- Plastics, Polymers & Resins

- TPE Films and Sheets Market

TPE Films and Sheets Market Size, Share, and Growth Forecast, 2026 - 2033

TPE Films and Sheets Market by Material (Styrenic Block Copolymers (SBC), Thermoplastic Polyurethanes (TPU), Others), Form (Films, Sheets, Others), Application, and Regional Analysis for 2026 - 2033

TPE Films and Sheets Market Size and Trends Analysis

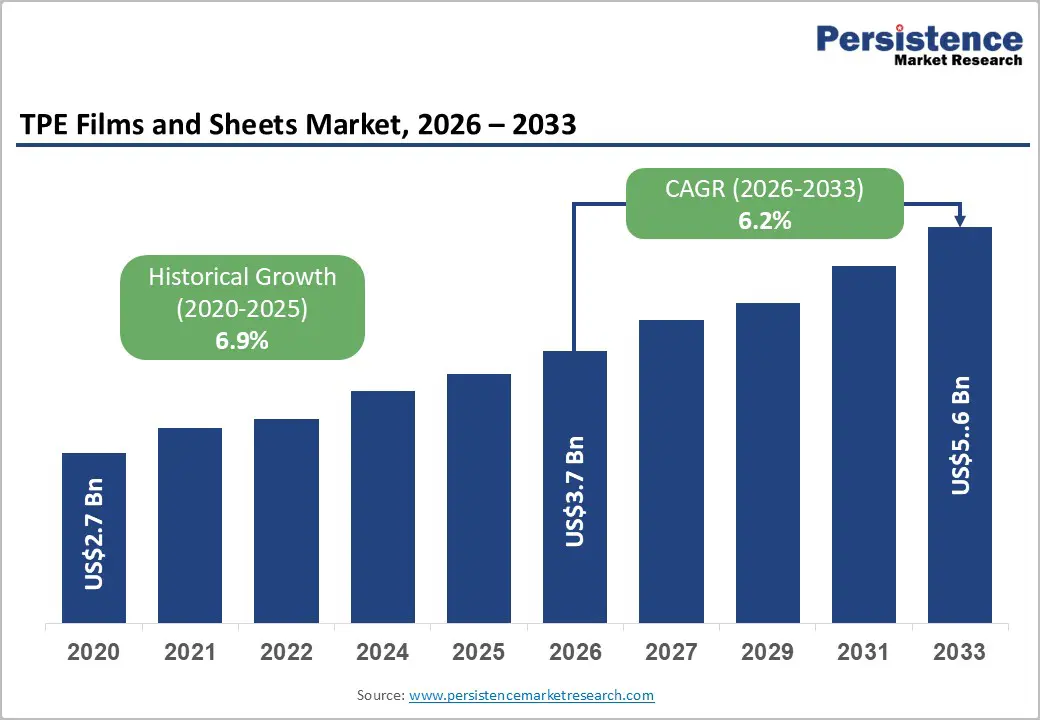

The global TPE films and sheets market size is likely to be valued at US$3.7 billion in 2026 and is expected to reach US$5.6 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033, driven by increasing adoption of thermoplastic elastomer (TPE) materials across medical, automotive, packaging, consumer goods, and construction applications. Growing emphasis on lightweight materials, recyclability, regulatory compliance, and product durability is supporting long-term demand.

Manufacturers are increasingly investing in advanced TPE formulations that offer enhanced flexibility, biocompatibility, abrasion resistance, and processing efficiency. As sustainability regulations become more stringent across major economies, TPE films and sheets are emerging as preferred alternatives to traditional elastomeric and multi-material structures.

Key Industry Highlights:

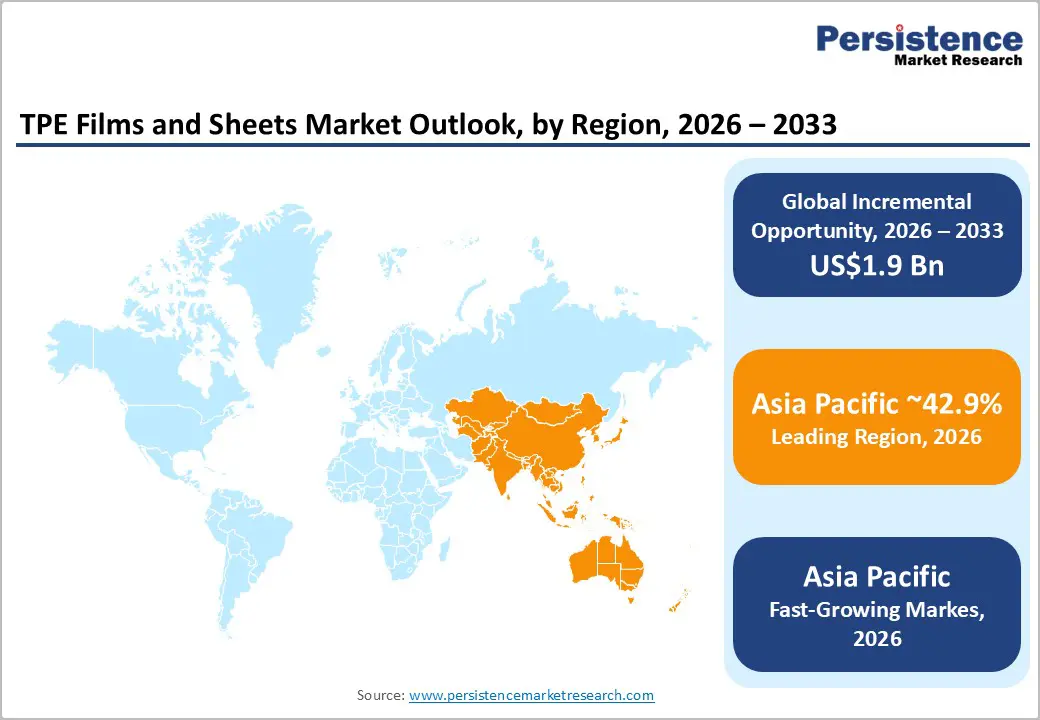

- Leading Region: Asia Pacific is projected to account for 42.9% of the market share in 2026, supported by strong manufacturing capabilities, expanding healthcare infrastructure, and growing automotive production.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing region, driven by industrial expansion in China, India, and ASEAN economies.

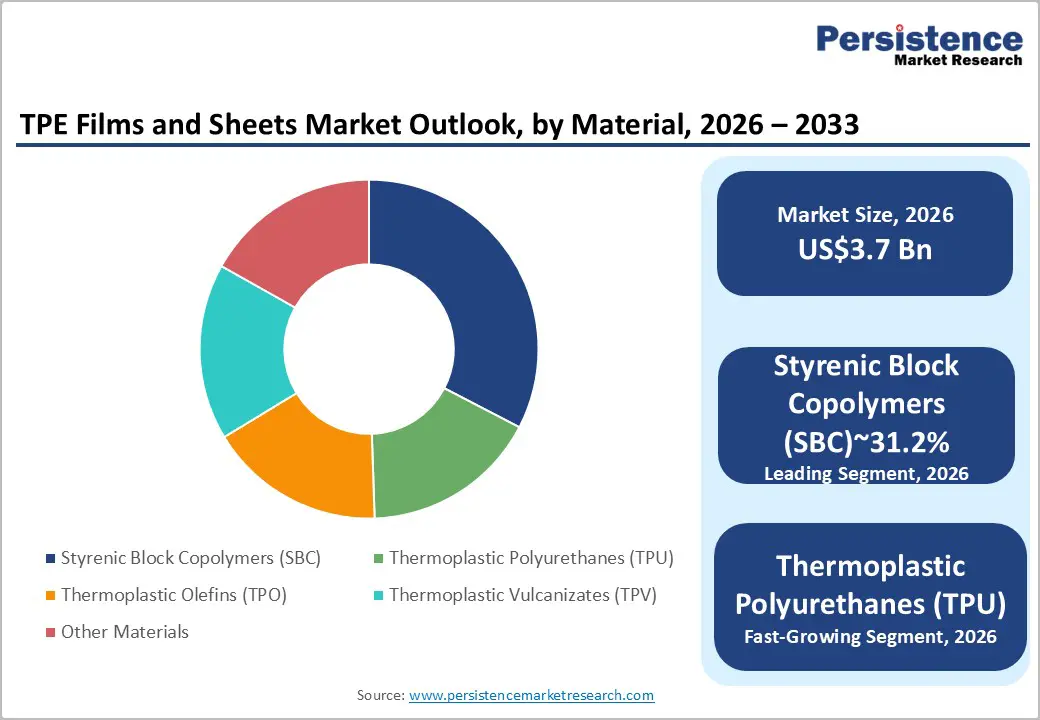

- Dominant Material: Styrenic Block Copolymers (SBC) are anticipated to account for 31.2% market share in 2026, owing to their cost-effectiveness, flexibility, and broad use in hygiene and medical applications.

- Leading Form: Films are anticipated to hold a 61.5% market share in 2026, supported by extensive use in medical packaging, consumer goods, protective coverings, and flexible packaging applications.

DRO Analysis

Driver - Rising Demand from Medical and Healthcare Applications

The medical and healthcare industry has emerged as one of the most significant growth drivers for the TPE films and sheets market. Healthcare providers and medical device manufacturers increasingly require materials that combine flexibility, softness, chemical resistance, sterilization compatibility, and biocompatibility. TPE films are widely used in wound care products, medical drapes, wearable devices, protective barriers, ostomy products, and patient-contact components.

The global expansion of healthcare infrastructure, rising healthcare expenditures, and increasing adoption of disposable medical products continue to strengthen demand. Regulatory standards governing patient safety and medical device performance are encouraging manufacturers to adopt high-performance thermoplastic elastomers that meet strict quality requirements. As healthcare systems focus on infection prevention and patient comfort, demand for specialized medical-grade TPE films and sheets is expected to increase steadily, creating sustained opportunities for material suppliers and converters.

Growing Focus on Lightweighting and Sustainable Materials

Automotive manufacturers, packaging companies, and consumer goods producers are actively seeking lightweight and recyclable materials to improve product performance and reduce environmental impact. TPE films and sheets provide an attractive combination of durability, flexibility, lower processing costs, and recyclability compared with conventional rubber-based materials.

In the automotive industry, lightweight materials contribute to improved fuel efficiency and support vehicle electrification strategies. Packaging manufacturers are increasingly adopting recyclable flexible materials to comply with circular economy initiatives and sustainability targets. Consumer goods companies are also integrating TPE-based solutions into footwear, personal care products, and protective coverings due to their versatility and aesthetic properties. These trends are creating a favorable environment for long-term market expansion and encouraging investments in advanced TPE technologies.

Restraint - Raw Material Price Volatility and Regulatory Compliance Costs

Despite positive growth prospects, the market faces challenges associated with fluctuating raw material prices and increasing regulatory requirements. Many thermoplastic elastomer materials remain dependent on petrochemical feedstocks, making manufacturers vulnerable to changes in crude oil and chemical pricing.

Regulatory compliance presents another significant challenge, particularly in healthcare, food-contact packaging, and specialty industrial applications. Product qualification, testing, certification, and ongoing compliance monitoring increase development costs and extend commercialization timelines. Small and medium-sized manufacturers often face difficulties in maintaining regulatory expertise and investing in continuous product validation. These factors can constrain profit margins and create barriers to entry, particularly for new market participants seeking to compete with established suppliers.

Opportunity - Expansion of Manufacturing and Consumption in Asia Pacific

Asia Pacific represents the largest growth opportunity for the TPE films and sheets industry. Rapid industrialization, urbanization, healthcare expansion, and automotive production growth are driving substantial demand across China, India, Japan, South Korea, and ASEAN countries.

Regional governments continue to support domestic manufacturing through infrastructure investments and industrial development programs. Growing middle-class populations are increasing demand for consumer goods, medical products, and packaged products that utilize TPE films and sheets. The combination of strong domestic consumption and cost-efficient manufacturing capabilities positions Asia Pacific as a strategic investment destination for global suppliers seeking capacity expansion and market penetration.

Development of High-Performance Specialty Films

Growing demand for premium applications is creating opportunities for high-value specialty TPE films. Medical-grade TPU films, protective films, wearable-device components, smart surface technologies, and advanced industrial laminates represent attractive growth segments.

Customers increasingly prioritize performance characteristics such as transparency, abrasion resistance, skin compatibility, sterilization resistance, and durability. These requirements are encouraging manufacturers to develop specialized formulations that command higher margins and strengthen customer relationships. Companies capable of combining material innovation with application engineering expertise are expected to gain competitive advantages in these rapidly evolving market segments.

Category-wise Analysis

Material Insights

Styrenic Block Copolymers (SBC) are anticipated to account for 31.2% of the market share in 2026, making them the leading material segment. Their dominance is driven by an optimal balance of flexibility, softness, processability, and cost-effectiveness. SBC-based films are widely used in hygiene products, medical disposables, baby care products, and personal care applications. For example, SBC films are commonly incorporated into diaper back sheets and medical drapes due to their comfort and elasticity. Their compatibility with high-volume extrusion processes further supports widespread adoption across consumer-focused applications.

Thermoplastic Polyurethanes (TPU) are projected to be the fastest-growing material segment. TPU films offer excellent abrasion resistance, transparency, durability, and chemical stability, making them suitable for premium applications. They are increasingly used in wound-care dressings, wearable medical devices, automotive paint protection films, and industrial laminates. Growing demand for high-performance materials in healthcare and automotive sectors is expected to accelerate TPU adoption and expand its revenue contribution over the forecast period.

Form Insights

Films are anticipated to hold 61.5% of the market share in 2026, maintaining their position as the dominant form segment. Their leadership is supported by extensive use across medical packaging, hygiene products, protective coverings, and consumer goods. TPE films are valued for their lightweight properties, flexibility, breathability, and ease of integration into multilayer structures. For instance, breathable medical films and flexible packaging laminates increasingly utilize TPE-based solutions to enhance product performance while maintaining processing efficiency.

TPE sheets are projected to be the fastest-growing form segment. Demand is increasing across automotive interiors, industrial protection systems, construction membranes, and reusable healthcare products. For example, TPE sheets are used in vehicle interior panels, protective industrial liners, and durable construction barriers where greater thickness and structural stability are required. Their ability to support thermoforming and customized fabrication is expected to drive continued growth in specialized industrial applications.

Regional Insights

North America TPE Films and Sheets Market Trends

North America remains one of the most technologically advanced markets for TPE films and sheets, supported by strong healthcare infrastructure, advanced manufacturing capabilities, and continuous investment in polymer innovation. The region benefits from growing demand for medical-grade materials, sustainable packaging solutions, and lightweight automotive components. Regulatory emphasis on product safety, healthcare compliance, and environmental sustainability continues to encourage the adoption of high-performance TPE materials.

U.S. TPE Films and Sheets Market Trends

The U.S. is the largest market in North America and serves as the region's primary growth engine. A well-established medical device industry, robust healthcare spending, and a highly developed automotive sector drive demand for TPE films and sheets. Medical-grade films are increasingly utilized in wound care products, wearable medical devices, surgical drapes, and protective barriers. Automotive manufacturers are also incorporating lightweight TPE materials into interior components and protective films to support vehicle efficiency and electrification initiatives. Continuous investments in advanced TPU technologies and recyclable film solutions further strengthen the country's market position.

Canada TPE Films and Sheets Market Trends

Canada market growth is supported through its growing healthcare sector, sustainable packaging initiatives, and industrial manufacturing activities. Demand for recyclable and environmentally responsible materials is encouraging adoption of TPE-based films across packaging and consumer goods applications. The country's focus on environmental stewardship and circular economy practices is expected to create additional opportunities for advanced elastomer-based materials.

Europe TPE Films and Sheets Market Trends

Europe represents a mature yet strategically important market characterized by strong sustainability regulations, advanced manufacturing capabilities, and high-value industrial applications. The region's focus on circular economy initiatives and material efficiency is accelerating demand for recyclable and environmentally responsible TPE solutions. Innovation, regulatory compliance, and sustainable product development remain key competitive factors across the region.

Germany TPE Films and Sheets Market Trends

Germany is projected to be the leading market in Europe, accounting for approximately 30.1% of regional revenue in 2026, supported by its strong automotive manufacturing sector, industrial engineering expertise, and concentration of major chemical and materials companies. Demand for TPE films and sheets is driven by automotive interiors, medical devices, industrial applications, and advanced packaging solutions. The country's leadership in sustainable manufacturing and polymer innovation continues to support market growth.

France TPE Films and Sheets Market Trends

France is expected to account for approximately 20.8% of the Europe market in 2026, benefiting from strong healthcare, packaging, and consumer goods industries. Growing demand for medical-grade materials, flexible packaging solutions, and sustainable products is supporting TPE adoption across multiple sectors. Investments in healthcare modernization and environmentally friendly materials continue to create growth opportunities.

U.K. TPE Films and Sheets Market Trends

The U.K. remains an important market for specialty films, healthcare products, and advanced manufacturing applications. Increasing demand for sustainable packaging and medical materials is encouraging adoption of high-performance TPE solutions. Research-driven innovation and specialty product development remain key growth drivers.

Spain TPE Films and Sheets Market Trends

Spain is emerging as one of the faster-growing markets within Europe due to expanding industrial production, infrastructure investments, and growing demand for sustainable packaging materials. Increased adoption of TPE sheets and films across construction, automotive, and consumer goods applications is contributing to market expansion.

Asia Pacific TPE Films and Sheets Market Trends

Asia Pacific is projected to hold approximately 42.9% of the market share in 2026, making it the largest regional market. The region's dominance is supported by extensive manufacturing capabilities, expanding healthcare infrastructure, rapid urbanization, and rising consumer demand. Growing automotive production, increasing healthcare expenditures, and strong industrial development continue to drive demand for advanced thermoplastic elastomer materials.

China TPE Films and Sheets Market Trends

China is expected to be the dominant market within Asia Pacific, accounting for approximately 67.3% of regional demand in 2026. Its leadership is supported by a vast manufacturing ecosystem, a large domestic consumer base, and a strong presence in automotive, electronics, healthcare, and packaging industries. Demand for TPE films and sheets continues to increase due to expanding production of medical devices, consumer goods, and electric vehicles. Ongoing investments in specialty polymers and advanced manufacturing technologies further strengthen China's market position.

India TPE Films and Sheets Market Trends

India represents the fastest-growing major market in the region, accounting for approximately 17.1% of Asia Pacific demand. Rapid healthcare expansion, industrial development, urbanization, and rising disposable incomes are driving increased consumption of TPE materials. Growing investments in medical device manufacturing, flexible packaging, and automotive production are creating significant opportunities for TPE film and sheet suppliers. Government initiatives supporting domestic manufacturing are also contributing to market growth.

Japan TPE Films and Sheets Market Trends

Japan maintains a strong position in the market through its expertise in advanced materials, precision manufacturing, and high-quality industrial production. Demand for TPE films and sheets is supported by automotive innovation, medical technologies, and premium consumer products. Japanese manufacturers continue to focus on high-performance specialty materials that offer enhanced durability and functionality.

Competitive Landscape

The global TPE films and sheets market exhibits a moderately fragmented competitive structure characterized by the presence of multinational chemical companies, specialized thermoplastic elastomer producers, and regional film converters. Competition is based primarily on material performance, regulatory compliance capabilities, product innovation, technical support, and manufacturing scale.

Leading companies are pursuing strategies centered on product innovation, regional manufacturing expansion, sustainability, and healthcare specialization. Investment in medical-grade materials, specialty TPU technologies, recyclable formulations, and technical service capabilities remains a key priority. Strategic acquisitions, partnerships, and localized production networks continue to support competitive differentiation and long-term growth.

Key Industry Developments:

- In August 2025, Covestro AG completed the acquisition of Pontacol, integrating the company's multilayer adhesive film technologies and specialized production facilities in Switzerland and Germany to enhance its global specialty films business and support growth in high-performance film applications.

- In September 2025, Lubrizol Corporation introduced next-generation ESTANE® TPU specialty materials for films, adhesives, and cable applications, expanding its portfolio of high-performance thermoplastic polyurethane solutions designed to meet increasingly stringent durability, flexibility, and regulatory requirements.

Companies Covered in TPE Films and Sheets Market

- BASF SE

- Covestro AG

- Lubrizol Corporation

- Kraton Corporation

- HEXPOL TPE

- Kuraray Co., Ltd.

- Teknor Apex Company

- RTP Company

- Avient Corporation

- Huntsman Corporation

- DuPont de Nemours, Inc.

- 3M Company

- American Polyfilm, Inc.

- Mitsui Chemicals, Inc.

- Dynasol Group

- Celanese Corporation

Frequently Asked Questions

The global TPE films and sheets market is estimated to be valued at US$3.7 billion in 2026.

The TPE films and sheets market is projected to reach US$5.6 billion by 2033.

Key trends include the growing adoption of medical-grade TPE materials, increasing demand for lightweight and recyclable films, expansion of TPU-based specialty films, and rising investments in regional manufacturing and sustainable material solutions.

Styrenic Block Copolymers (SBC) are the leading material segment, anticipated to account for 31.2% of the market share due to their cost-effectiveness, flexibility, and widespread use in hygiene and healthcare applications.

The TPE films and sheets market is expected to grow at a CAGR of 6.2% between 2026 and 2033.

Major companies include BASF SE, Covestro AG, Lubrizol Corporation, DuPont de Nemours, Inc., and Kraton Corporation.