geological Survey has highlighted the need to develop domestic sources of critical minerals. This is pushing interest in modern mining methods, including automation. The U.K. is also supporting research in robotics and AI for mining through university and industry collaborations. While deployment levels are still low compared to Australia or China, the focus on innovation and sustainability gives the country a stable growth outlook.

Germany Mining Automation Market Trends

Germany is focusing more on mining technology rather than large-scale mining operations. The country has limited active mining compared to others, but it plays a key role in automation solutions. Companies such as Siemens are developing digital twin technology and industrial automation systems for global mining operations. These solutions are used in mines across different regions. Germany’s research institutions are also active. Government-backed programs are supporting Industry 4.0 applications in mining. This positions the country as a technology provider rather than a leading mining adopter.

Competitive Landscape

The global mining automation market is moderately consolidated at the equipment level but increasingly fragmented in software, AI, and interoperability solutions. The competitive landscape is currently led by key players such as Caterpillar, Komatsu, Sandvik, and Epiroc, which control much of the autonomous haulage, drilling, and underground automation networks. These companies benefit from decades-long mine relationships, installed fleets, and integrated platforms combining hardware, software, and analytics.

Competition is shifting from pure machinery sales to platform ownership and recurring software revenue. Vendors are building closed networks where fleet data, AI-backed maintenance, and real-time mine optimization create high switching costs for miners. Underground mining automation is even more concentrated because of the technical complexity and safety requirements involved. Software-focused firms are becoming increasingly influential despite small market shares.

Key Industry Developments:

- In March 2026, Epiroc secured a US$41 million order from an undisclosed customer in Africa for a fleet of autonomous, cable-electric Pit Viper 275 E blasthole drill rigs. The machines will be operated fully autonomously, with zero exhaust emissions, and deliveries are expected to be completed by the end of 2027.

- In April 2025, Weir completed the acquisition of Micromine, a provider of mining software solutions, for an enterprise value equivalent to approximately US$840 million. The former intends to integrate Micromine with its MOTION METRICS and NEXT intelligent solutions to create a unified digital optimization platform spanning resource planning, mine design, and processing activities.

- In March 2025, Luminar Technologies announced a collaboration with Caterpillar to integrate its LiDAR technology into Caterpillar's next-generation autonomous solution, Cat Command for hauling. Each Cat off-highway truck will feature two Iris LiDAR units with an integration system designed exclusively for Caterpillar.

Companies Covered in Mining Automation Market

- Atlas Copco AB

- Autonomous Solution Inc.

- Caterpillar, Inc.

- The Weir Group PLC

- Epiroc AB

- Hexagon AB

- Hitachi, Construction Machinery Co. Ltd.

- Komatsu Ltd.

- Liebherr Group

- MST (Mine Site Technologies)

- Rio Tinto

- Rockwell Automation, Inc.

- RPM Global Holdings Ltd.

- Sandvik AB

- Siemens AG

- Trimble Inc.

Frequently Asked Questions

The global mining automation market is projected to be valued at US$6.3 billion in 2026.

The mining automation market is expected to reach US$12.9 billion by 2033.

Key market trends include the shift toward AI-driven decision-making and integration of battery-electric autonomous equipment.

Software automation is expected to be the leading solution with a share of nearly 44.6% in 2026, as it enables predictive maintenance and real-time optimization.

The mining automation market is expected to grow at a CAGR of 10.8% from 2026 to 2033.

Atlas Copco AB, Autonomous Solution Inc., Caterpillar, Inc., and The Weir Group PLC are a few key market players.